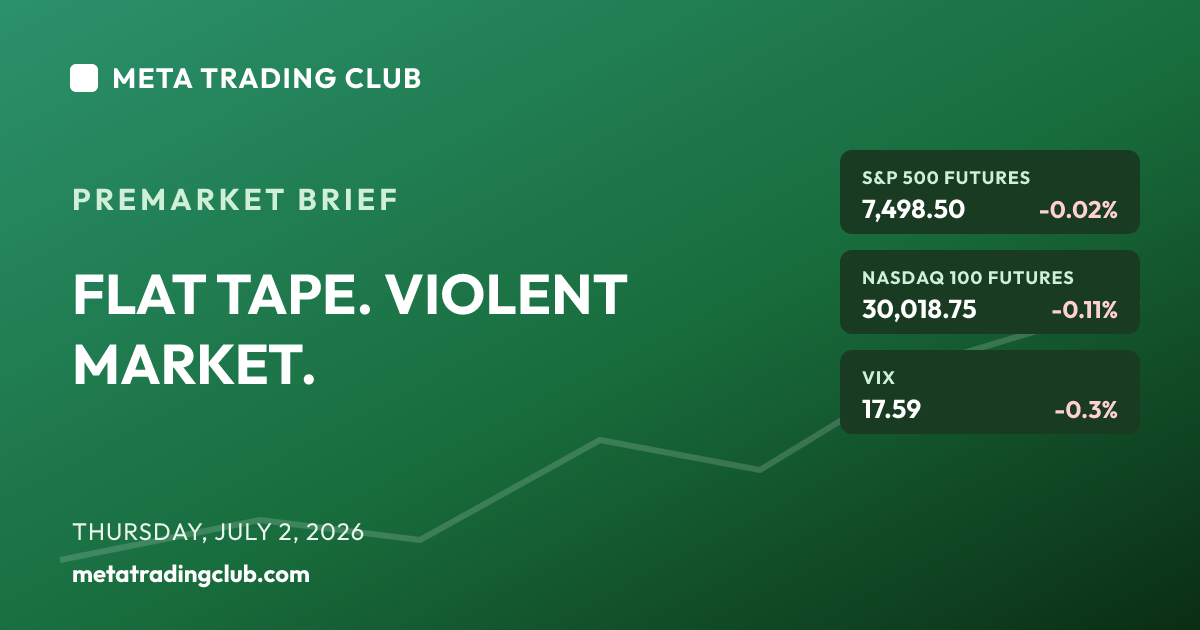

Thursday, July 2, 2026 · 8:45 AM ET · MTC Market Intelligence

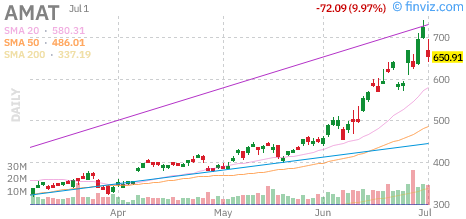

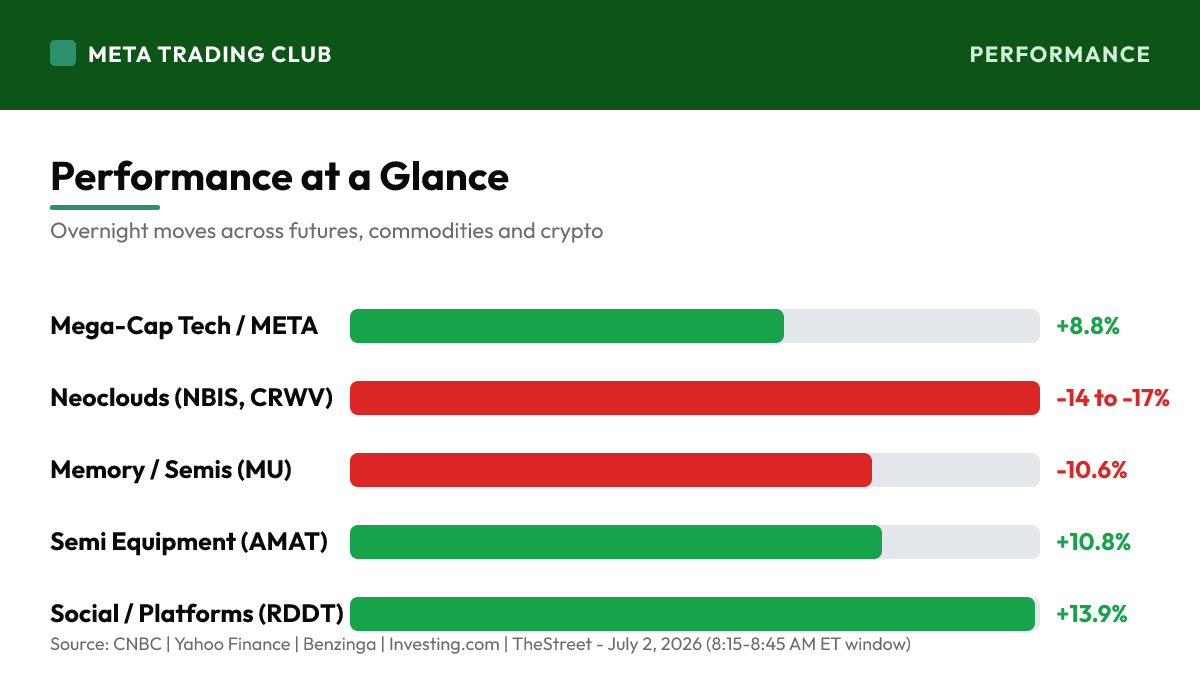

Jobs day meets an AI repricing — and the index is hiding both. Wednesday’s close looked like nothing: the Dow eased 0.03% to 52,305.24 after touching another record intraday, the S&P 500 slipped 0.22% to 7,483.23, and the Nasdaq fell 0.66% to 26,040.03. Underneath, the tape was violent. Bloomberg reported Meta plans ‘Meta Compute’ — selling its excess AI cloud capacity to outside developers — and the market repriced an entire sector in a day: META jumped 8.8% to $612.91, while the neoclouds it now threatens got crushed — Nebius -17% to $229.18, CoreWeave -13.9% to $85.69. Micron dropped 10.6% to $1,032.28 as traders took profit on a stock still up over 260% this year, and Reddit ripped 13.9% to $197.76 on 500M weekly users and 17% DAU growth. This morning the story is the June jobs report, pulled forward to today’s 8:30 AM release ahead of Friday’s July 4 closure. Consensus looked for roughly 110-115K jobs and a 4.3% unemployment rate after Wednesday’s soft 98K ADP print — and the first reaction in futures is telling: essentially flat, with S&P futures -0.02% at 7,498.50, Nasdaq-100 -0.11%, Dow -0.03% and Russell -0.17% approaching the open. No shock in either direction. The rate backdrop is the tension: new Fed Chair Kevin Warsh said ‘prices are too high’ at Sintra, the 10-year pushed up near 4.48%, and the market’s fear has flipped from cuts-delayed to hike-possible — which means a hot jobs number is a threat, not a gift. Cross-asset: VIX 17.59 and easing, WTI trading 67.59-68.16 and pressing below yesterday’s four-month low as Iran talks stall without escalation, Bitcoin soft at $58.4K (-1.8%), gold off 0.4% at $4,023. Premarket, AMAT is up nearly 11% at $694.64 as Susquehanna ($900), Cantor ($850) and KeyBanc ($750) hike targets on AI equipment spend — the equipment layer catching the bid the memory layer just lost. The read: a flat index over a violent tape is rotation, not calm. Let the market digest the jobs print, let SPX prove it can reclaim 7,500 or hold 7,440, and trade the stocks that are actually moving — not the average that isn’t. No alignment, no trade.

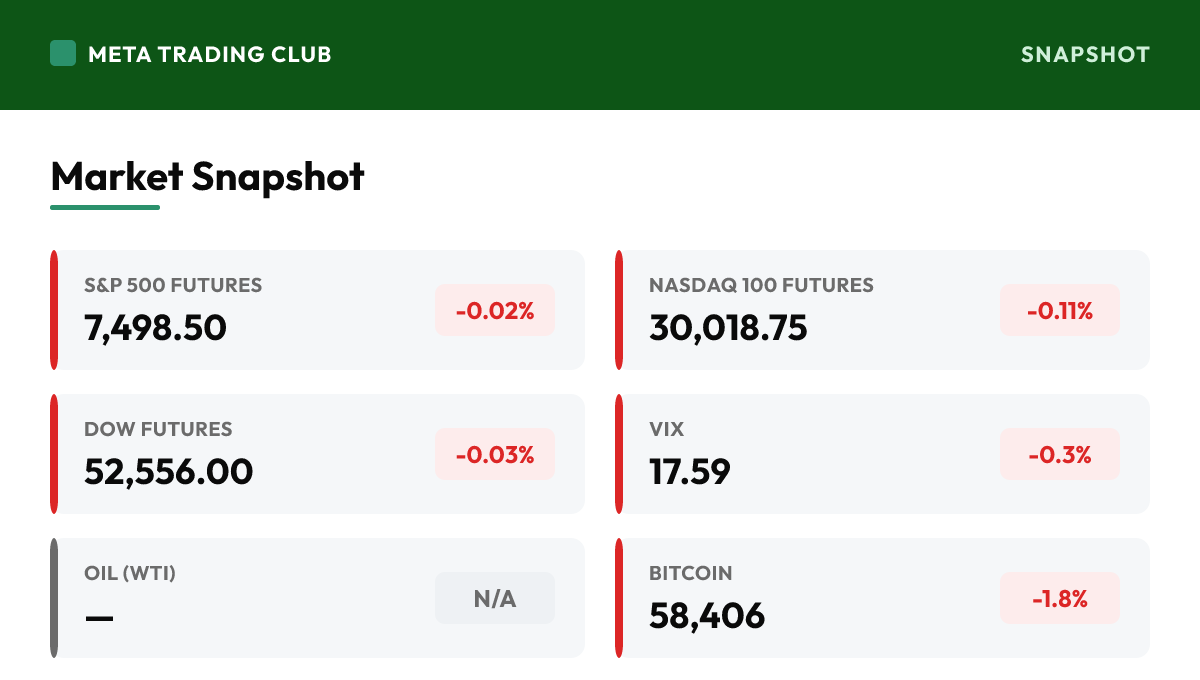

Market Snapshot

| Instrument | Level | Change | Note |

|---|---|---|---|

| S&P 500 Futures | 7,498.50 | -0.02% | Essentially flat through the 8:30 jobs release — no shock either way; sitting just under the record zone, and the first hour decides whether 7,500 gets reclaimed or becomes the ceiling |

| Nasdaq 100 Futures | 30,018.75 | -0.11% | Mildly softer after Wednesday’s chip-led slide; the AI complex is repricing internally — equipment names catching bids while memory and neoclouds digest — rather than rolling over as a group |

| Dow Futures | 52,556.00 | -0.03% | Flat after Wednesday’s record intraday touch and near-flat close at 52,305.24; the blue-chip tape remains the calmest corner of a market that is anything but calm underneath |

| Russell 2000 Futures | 3,025.30 | -0.17% | Small caps lag slightly into the jobs print; they are the most rate-sensitive corner of the tape, so the bond market’s read on the number matters more here than anywhere else |

| VIX | 17.59 | -0.3% | Easing slightly after rising through Wednesday’s rotation; low-17s says the market expected this jobs print to be manageable — a push back above 18-20 would say it was wrong |

| 10-Yr Yield | 4.48% | — | Pushed up near 4.48% into the release after Warsh’s ‘prices are too high’ line at Sintra; with the market now pricing hike risk rather than cut timing, a hot jobs number is a threat to equities, not a gift |

| Oil (WTI) | — | N/A | Trading a 67.59-68.16 range this morning, pressing below yesterday’s four-month-low close near $68.77 as Iran declines U.S. talks without fresh escalation; the war premium keeps draining out |

| Bitcoin | 58,406 | -1.8% | Soft at $58.4K and not confirming any risk appetite; crypto has now lagged this tape for a week — treat it as a mild caution flag on conviction behind the highs |

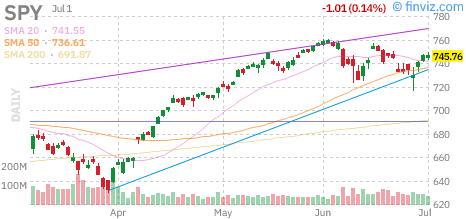

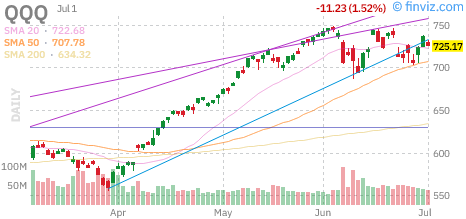

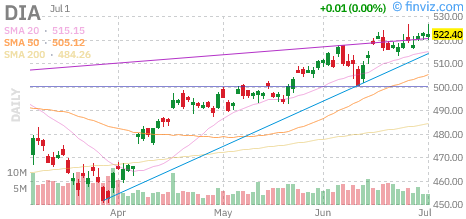

Charts to Watch

Daily candle charts with moving averages for the index proxies and today’s standout mover. Source: Finviz.

Performance at a Glance

Overnight & Global Markets

Read Wednesday properly, because the index number lies. The Dow eased 0.03% to 52,305.24 after another record intraday touch, the S&P 500 slipped 0.22% to 7,483.23, and the Nasdaq fell 0.66% to 26,040.03 — a nothing day on the surface. Underneath, one Bloomberg headline repriced a sector: Meta plans ‘Meta Compute,’ an internal push to sell excess AI cloud capacity to external developers. META jumped 8.8% to $612.91. The neoclouds it just turned from customer into competitor got hammered — Nebius fell 17% to $229.18, CoreWeave dropped 13.9% to $85.69 — because the deeper problem isn’t just competition, it’s concentration: Nebius carries a $27B Meta deal, CoreWeave a $21B agreement. When your biggest customer becomes your biggest rival, the multiple changes. Micron slid 10.6% to $1,032.28 — not on bad news, its CEO reiterated memory demand exceeding expectations and supply constrained beyond 2027 — but because a 260%+ year-to-date winner gives ambitious holders a reason to ring the register at the first sign of sector turbulence. Meanwhile Reddit gained 13.9% to $197.76 on 500M weekly users and 17% DAU growth. This morning adds the macro layer: the June jobs report, pulled forward to 8:30 AM today ahead of Friday’s July 4 market closure, landed against consensus of roughly 110-115K jobs and 4.3% unemployment after Wednesday’s soft 98K ADP. The tell so far is the reaction, not the number: futures held essentially flat through the release — S&P -0.02% at 7,498.50, Nasdaq-100 -0.11%, Dow -0.03% — which says no shock in either direction. The stakes are inverted from last year: Warsh told Sintra ‘prices are too high,’ the 10-year pushed toward 4.48%, and the market is debating a possible hike, not the timing of cuts. That makes labor-market strength a rates problem and labor-market softness a growth problem — the window for ‘good news’ is narrow. Premarket, AMAT is up nearly 11% at $694.64 on a wave of target hikes (Susquehanna $900, Cantor $850, KeyBanc $750) tied to AI equipment spend growing 30%+ this year. The read: this is rotation inside a bull tape, not distribution — until the levels say otherwise. Let SPX reclaim 7,500 or defend 7,440, and trade the names that are actually moving rather than the average that isn’t.

MAJOR HEADLINES AND CATALYSTS

Top Premarket Stories

- The June jobs report landed at 8:30 AM today — pulled forward ahead of Friday’s July 4 closure. Consensus looked for roughly 110-115K jobs and a 4.3% unemployment rate after Wednesday’s soft 98K ADP print. The first reaction in futures is the tell: essentially flat, no shock in either direction.

- Meta repriced a sector overnight. Bloomberg reported ‘Meta Compute’ — Meta selling excess AI cloud capacity to external developers. META +8.8% to $612.91; the neoclouds it threatens got crushed: Nebius -17% (holds a $27B Meta deal), CoreWeave -13.9% (a $21B agreement). Customer concentration just became the story.

- Micron fell 10.6% to $1,032.28 on no bad news — the CEO reiterated AI memory demand above expectations and supply constrained beyond 2027. A 260%+ YTD winner giving back 10% on sector turbulence is profit-taking mechanics, not a broken thesis. Watch whether dip buyers defend it today.

- AMAT is the premarket winner, up nearly 11% at $694.64 as Susquehanna ($900), Cantor Fitzgerald ($850) and KeyBanc ($750) hike targets on AI equipment spend growing 30%+ in 2026. Capital is rotating down the AI stack — from memory and neoclouds into the equipment layer — not out of AI.

Macro and the Week Ahead

- The rate regime is inverted from last year and that changes how to read today’s jobs number. Warsh told Sintra ‘prices are too high,’ the 10-year pushed near 4.48%, and the debate is about a possible hike — not cut timing. Labor strength is now a rates problem; labor softness is a growth problem. The good-news window is narrow.

- Markets are closed tomorrow, Friday July 3, for Independence Day. Today is the last session of the week — expect positioning to compress into the afternoon and treat late-day moves on thinning volume with suspicion. Jobless claims also print today alongside the payrolls data.

Global and Geopolitical

- Oil keeps bleeding: WTI is trading a 67.59-68.16 range this morning, pressing below yesterday’s four-month-low area near $68.77, as Iran declines U.S. talks in Qatar without fresh escalation. Falling crude with stalled talks says the market has stopped pricing a supply shock — risk-friendly, but a headwind for energy names.

- Bitcoin is soft at $58.4K (-1.8%) and gold eased 0.4% to $4,023. Crypto has lagged this equity tape for a week now — when the speculative end of the risk curve won’t confirm record-zone equities, log it as a caution flag on conviction, not a reason to short.

TECHNICAL ANALYSIS

S&P 500 Key Levels

- SPX closed Wednesday at 7,483.23, just under the ~7,500 record zone it set to close Q2. Futures sit at 7,498.50 — parked right at the decision point. Today’s question is binary: reclaim and hold 7,500 on the jobs reaction, or reject it and test the shelf below. Don’t front-run the answer.

- Resistance: the ~7,500 record zone, then 7,550 above. Support: 7,440 (the prior breakout shelf), then 7,400. Two closes under 7,440 would flip the second-half read from digestion to correction; holding it keeps every pullback a buyable rotation.

- Bias: constructive but two-sided into a jobs print and a holiday. A flat index over violent single-stock moves is rotation — bullish structure — but rotation tapes punish index traders and reward stock pickers. Trade the names with real catalysts, anchor risk to 7,440, and let 7,500 prove itself.

Sector and Sentiment

- The AI stack is repricing internally, not deflating: money left memory (MU -10.6%) and neoclouds (NBIS -17%, CRWV -13.9%) and showed up in the platform with excess capacity (META +8.8%) and the equipment layer (AMAT +10.8% premarket). That’s a food chain re-ranking, not an AI exit.

- VIX 17.59 and easing into the print says the options market expected a manageable number. It rose through Wednesday’s rotation, so the floor is higher than last week’s mid-16s — a push above 18-20 today would say the calm read on jobs was wrong.

- Breadth check: Russell futures lag (-0.17%) and Bitcoin won’t confirm (-1.8%). The record zone is being defended by a narrowing group of large caps with idiosyncratic catalysts. That can persist — but it means index-level conviction should stay smaller than single-name conviction.

TODAY’S ECONOMIC CALENDAR

Key Releases (ET)

- 8:30 AM — June nonfarm payrolls (pulled forward from Friday) plus weekly jobless claims. Consensus: ~110-115K jobs, 4.3% unemployment, wages +0.3% m/m. The confirmed print was not yet published in our data window — but the futures reaction through 8:45 was flat, which says the market read it as no-shock.

- The bond market is the judge today, not the stock market. With the 10-year near 4.48% and Warsh talking hike risk, watch yields’ reaction to the payrolls detail (wages and revisions especially). Yields spiking through 4.5% would pressure the record zone regardless of the headline jobs number.

- Last session before the July 4 closure — markets are shut tomorrow. Expect volume to thin into the afternoon; moves after lunch on light tape deserve less trust, not more. Position for the close by midday or don’t position at all.

Earnings Today

- No confirmed tape-moving earnings in today’s holiday-shortened calendar — the overnight movers were all story-driven: META (cloud push), NBIS/CRWV (competitive repricing), MU (profit-taking after its report cycle), RDDT (user growth), AMAT (analyst targets).

- The next real earnings catalyst wave is Q2 season starting mid-July with the banks. Until then, this market trades on macro prints, Fed speak and AI-stack headlines — exactly what today delivers.

PREMARKET PLAYBOOK

Key Levels

- SPX 7,500 — the record zone and today’s decision point. Futures are parked at 7,498.50 into the open. A reclaim-and-hold on the jobs reaction keeps the breakout alive; a rejection here with yields rising turns 7,500 into resistance and says wait.

- SPX 7,440 — the prior breakout shelf and the risk anchor. Rotation stays buyable while 7,440 holds; losing it — especially on a hot-wages, hawkish-yields reaction — flips the tape to sell-the-rip and opens 7,400.

- 10-Yr 4.50% and VIX 18 — the confirmation pair. Yields staying under 4.5% and VIX under 18 say the jobs print was absorbed; either breaking through says the flat futures reaction was wrong and the repricing goes macro.

Bull case: The jobs print stays in the no-shock zone, yields hold under 4.5%, and the flat futures tape resolves higher as SPX reclaims 7,500 with the AI rotation broadening — AMAT’s equipment bid spreading, dip buyers defending Micron, META holding its gap. VIX slides back toward 17 into the holiday and the record zone converts from ceiling to floor before the long weekend.

Bear case: Wage detail or revisions run hot, the 10-year pushes through 4.5% as Warsh’s hike risk gets real pricing, and SPX rejects 7,500 then loses 7,440 on thinning pre-holiday volume. The neocloud damage spreads up the stack, Micron’s dip finds no buyers, and a narrow, Bitcoin-unconfirmed record zone gives back the quarter-end run into the close.

What We’re Watching

- The 7,500 test — futures sit exactly at the record zone into the open. Reclaim-and-hold on the jobs reaction is the green light; rejection plus rising yields is the wait signal. This one level answers most of today’s questions.

- The bond market’s verdict — 10-year through 4.5% would pressure equities regardless of the headline jobs number. Watch wages and revisions, not just the payroll count. In a hike-risk regime, strong data is the threat.

- The rotation’s next move — whether AMAT’s equipment bid holds its gap, whether Micron gets defended, and whether META consolidates above $600. If the AI stack finishes re-ranking without index damage, the record run survives the week.

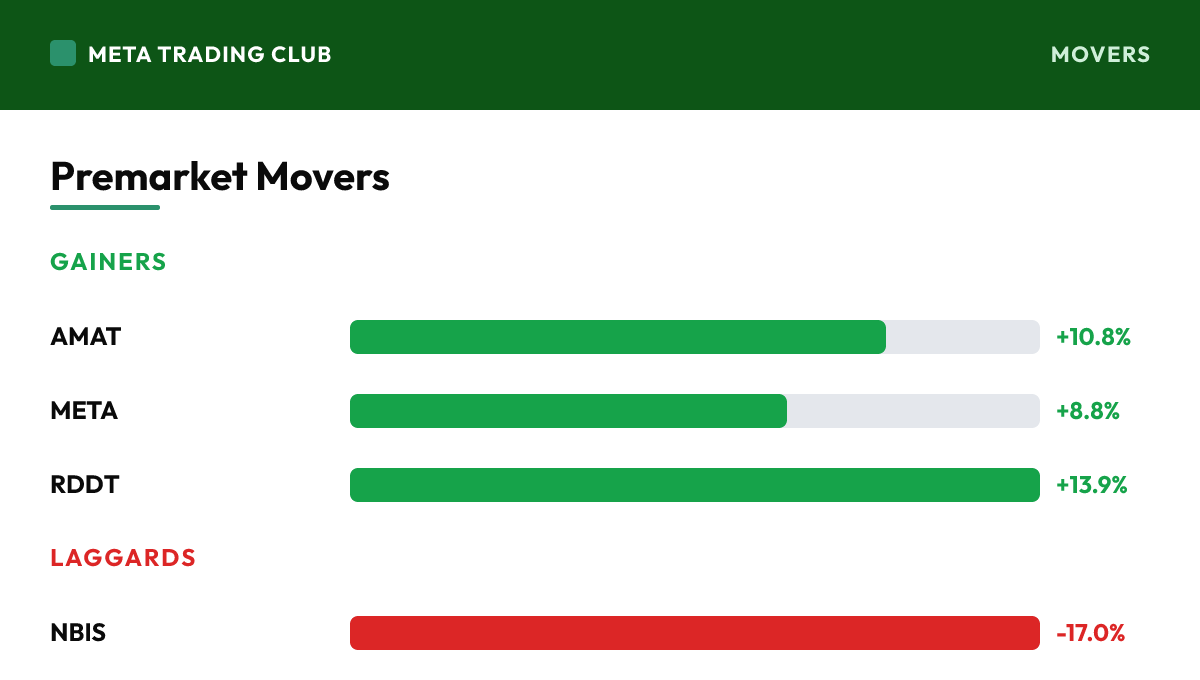

Premarket Movers

Gainers

| AMAT | Applied Materials | +10.8% | Near $694.64 premarket as Susquehanna ($900), Cantor Fitzgerald ($850) and KeyBanc ($750) hike targets on 30%+ AI equipment growth — the equipment layer catching the bid the memory layer just lost |

| META | Meta Platforms | +8.8% | Closed at $612.91 on the ‘Meta Compute’ report — selling excess AI cloud capacity to external developers adds a new revenue narrative and repriced the entire AI infrastructure stack in a day |

| RDDT | +13.9% | Closed at $197.76 on 500M weekly users and 17% DAU growth — a clean reminder that user-growth stories still get paid in this tape |

Laggards

| NBIS | Nebius Group | -17.0% | Closed at $229.18 as Meta turns from $27B anchor customer into potential competitor; the sharpest casualty of the Meta Compute repricing |

| CRWV | CoreWeave | -13.9% | Closed at $85.69 on the same customer-concentration logic — a $21B Meta agreement now cuts both ways |

| MU | Micron | -10.6% | Closed at $1,032.28 on profit-taking after a 260%+ YTD run — the CEO’s demand outlook didn’t change, the holders’ patience did |

Risks Into the Open

- Primary risk: trading the index in a rotation tape. The S&P moved 0.22% Wednesday while single names moved 9-17%. Index-level positions carry all of the chop and none of the edge right now — size single-name conviction around real catalysts and keep index exposure honest to the 7,440 anchor.

- Secondary risk: misreading the jobs number’s sign. In a hike-risk regime with Warsh saying ‘prices are too high,’ a hot print is bearish for the record zone and a soft print cuts both ways. Watch the 10-year’s reaction, not the headline — the bond market grades this exam.

- Constructive: this is rotation inside a bull structure, not distribution. Money moved down the AI stack (into equipment, out of memory and neoclouds), the VIX is easing, oil is calm at four-month lows, and futures absorbed the jobs release flat. The setup for the record zone to hold is intact — let 7,500 confirm it.

Frequently Asked Questions

Where are S&P 500 futures trading ahead of the open?

Ahead of Thursday, July 2, 2026, S&P 500 futures are at 7,498.50 (-0.02%), with the VIX near 17.59. Jobs day meets an AI repricing — and the index is hiding both. Wednesday’s close looked like nothing: the Dow eased 0.03% to 52,305.24 after touching another record intraday, the S&P 500 slipped 0.22% to 7,483.23, and the Nasdaq fell 0.66% to 26,040.03. Underneath, the tape was violent. Bloomberg reported Meta plans ‘Meta Compute’ — selling its excess AI cloud capacity to outside developers — and the market repriced an entire sector in a day: META jumped 8.8% to $612.91, while the neoclouds it now threatens got crushed — Nebius -17% to $229.18, CoreWeave -13.9% to $85.69. Micron dropped 10.6% to $1,032.28 as traders took profit on a stock still up over 260% this year, and Reddit ripped 13.9% to $197.76 on 500M weekly users and 17% DAU growth. This morning the story is the June jobs report, pulled forward to today’s 8:30 AM release ahead of Friday’s July 4 closure. Consensus looked for roughly 110-115K jobs and a 4.3% unemployment rate after Wednesday’s soft 98K ADP print — and the first reaction in futures is telling: essentially flat, with S&P futures -0.02% at 7,498.50, Nasdaq-100 -0.11%, Dow -0.03% and Russell -0.17% approaching the open. No shock in either direction. The rate backdrop is the tension: new Fed Chair Kevin Warsh said ‘prices are too high’ at Sintra, the 10-year pushed up near 4.48%, and the market’s fear has flipped from cuts-delayed to hike-possible — which means a hot jobs number is a threat, not a gift. Cross-asset: VIX 17.59 and easing, WTI trading 67.59-68.16 and pressing below yesterday’s four-month low as Iran talks stall without escalation, Bitcoin soft at $58.4K (-1.8%), gold off 0.4% at $4,023. Premarket, AMAT is up nearly 11% at $694.64 as Susquehanna ($900), Cantor ($850) and KeyBanc ($750) hike targets on AI equipment spend — the equipment layer catching the bid the memory layer just lost. The read: a flat index over a violent tape is rotation, not calm. Let the market digest the jobs print, let SPX prove it can reclaim 7,500 or hold 7,440, and trade the stocks that are actually moving — not the average that isn’t. No alignment, no trade.

What is the biggest catalyst for the market today?

The June jobs report landed at 8:30 AM today — pulled forward ahead of Friday’s July 4 closure. Consensus looked for roughly 110-115K jobs and a 4.3% unemployment rate after Wednesday’s soft 98K ADP print. The first reaction in futures is the tell: essentially flat, no shock in either direction.

What key levels should traders watch today?

SPX 7,500 — the record zone and today’s decision point. Futures are parked at 7,498.50 into the open. A reclaim-and-hold on the jobs reaction keeps the breakout alive; a rejection here with yields rising turns 7,500 into resistance and says wait. SPX 7,440 — the prior breakout shelf and the risk anchor. Rotation stays buyable while 7,440 holds; losing it — especially on a hot-wages, hawkish-yields reaction — flips the tape to sell-the-rip and opens 7,400. 10-Yr 4.50% and VIX 18 — the confirmation pair. Yields staying under 4.5% and VIX under 18 say the jobs print was absorbed; either breaking through says the flat futures reaction was wrong and the repricing goes macro.

How does Meta Trading Club approach the market open?

We qualify every setup through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

Trade the next session with us live. Start your 7-day free trial →

Trade with a system, not signals.

This is exactly how MTC members read the open — bias, level, reaction, confirmation, execution. If you want to learn to qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process.

Apply for the Incubator → Learn moreSources: CNBC | Yahoo Finance | Benzinga | Investing.com | TheStreet – July 2, 2026 (8:15-8:45 AM ET window). For educational purposes only. Not financial advice.