Wednesday, July 1, 2026 · 8:45 AM ET · MTC Market Intelligence

Wall Street opens the second half sitting on the best quarter since 2020 — and this morning is the hangover check. Q2 closed Tuesday with the Dow’s second straight record close at 52,319.20 (+0.26%, +136), the S&P 500 up 0.79% and the Nasdaq Composite up 1.52%, capping a first half where the Dow ran +8.9% (best H1 since 2021), the S&P +9.6% and the Nasdaq +12.8%. Now the tape cools: S&P 500 futures -0.2%, Nasdaq-100 futures -0.4%, Dow futures -0.2% (about 105 points). That pullback isn’t a warning — it’s digestion after a historic run, exactly what you’d expect as Q3 opens and funds stop marking up books. The cross-asset read leans cautious: the VIX ticks up ~1.4% toward 16.7 as buyers step back, the 10-year sits firm near 4.38% with new Fed Chair Kevin Warsh speaking at the ECB’s Sintra forum, WTI drops 1.1% to $68.77 — a four-month low — after Iran said it won’t meet U.S. delegates in Qatar and peace talks stalled, and Bitcoin is flat near $58.3K. The data flipped soft early: June ADP private payrolls rose just 98,000, below expectations and down from 122,000 in May, ahead of ISM manufacturing and Thursday’s pulled-forward jobs report (markets close Friday for July 4). Stock-specific, the lesson of the morning is Nike: it ‘beat’ with $0.72 EPS on $10.97B revenue, but strip the one-time $0.52 tariff-refund benefit and it earned $0.20, Greater China fell 12%, and the stock is down ~3.6% near $39.58. SpaceX (SPCX) is the bright spot, +2% to $174.32 on a Wedbush Outperform initiation ($190 target). Translation for traders: a record quarter feels like a green light, but futures cooling, a soft ADP, and a Nike ‘beat’ that wasn’t all say the same thing — read the details, not the headline, and let price hold the highs after the open before you trust the next leg. No alignment, no trade.

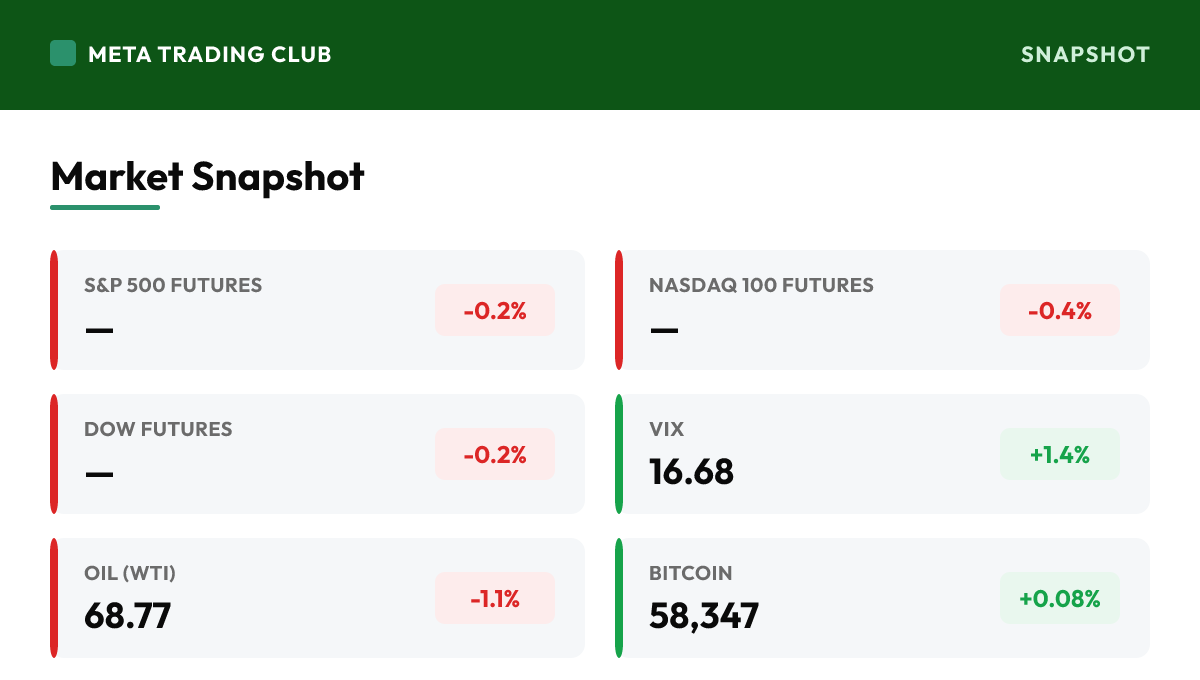

Market Snapshot

| Instrument | Level | Change | Note |

|---|---|---|---|

| S&P 500 Futures | — | -0.2% | Easing back after Tuesday’s record-setting quarter close; a modest pullback to open Q3 is digestion, not distribution — let price hold the highs before trusting the next leg up |

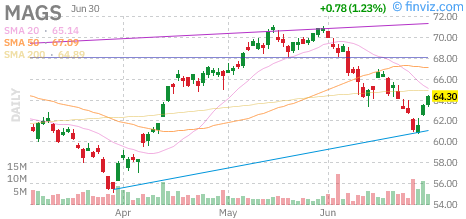

| Nasdaq 100 Futures | — | -0.4% | Leading the cool-down as tech takes a breather after a +12.8% first half; the Mag7 that carried the run is pausing, and MAGS is only +0.16% premarket — watch whether leadership stays intact |

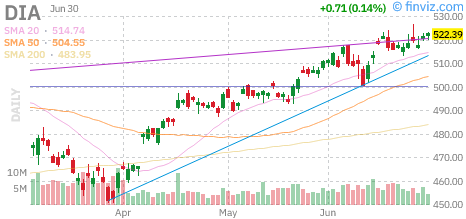

| Dow Futures | — | -0.2% | Off about 105 points after a second straight record close at 52,319.20; giving a little back after a +8.9% first half (best since 2021) is normal quarter-flip behavior, not a top signal |

| Russell 2000 Futures | — | N/A | Small-cap futures not confirmed in-window; breadth remains the thing to watch — a record run led only by mega-caps needs the small caps to join to be durable |

| VIX | 16.68 | +1.4% | Ticking up off the mid-16s as buyers step back into the quarter flip; low fear is still the backdrop, but a VIX creeping higher into a thin holiday week is the market asking for confirmation |

| 10-Yr Yield | 4.38% | — | Firm near 4.38% with new Fed Chair Warsh on the wire at Sintra; sticky yields cap how far a melt-up runs, so a hawkish tone or a rate jump would change this tape’s character fast |

| Oil (WTI) | 68.77 | -1.1% | Dropping to a four-month low as Iran declines U.S. talks in Qatar and the war premium keeps bleeding out; calm-to-falling crude is risk-friendly, but it also pressures energy names like XOM and CVX |

| Bitcoin | 58,347 | +0.08% | Flat near $58.3K and not leading the tone; when crypto won’t confirm a record-setting equity backdrop, treat it as a small caution flag rather than a green light |

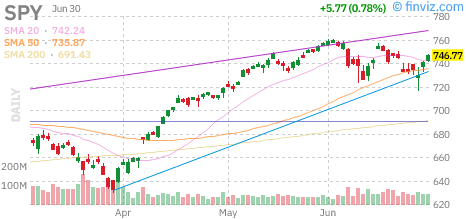

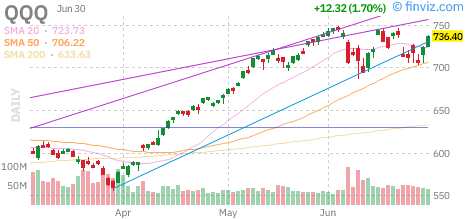

Charts to Watch

Daily candle charts with moving averages for the index proxies and today’s standout mover. Source: Finviz.

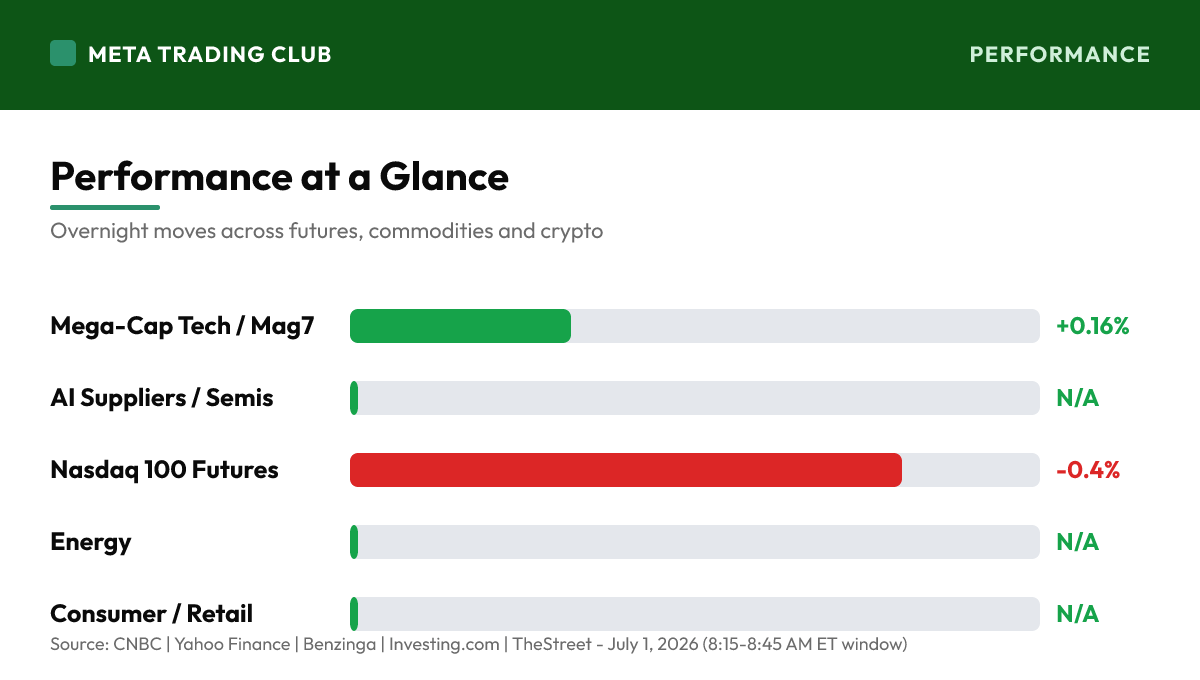

Performance at a Glance

Overnight & Global Markets

This is a digestion morning after a historic run, and the distinction matters. Q2 closed Tuesday as the best quarter since 2020: the Dow logged its second straight record close at 52,319.20 (+0.26%), the S&P 500 rose 0.79% and the Nasdaq Composite jumped 1.52%, sealing a first half of +8.9% on the Dow (best since 2021), +9.6% on the S&P and +12.8% on the Nasdaq. This morning the tape cools: S&P futures -0.2%, Nasdaq-100 -0.4%, Dow -0.2% (about 105 points). After a run like that, a soft open is the pause you expect on the calendar flip — funds stop marking up books and the crowd that chased the highs into quarter-end has no fresh catalyst to keep pressing. The data leaned soft early: June ADP private payrolls came in at just 98,000, below expectations and down from 122,000 in May, with ISM manufacturing and Thursday’s pulled-forward June jobs report still ahead in a week that closes Friday for July 4. The cross-asset backdrop is cautious but not broken: the VIX is up ~1.4% toward 16.7 as buyers step back, the 10-year is firm near 4.38% with new Chair Kevin Warsh speaking at the ECB’s Sintra forum, and WTI is down 1.1% to a four-month low near $68.77 after Iran declined U.S. talks in Qatar. The morning’s cleanest lesson is Nike: the headline was a beat — $0.72 EPS on $10.97B revenue — but $0.52 of that EPS was a one-time tariff-refund benefit, so the real number was $0.20, Greater China revenue fell 12%, and the stock is down ~3.6% near $39.58. That is the whole game in one print: the number that moves price is the one they bury, not the one in the headline. The read: respect the record quarter, don’t chase the open. A pullback into Q3 needs price to hold the highs and the data to firm before it earns fresh size. A great quarter can be marked up; only the next sessions confirm whether the strength was real or just positioning.

MAJOR HEADLINES AND CATALYSTS

Top Premarket Stories

- Wall Street opens Q3 on the best quarter since 2020. Tuesday closed Q2 with the Dow’s second straight record close (52,319.20, +0.26%), the S&P 500 up 0.79% and the Nasdaq Composite up 1.52% — capping a first half of +8.9% (Dow, best since 2021), +9.6% (S&P) and +12.8% (Nasdaq).

- This morning is digestion, not extension. Futures cool as Q3 begins — S&P -0.2%, Nasdaq-100 -0.4%, Dow -0.2% (about 105 points). After a historic run, a soft open on the calendar flip is a pause, exactly what you’d expect once quarter-end markups stop and the crowd that chased the highs has no fresh catalyst.

- Nike is the lesson of the morning. It ‘beat’ with $0.72 EPS on $10.97B revenue, but $0.52 was a one-time IEEPA tariff-refund benefit — strip it and EPS was $0.20, Greater China fell 12%, and the stock is down ~3.6% near $39.58. The number that moves price is the one they bury, not the headline.

- The data leaned soft early: June ADP private payrolls rose just 98,000, below expectations and down from 122,000 in May, with weakness concentrated in leisure and hospitality. It sets a cautious tone into ISM manufacturing today and Thursday’s pulled-forward June jobs report.

Macro and the Week Ahead

- Holiday-shortened, data-heavy week: markets close Friday for July 4, the June jobs report is pulled to Thursday, and today brings ADP (98K, a miss), ISM manufacturing, construction spending and EIA petroleum data. Fewer, thinner sessions mean moves can over-extend in both directions.

- Rates are the governor and the Fed is the swing. The 10-year sits firm near 4.38% as new Chair Kevin Warsh speaks at the ECB’s Sintra forum; any signal on the rate path matters more than any single data point on a thin summer session. Sticky yields cap how far a melt-up can run.

Global and Geopolitical

- Oil is the confirmation signal and it’s falling. WTI is down 1.1% to a four-month low near $68.77 after Iran said it won’t meet U.S. delegates in Qatar and peace talks stalled. Falling crude with talks faltering says the market no longer fears a supply shock — the war premium keeps bleeding out.

- Bitcoin is the laggard, flat near $58.3K and not confirming the record-quarter backdrop. When crypto won’t lead a risk-on tape, note it as a small caution flag rather than read it as conviction behind the highs.

TECHNICAL ANALYSIS

S&P 500 Key Levels

- The S&P closed Q2 at a fresh record near 7,500 after Tuesday’s +0.79% gain. With futures pointing -0.2%, the open sits just below the highs, and the question isn’t whether it dips — it’s whether the record zone holds as support. A record that can’t hold on the first session of a new quarter is a fade signal, not a launch.

- Resistance: the ~7,500 record area, then the round 7,500-7,550 zone above. Support: 7,440 (the prior breakout shelf), then 7,400. Holding 7,440 keeps the second-half uptrend intact; losing it opens a deeper digestion of the quarter-end run.

- Bias: constructive but extended. A record into a soft, holiday-shortened week is the setup that over-extends, then gives some back. Let SPX prove it can hold the record zone and build on 7,440 before trusting a new leg — don’t pay up to chase a run that’s already booked its best quarter in years.

Sector and Sentiment

- Leadership is rotating and that’s the tell. Cramer’s read — Wall Street rewarding AI suppliers (MU, INTC, MRVL, AMD, SNDK) over the Mag7 that fund the buildout — matters after the Mag7 shed ~$2.3T in June. Watch whether chips carry Q3 or whether the whole complex just digests.

- The VIX near 16.7 and up ~1.4% says fear is low but creeping back as buyers step aside on the quarter flip. That’s the right backdrop for records to hold — but a VIX pushing back above 18-20 into a thin week would warn the calm is fading.

- Respect the calendar twice over: a soft ADP and a pulled-forward jobs report compress the week’s catalysts, and a holiday-shortened session thins liquidity. Don’t confuse a low-volume drift with real demand — wait for volume and follow-through before trusting the record holds.

TODAY’S ECONOMIC CALENDAR

Key Releases (ET)

- June ADP private payrolls already printed soft at +98,000 (below expectations, down from 122,000 in May), with nearly half the gains in education and health services and leisure/hospitality weak for a sixth straight month. It’s the early tell into Thursday’s official jobs report.

- Still ahead: ISM manufacturing PMI, the final June S&P Global manufacturing PMI, construction spending and EIA petroleum inventories. Watch ISM for the demand pulse — a soft print stacked on a weak ADP would temper the record optimism; a firm read would say the rally has fundamental legs.

- The bigger event is Fed Chair Kevin Warsh at the ECB’s Sintra forum. On a thin, quarter-flip session, any signal on the rate path carries more weight than the data. After the open, let the tape confirm whether the record quarter carries into Q3 or fades.

Earnings Today

- The overnight headliner is Nike — a beat on paper ($0.72 EPS / $10.97B revenue) that was really $0.20 once you strip a one-time $0.52 tariff-refund benefit, with Greater China down 12% and the stock off ~3.6% near $39.58. A clean reminder that guidance and detail, not the headline number, move the stock.

- Today’s calendar brings General Mills (GIS, ~$0.80 EPS / ~$4.60B), FactSet (FDS, ~$4.45 EPS), MSC Industrial (MSM, ~$1.26), UniFirst (UNF, ~$1.91) and Greenbrier (GBX, ~$0.59). None is a tape-mover on its own, but the read-through on the consumer and industrials is worth watching into the holiday.

PREMARKET PLAYBOOK

Key Levels

- SPX ~7,500 — Tuesday’s record area and the line in the sand. The second-half uptrend is real only while price holds the record zone after the open. A record that fades back through it on the first session of Q3 is a failed breakout, not a launch — anchor risk around it today.

- SPX 7,440 — the prior breakout shelf and first real support. As long as 7,440 holds, the quarter-end run stays intact; lose it and the whole record push comes into question, with 7,400 the next line below.

- VIX 16-18 and oil sub-$70 — the confirmation pair. A VIX staying near 16-17 and crude holding below $70 says the risk premium is gone and records can hold; a VIX spiking above 18-20 would warn the calm is cracking into the thin week. Let them confirm the tone.

Bull case: The pullback is shallow, SPX holds the record zone and rebuilds above 7,440, and the AI-supplier rotation keeps the tape moving even as the Mag7 rests. A calm VIX near 16-17 plus oil below $70 confirm the geopolitical risk is gone, ISM firms up to offset the soft ADP, and Warsh strikes a balanced tone — turning the best quarter since 2020 into follow-through buying, not a one-quarter peak.

Bear case: The record fades on thin holiday volume, SPX slips back under 7,440, the soft ADP is confirmed by a weak ISM and a cautious Warsh, and the Mag7 that shed $2.3T in June can’t find a bid as rotation fails to carry the tape. Add Nike’s turnaround worries and a sticky 10-year above 4.4%, and Q3 opens with a sell-the-strength session that hands back part of the quarter-end run.

What We’re Watching

- The record hold — whether SPX stays in the ~7,500 zone and above 7,440 after the open or fades back through them. Holding keeps the second-half uptrend alive; losing 7,440 flips the read to failed breakout and sell-the-rip.

- Rotation and breadth — whether AI suppliers and semis carry the tape while the Mag7 rests, and whether small caps join. A broadening, rotating market is durable; a narrow run that stalls when the mega-caps pause is fragile.

- ISM, oil and Warsh — a firm ISM offsets the soft ADP, oil below $70 confirms the risk premium is gone, and Warsh’s tone sets the rate path. A weak ISM plus a hawkish Fed would say the record quarter’s momentum is fading.

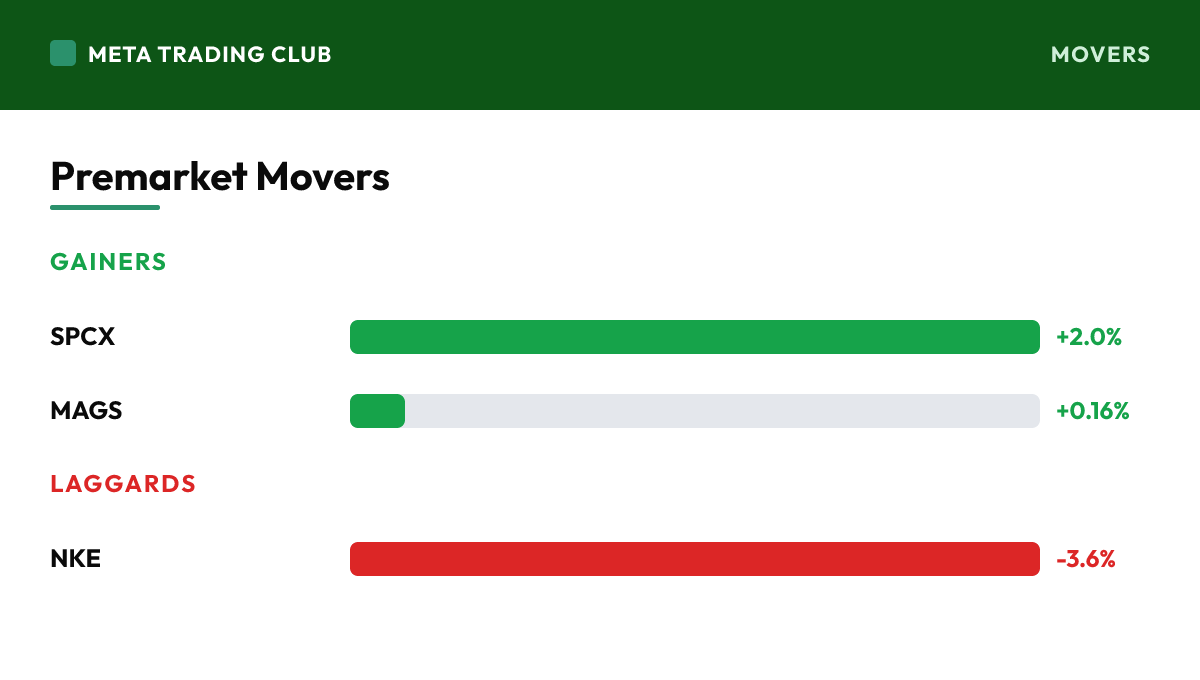

Premarket Movers

Gainers

| SPCX | SpaceX | +2.0% | Up to $174.32 premarket after Wedbush initiated coverage with an Outperform rating and a $190 target; a rare clean bid in an otherwise cooling tape |

| MAGS | Roundhill Magnificent Seven ETF | +0.16% | Barely green at $64.41 as the Mag7 rests after shedding ~$2.3T in June; strength is intact but reflexive — watch whether leadership holds past the open |

Laggards

| NKE | Nike | -3.6% | Down near $39.58 despite a headline beat; strip the one-time $0.52 tariff-refund benefit and EPS was $0.20, with Greater China -12% and a tough FY27 start — the detail, not the number, is the story |

Risks Into the Open

- Primary risk: chasing the record quarter. The best quarter since 2020 is already booked; buying the open into a soft ADP and cooling futures before price holds the highs is paying up for a run that’s already run. Let the next sessions prove the strength was real, not just quarter-end positioning.

- Secondary risk: reading headlines, not details. Nike ‘beat’ and still dropped ~3.6% once you stripped a one-time benefit and saw China down 12%. Into earnings season and a thin week, the number in the headline is not the number that moves the stock — do the work before you trade the print.

- Constructive: the backdrop still supports the highs. Fear is low (VIX ~16.7), oil is calm at a four-month low, the AI-supplier rotation is keeping the tape alive, and the geopolitical premium keeps bleeding out. The setup for records to hold is right — let breadth broaden and price hold the levels to confirm it.

Frequently Asked Questions

Where are S&P 500 futures trading ahead of the open?

Ahead of Wednesday, July 1, 2026, S&P 500 futures are at — (-0.2%), with the VIX near 16.68. Wall Street opens the second half sitting on the best quarter since 2020 — and this morning is the hangover check. Q2 closed Tuesday with the Dow’s second straight record close at 52,319.20 (+0.26%, +136), the S&P 500 up 0.79% and the Nasdaq Composite up 1.52%, capping a first half where the Dow ran +8.9% (best H1 since 2021), the S&P +9.6% and the Nasdaq +12.8%. Now the tape cools: S&P 500 futures -0.2%, Nasdaq-100 futures -0.4%, Dow futures -0.2% (about 105 points). That pullback isn’t a warning — it’s digestion after a historic run, exactly what you’d expect as Q3 opens and funds stop marking up books. The cross-asset read leans cautious: the VIX ticks up ~1.4% toward 16.7 as buyers step back, the 10-year sits firm near 4.38% with new Fed Chair Kevin Warsh speaking at the ECB’s Sintra forum, WTI drops 1.1% to $68.77 — a four-month low — after Iran said it won’t meet U.S. delegates in Qatar and peace talks stalled, and Bitcoin is flat near $58.3K. The data flipped soft early: June ADP private payrolls rose just 98,000, below expectations and down from 122,000 in May, ahead of ISM manufacturing and Thursday’s pulled-forward jobs report (markets close Friday for July 4). Stock-specific, the lesson of the morning is Nike: it ‘beat’ with $0.72 EPS on $10.97B revenue, but strip the one-time $0.52 tariff-refund benefit and it earned $0.20, Greater China fell 12%, and the stock is down ~3.6% near $39.58. SpaceX (SPCX) is the bright spot, +2% to $174.32 on a Wedbush Outperform initiation ($190 target). Translation for traders: a record quarter feels like a green light, but futures cooling, a soft ADP, and a Nike ‘beat’ that wasn’t all say the same thing — read the details, not the headline, and let price hold the highs after the open before you trust the next leg. No alignment, no trade.

What is the biggest catalyst for the market today?

Wall Street opens Q3 on the best quarter since 2020. Tuesday closed Q2 with the Dow’s second straight record close (52,319.20, +0.26%), the S&P 500 up 0.79% and the Nasdaq Composite up 1.52% — capping a first half of +8.9% (Dow, best since 2021), +9.6% (S&P) and +12.8% (Nasdaq).

What key levels should traders watch today?

SPX ~7,500 — Tuesday’s record area and the line in the sand. The second-half uptrend is real only while price holds the record zone after the open. A record that fades back through it on the first session of Q3 is a failed breakout, not a launch — anchor risk around it today. SPX 7,440 — the prior breakout shelf and first real support. As long as 7,440 holds, the quarter-end run stays intact; lose it and the whole record push comes into question, with 7,400 the next line below. VIX 16-18 and oil sub-$70 — the confirmation pair. A VIX staying near 16-17 and crude holding below $70 says the risk premium is gone and records can hold; a VIX spiking above 18-20 would warn the calm is cracking into the thin week. Let them confirm the tone.

How does Meta Trading Club approach the market open?

We qualify every setup through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

Trade with a system, not signals.

This is exactly how MTC members read the open — bias, level, reaction, confirmation, execution. If you want to learn to qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process.

Apply for the Incubator → Learn moreSources: CNBC | Yahoo Finance | Benzinga | Investing.com | TheStreet – July 1, 2026 (8:15-8:45 AM ET window). For educational purposes only. Not financial advice.