Monday, June 29, 2026 · 4:30 PM ET · MTC Market Close

After one of the ugliest weeks of the year, the tape did more than exhale — it ripped. A weekend de-escalation between the US and Iran, plus a Supreme Court decision letting Fed Governor Lisa Cook keep her job, gave risk assets the all-clear, and the beaten-down mega-caps led the recovery. The Nasdaq Composite jumped 2.07% to 25,820.14, the S&P 500 rose 1.18% to 7,440.43 — reclaiming the 7,400 shelf it failed at all last week — and the Dow added 306.63 points to 52,182.74, closing above 52,000 for the first time ever on the same day Alphabet made its debut in the index (replacing Verizon). Alphabet rose nearly 5% on its first session as a Dow member. The macro backdrop confirmed the calmer tone: the VIX collapsed to 17.65, the 10-year held at 4.38%, WTI eased to $70.57 as the war premium kept bleeding out, gold firmed to $4,030, and Bitcoin sat near $59.6K. But the honest read for traders is the one underneath the green: this was a relief rally led by the exact names that got crushed last week, and the leadership was uneven. Space stocks stole the show — Iridium soared ~25% and Rocket Lab ~16% on an $8B acquisition deal — while Comcast jumped ~10% on a plan to split into two public companies. The tell to respect: the chip complex still leaked. Micron fell ~6% and the broader memory names lagged even as the index ripped, and Verizon dropped ~5.8% on its Dow removal, a BT joint-venture spinoff, and up to $1.55B in restructuring charges. So the rebound is real but narrow — it’s a positioning bounce off de-escalation, not a confirmed trend change. Tomorrow the data starts: Chicago PMI, Consumer Confidence and JOLTS all hit before noon, Nike and Constellation Brands report after the close, and it’s quarter-end. A gap-up off geopolitics into month-end is exactly the kind of move that needs confirmation before you trust it. No alignment, no trade.

The Closing Bell

| Instrument | Close | Change | Note |

|---|---|---|---|

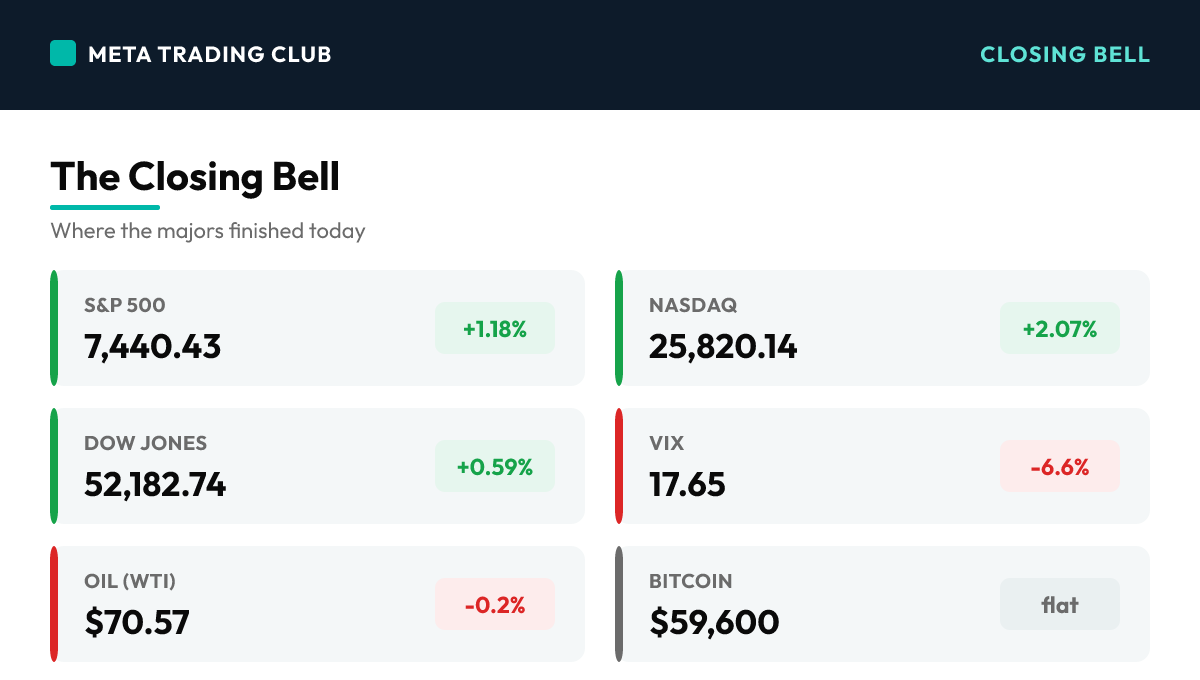

| S&P 500 | 7,440.43 | +1.18% | Reclaimed the 7,400 shelf it failed at all last week, adding ~86 points as the beaten-down mega-caps led a de-escalation relief rally |

| Nasdaq | 25,820.14 | +2.07% | Jumped ~523 points as last week’s hardest-hit tech names bounced hardest — though the chip complex notably lagged the move |

| Dow Jones | 52,182.74 | +0.59% | Closed above 52,000 for the FIRST time ever (+306.63 pts) on the same day Alphabet debuted in the index, replacing Verizon |

| Russell 2000 | — | N/A | Rode the risk-on bid alongside the large caps; the post-reconstitution small-cap complex caught the de-escalation relief |

| VIX | 17.65 | -6.6% | Collapsed back below 18 as the weekend US-Iran de-escalation drained the fear premium that built up through last week’s selloff |

| 10-Yr Yield | 4.38% | flat | Essentially unchanged near seven-week lows — rates stayed calm and capped, giving the equity rebound clean air to run |

| Gold | $4,030.20 | +0.5% | Firmed back above $4,030 even on a risk-on day — the metal held its bid as the dollar stayed contained |

| Oil (WTI) | $70.57 | -0.2% | Held near pre-war levels as the geopolitical premium kept bleeding out following the weekend de-escalation |

| Bitcoin | $59,600 | flat | Held near $59.6K — roughly flat as crypto stayed on the sidelines of the equity-led relief rally |

Today’s Charts

Daily candlestick charts with 20/50/200-day moving averages — the index majors, the day’s biggest mover on each side, and the leading sector ETF.

Charts: Finviz (daily). Levels and overlays update through the next session.

Sector Scoreboard

What Drove The Day

Monday was a clean relief rally, and it’s important to call it that. The catalysts were geopolitical and legal, not fundamental: the US and Iran halted the weekend’s tit-for-tat attacks and signaled peace talks were on track, and the Supreme Court rejected the administration’s attempt to remove Fed Governor Lisa Cook, who keeps her seat for now. With the two biggest overhangs lifted at once, the beaten-down mega-caps that drove last week’s 4.6% Nasdaq collapse came roaring back. The Nasdaq Composite jumped 2.07% to 25,820.14, the S&P 500 rose 1.18% to 7,440.43 — finally reclaiming the 7,400 level it had failed at repeatedly — and the Dow climbed 306.63 points to 52,182.74, its first close ever above 52,000. The Dow’s milestone coincided with a structural change: Alphabet officially joined the index, replacing Verizon, and rose nearly 5% in its debut session. The single-stock tape was dominated by corporate action. Space names led the entire market: Iridium Communications soared roughly 25.4% after Rocket Lab agreed to acquire it in an $8B cash-and-stock deal, and Rocket Lab itself rose about 15.9%. Comcast jumped about 9.8% on a plan to split into two independent public companies. But the rebound was uneven, and the divergences are the story for traders. The chip complex did not participate — Micron fell about 6% on memory-pricing and AI-demand-sustainability worries, and the broader semis lagged even as the index ripped, a reminder that the AI-cost anxiety that defined last week hasn’t fully cleared. Verizon was the day’s notable large-cap loser, down about 5.8% on a triple hit: its removal from the Dow and the Russell Top 50 (forcing mechanical index selling), a plan to spin its international enterprise unit into a joint venture with BT Group, and up to $1.55B in second-quarter restructuring charges. The macro confirmed the calmer mood: the VIX collapsed to 17.65, the 10-year held near seven-week lows at 4.38%, WTI eased to $70.57 as the war premium kept draining, and gold firmed to $4,030. The trader’s read into tomorrow is disciplined: a gap-up off de-escalation, led by the same names that just got crushed, is a positioning bounce — not a confirmed trend change. With Chicago PMI, Consumer Confidence and JOLTS all due before noon, Nike and Constellation Brands after the close, and quarter-end flows in play, the move needs to hold its levels before you trust the turn.

MAJOR HEADLINES AND CATALYSTS

Top Market-Moving Stories

- DOW CLOSES ABOVE 52,000 FOR THE FIRST TIME AS TECH RIPS BACK (Day) — The Dow added 306.63 points to 52,182.74, its first-ever close above 52,000, while the Nasdaq jumped 2.07% and the S&P rose 1.18% to 7,440.43. A weekend US-Iran de-escalation and a Supreme Court ruling letting Fed Governor Cook keep her seat lifted the two biggest overhangs at once.

- ALPHABET DEBUTS IN THE DOW, VERIZON DROPS OUT (Day) — Alphabet officially joined the Dow Jones Industrial Average, replacing Verizon, and rose nearly 5% in its first session as a member. Verizon fell ~5.8% on the mechanical index removal, a BT Group JV spinoff plan, and up to $1.55B in Q2 restructuring charges.

- SPACE STOCKS STEAL THE SHOW ON AN $8B DEAL (Day) — Iridium Communications soared ~25.4% after Rocket Lab agreed to acquire it in an $8B cash-and-stock deal; Rocket Lab itself rose ~15.9%. Comcast jumped ~9.8% on a plan to split into two independent public companies. M&A and corporate action drove the single-name tape.

Fed and Macro Context

- The fear premium drained fast — the VIX collapsed to 17.65 (-6.6%) as the weekend de-escalation removed the war risk that spiked volatility last week. The 10-year held calm at 4.38% near seven-week lows, giving the equity rebound clean air to run without a yield shock.

- Oil kept normalizing — WTI eased to $70.57, holding near pre-war levels as the geopolitical premium bled out. A calm, orderly crude tape keeps the disinflationary tailwind alive and takes one variable off the Fed’s plate.

What Changed

- Two overhangs lifted at once — the US-Iran de-escalation and the SCOTUS ruling on Fed independence removed the geopolitical and policy tail risks that drove last week’s selloff. With both gone, the beaten-down mega-caps had room to mean-revert hard, which is exactly what they did.

- But the rebound was narrow — the chip complex (Micron ~-6%) and Verizon lagged badly even as the index ripped. A relief rally led by last week’s biggest losers, with the AI-chip group still leaking, is a bounce that needs confirmation, not a clean all-clear.

AFTER-HOURS EARNINGS SPOTLIGHT

Earnings Reported After 4:05 PM ET Today

- LIGHT POST-CLOSE SLATE — No major names reported after Monday’s bell; the start of the week is typically quiet for earnings, and today was no exception. The first big read lands tomorrow: Nike (NKE) reports fiscal Q4 after Tuesday’s close, alongside Constellation Brands (STZ).

- The after-hours conversation stayed on the day’s M&A and index news — Rocket Lab’s $8B Iridium deal and Comcast’s split plan dominated post-close chatter, while traders positioned for the data wave that begins tomorrow morning.

Regular Session Highlights — Day-Session Movers

- IRDM +25.4% / RKLB +15.9% / CMCSA +9.8% (Day) — Corporate action led the tape. Rocket Lab’s $8B Iridium acquisition powered both names, and Comcast ripped on its plan to split into two public companies. Alphabet (~+5%) debuted in the Dow.

- VZ -5.8% / MU -6.0% (Day) — The day’s notable laggards. Verizon was hit by its Dow removal, a BT JV spinoff and up to $1.55B in charges; Micron sank on memory-pricing and AI-demand worries as the chip complex lagged the broad rebound.

- The mega-caps led the bounce (Day) — Tesla, Amazon and Meta all rode the de-escalation relief higher, reversing chunks of last week’s losses. The recovery was led by exactly the names that fell hardest — a positioning snap-back more than fresh conviction.

NEXT SESSION SETUP — TUESDAY JUNE 30, 2026

Key Calendar (ET)

- A busy data morning — 9:00 AM FHFA Home Price Index (April), 9:45 AM Chicago PMI (June), and the big one at 10:00 AM: June Consumer Confidence and May JOLTS job openings. These offer an early read on whether the labor slowdown is showing up in hiring demand.

- Earnings after the close — Nike (NKE) reports fiscal Q4 (consensus ~$0.13 EPS, revenue ~$10.8B, margins under pressure) alongside Constellation Brands (STZ). And it’s quarter-end / first-half-end, so rebalancing flows can amplify moves.

Events and Risk

- Does the bounce hold? — Today’s rip was a de-escalation relief rally led by last week’s biggest losers. A real trend change needs follow-through with the chip complex stabilizing, not just a one-day mean reversion. Watch whether the S&P holds 7,400 on the open.

- Quarter-end positioning + first data of the week — Tuesday closes Q2 and H1, so window-dressing and rebalancing flows can distort the tape. Layer the Consumer Confidence and JOLTS prints on top and you get a session that can move fast in both directions.

MTC Framework for Tuesday

- Higher timeframe bias: CAUTIOUSLY CONSTRUCTIVE — The S&P reclaimed 7,400, the VIX is back under 18, and rates are calm. But the rebound was narrow and chip-led weakness lingers, so this is a bounce earning the benefit of the doubt, not a confirmed uptrend. Respect both sides.

- Key level: S&P 500 7,400. The index closed at 7,440 just above the shelf it failed at all last week. Hold 7,400 as support on the open and dip-buyers stay in control toward 7,500; lose it and today’s gap looks like a one-day relief pop.

- Confirmation rule: Don’t chase the gap-up off geopolitics. Let price hold the reclaimed level after the open and let the data clear before you trust the turn. No alignment, no trade.

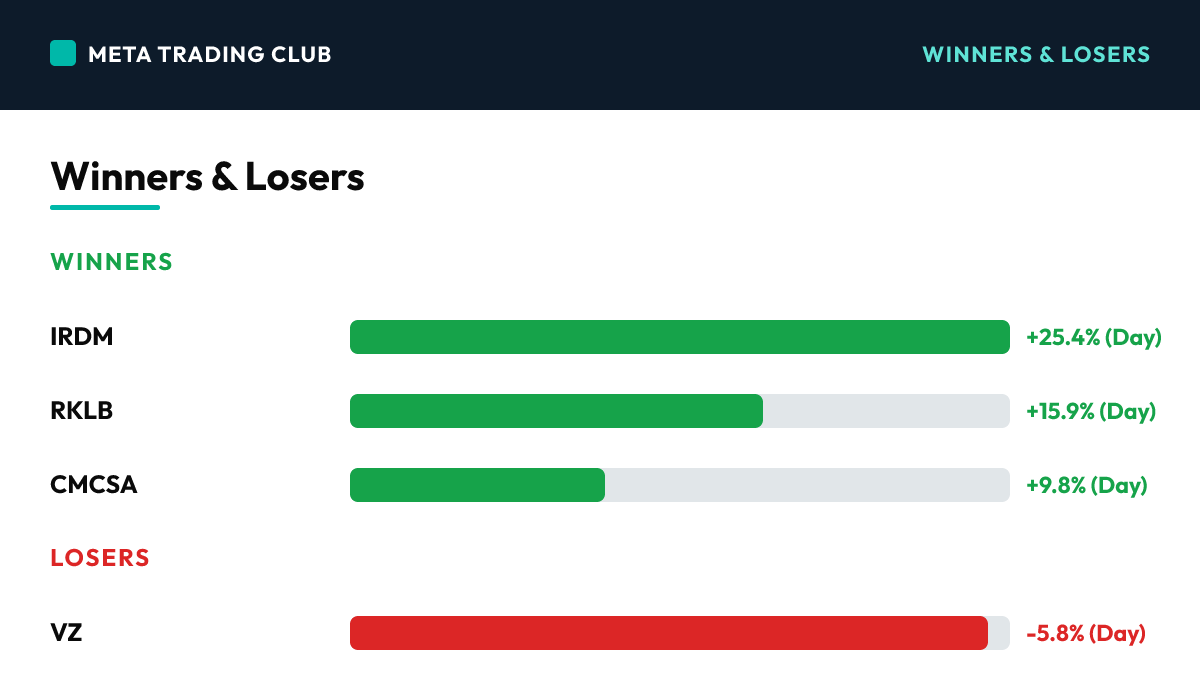

Winners & Losers

Winners

| IRDM | Iridium Communications | +25.4% (Day) | Day Session — soared after Rocket Lab agreed to acquire it in an $8B cash-and-stock deal; the day’s biggest single-name move and the leader of a space-stock surge |

| RKLB | Rocket Lab | +15.9% (Day) | Day Session — jumped on its $8B acquisition of Iridium, with the market rewarding the strategic expansion into satellite communications |

| CMCSA | Comcast | +9.8% (Day) | Day Session — ripped on a plan to split into two independent, publicly traded companies; a structural-unlock story that powered Communication Services |

Losers

| VZ | Verizon | -5.8% (Day) | Day Session — the day’s notable large-cap laggard, hit by its removal from the Dow and Russell Top 50 (mechanical index selling), a BT Group JV spinoff plan, and up to $1.55B in Q2 restructuring charges |

| MU | Micron Technology | -6.0% (Day) | Day Session — sank on memory-pricing and AI-demand-sustainability worries; the chip complex lagged badly even as the broad index ripped 2% |

What It Sets Up For Tomorrow

Levels Into Tomorrow

- SPX 7,400 — The shelf that capped the index all last week, now reclaimed; the S&P closed at 7,440 just above it. Hold 7,400 as support on Tuesday’s open and the relief rally earns follow-through toward 7,500.

- SPX 7,500 / 7,354 — Upside target is the 7,500 round number; downside line is 7,354 (Friday’s close). Lose 7,400 and slip back toward 7,354 and today’s gap-up reads as a one-day positioning pop, not a trend change.

- Data gauntlet at 10:00 AM — Consumer Confidence and JOLTS land mid-morning into quarter-end flows. Price action around those prints sets the tone; don’t pre-position into the number.

Bull case: The two overhangs that drove last week’s selloff are gone — the US-Iran de-escalation drained the war premium (VIX back under 18) and the SCOTUS ruling settled the Fed-independence scare. The S&P reclaimed 7,400, the Dow printed a record above 52,000, rates are calm at 4.38%, and breadth turned positive as the beaten-down mega-caps mean-reverted hard. If the chip complex simply stabilizes and the data tomorrow cooperates, the bounce extends toward 7,500 into the new quarter.

Bear case: Today was a relief rally led by exactly the names that fell hardest — a positioning snap-back, not fresh conviction. The chip complex still leaked (Micron ~-6%), the AI-cost anxiety that defined last week hasn’t cleared, and a gap-up off geopolitics is fragile. If the S&P fails to hold 7,400 on the open, or Consumer Confidence/JOLTS disappoint, the index can give back the gap and slide toward 7,354 as quarter-end flows amplify the reversal.

What We’re Watching

- Chip stabilization — does the semiconductor complex (Micron, the memory names) find a floor and rejoin the rally, or keep lagging? The bounce isn’t trustworthy until the group that led last week’s selloff stops bleeding.

- The 7,400 hold — does the S&P defend the reclaimed shelf on the open, or fade the gap? This is the single cleanest tell for whether today was a turn or a one-day pop.

- 10:00 AM data + quarter-end flows — Consumer Confidence and JOLTS into rebalancing can whip the tape. As long as rates stay capped at 4.38% and the VIX stays under 18, the rebound keeps room to run.

Risks Into Tomorrow

- It’s a Relief Rally, Not a Bottom — Today’s rip was led by the exact mega-caps that got crushed last week, on de-escalation and a SCOTUS ruling — not fresh fundamentals. A positioning snap-back off geopolitics is fragile. Don’t fight the green, but don’t pay up for the gap. Let price hold 7,400 before you trust the turn.

- The Chips Still Lagged — Micron fell ~6% and the semis trailed even as the Nasdaq jumped 2%. The AI-cost anxiety that drove last week hasn’t cleared, just paused. Until the group that led the selloff stops bleeding, the rebound is narrow and incomplete.

- Index Mechanics Move Stocks — Verizon’s ~5.8% drop on its Dow removal and Alphabet’s ~5% pop on joining are a reminder that passive flows are real money. Reconstitution and rebalancing into quarter-end can drive moves that have nothing to do with the underlying business. Mind the calendar, not just the chart.

Frequently Asked Questions

How did the S&P 500 close today?

On Monday, June 29, 2026, the S&P 500 closed at 7,440.43 (+1.18%), with the VIX at 17.65. After one of the ugliest weeks of the year, the tape did more than exhale — it ripped.

What drove the market today?

DOW CLOSES ABOVE 52,000 FOR THE FIRST TIME AS TECH RIPS BACK (Day) — The Dow added 306.63 points to 52,182.74, its first-ever close above 52,000, while the Nasdaq jumped 2.07% and the S&P rose 1.18% to 7,440.43. A weekend US-Iran de-escalation and a Supreme Court ruling letting Fed Governor Cook keep her seat lifted the two biggest overhangs at once.

What levels matter for tomorrow?

SPX 7,400 — The shelf that capped the index all last week, now reclaimed; the S&P closed at 7,440 just above it. Hold 7,400 as support on Tuesday’s open and the relief rally earns follow-through toward 7,500. SPX 7,500 / 7,354 — Upside target is the 7,500 round number; downside line is 7,354 (Friday’s close). Lose 7,400 and slip back toward 7,354 and today’s gap-up reads as a one-day positioning pop, not a trend change. Data gauntlet at 10:00 AM — Consumer Confidence and JOLTS land mid-morning into quarter-end flows. Price action around those prints sets the tone; don’t pre-position into the number.

How does Meta Trading Club prepare for the next session?

We wrap every session and carry the read forward through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

New to this? Start with the free training.

Learn how we read the market before you risk a dollar — our free education library and ebook break down the fundamentals step by step.

Free education → Get the free ebookThe session’s over. The prep isn’t.

This is how MTC members close each day — wrap what happened, mark the levels, and carry one clean read into tomorrow. If you want to build that habit and qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process. It’s application-based — see if it’s a fit.

Explore the MTC Incubator → Apply nowSources: Yahoo Finance | CNBC | TheStreet | Investing.com | Benzinga — June 29, 2026. For educational purposes only. Not financial advice.