Everyone’s trying to pick the next Eli Lilly. Almost nobody’s buying the companies Lilly physically can’t ship a single injection without.

That’s the mistake — and this week the market handed us the cleanest proof of it all year.

AI stocks sold off hard on fears about the cost of building data centers. Money rotated out of crowded tech and into defensives. And while the front-page AI names dropped, one secular theme quietly kept compounding right through the chaos: the obesity-drug build-out. Its demand curve doesn’t care what hyperscaler capex does next quarter.

In every gold rush, the miners get the headlines. The people who quietly got rich sold the picks and shovels. An injectable GLP-1 isn’t just a molecule — it’s a peptide API, a glass cartridge, an elastomer seal, and a self-injection device, each made by a specialist with real pricing power. The crowd buys Lilly and Novo. The edge is in the verifiable supplier the crowd hasn’t crowded into yet.

Here are three names on our radar this week — each with a named, verifiable demand link back to the GLP-1 boom.

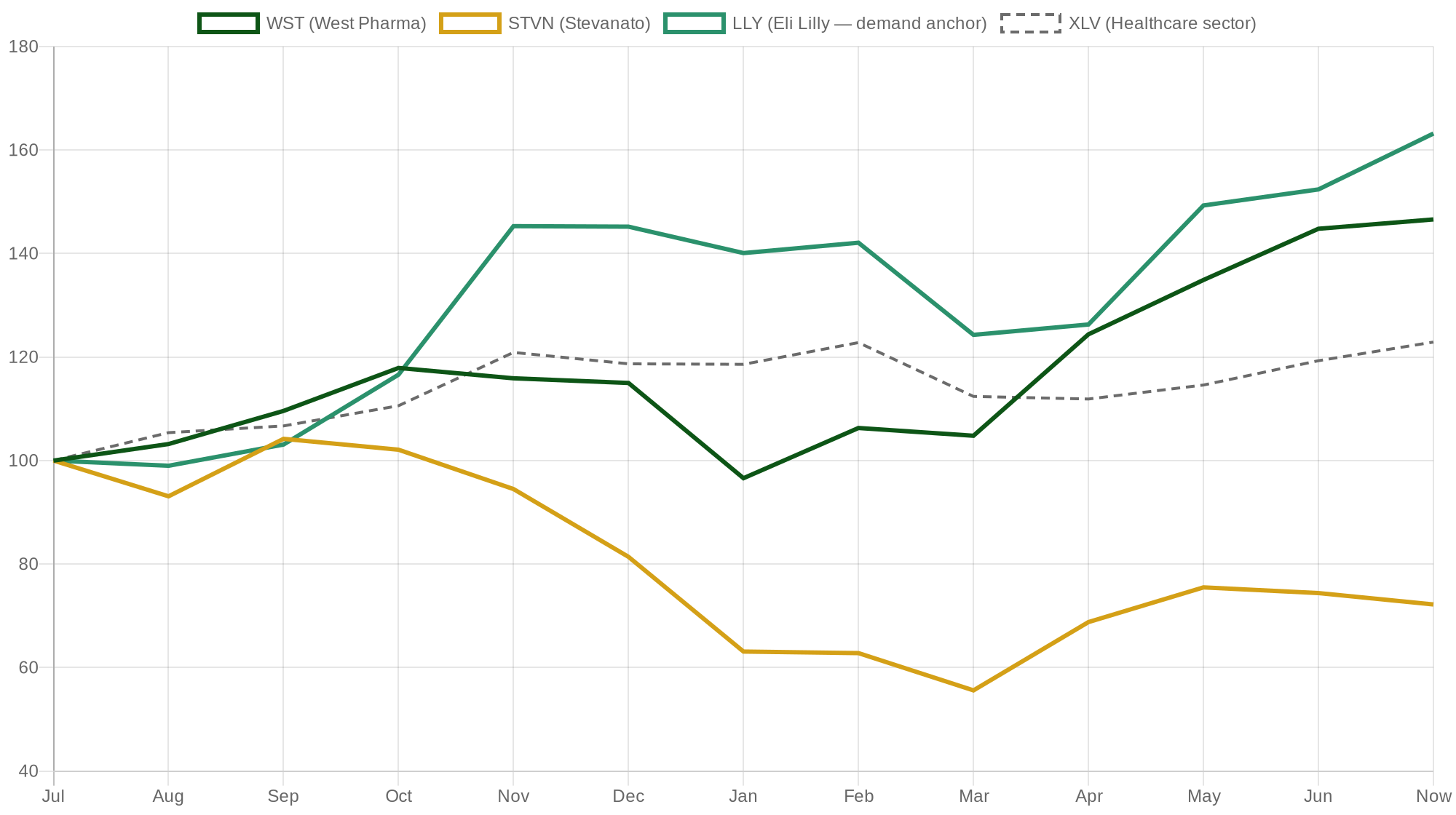

One year, indexed to 100. The suppliers track the demand anchor (Lilly) — with more room and less crowding. Stevanato is the beaten-down contrarian; West is re-rating to new highs.

Makes the elastomer closures, seals, and self-injection device platforms that go into injectable biologics — including every injectable GLP-1 pen and vial. The boring, high-margin containment layer the drug literally can’t ship without.

Italian maker of glass vials, cartridges, and pre-fillable syringes — plus the fill-finish and device-assembly lines that turn them into a finished pen. The contrarian name here: beaten down from $28 on a heavy capex ramp, not a demand problem.

The deepest layer: Bachem makes the molecule itself. It’s the leading peptide CDMO, producing commercial semaglutide and tirzepatide APIs via solid-phase peptide synthesis. When demand for GLP-1s scales, the peptide supply chain is the first physical bottleneck.

The demand anchor: Eli Lilly (LLY)

None of these suppliers matter without the demand pulling product through them. Lilly is that anchor — Mounjaro sales up ~125% and Zepbound up ~80% year-over-year in the latest quarter, with an oral pipeline that could widen the funnel further. We’re not chasing it here. The level we like is a pullback toward $1,100; the risk is US drug-pricing policy and oral-pill competition. But it’s the gravity that makes the whole supply chain investable.

We grade our own calls — including the losers

Last week we spotlighted four AI silent suppliers. This week, as the AI-capex trade unwound, all four gave back ground: Fabrinet (−6.3%), Credo (−8.5%), Modine (−8.6%), Astera (−2.1%). We’re not going to pretend otherwise. None of their contracted demand stories broke — what fell was the multiple the market was willing to pay. We’ve moved all four from Working to Watching.

Across all 24 priced picks, the book is averaging −2.7% with a 41.7% win rate this week — but the spread is the whole point. The conservative sleeve was +1.9% (JNJ +11.5%, healthcare led the rotation) while the aggressive AI sleeve was −7.4%. That’s risk tiers doing exactly what they’re built to do. No track record, no authority — so we publish the scorecard every week, winners and losers alike.

The lesson underneath the picks

This isn’t “go buy small caps.” It’s this: when the front-page trade gets repriced, the edge doesn’t disappear — it moves one layer down the supply chain. The market proved it twice this week. AI’s suppliers fell with AI. The GLP-1 suppliers kept compounding because their demand isn’t tied to the trade that broke.

Every name above passes the same four-part filter: it sells into the hot theme, it’s under-covered by retail, it has real pricing power, and it traces a verifiable demand link — a named customer, a contract, or a capex line. No link, no pick. That discipline is the difference between an insight and a hot take.

FAQ

What is a “silent supplier” in the GLP-1 space?

A company that sells a critical input into the obesity-drug build-out — the API, the glass, the seal, the injection device — but isn’t a front-page name like Lilly or Novo. Lower awareness, real pricing power, demand you can trace.

Won’t oral GLP-1 pills kill the injectable suppliers?

It’s the key risk, and we name it on every card. But roughly 70% of the market is still expected to stay injectable for now, and capacity is being reserved against named programs into 2026. Watch the oral-vs-injectable mix closely.

Is this financial advice?

No. This is educational research. Entry levels are analytical reference points, not solicitations. Do your own research and consult a licensed professional before investing.

Disclaimer: This article is for educational purposes only and is not financial, investment, tax, or legal advice. Meta Trading Club is not a registered investment adviser. Markets carry risk, including loss of principal. Entry levels are illustrative analytical reference points, not solicitations to buy or sell any security. Prices referenced are as of the close on June 26, 2026. Do your own research and consult a licensed professional before investing.