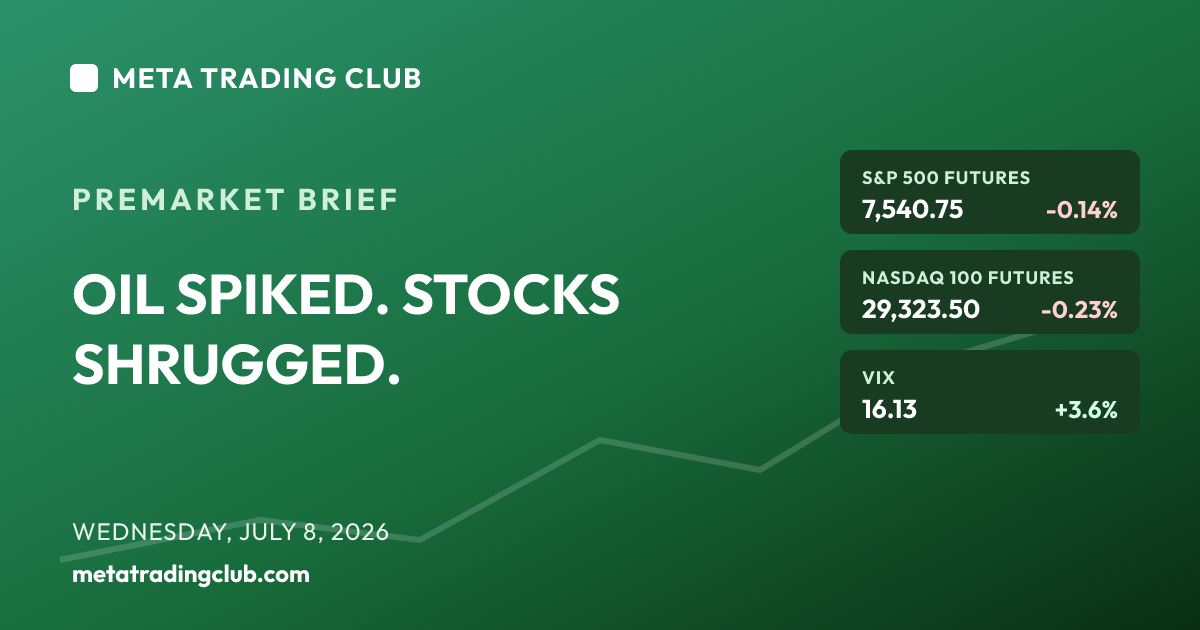

Wednesday, July 8, 2026 · 8:45 AM ET · MTC Market Intelligence

Two heavy weights hit the tape at once — and the market is barely flinching. That’s the whole story this morning. Overnight, US forces struck Iran after Tehran attacked three commercial vessels in the Strait of Hormuz, Trump declared the ceasefire “over,” and the Treasury revoked the license that let Iran export oil. Crude jumped — WTI up 2.7% to $72.34 — reviving a supply-shock premium the market had spent weeks pricing out. Layer that on top of a semiconductor sector that’s already in a bear market: Micron closed -4.7% Tuesday, SMH fell more than 3%, and the memory complex is still unwinding after Samsung’s AI print disappointed and a report surfaced that China’s DeepSeek is building its own chip. So you have a war premium and a chip bear market both pressing on a market sitting at record ground — and futures are only mildly red. S&P 500 futures -0.14% at 7,540.75, Dow futures -0.08% at 53,156, Nasdaq-100 futures -0.23% at 29,323, Russell 2000 futures -0.17%. Cross-asset leans cautious but controlled: VIX 16.13 (+3.6%) — nervous, not fearful; the 10-year at 4.50%, a two-week high as oil reignites inflation worry and pushes September hike odds near 58%; gold soft at $4,110; Bitcoin holding the low-$62Ks. The one event that matters today lands this afternoon: minutes from the Fed’s June meeting — the first under Chair Kevin Warsh — which the market will read for how hawkish this new Fed really is. The read: this is a test, not a top. Records don’t die quietly, they get tested, and the market is being asked to hold 7,500 through an oil shock and a chip drag on the same morning. If it holds into the Fed minutes, buyers are defending the record structure and the bad news is already absorbed. If 7,500 breaks and oil keeps climbing, the war premium wins and the record zone gives back. No alignment, no trade.

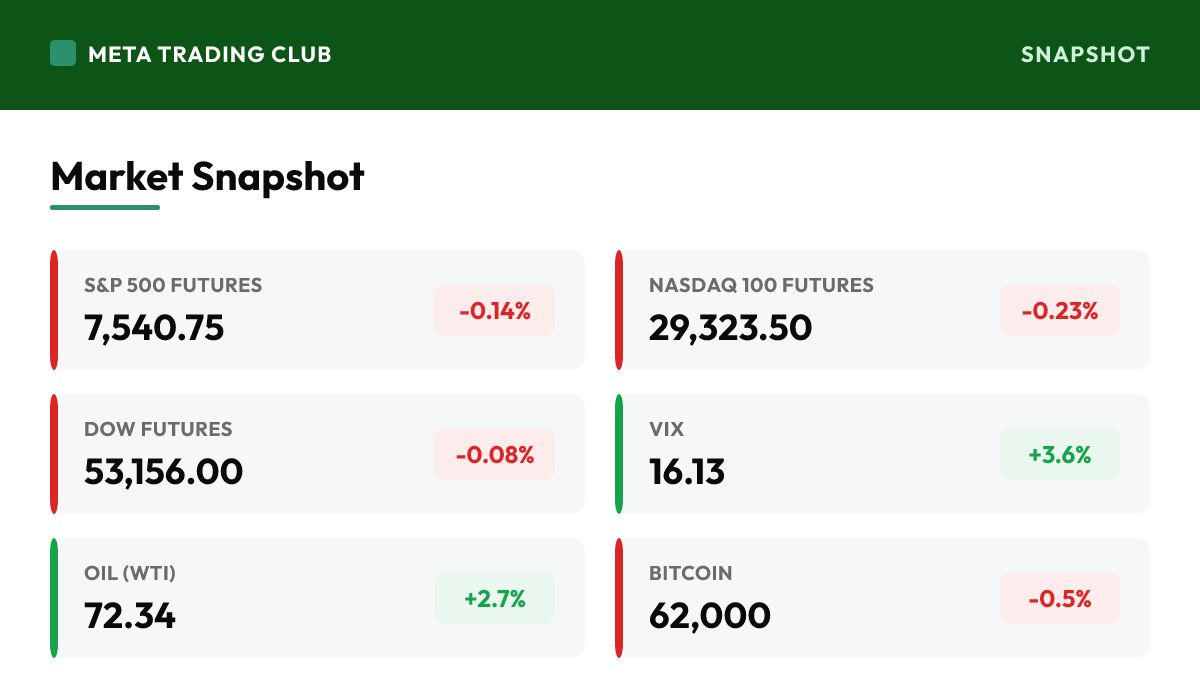

Market Snapshot

| Instrument | Level | Change | Note |

|---|---|---|---|

| S&P 500 Futures | 7,540.75 | -0.14% | Hovering just below the flatline after Tuesday’s 7,503.85 close, holding above the 7,500 line that decides everything today; the fact that futures are only marginally red with oil spiking and chips falling is itself the tell — the tape is absorbing the shock |

| Nasdaq 100 Futures | 29,323.50 | -0.23% | The soft spot again as the chip bear market keeps a lid on growth; a modest underperformance versus the Dow says money still leans toward value over long-duration tech while yields sit at a two-week high |

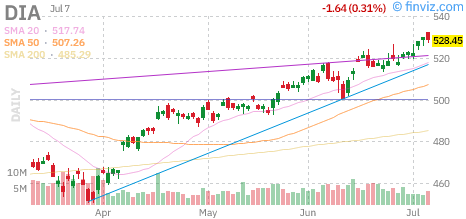

| Dow Futures | 53,156.00 | -0.08% | The steadiest index, barely red after Tuesday’s 52,925 close and Monday’s record at 53,055.91; blue chips and energy exposure are cushioning the average while chips do the bleeding |

| Russell 2000 Futures | 2,993.80 | -0.17% | Small caps in line with the majors — no outsized divergence, which says this isn’t a broad risk-off unwind yet; with the 10-year at 4.50%, the rate-sensitive corner has little room until yields settle |

| VIX | 16.13 | +3.6% | Ticking up on the Iran headlines but still in the low-16s — nervous, not fearful; this is the options market pricing caution, not panic. A push toward 18-20 would say the war premium is starting to bite for real |

| 10-Yr Yield | 4.50% | — | Up to a two-week high as the oil spike reignites inflation worry and pushes September rate-hike odds near 58%; higher yields press long-duration tech and are part of why the Nasdaq is the soft spot this morning |

| Oil (WTI) | 72.34 | +2.7% | The morning’s real mover — up to $72.34 after US strikes on Iran, the ceasefire declared over, and the Treasury revoking Iran’s oil-export license; a supply-shock premium the market had priced out is back on the table |

| Bitcoin | 62,000 | -0.5% | Holding the low-$62Ks, leaning slightly risk-off with the growth complex rather than catching a safe-haven bid; crypto is a passenger this morning, not a driver |

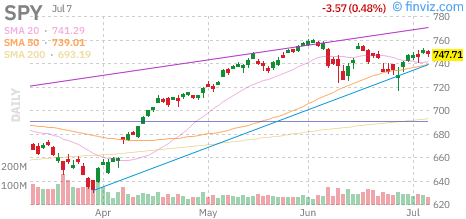

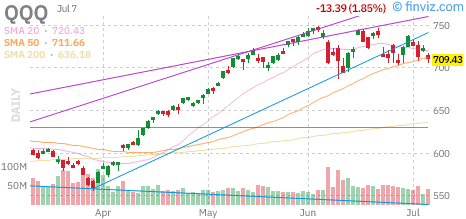

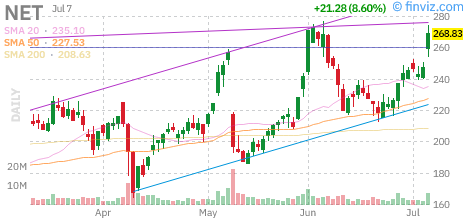

Charts to Watch

Daily candle charts with moving averages for the index proxies and today’s standout mover. Source: Finviz.

Performance at a Glance

Overnight & Global Markets

Read the calm, because the calm is the story. Overnight the market got hit with two things that should move a tape hard — a hot escalation in the US-Iran conflict and a fresh reminder that the semiconductor sector is in a bear market — and futures are barely red. That combination is the whole read. On the geopolitics: US forces struck Iran late Tuesday after Tehran attacked three commercial vessels in the Strait of Hormuz, Trump declared the ceasefire over, and the Treasury pulled the license allowing Iran to export oil. Crude responded exactly as you’d expect — WTI up 2.7% to $72.34 — putting a war premium back into energy that the market had spent weeks fading. On the chips: the memory complex is still unwinding after Samsung’s AI print underwhelmed and a report that China’s DeepSeek is building its own inference chip added a competitive worry; Micron closed -4.7% Tuesday and the semi ETF SMH fell more than 3%, dragging the Nasdaq to a 1.2% loss on the day. So growth is heavy and energy has a supply scare — and yet S&P futures sit just below 7,540, holding above 7,500, with the Dow nearly flat. That resilience is the signal: when a market refuses to break on bad news, it’s telling you sellers don’t have control yet. The macro layer isn’t helping tech — the 10-year rose to 4.50%, a two-week high, as the oil move reignited inflation worry and lifted September hike odds toward 58%, and higher yields hit long-duration names hardest. Cross-asset is cautious but orderly: VIX 16.13, gold soft at $4,110, Bitcoin holding low-$62Ks — nervous positioning, not a fear spike. The one event that matters today is this afternoon’s Fed minutes, the first set under Chair Kevin Warsh, which the market will comb for how hawkish this new Fed really is with oil back on the boil. The read: this is a test of the record, not a top. The market is being asked to hold 7,500 through an oil shock and a chip drag on the same session. Let it hold before you trust the bounce — and let it lose 7,500 before you trust the fade.

MAJOR HEADLINES AND CATALYSTS

Top Premarket Stories

- The US-Iran conflict escalated overnight. American forces struck Iran after Tehran attacked three commercial vessels in the Strait of Hormuz, Trump declared the ceasefire “over,” and the Treasury revoked the license that allowed Iran to export oil globally. WTI jumped 2.7% to $72.34 as a supply-disruption premium the market had faded came roaring back.

- Stocks are absorbing the shock, and that’s the tell. Despite the oil spike and a chip sector in a bear market, S&P futures are down just 0.14% and holding above 7,500, with the Dow nearly flat. When a market refuses to break on genuinely bad news, sellers don’t have control yet — this reads as a test of the record, not the start of a breakdown.

- Chips are still the anchor. The semiconductor complex sits in bear-market territory after Samsung’s AI print underwhelmed and a report that China’s DeepSeek is building its own inference chip; Micron closed -4.7% Tuesday and SMH fell 3%+. Until memory finds a floor, the Nasdaq stays the soft spot and the index has to hold record ground without its 2026 leaders helping.

- Yields are the quiet pressure. The oil move reignited inflation worry, pushing the 10-year to 4.50% — a two-week high — and lifting September rate-hike odds toward 58%. Higher yields hit long-duration tech hardest, so the rate tape and the chip selloff are reinforcing each other on the Nasdaq. Watch the 10-year into the Fed minutes.

Stock-Specific

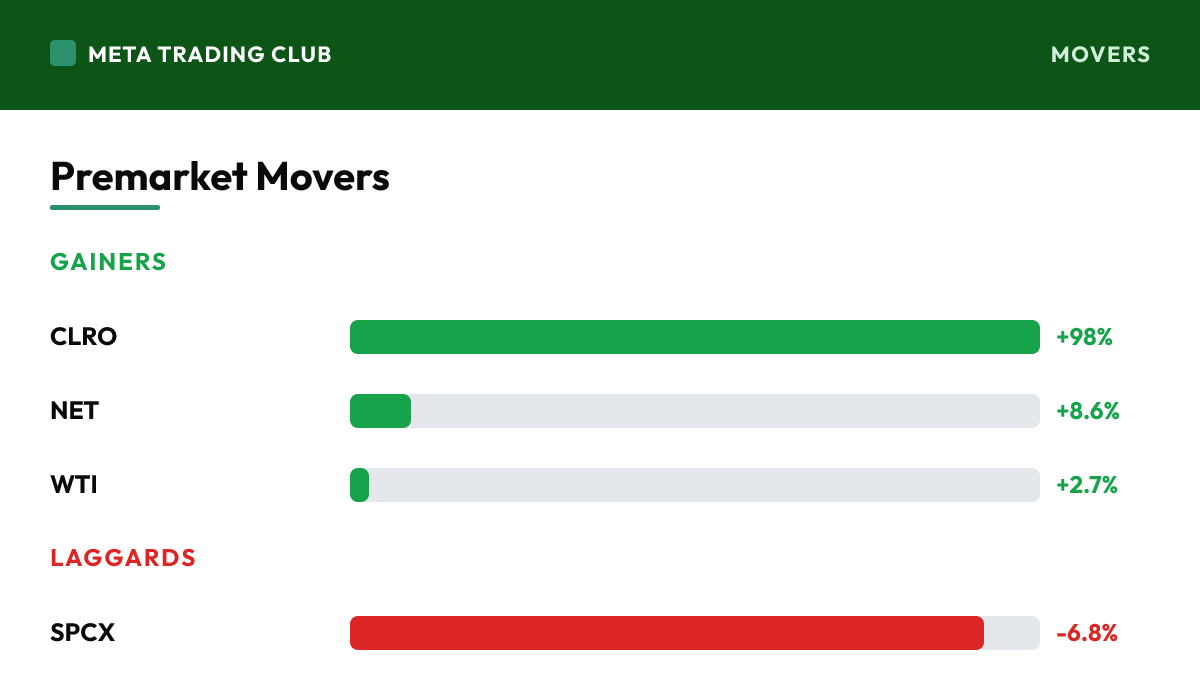

- SpaceX (SPCX) fell below its IPO price, off ~6.8% to $149.47, after inclusion in the Nasdaq let early investors offload shares into index funds. Wall Street is still bullish — JPMorgan at a $225 target, Morgan Stanley Street-high at $300 — but the mechanical selling is a reminder that index inclusion can be a near-term headwind, not just a badge.

- Low-float names are running against the heavy tape: ClearOne (CLRO) spiked ~98% to $13.84 and Cloudflare (NET) jumped 8.6% to $268.83, while Penguin Solutions (PENG) fell 7.4%. In a rotation-and-headline market, single-name catalysts still move harder than the index — trade the story, not the average.

Global and Macro

- The whole tape is waiting on one event: this afternoon’s Fed minutes, the first set under Chair Kevin Warsh. After the June meeting held rates steady with a more hawkish tone, and with oil now reigniting inflation worry, the market wants to know how this new Fed reads the labor-and-inflation picture. Position around the release — don’t front-run it.

- The macro cross-current is real: last week’s June jobs data showed a sharp slowdown and downward revisions, which cooled near-term hike bets — but this week’s oil spike is pushing them back up. That tug-of-war between soft labor and hot energy is exactly what the Fed minutes will be read against. The bond market is the tell all session.

TECHNICAL ANALYSIS

S&P 500 Key Levels

- SPX closed 7,503.85 Tuesday and futures sit near 7,540 — the line that matters on the open is 7,500. It’s the round number, the prior shelf, and the decision point for the whole session. Hold above it through the oil shock and this is a controlled test of the record; lose it intraday and the war premium plus chip drag start to compound. Let 7,500 answer before you commit.

- Resistance: 7,540 (overnight futures high), then the 7,575-7,600 record zone overhead. Support: 7,500 (the decision line), then 7,460, then 7,420 (the breakout shelf and risk anchor). Two closes back under 7,420 would flip the read from digestion to distribution — until then, the trend structure is intact.

- Bias: two-sided and patient into a headline-and-Fed session. Tuesday’s weakness was chip-led and the overnight risk is oil-led — the index is being pressed from two directions while sitting at record ground. That’s a lot to ask of one session. Trade the reaction at 7,500, anchor risk there, and let the Fed minutes clear the air this afternoon.

Sector and Sentiment

- The pressure is identifiable, which helps. Chips are the drag (Micron -4.7%, SMH -3%+) and oil is the wildcard, while the Dow holds flat and small caps are in line — that’s a market with a couple of known problems, not a broad panic. Watch whether the chip weakness stays boxed in semis or bleeds into the broader Nasdaq — that’s the line between a test and a breakdown.

- VIX at 16.13, up 3.6%, is a controlled move — the options market is pricing caution, not fear, even with an active geopolitical headline. Low-16s says the shock is being absorbed. A break toward 18-20 into or after the Fed minutes would tell you the war premium and the rate worry are starting to bite for real.

- The 10-year at 4.50% is the real headwind under growth. The oil spike reignited inflation worry, and higher yields hit long-duration tech hardest, so rates and the chip selloff are reinforcing each other on the Nasdaq. If yields settle after the minutes, chips get room to stabilize; if they push higher, the growth pullback has more to go.

TODAY’S ECONOMIC CALENDAR

Key Releases (ET)

- The event of the day is the Fed’s June meeting minutes this afternoon — the first under Chair Kevin Warsh. With oil reigniting inflation worry and September hike odds near 58%, the market will comb the text for how hawkish this new Fed really is. Expect the tape to trade quietly until the release, then move on the tone. Position around it, don’t front-run it.

- The 10-year at 4.50% is the number to watch all session. It’s the swing factor in a light-data morning: a move back down after the minutes relieves the Nasdaq, while a further climb compounds the chip selloff and pressures the highest-multiple names. In a headline-driven session, the rate tape is the macro read.

- Ahead this week: Q2 earnings season proper kicks off Thursday with PepsiCo, then Delta on Friday, before the big banks next week. Today’s US earnings calendar is light with no tape-movers, so the session belongs to the Iran headlines, the chip rotation, and the Fed minutes.

Earnings Today

- No tape-moving US earnings on today’s domestic calendar — the movers are story-driven: energy on the oil spike, chips on the memory bear market, and low-float names on single-stock catalysts. The session is headline- and Fed-driven, not earnings-driven. Save the earnings focus for Thursday when PepsiCo and Delta open the Q2 season.

- The lesson still standing from this week’s tape: Samsung’s AI print couldn’t hold semis up, and a great number wasn’t enough to stop a crowded trade from unwinding. When strong news can’t lift a stock, that’s a positioning signal — the good news was already in the price. Respect what the tape does with the news, not just the news itself.

PREMARKET PLAYBOOK

Key Levels

- SPX 7,500 — the decision line and today’s whole story. Futures sit near 7,540, so the open question is whether the round number holds as support through the oil shock. Hold keeps this a controlled test of the record with the trend intact; a clean loss says the war premium and chip drag are winning and the record zone is exposed. Let it hold before committing.

- SPX 7,420 — the prior breakout shelf and the risk anchor. As long as 7,420 holds, this is digestion inside an uptrend and pullbacks stay buyable. Two closes under it flip the read from test to distribution and open the door toward 7,400 and below.

- WTI and the 10-year — the confirmation pair for the macro read. If oil cools and yields settle after the Fed minutes, the pressure on stocks lifts and 7,500 holds easily. If crude keeps climbing and the 10-year pushes past 4.50%, the inflation-and-war combination presses the tape and 7,500 gets tested for real.

Bull case: The market absorbs the shock. SPX defends 7,500, oil’s spike fades as the initial Iran fear cools, and the Fed minutes read less hawkish than feared, letting the 10-year settle back off 4.50%. Chip selling stays boxed in memory without bleeding into the broader Nasdaq, VIX drifts back toward 15, and the record structure survives a genuine two-sided test. A market that holds record ground through an oil shock and a chip drag is showing real underlying strength.

Bear case: The pressure compounds. Oil keeps climbing as the Iran conflict escalates, the 10-year pushes past 4.50% on the inflation scare, and the Fed minutes land hawkish — a triple hit to long-duration tech. The chip bear market deepens (Micron, memory), SPX loses 7,500 then 7,420, and VIX breaks 18. What looked like a controlled test becomes a real drawdown as the war premium and the rate worry finally overwhelm the record bid.

What We’re Watching

- The 7,500 hold — futures are just above it and both the oil shock and the chip drag are testing it. This one level decides whether today is a controlled test or the start of a fade. Let it prove itself as support before trusting any bounce.

- The Fed minutes this afternoon — the session’s real catalyst. A hawkish tone with oil already hot could push yields and pressure stocks; a balanced read clears the air. Don’t over-position into the release; trade the reaction after it.

- Oil and the 10-year together — the macro tell. Crude cooling and yields settling relieves the whole tape; both climbing compounds the pressure on growth. In a light-data session, this pair is the read that matters all morning.

Premarket Movers

Gainers

| CLRO | ClearOne | +98% | Spiked ~98% to $13.84 premarket on a low-float, story-driven move — the kind of single-name run that ignores the macro tape entirely; size it like the volatility it is |

| NET | Cloudflare | +8.6% | Jumped 8.6% to $268.83, a rare growth-name winner against a heavy chip backdrop — capital still finds select tech even as the semi complex unwinds |

| WTI | Energy / crude proxy | +2.7% | WTI at $72.34 after the Iran strikes gives energy equities the morning’s clearest sector bid as a supply-shock premium returns |

Laggards

| SPCX | Space Exploration Technologies | -6.8% | Fell below its IPO price to $149.47 as Nasdaq inclusion let early investors sell into index funds; a mechanical headwind, not a fundamental one — Street targets still range $225-$300 |

| PENG | Penguin Solutions | -7.4% | Off 7.4% to $62.71, caught in the broader chip and AI-hardware weakness dragging the semiconductor complex this week |

| MU | Micron Technology | -4.7% | Closed -4.7% Tuesday as the memory group leads the semiconductor bear market lower; still no floor in the names that led the 2026 AI run |

Risks Into the Open

- Primary risk: the oil shock deepens. The Iran escalation put a war premium back into crude, and if the conflict widens or Hormus supply is genuinely threatened, the inflation channel hits yields and stocks together. Watch WTI — a run further above $72 turns a headline into a macro problem the Fed can’t ignore.

- Secondary risk: the Fed minutes land hawkish. With oil hot and September hike odds near 58%, a hawkish read from Chair Warsh’s first meeting could push the 10-year past 4.50% and pressure the whole growth complex. The rate reaction after 2pm is the swing factor for the back half of the session.

- Constructive: the tape is absorbing the shock. Futures are only marginally red despite an oil spike and a chip bear market, the Dow is holding record ground, and VIX is only mildly higher — the market is refusing to break on bad news. As long as SPX holds 7,500, this reads as a controlled test of the record, not the start of a top.

Frequently Asked Questions

Where are S&P 500 futures trading ahead of the open?

Ahead of Wednesday, July 8, 2026, S&P 500 futures are at 7,540.75 (-0.14%), with the VIX near 16.13. Two heavy weights hit the tape at once — and the market is barely flinching. That’s the whole story this morning. Overnight, US forces struck Iran after Tehran attacked three commercial vessels in the Strait of Hormuz, Trump declared the ceasefire “over,” and the Treasury revoked the license that let Iran export oil. Crude jumped — WTI up 2.7% to $72.34 — reviving a supply-shock premium the market had spent weeks pricing out. Layer that on top of a semiconductor sector that’s already in a bear market: Micron closed -4.7% Tuesday, SMH fell more than 3%, and the memory complex is still unwinding after Samsung’s AI print disappointed and a report surfaced that China’s DeepSeek is building its own chip. So you have a war premium and a chip bear market both pressing on a market sitting at record ground — and futures are only mildly red. S&P 500 futures -0.14% at 7,540.75, Dow futures -0.08% at 53,156, Nasdaq-100 futures -0.23% at 29,323, Russell 2000 futures -0.17%. Cross-asset leans cautious but controlled: VIX 16.13 (+3.6%) — nervous, not fearful; the 10-year at 4.50%, a two-week high as oil reignites inflation worry and pushes September hike odds near 58%; gold soft at $4,110; Bitcoin holding the low-$62Ks. The one event that matters today lands this afternoon: minutes from the Fed’s June meeting — the first under Chair Kevin Warsh — which the market will read for how hawkish this new Fed really is. The read: this is a test, not a top. Records don’t die quietly, they get tested, and the market is being asked to hold 7,500 through an oil shock and a chip drag on the same morning. If it holds into the Fed minutes, buyers are defending the record structure and the bad news is already absorbed. If 7,500 breaks and oil keeps climbing, the war premium wins and the record zone gives back. No alignment, no trade.

What is the biggest catalyst for the market today?

The US-Iran conflict escalated overnight. American forces struck Iran after Tehran attacked three commercial vessels in the Strait of Hormuz, Trump declared the ceasefire “over,” and the Treasury revoked the license that allowed Iran to export oil globally. WTI jumped 2.7% to $72.34 as a supply-disruption premium the market had faded came roaring back.

What key levels should traders watch today?

SPX 7,500 — the decision line and today’s whole story. Futures sit near 7,540, so the open question is whether the round number holds as support through the oil shock. Hold keeps this a controlled test of the record with the trend intact; a clean loss says the war premium and chip drag are winning and the record zone is exposed. Let it hold before committing. SPX 7,420 — the prior breakout shelf and the risk anchor. As long as 7,420 holds, this is digestion inside an uptrend and pullbacks stay buyable. Two closes under it flip the read from test to distribution and open the door toward 7,400 and below. WTI and the 10-year — the confirmation pair for the macro read. If oil cools and yields settle after the Fed minutes, the pressure on stocks lifts and 7,500 holds easily. If crude keeps climbing and the 10-year pushes past 4.50%, the inflation-and-war combination presses the tape and 7,500 gets tested for real.

How does Meta Trading Club approach the market open?

We qualify every setup through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

Trade with a system, not signals.

This is exactly how MTC members read the open — bias, level, reaction, confirmation, execution. If you want to learn to qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process.

Apply for the Incubator → Learn moreSources: CNBC | Yahoo Finance | Benzinga | Investing.com | TheStreet – July 8, 2026 (8:15-8:45 AM ET window). For educational purposes only. Not financial advice.