Monday, July 6, 2026 · 8:45 AM ET · MTC Market Intelligence

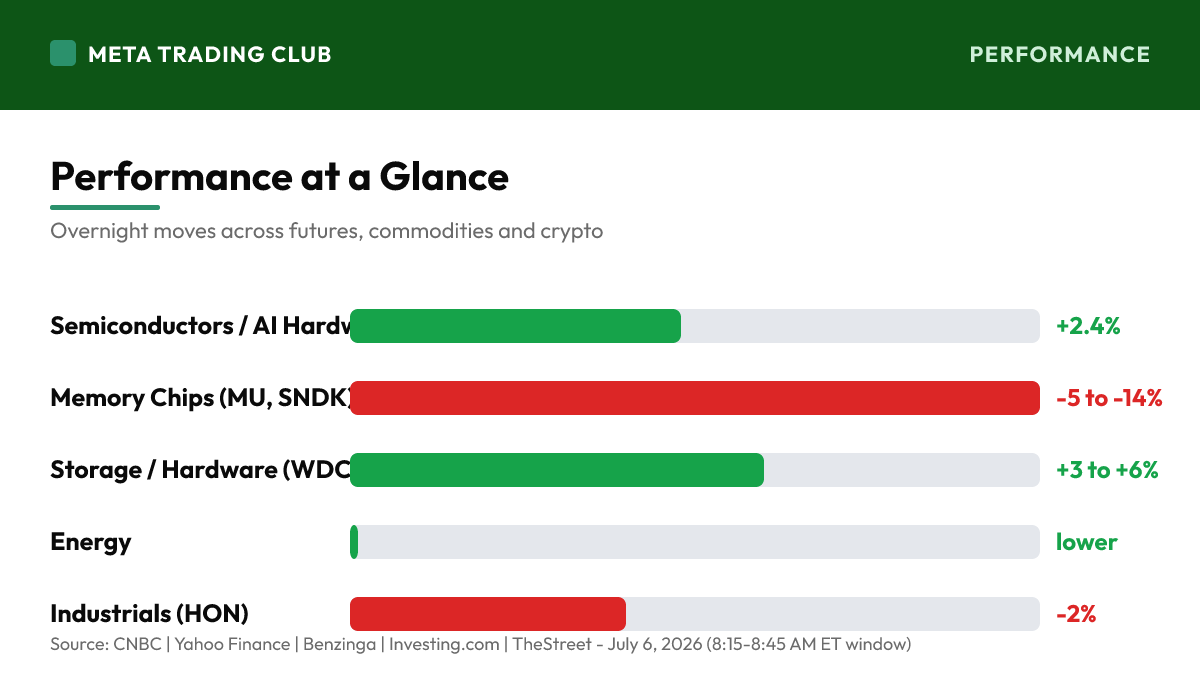

The AI trade is getting its confidence back — and the tape is leading with it. After a bruising late-June chip slump, techs are out front to start the holiday-shortened week: Nasdaq-100 futures jumped 1.13% to 29,890.50, S&P 500 futures added 0.39% to 7,557.50, while Dow futures slipped 0.11% to 53,125.00 after the blue-chip index closed Thursday at a fresh record 52,900.07. The spark came overnight from Taiwan — Nvidia supplier Hon Hai (Foxconn) reported stronger-than-expected quarterly sales on Sunday, a clean read that AI hardware demand is still intact. The VanEck Semiconductor ETF (SMH) is up 2.4% premarket, with Intel +3% to $123.98 and Western Digital +6.3% leading the rebound. But look under the hood: memory is still the laggard — Micron is soft again near $975 after last week’s post-earnings unwind, and Samsung’s preliminary Q2 print Tuesday (expected to show an 18-fold profit jump) is the next real test for the group. The macro backdrop flipped last week: June payrolls rose just 57,000 versus ~115K expected, with May revised down to 129K — a soft number that pulled the market’s fear away from rate hikes and back toward cuts. The 10-year eased to about 4.46%, and this morning’s ISM Services data plus Wednesday’s Fed minutes (Chair Warsh’s first meeting) are the near-term catalysts. Cross-asset: VIX ticked up to 16.40 even as stocks rose, WTI fell 0.5% to $68.33 after OPEC+ agreed to raise output for a fifth straight month and the Strait of Hormuz reopened, Bitcoin firmed to $62,734 (+0.2%), gold pushed to $4,163 (+0.9%). Two voices keep it honest: JPMorgan raised its S&P target to 7,800 but warned the path won’t be a straight line, and Michael Burry issued a blunt warning on AI stocks. The read: this is a risk-on reopen with real fuel — AI demand confirmed, oil falling, rate pressure easing — but leadership is narrow and memory is dragging. Let SPX prove it can hold above 7,500 and trade the names actually moving, not the index average. No alignment, no trade.

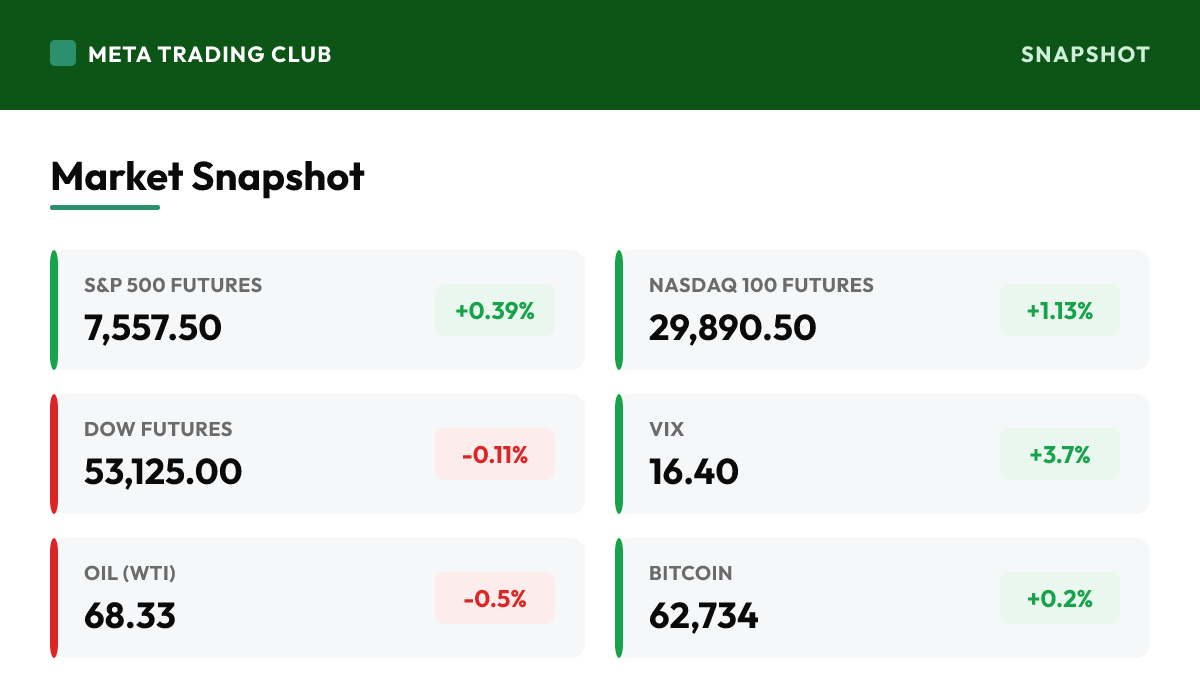

Market Snapshot

| Instrument | Level | Change | Note |

|---|---|---|---|

| S&P 500 Futures | 7,557.50 | +0.39% | Pushing into fresh record territory, led from behind by tech; the level to respect on the open is 7,500 — hold above it and the breakout stays clean, lose it and this becomes a fade |

| Nasdaq 100 Futures | 29,890.50 | +1.13% | The clear leader this morning as the AI trade regains its footing on Foxconn’s strong sales; a 1%+ premarket lead over the Dow tells you where the money wants to go today |

| Dow Futures | 53,125.00 | -0.11% | Easing slightly after Thursday’s record close at 52,900.07; the blue-chip index already made its high, so today the tape rotates toward growth, not the average that just topped out |

| Russell 2000 Futures | 3,018.30 | +0.14% | Small caps firm modestly as the soft jobs report eases rate-hike fear; the most rate-sensitive corner of the tape has room if yields keep drifting lower |

| VIX | 16.40 | +3.7% | Ticking up even as stocks rise — a small tell that the options market isn’t fully buying the calm; low-16s is still a constructive backdrop, but watch for a push toward 18 |

| 10-Yr Yield | 4.46% | — | Eased after June payrolls came in soft (+57K vs ~115K expected); the rate regime flipped from hike-risk back toward cuts, which turns weak data into a tailwind for growth |

| Oil (WTI) | 68.33 | -0.5% | Falling after OPEC+ agreed to raise output for a fifth straight month and the Strait of Hormuz reopened; the war premium is gone and cheaper crude eases the inflation worry |

| Bitcoin | 62,734 | +0.2% | Firming to $62.7K as it extends a weekend rally — crypto is quietly confirming the risk-on tone this time rather than lagging it; a mild positive for conviction behind the highs |

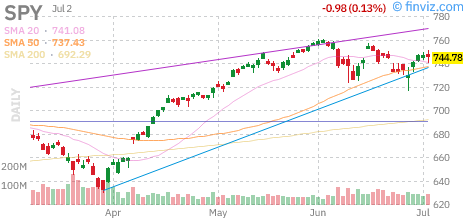

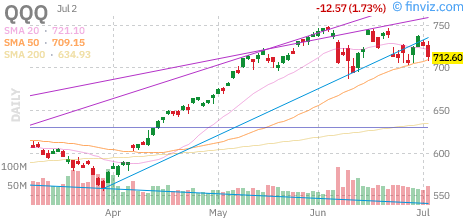

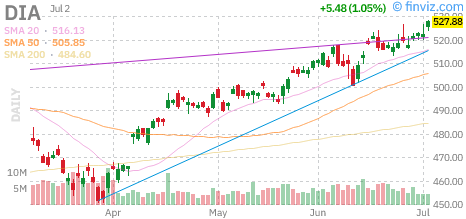

Charts to Watch

Daily candle charts with moving averages for the index proxies and today’s standout mover. Source: Finviz.

Performance at a Glance

Overnight & Global Markets

Read the leadership, because it tells you the whole story this morning. Nasdaq-100 futures are up 1.13% to 29,890.50 while Dow futures sit flat-to-lower at 53,125.00 — a clean rotation back into growth and away from the blue-chip average that just printed a record 52,900.07 on Thursday. The catalyst is specific and real: on Sunday, Nvidia supplier Hon Hai (Foxconn) reported stronger-than-expected quarterly sales, and the market read it as proof the AI hardware cycle didn’t break in late June — it just paused. The VanEck Semiconductor ETF (SMH) is up 2.4% premarket, Intel is +3% at $123.98, and Western Digital is +6.3%. But this is a rebound with a hole in it: memory is still the laggard. Micron is soft again near $975 after last week’s post-earnings unwind, and the real test comes Tuesday when Samsung posts preliminary Q2 numbers expected to show an 18-fold profit jump — the memory group needs that confirmation to catch up to the rest of the chip space. The macro layer flipped the tape’s psychology last week. June payrolls rose just 57,000 against roughly 115K expected, with May revised down to 129K — soft enough that the market’s fear swung from ‘the Fed might hike’ back to ‘the Fed might cut.’ The 10-year eased to about 4.46%, and that’s why weak data is now being bought, not sold. This morning’s ISM Services print and Wednesday’s Fed minutes — the first meeting under Chair Kevin Warsh — are the next inputs. Cross-asset agrees with the risk-on read: WTI is down 0.5% to $68.33 after OPEC+ raised output a fifth straight month and the Strait of Hormuz reopened, Bitcoin firmed to $62,734, gold pushed to $4,163. The honest caveats: JPMorgan lifted its S&P target to 7,800 but warned the path won’t be straight, and Michael Burry issued a blunt warning on AI names. The read: risk-on with genuine fuel, but narrow leadership and a lagging memory group. Let SPX hold 7,500, watch whether the chip rebound broadens past hardware into memory, and trade the movers — not the index.

MAJOR HEADLINES AND CATALYSTS

Top Premarket Stories

- The AI trade is rebounding on a real catalyst. Nvidia supplier Hon Hai (Foxconn) reported stronger-than-expected quarterly sales Sunday — a sign AI hardware demand is still intact. SMH is +2.4% premarket, Intel +3% to $123.98, Western Digital +6.3%. Nasdaq-100 futures lead at +1.13%. This is the group that led all of 2026 getting its footing back.

- But memory is still the laggard. Micron is soft again near $975 after last week’s post-earnings unwind, and the storage/memory complex hasn’t fully joined the rebound. The real test is Tuesday: Samsung posts preliminary Q2 numbers expected to show an 18-fold profit jump. That print either confirms memory or extends the divergence within chips.

- The rate story flipped. June payrolls rose just 57,000 versus ~115K expected, with May revised down to 129K — a soft report that pulled the market’s fear from rate hikes back toward cuts. The 10-year eased to about 4.46%. In this regime, weak data is a tailwind for growth, not a threat — the opposite of last week’s setup.

- Oil is falling on supply, not demand fear. WTI is down 0.5% to $68.33 after OPEC+ agreed to raise output for a fifth straight month (seven members adding ~188K bpd in August) and the Strait of Hormuz reopened. The war premium has drained out — risk-friendly for the broad market, a headwind for energy names.

Macro and the Week Ahead

- Today: ISM Services and a batch of US services data give the first read on the economy since Thursday’s soft jobs number. Wednesday brings the Fed minutes from Chair Kevin Warsh’s first meeting — the market wants clarity on whether a soft labor market pulls cuts back onto the table. Tuesday: Samsung earnings and SpaceX (SPCX) officially joins the Nasdaq-100 before the open.

- Two honest caveats on the record run: JPMorgan raised its S&P 500 target to 7,800 but warned the path there won’t be a straight line and flagged flash-crash risk. Michael Burry issued a blunt warning on AI stocks. Neither is a reason to short a rebound — but both are a reason to keep size honest and levels tight.

Global and Geopolitical

- The Strait of Hormuz reopening and OPEC+’s output hike mark a genuine de-escalation in the energy picture that dominated June. Flows have revived, crude is pressing lower, and the inflationary knock-on worry is fading. For equities this is a quiet tailwind — one less thing pushing yields and input costs up.

- Bitcoin extended its weekend rally to $62,734 (+0.2%) and gold pushed to $4,163 (+0.9%). Crypto confirming the risk-on tone rather than lagging it is a mild positive for conviction; gold at record-zone levels alongside stocks says liquidity, not fear, is driving the bid.

TECHNICAL ANALYSIS

S&P 500 Key Levels

- SPX futures sit at 7,557.50, pushing into fresh record territory after Thursday’s holiday-shortened session. The line that matters on the open is 7,500 — the round number and prior ceiling. Hold above it and the breakout is clean; lose it intraday and this morning’s gap becomes a fade setup. Don’t chase the gap; let it hold first.

- Resistance: the 7,575-7,600 record zone directly overhead, then open air toward JPMorgan’s 7,800 target. Support: 7,500 (the reclaim line), then 7,440 (the prior breakout shelf). Two closes back under 7,440 would flip the read from breakout to digestion — until then, pullbacks stay buyable.

- Bias: constructive but two-sided into a narrow-leadership tape. A gap led by one sector (chips) on one catalyst (Foxconn) is a real move but a fragile one — it needs the memory group and breadth to join. Trade the leaders with catalysts, anchor risk to 7,500, and let the record zone prove itself before adding.

Sector and Sentiment

- The rebound is real but uneven: SMH +2.4%, Intel +3%, WDC +6.3% — yet Micron is soft near $975 and memory lags. That’s rotation within chips, not a clean group rally. Watch Samsung Tuesday: if memory confirms, the chip trade broadens and the rally has legs; if it disappoints, leadership stays narrow and vulnerable.

- VIX at 16.40 ticking up while stocks rise is a small non-confirmation — the options market isn’t fully sold on the calm. Low-16s is still constructive, but a push toward 18 into the Fed minutes would say the record zone is being defended by fewer hands than the index level implies.

- Breadth and cross-asset are cooperating: Russell firm (+0.14%), Bitcoin confirming (+0.2%), oil falling on supply, yields easing. That’s a healthier backdrop than late June — the pieces are aligned for the record zone to hold, provided leadership broadens past a handful of chip names.

TODAY’S ECONOMIC CALENDAR

Key Releases (ET)

- 9:45-10:00 AM — S&P Global Services PMI (final) and ISM Services PMI for June. This is the first hard data since Thursday’s soft jobs print; a weak services read would reinforce the cuts-back-on-the-table narrative that’s fueling the growth bid, while a strong one complicates it. Watch the prices-paid component for the inflation signal.

- The bond market is the swing factor again, but in the other direction from last week. With the 10-year at 4.46% and payrolls soft, yields drifting lower is now the tailwind under growth. A move back up in yields — not down — would be the thing that pressures the record zone today.

- Ahead this week: Fed minutes Wednesday (Warsh’s first meeting), Samsung preliminary Q2 earnings Tuesday, and SpaceX joining the Nasdaq-100 before Tuesday’s open. Q2 US earnings season proper kicks off next week with the banks — until then the tape trades on macro prints and AI-chain headlines.

Earnings Today

- No tape-moving US earnings on today’s calendar — the session is macro- and headline-driven. The overnight catalyst was Foxconn’s strong sales (AI demand), and the movers are story- and analyst-driven: chips rebounding, Intel and WDC leading hardware, energy soft on OPEC+.

- The real earnings catalyst is Tuesday: Samsung’s preliminary Q2 print, expected to show an 18-fold profit jump year-on-year on memory strength. That’s the number that tells you whether the lagging memory group joins the chip rebound or keeps dragging. Position around it, don’t front-run it.

PREMARKET PLAYBOOK

Key Levels

- SPX 7,500 — the reclaim line and today’s decision point. Futures are at 7,557.50, so the open question is whether the gap holds above 7,500 or fills back below it. Hold keeps the breakout clean and leaders in play; a loss turns the morning pop into a fade and says wait.

- SPX 7,440 — the prior breakout shelf and the risk anchor. As long as 7,440 holds, every pullback is a buyable rotation. Two closes under it flip the second-half read from breakout to digestion and open 7,400 below.

- SMH and Micron — the confirmation pair for the chip trade. SMH holding its +2.4% gap says the rebound is real; Micron reclaiming ground (not just SMH) is what tells you memory is joining. If the leaders hold and memory turns, the rally broadens. If not, it stays narrow.

Bull case: Foxconn’s demand signal holds, ISM Services comes in soft enough to keep cuts on the table, and yields keep drifting lower — letting SPX hold above 7,500 and grind toward the 7,575-7,600 record zone. The chip rebound broadens as Samsung’s Tuesday print confirms memory, Intel and WDC keep hardware bid, and VIX settles back toward 15. Risk-on with real fuel: AI demand confirmed, oil falling, rate pressure easing.

Bear case: The gap proves to be one sector on one headline. Memory keeps dragging, Micron can’t hold $975, and Samsung disappoints Tuesday — exposing narrow leadership. ISM Services runs hot, yields tick back up, and SPX loses 7,500 then 7,440 as Burry’s AI warning and JPMorgan’s flash-crash flag get real pricing. VIX pushes through 18 and the record zone gives back the reopen pop.

What We’re Watching

- The 7,500 hold — futures gapped above it; the first test is whether it holds as support or fills as resistance. This one level decides whether today’s tape is a clean breakout or a fade. Let it prove itself before committing.

- Whether the chip rebound broadens — SMH is up 2.4% but memory (Micron) lags. Watch for memory to join, not just hardware. A broadening chip bid means the rally has legs; a narrow one led by three names is fragile into Samsung’s Tuesday print.

- Yields and ISM Services — with the rate regime flipped, lower yields are the tailwind and a yield pop is the threat. Watch the 10-year’s reaction to the services data; 4.46% drifting lower supports growth, a move back toward 4.55% pressures the record zone.

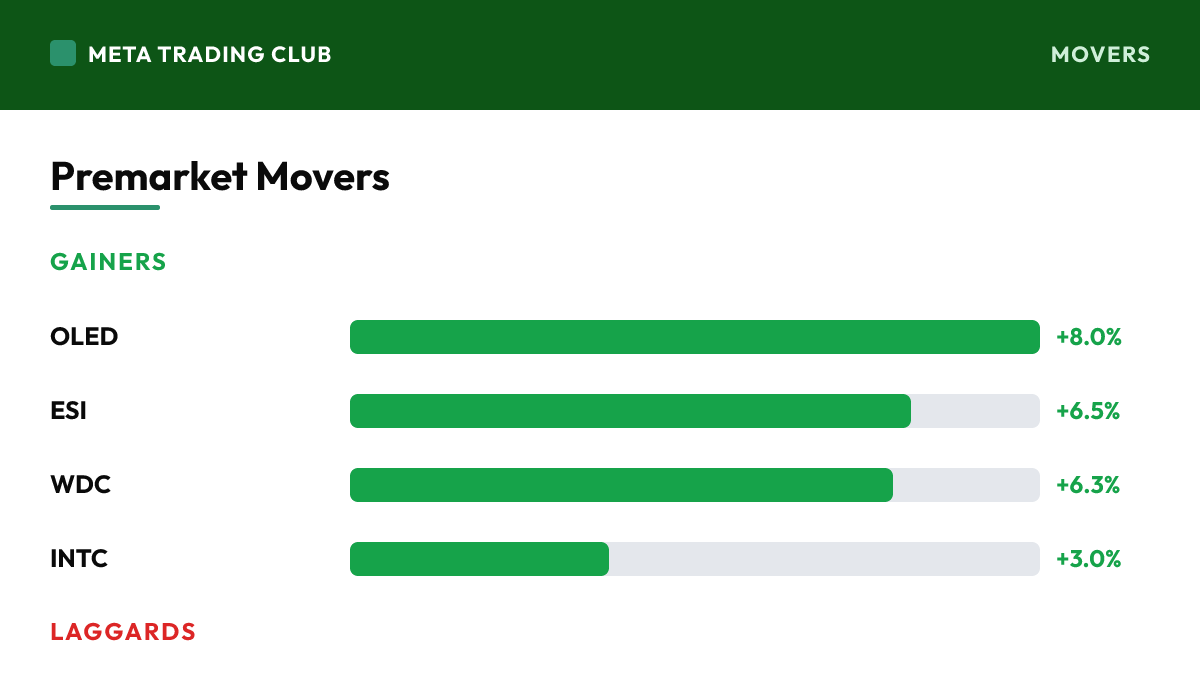

Premarket Movers

Gainers

| OLED | Universal Display | +8.0% | The premarket leader, up 8% as the tech/AI complex catches a broad bid on renewed hardware demand |

| ESI | Element Solutions | +6.5% | Up 6.5% premarket alongside the materials-and-hardware bid feeding the chip rebound |

| WDC | Western Digital | +6.3% | Up 6.3% as the storage/hardware layer joins the AI rebound — a sign the bid is reaching past pure accelerators |

| INTC | Intel | +3.0% | Up 3% to $123.98 as chip stocks rebound following the late-June sector weakness; SMH broadly +2.4% |

Laggards

| ICLR | Icon PLC | -6.0% | Down 6% premarket, one of the session’s clearest decliners against a risk-on tape |

| LOAR | Loar Holdings | -3.5% | Off 3.5% premarket as the industrials/defense corner lags the growth-led move |

| HON | Honeywell | -2.0% | Down 2% — old-economy industrials take a back seat with the Dow already at a record and money rotating into growth |

Risks Into the Open

- Primary risk: narrow leadership. This morning’s gap is chips on one catalyst (Foxconn) with memory (Micron) still lagging. A one-sector, one-headline move is real but fragile — size the leaders around real catalysts and keep index conviction honest to the 7,500 line until breadth confirms.

- Secondary risk: the yield tell. The rate regime flipped soft last week, so lower yields are the tailwind and a yield pop is the threat. Watch the 10-year’s reaction to ISM Services — a move back toward 4.55% pressures the record zone regardless of how strong the chip tape looks.

- Constructive: this is risk-on with real fuel. AI demand confirmed by Foxconn, oil falling on OPEC+ supply, yields easing on soft jobs, Bitcoin confirming the tone. The pieces are aligned for the record zone to hold — the job now is to let 7,500 confirm it and trade the names that are actually moving.

Frequently Asked Questions

Where are S&P 500 futures trading ahead of the open?

Ahead of Monday, July 6, 2026, S&P 500 futures are at 7,557.50 (+0.39%), with the VIX near 16.40. The AI trade is getting its confidence back — and the tape is leading with it. After a bruising late-June chip slump, techs are out front to start the holiday-shortened week: Nasdaq-100 futures jumped 1.13% to 29,890.50, S&P 500 futures added 0.39% to 7,557.50, while Dow futures slipped 0.11% to 53,125.00 after the blue-chip index closed Thursday at a fresh record 52,900.07. The spark came overnight from Taiwan — Nvidia supplier Hon Hai (Foxconn) reported stronger-than-expected quarterly sales on Sunday, a clean read that AI hardware demand is still intact. The VanEck Semiconductor ETF (SMH) is up 2.4% premarket, with Intel +3% to $123.98 and Western Digital +6.3% leading the rebound. But look under the hood: memory is still the laggard — Micron is soft again near $975 after last week’s post-earnings unwind, and Samsung’s preliminary Q2 print Tuesday (expected to show an 18-fold profit jump) is the next real test for the group. The macro backdrop flipped last week: June payrolls rose just 57,000 versus ~115K expected, with May revised down to 129K — a soft number that pulled the market’s fear away from rate hikes and back toward cuts. The 10-year eased to about 4.46%, and this morning’s ISM Services data plus Wednesday’s Fed minutes (Chair Warsh’s first meeting) are the near-term catalysts. Cross-asset: VIX ticked up to 16.40 even as stocks rose, WTI fell 0.5% to $68.33 after OPEC+ agreed to raise output for a fifth straight month and the Strait of Hormuz reopened, Bitcoin firmed to $62,734 (+0.2%), gold pushed to $4,163 (+0.9%). Two voices keep it honest: JPMorgan raised its S&P target to 7,800 but warned the path won’t be a straight line, and Michael Burry issued a blunt warning on AI stocks. The read: this is a risk-on reopen with real fuel — AI demand confirmed, oil falling, rate pressure easing — but leadership is narrow and memory is dragging. Let SPX prove it can hold above 7,500 and trade the names actually moving, not the index average. No alignment, no trade.

What is the biggest catalyst for the market today?

The AI trade is rebounding on a real catalyst. Nvidia supplier Hon Hai (Foxconn) reported stronger-than-expected quarterly sales Sunday — a sign AI hardware demand is still intact. SMH is +2.4% premarket, Intel +3% to $123.98, Western Digital +6.3%. Nasdaq-100 futures lead at +1.13%. This is the group that led all of 2026 getting its footing back.

What key levels should traders watch today?

SPX 7,500 — the reclaim line and today’s decision point. Futures are at 7,557.50, so the open question is whether the gap holds above 7,500 or fills back below it. Hold keeps the breakout clean and leaders in play; a loss turns the morning pop into a fade and says wait. SPX 7,440 — the prior breakout shelf and the risk anchor. As long as 7,440 holds, every pullback is a buyable rotation. Two closes under it flip the second-half read from breakout to digestion and open 7,400 below. SMH and Micron — the confirmation pair for the chip trade. SMH holding its +2.4% gap says the rebound is real; Micron reclaiming ground (not just SMH) is what tells you memory is joining. If the leaders hold and memory turns, the rally broadens. If not, it stays narrow.

How does Meta Trading Club approach the market open?

We qualify every setup through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

Trade with a system, not signals.

This is exactly how MTC members read the open — bias, level, reaction, confirmation, execution. If you want to learn to qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process.

Apply for the Incubator → Learn moreSources: CNBC | Yahoo Finance | Benzinga | Investing.com | TheStreet – July 6, 2026 (8:15-8:45 AM ET window). For educational purposes only. Not financial advice.