Tuesday, June 30, 2026 · 4:30 PM ET · MTC Market Close

The bounce got its confirmation. Monday’s relief rally was narrow — led by the beaten-down mega-caps while the chip complex still leaked — and the honest read was that you couldn’t trust the turn until the semis stopped bleeding. Tuesday they didn’t just stop; they ripped to the front. AMD jumped 7.7%, Intel rose 6%, Nvidia added 2.6%, and the SMH semiconductor ETF climbed about 3% to push its year-to-date gain to roughly 82%. That chip leadership carried the tape into quarter-end: the Nasdaq Composite climbed 1.52% to 26,213.72, the S&P 500 rose 0.79% to 7,499.36 — closing right at the 7,500 round number — and the Dow added 136.46 points to a fresh record 52,319.20. With that, Wall Street wrapped its best quarter since 2020: the S&P gained roughly 13.5% on the quarter and 9.6% on the first half, the Nasdaq advanced more than 12% in H1, and the Dow’s 8.9% first-half climb was its best since 2021. But the cross-asset tape carried a quieter warning under the green. Gold slipped to about $4,007 and Bitcoin broke below $60,000 for the first time since 2024 as the quarter closed — both classic risk-appetite tells that didn’t confirm the equity euphoria. The macro stayed calm: the VIX held under 18, the 10-year sat near 4.37% at multi-week lows, and WTI firmed to $70.91. The data was mixed — Chicago PMI tumbled to 56.7 from 62.7, while Consumer Confidence and JOLTS came in around forecast. After the close, Nike headlined a light earnings slate: a headline EPS beat ($0.72 vs ~$0.13) flattered by a $0.52 tariff-refund benefit, but a 12% drop in Greater China sales sent shares down as much as 8% after hours before they pared. Constellation Brands beat cleanly. The trader’s read into the new half: chips rejoining leadership broadens the rally and earns the bounce real benefit of the doubt — but it’s quarter-end, window-dressing can flatter the tape, and the first session of Q3 is exactly where a flattered close gets re-tested. Watch whether the S&P holds 7,500. No alignment, no trade.

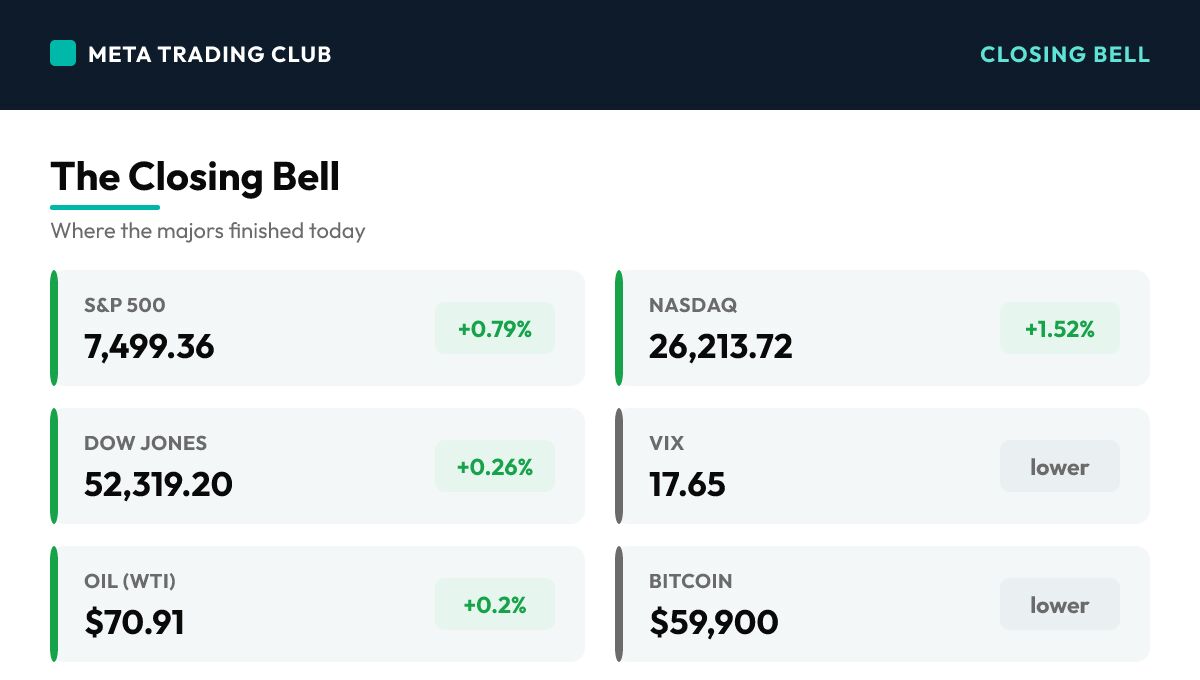

The Closing Bell

| Instrument | Close | Change | Note |

|---|---|---|---|

| S&P 500 | 7,499.36 | +0.79% | Closed right at the 7,500 round number as the chip complex rejoined leadership; the index capped its best quarter since 2020, up roughly 13.5% on the quarter |

| Nasdaq | 26,213.72 | +1.52% | Led the majors as semiconductors ripped — AMD +7.7%, Intel +6%, Nvidia +2.6% — pushing the index more than 12% higher on the first half |

| Dow Jones | 52,319.20 | +0.26% | Added 136.46 points to a fresh record close, its second straight all-time high; up 8.9% in H1, the Dow’s best first half since 2021 |

| Russell 2000 | — | flat | Roughly flat into the quarter-end close as the small-cap complex sat out the chip-led, large-cap-driven advance |

| VIX | 17.65 | lower | Held under 18 near multi-week lows — the fear gauge stayed subdued through the risk-on, quarter-end tape as chips led the bid |

| 10-Yr Yield | 4.37% | flat | Sat near 4.37% at multi-week lows — rates stayed calm and capped, giving the chip-led rally clean air into the close |

| Gold | $4,007.20 | -0.2% | Slipped toward $4,000, briefly dipping under it intraday for the first time since November — the metal eased on the risk-on, calm-rates tape |

| Oil (WTI) | $70.91 | +0.2% | Firmed modestly, holding near pre-war levels as the geopolitical premium stayed drained following the weekend de-escalation |

| Bitcoin | $59,900 | lower | Broke below $60,000 for the first time since 2024 as Q2 closed — crypto sat out the equity rally, a quiet risk-appetite divergence to respect |

Today’s Charts

Daily candlestick charts with 20/50/200-day moving averages — the index majors, the day’s biggest mover on each side, and the leading sector ETF.

Charts: Finviz (daily). Levels and overlays update through the next session.

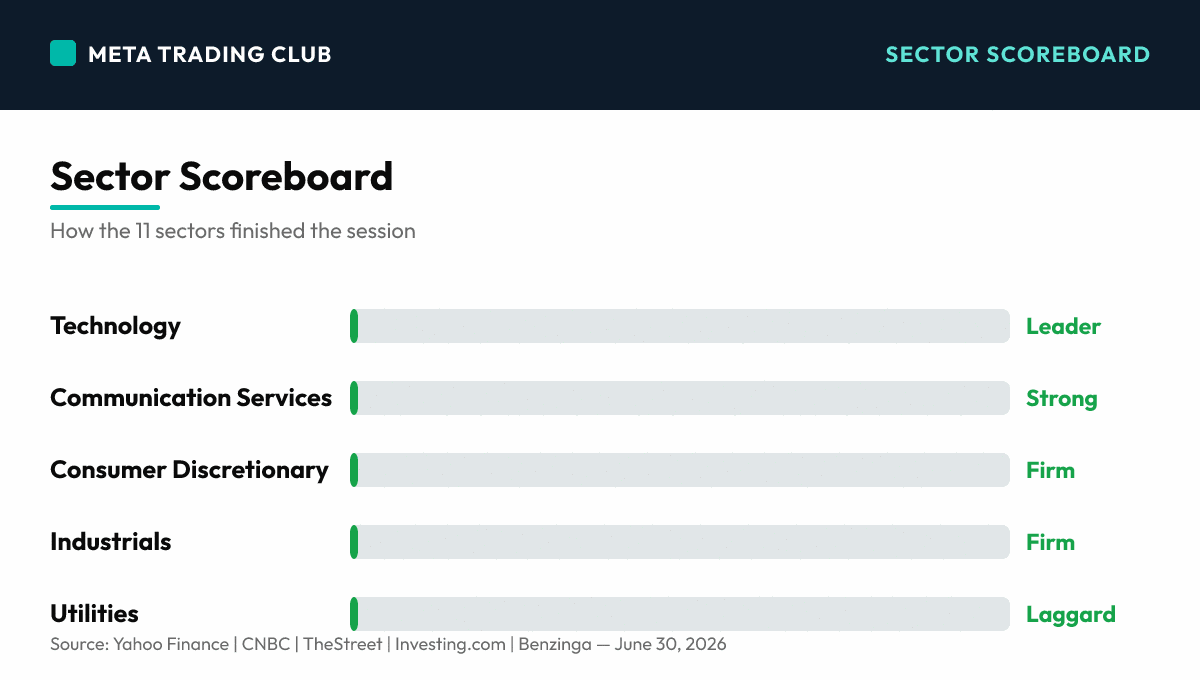

Sector Scoreboard

What Drove The Day

Tuesday was the session that gave Monday’s bounce its missing piece. The relief rally to start the week was narrow — the beaten-down mega-caps mean-reverted hard while the semiconductor complex kept leaking, and the disciplined read was that the rebound couldn’t be trusted until the chips stopped bleeding. They did more than stop. The group that led last week’s selloff ripped straight to the front: AMD jumped about 7.7%, Intel rose about 6%, Nvidia added 2.6%, and the SMH semiconductor ETF climbed roughly 3%, lifting its year-to-date gain to around 82%. That leadership powered the Nasdaq Composite up 1.52% to 26,213.72 and carried the S&P 500 up 0.79% to 7,499.36 — closing right at the 7,500 round number — while the Dow tacked on 136.46 points to a record 52,319.20, its second consecutive all-time high. The timing mattered: Tuesday closed the quarter and the first half, and the books were strong. The S&P finished the quarter up roughly 13.5%, its best since 2020, and gained 9.6% on the half; the Nasdaq advanced more than 12% in H1; and the Dow’s 8.9% first-half climb was its best since 2021. The macro confirmed the calm: the VIX held under 18 near multi-week lows, the 10-year sat near 4.37%, and WTI firmed to $70.91. The economic data was a split read — Chicago PMI tumbled to 56.7 from 62.7, a sharp cooling, while June Consumer Confidence and May JOLTS landed near forecast and didn’t disturb the tape. But the honest trader notes what didn’t confirm. Gold slipped to about $4,007, briefly trading under $4,000 intraday, and Bitcoin broke below $60,000 for the first time since 2024 as the quarter closed. On a day equities rallied into record territory, two of the market’s cleaner risk-appetite gauges quietly leaked — not a red flag on its own, but a divergence worth respecting. After the bell, Nike headlined a light slate: fiscal Q4 revenue of about $10.97B beat the ~$10.86B estimate and EPS of $0.72 crushed the ~$0.13 consensus, but the beat was flattered by a $0.52 benefit tied to expected IEEPA tariff refunds, and a 12% drop in Greater China sales sent shares down as much as 8% after hours before they pared much of the loss. Constellation Brands beat more cleanly, posting $3.43 EPS on $2.43B revenue. The read into the new half is constructive but not complacent: chips rejoining leadership broadens the rally and earns the bounce genuine benefit of the doubt — but quarter-end window-dressing can flatter a tape, and the first session of Q3 is precisely where a flattered close gets re-tested. The level to watch is 7,500. Hold it and the second half opens with momentum; lose it and Tuesday’s record print looks like a quarter-end mark. No alignment, no trade.

MAJOR HEADLINES AND CATALYSTS

Top Market-Moving Stories

- CHIPS RIP BACK TO LEAD AS WALL STREET CAPS BEST QUARTER SINCE 2020 (Day) — The semiconductor complex that leaked through last week’s selloff and lagged Monday’s bounce roared to the front: AMD +7.7%, Intel +6%, Nvidia +2.6%, SMH +3% (YTD ~82%). That leadership lifted the Nasdaq 1.52% to 26,213.72 and the S&P 0.79% to 7,499.36, closing the strongest quarter in six years.

- DOW PRINTS A SECOND STRAIGHT RECORD CLOSE AT 52,319 (Day) — The Dow added 136.46 points to a fresh all-time high of 52,319.20, its second consecutive record. It gained 8.9% in the first half — its best H1 since 2021 — as the chip-led, broadening rally carried the cyclicals along with tech.

- GOLD AND BITCOIN DON’T CONFIRM (Day) — As equities printed records, gold slipped to ~$4,007 (briefly under $4,000 intraday, first time since November) and Bitcoin broke below $60,000 for the first time since 2024. Two clean risk-appetite gauges quietly leaked on a euphoric equity day — a divergence to respect, not ignore.

Fed and Macro Context

- The data split — Chicago PMI tumbled to 56.7 in June from 62.7, a sharp cooling in the regional read, while June Consumer Confidence (~94 area) and May JOLTS job openings (~7.3M) landed near forecast and didn’t disturb the tape. The labor and confidence reads stayed steady even as the factory gauge softened.

- Volatility stayed asleep — the VIX held under 18 near multi-week lows and the 10-year sat calm at ~4.37%. With rates capped and the fear gauge subdued, the chip-led rally had clean air to run into the quarter-end close.

What Changed

- The chips confirmed — Monday’s bounce was narrow and the semis lagged, which is why the turn wasn’t trustworthy. Tuesday the group that led the selloff led the rally instead. That broadening is the single most important shift: it turns a positioning snap-back into something closer to a real risk-on move.

- But the close was a quarter-end mark — Tuesday wrapped Q2 and H1 with the best quarter since 2020, and window-dressing flows can flatter a tape on the last day. Pair that with gold and Bitcoin not confirming, and the record print earns benefit of the doubt but still needs to hold its level on the first day of the new half.

AFTER-HOURS EARNINGS SPOTLIGHT

Earnings Reported After 4:05 PM ET Today

- NIKE (NKE) — MIXED, SHARES WHIPSAWED — Fiscal Q4 revenue ~$10.97B beat the ~$10.86B estimate and EPS of $0.72 crushed the ~$0.13 consensus, but the beat was flattered by a $0.52 benefit tied to expected IEEPA tariff refunds. A 12% drop in Greater China sales sent shares down as much as 8% after hours before they pared much of the loss. The headline beat masked a tough setup into FY2027.

- CONSTELLATION BRANDS (STZ) — CLEAN BEAT — Posted $3.43 EPS versus the ~$3.21 estimate (a ~7% beat) on $2.43B revenue, ahead of the ~$2.39B Street number. A steadier print than Nike’s, with the beer portfolio carrying the quarter.

Regular Session Highlights — Day-Session Movers

- AMD +7.7% / INTC +6.0% / NVDA +2.6% (Day) — The chip complex led the entire market, with the SMH semis ETF up ~3% (YTD ~82%). The exact group that lagged Monday’s relief rally ripped to the front, broadening the advance into quarter-end.

- MSTR -5% (Day) — MicroStrategy, the leading bitcoin-treasury proxy, leaked as Bitcoin slipped below $60,000 for the first time since 2024. Crypto-linked names sat out the equity rally — a small but clean risk-appetite divergence on a record-setting day.

- Mega-cap growth rode along (Day) — the broadening rally pulled the large-cap growth complex higher alongside the chips, helping the Nasdaq to its 1.5% gain and the S&P right up to the 7,500 line.

NEXT SESSION SETUP — WEDNESDAY JULY 1, 2026

Key Calendar (ET)

- First day of Q3 / H2, and the jobs week starts — 8:15 AM ADP private payrolls and 10:00 AM ISM Manufacturing PMI (June) headline Wednesday. With the July 3 market holiday, the June jobs report is expected to be pulled forward to Thursday, July 2 — so this week’s labor read lands fast and matters.

- Watch Nike’s regular-session reaction — after the after-hours whipsaw, Wednesday’s cash open shows where the market actually settles on the tariff-flattered beat and the China weakness. The first session of a new quarter also tends to unwind any quarter-end window-dressing from Tuesday’s close.

Events and Risk

- Does the chip leadership hold? — Tuesday’s broadening came entirely from semis. A real second-half trend needs the group to follow through, not give it all back on day one. Watch whether SMH holds its breakout and the S&P defends 7,500 on the open.

- The cross-asset divergence — gold under ~$4,007 and Bitcoin below $60K say risk appetite isn’t as clean as the equity record implies. Layer ADP and ISM on top and Wednesday can move fast in both directions. Don’t pre-position into the data.

MTC Framework for Wednesday

- Higher timeframe bias: CONSTRUCTIVE BUT WATCHFUL — The chips confirmed the bounce, the S&P closed at 7,500, the Dow printed a record, and rates and the VIX are calm. That’s a genuinely improved tape. But it’s a quarter-end mark, and gold and Bitcoin didn’t confirm — so this is a trend earning the benefit of the doubt, not a green light to chase.

- Key level: S&P 500 7,500. The index closed right on the round number. Hold 7,500 as support on the open and the second half starts with momentum toward 7,550/7,600; lose it and Tuesday’s record print reads like a quarter-end mark, with 7,440 the first line below.

- Confirmation rule: Don’t chase the record into the new quarter. Let price hold 7,500 after the open and let ADP and ISM clear before you trust the second-half follow-through. No alignment, no trade.

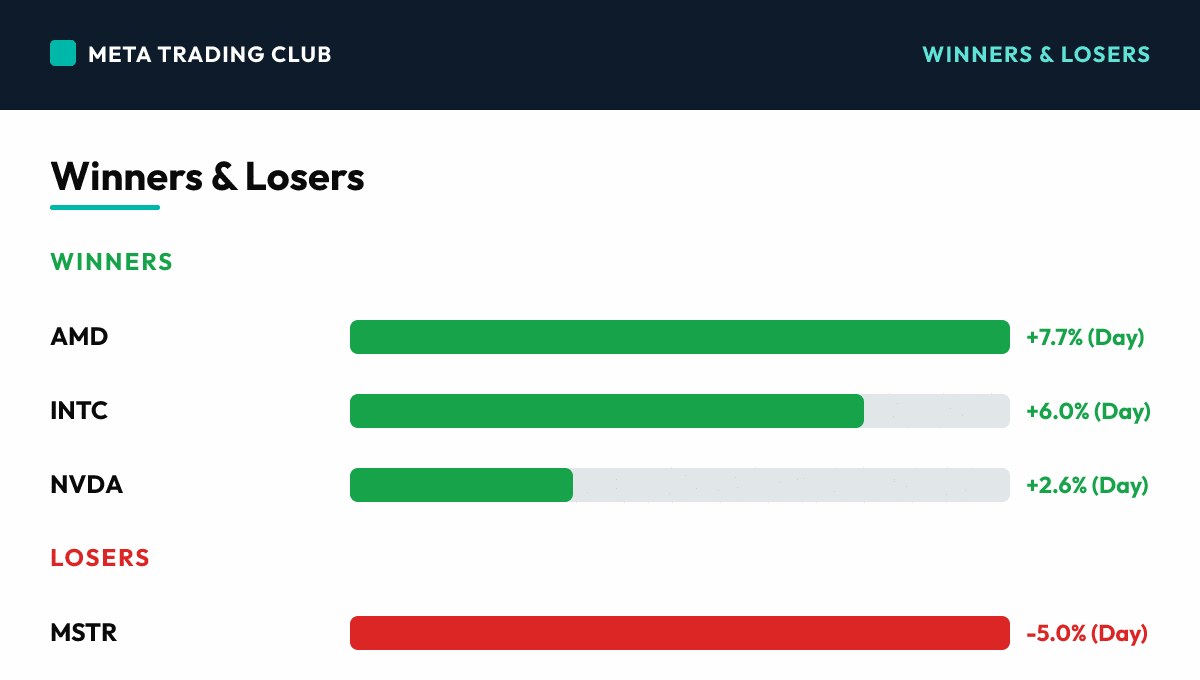

Winners & Losers

Winners

| AMD | Advanced Micro Devices | +7.7% (Day) | Day Session — led the chip complex’s roaring comeback, helping the SMH semis ETF jump ~3%; the exact group that lagged Monday’s relief rally ripped to the front of the tape |

| INTC | Intel | +6.0% (Day) | Day Session — joined the semiconductor surge as money rotated back into the beaten-down chip names that had leaked through last week’s selloff |

| NVDA | Nvidia | +2.6% (Day) | Day Session — the AI bellwether added to the chip-led advance, anchoring the Nasdaq’s 1.5% gain into the quarter-end close |

Losers

| MSTR | MicroStrategy | -5.0% (Day) | Day Session — the leading bitcoin-treasury proxy leaked as Bitcoin slipped below $60,000 for the first time since 2024; crypto-linked names sat out the equity rally on a record-setting day |

| NKE | Nike | AH | After Hours — fiscal Q4 EPS of $0.72 beat the ~$0.13 consensus but was flattered by a $0.52 IEEPA tariff-refund benefit; a 12% drop in Greater China sales sent shares down as much as 8% after the close before they pared the loss |

What It Sets Up For Tomorrow

Levels Into Tomorrow

- SPX 7,500 — The round number the index closed right on. Hold 7,500 as support on Wednesday’s open and the new half opens with momentum; this is the single cleanest tell for whether Tuesday’s record was a turn or a quarter-end mark.

- SPX 7,550 / 7,440 — Upside continuation targets the 7,550-7,600 zone; downside line is 7,440 (Monday’s close). Lose 7,500 and slip toward 7,440 and the record print looks like window-dressing, not trend.

- Jobs-week data — ADP at 8:15 AM and ISM Manufacturing at 10:00 AM Wednesday, with the June jobs report pulled forward to Thursday ahead of the July 3 holiday. Price action around the prints sets the H2 tone; don’t pre-position into the number.

Bull case: The bounce finally broadened. The chip complex that led last week’s selloff and lagged Monday’s relief rally ripped to the front — AMD +7.7%, Intel +6%, Nvidia +2.6%, SMH +3% — turning a narrow positioning snap-back into a genuine risk-on move. The S&P closed at 7,500, the Dow printed a second straight record, rates are calm at ~4.37% and the VIX is asleep under 18, and Wall Street capped its best quarter since 2020 with momentum into H2. If chips follow through and the S&P holds 7,500, the second half opens with a tailwind toward 7,550-7,600.

Bear case: Tuesday was the last day of the quarter, and window-dressing flows flatter a tape into the close — the first session of Q3 is exactly where that gets re-tested. The leadership was narrow and chip-concentrated, gold slipped under $4,007 and Bitcoin broke below $60,000 for the first time since 2024 — two risk-appetite gauges that didn’t confirm the equity record. Chicago PMI tumbled to 56.7. If the S&P fails to hold 7,500 on the open, or ADP/ISM disappoint, the index can give back the quarter-end mark and slide toward 7,440.

What We’re Watching

- Chip follow-through — does the semiconductor complex (AMD, Intel, Nvidia, SMH) hold Tuesday’s breakout, or give it back on the first day of the quarter? The broadening only counts if it sticks past the quarter-end mark.

- The 7,500 hold — does the S&P defend the round number on the open, or fade the record print? This is the cleanest single tell for whether Tuesday was a turn or a quarter-end mark.

- ADP + ISM into the jobs week — Wednesday’s labor and factory reads, with the June jobs report pulled forward to Thursday. As long as rates stay capped near 4.37% and the VIX stays under 18, the rally keeps room to run; watch gold and BTC for the risk-appetite tell.

Risks Into Tomorrow

- The Bounce Broadened — Respect It, Don’t Chase It — Monday’s rally was narrow; Tuesday the chips confirmed and led. That’s a real improvement that turns a positioning snap-back into a risk-on move. But it printed on the last day of the quarter, when window-dressing flatters the tape. Don’t fight the green, but let the S&P hold 7,500 on the first day of Q3 before you trust the follow-through.

- Gold and Bitcoin Didn’t Confirm — As equities printed records, gold slipped under $4,007 and Bitcoin broke below $60K for the first time since 2024. Two clean risk-appetite gauges quietly leaked on a euphoric equity day. It’s not a red flag on its own, but a cross-asset divergence into a new quarter is exactly the kind of tell disciplined traders log and watch.

- Earnings Flattered Is Still a Tell — Nike’s headline EPS beat ($0.72 vs ~$0.13) was driven by a $0.52 tariff-refund benefit, and China sales fell 12%. The market saw through it — shares dropped as much as 8% after hours. The lesson: read past the headline number to what actually drove it. The same discipline applies to a quarter-end record close.

Frequently Asked Questions

How did the S&P 500 close today?

On Tuesday, June 30, 2026, the S&P 500 closed at 7,499.36 (+0.79%), with the VIX at 17.65. The bounce got its confirmation.

What drove the market today?

CHIPS RIP BACK TO LEAD AS WALL STREET CAPS BEST QUARTER SINCE 2020 (Day) — The semiconductor complex that leaked through last week’s selloff and lagged Monday’s bounce roared to the front: AMD +7.7%, Intel +6%, Nvidia +2.6%, SMH +3% (YTD ~82%). That leadership lifted the Nasdaq 1.52% to 26,213.72 and the S&P 0.79% to 7,499.36, closing the strongest quarter in six years.

What levels matter for tomorrow?

SPX 7,500 — The round number the index closed right on. Hold 7,500 as support on Wednesday’s open and the new half opens with momentum; this is the single cleanest tell for whether Tuesday’s record was a turn or a quarter-end mark. SPX 7,550 / 7,440 — Upside continuation targets the 7,550-7,600 zone; downside line is 7,440 (Monday’s close). Lose 7,500 and slip toward 7,440 and the record print looks like window-dressing, not trend. Jobs-week data — ADP at 8:15 AM and ISM Manufacturing at 10:00 AM Wednesday, with the June jobs report pulled forward to Thursday ahead of the July 3 holiday. Price action around the prints sets the H2 tone; don’t pre-position into the number.

How does Meta Trading Club prepare for the next session?

We wrap every session and carry the read forward through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

New to this? Start with the free training.

Learn how we read the market before you risk a dollar — our free education library and ebook break down the fundamentals step by step.

Free education → Get the free ebookThe session’s over. The prep isn’t.

This is how MTC members close each day — wrap what happened, mark the levels, and carry one clean read into tomorrow. If you want to build that habit and qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process. It’s application-based — see if it’s a fit.

Explore the MTC Incubator → Apply nowSources: Yahoo Finance | CNBC | TheStreet | Investing.com | Benzinga — June 30, 2026. For educational purposes only. Not financial advice.