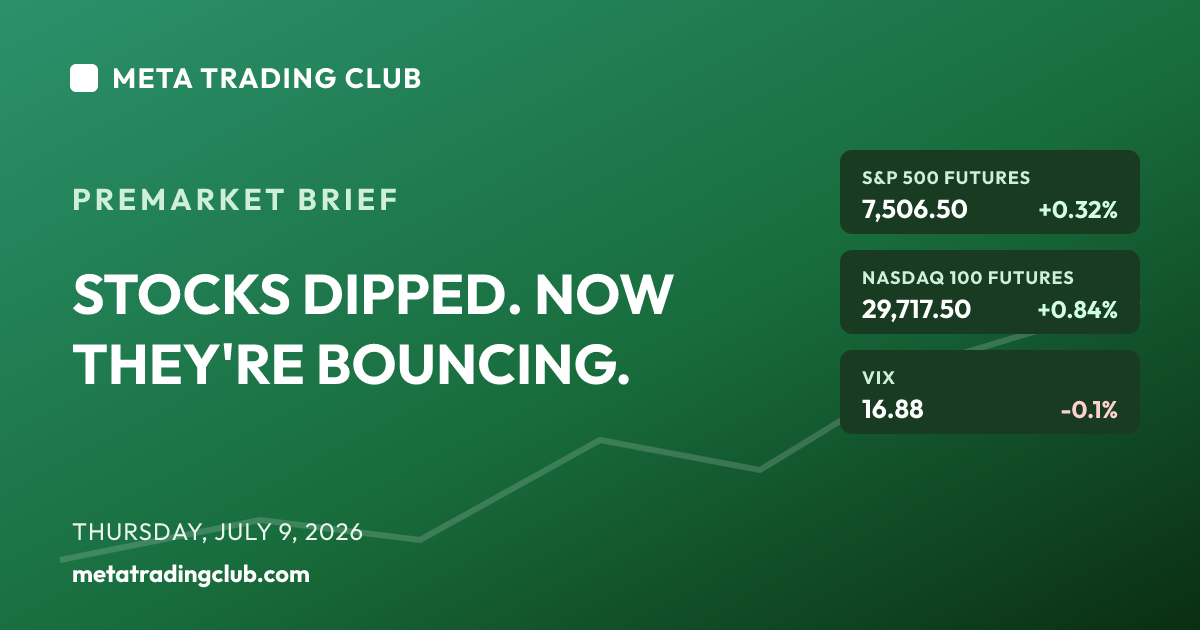

Thursday, July 9, 2026 · 4:30 PM ET · MTC Market Close

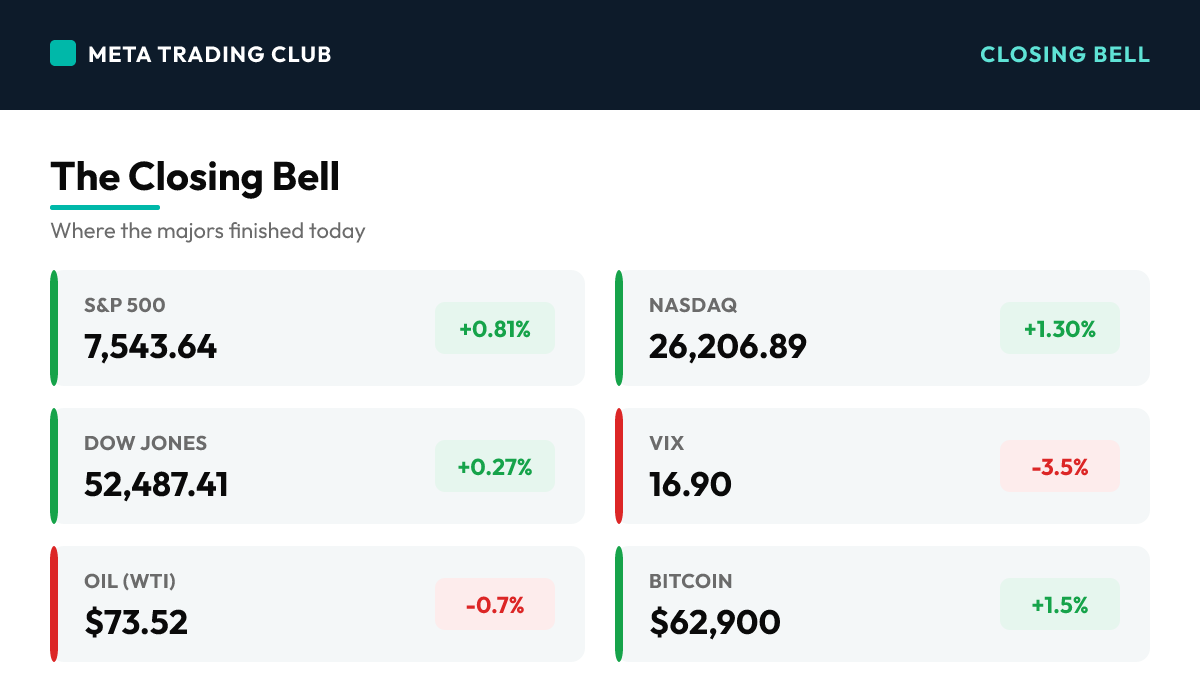

One day after the Iran oil shock knocked the Dow down 577, the tape flipped the script and did it on the back of a single group: semiconductors. A Micron-led chip surge powered a broad rebound and pulled the S&P 500 back above the 7,500 shelf it had just surrendered. The S&P rose 0.81% to 7,543.64, the Nasdaq jumped 1.30% to 26,206.89, the Dow added 139.02 points (+0.27%) to 52,487.41, and even the Russell 2000 joined, up 1.22% to 2,992.55. Four green indices — index-level alignment came back. The engine was clear: Micron rallied more than 7% after pledging up to $250 billion of US investment through 2035, and the whole chip complex went with it — ON Semiconductor +9.3%, AMD +7.2%, Applied Materials +7%, Broadcom +4.8%, the Philadelphia Semiconductor index up roughly 4.6%. Oil cooled off the prior day’s spike — WTI eased to $73.52 — which took the inflation fear off the table even as US forces struck Iran for a second straight day. The VIX slipped back to 16.90 and Bitcoin held above $62,000. But here’s the catch the recap has to name: the strength was narrow. The same session that lit up hardware chips punished software and hyperscalers — Alphabet fell about 2.5% and was the single biggest drag on both the S&P and the Nasdaq, while the Dow was held back by IBM, Salesforce, Microsoft, Coca-Cola, Disney and Procter & Gamble. The 10-year held near 4.55%. So the reclaim is real, but it rode one engine. Into Friday, the SK Hynix US listing gives the chip trade its next test and Delta opens the airline read. The lesson: reclaiming a level is a start, not a confirmation — a rally carried by one group has to prove it can broaden before you trust it. Alignment you can trade is alignment across the whole tape.

The Closing Bell

| Instrument | Close | Change | Note |

|---|---|---|---|

| S&P 500 | 7,543.64 | +0.81% | Reclaimed the 7,500 shelf it surrendered Wednesday, closing back above it as a semiconductor surge carried the tape — a clean recovery, but one led by a single group |

| Nasdaq | 26,206.89 | +1.30% | Led the rebound as chips ripped — Micron, AMD, ON Semi and Broadcom all rallied hard; the day’s clear leadership index even with software names lagging |

| Dow Jones | 52,487.41 | +0.27% | Recovered a fraction of Wednesday’s 577-point drop; the smallest gainer, held back by IBM, Salesforce, Microsoft and consumer names Coca-Cola, Disney and P&G |

| Russell 2000 | 2,992.55 | +1.22% | Small caps joined the rebound with a solid gain — a healthier breadth signal than the megacap-only tape, even as the leadership sat squarely in chips |

| VIX | 16.90 | -3.5% | Fear gauge eased back toward the mid-16s as the oil scare faded and equities rebounded — the opposite of Wednesday’s near-9% spike |

| 10-Yr Yield | 4.55% | flat | Held near 4.55%, a two-week-high, as the cooling oil price took some inflation pressure off but the hawkish Fed read from the minutes kept yields firm |

| Gold | $4,075.00 | -0.4% | Slipped modestly as the risk-on rebound and firm yields sapped the safe-haven bid that had supported it during the prior day’s geopolitical scare |

| Oil (WTI) | $73.52 | -0.7% | Gave back part of Wednesday’s 5% spike as the market looked past a second day of US strikes on Iran — the cooling that let equities rebound |

| Bitcoin | $62,900 | +1.5% | Steadied above $62,000 as risk appetite returned and the broad de-risking tone from the Iran shock eased across assets |

Today’s Charts

Daily candlestick charts with 20/50/200-day moving averages — the index majors, the day’s biggest mover on each side, and the leading sector ETF.

Charts: Finviz (daily). Levels and overlays update through the next session.

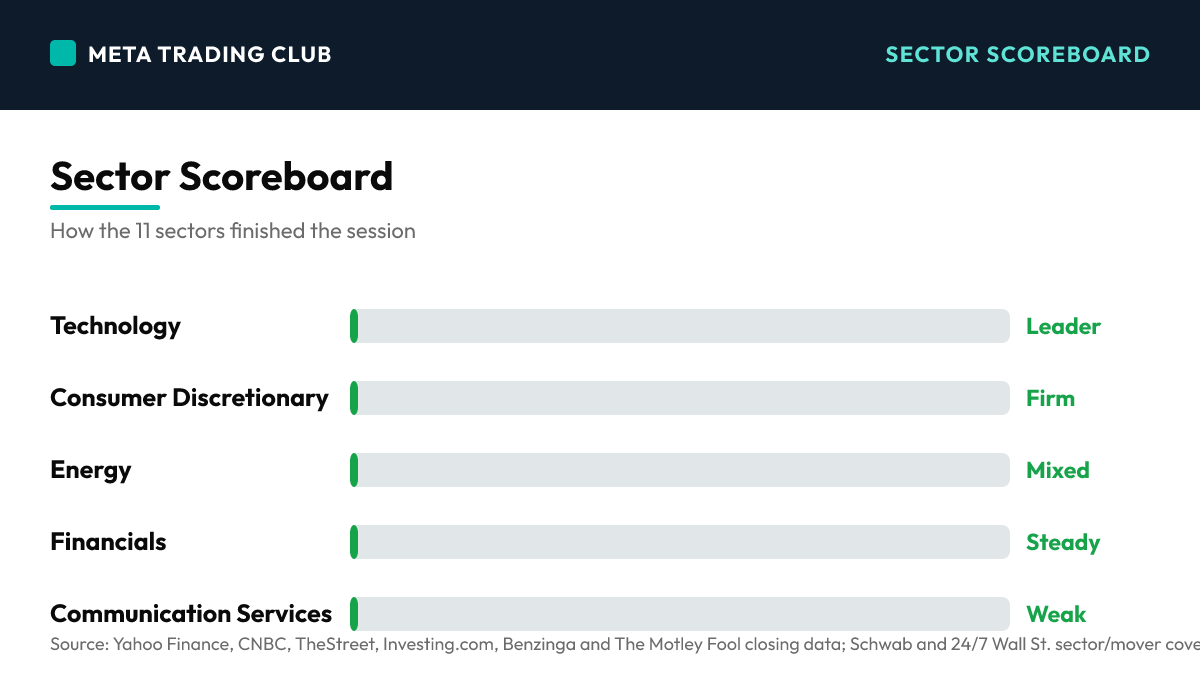

Sector Scoreboard

What Drove The Day

Thursday was a rebound day with a single engine, and the engine was chips. One session after the Iran oil shock sent the Dow down 577 points and knocked the S&P back below 7,500, semiconductors came roaring back and dragged the whole tape with them. The catalyst had a name: Micron Technology rallied more than 7% after announcing it would invest up to $250 billion in the US through 2035 to strengthen the domestic chip supply chain. The rest of the complex followed — ON Semiconductor jumped 9.3%, Advanced Micro Devices climbed 7.2%, Applied Materials rose about 7%, Broadcom added 4.8%, Nvidia gained 3.7%, and the Philadelphia Semiconductor Index rose roughly 4.6%. That lifted the Nasdaq 1.30% to 26,206.89 and pushed the S&P 500 up 0.81% to 7,543.64, reclaiming the 7,500 level it had surrendered on Wednesday. The Dow added 139.02 points (+0.27%) to 52,487.41, and the Russell 2000 rose 1.22% to 2,992.55 — four green indices, index-level alignment restored after Wednesday’s split. Helping the mood: oil cooled. WTI eased to $73.52, giving back part of the prior day’s 5% surge even as US forces struck Iran for a second straight day and President Trump kept the Strait of Hormuz threat alive. With the inflation scare off the boil, the VIX slipped to 16.90 and Bitcoin held above $62,000. But the recap has to name the catch, because it matters for tomorrow: the strength was narrow. The same rally that lit up hardware semis came at the expense of software and the hyperscalers. Alphabet fell about 2.5% and was the single biggest drag on both the S&P 500 and the Nasdaq, and the Dow was capped by weakness in IBM, Salesforce, Microsoft, Coca-Cola, Disney and Procter & Gamble. So the leadership was concentrated in one group rather than spread across the market. The 10-year Treasury held near 4.55%, a two-week high, as the cooling oil eased inflation fear but the hawkish June minutes kept a floor under yields; gold slipped about 0.4% to roughly $4,075 as the safe-haven bid faded. Into Friday, the SK Hynix US listing gives the chip trade its next verdict and Delta Air Lines opens the airline read after the week’s oil swings. The lesson is the one that separates a reclaim from a trend: getting back above a level is a start, but a rally carried by a single group has to prove it can broaden before it earns your trust. One engine can pull the tape up for a day. Confirmation is when the whole market pulls with it.

MAJOR HEADLINES AND CATALYSTS

Top Market-Moving Stories

- CHIPS LEAD THE REBOUND — MICRON’S $250B PLEDGE SPARKS A SEMI SURGE (Day) — Micron rose more than 7% after pledging up to $250 billion of US investment through 2035, and the whole complex followed: ON Semi +9.3%, AMD +7.2%, Applied Materials +7%, Broadcom +4.8%, the SOX up ~4.6%. That single group carried the Nasdaq up 1.3% and the S&P back over 7,500.

- S&P RECLAIMS 7,500 AS ALL FOUR INDICES CLOSE GREEN (Day) — The S&P rose 0.81% to 7,543.64, the Nasdaq +1.30%, the Dow +0.27% and the Russell 2000 +1.22% — index-level alignment restored after Wednesday’s split tape. Oil cooling to $73.52 took the inflation fear off the table and the VIX eased to 16.90.

- THE CATCH — SOFTWARE AND HYPERSCALERS LAGGED (Day) — The rally that lit up hardware chips punished the other side of tech: Alphabet fell about 2.5% and was the single biggest drag on both the S&P and Nasdaq, while IBM, Salesforce and Microsoft held the Dow back. Strong index prints, narrow leadership underneath.

Fed and Macro Context

- Oil did the heavy lifting for sentiment: WTI eased to $73.52, giving back part of Wednesday’s 5% spike even as US forces struck Iran for a second straight day. With the crude scare cooling, the market was willing to look past the geopolitical headline and buy the chip leaders.

- The 10-year Treasury held near 4.55%, a two-week high — the cooling oil eased the inflation channel, but the hawkish June FOMC minutes kept a floor under yields and gold slipped about 0.4% to roughly $4,075 as the safe-haven bid faded.

- Cross-asset, risk came back on: the VIX fell to 16.90 from Wednesday’s spike, Bitcoin held above $62,000, and small caps joined the move with the Russell 2000 up 1.22% — a broader breadth signal than a megacap-only tape.

Single-Stock Standouts

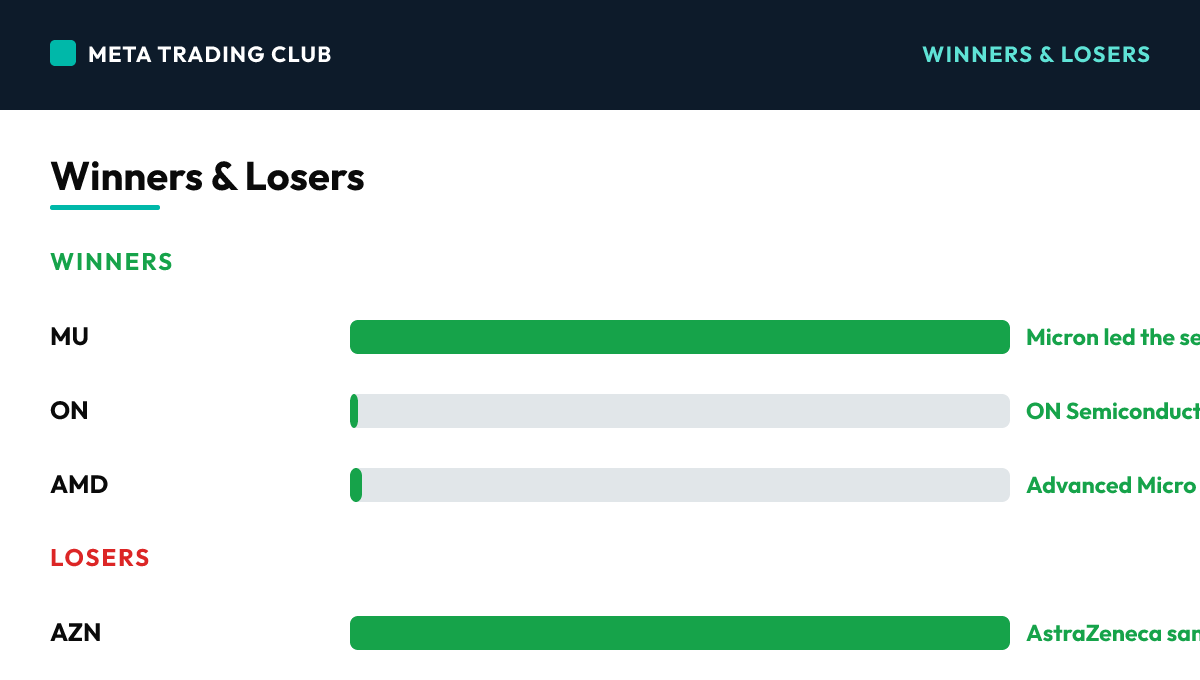

- Semis were the day’s clear winners: Micron +7%+ on its $250B US investment pledge, ON Semiconductor +9.3%, AMD +7.2%, Applied Materials +7%, Broadcom +4.8% and Nvidia +3.7% — the group that carried every index higher.

- AstraZeneca fell nearly 8% after its heart-disease drug Wainua failed to meet its primary endpoint in a late-stage trial — the day’s biggest single-stock casualty and a reminder that binary drug data cuts hard.

- Alphabet slid about 2.5% as money rotated out of the hyperscalers into hardware chips, and Levi Strauss fell more than 4% despite a top- and bottom-line beat — a beat that still sold off is a tell about positioning.

AFTER-HOURS EARNINGS SPOTLIGHT

Tonight’s Slate

- A light post-close slate — no major after-hours earnings tonight. The notable post-market item was Costco’s June sales update: net sales of about $29.24 billion for the five weeks ended July 5, up 10.6%, with US comparable sales also up 10.6% — a firm read on the consumer heading into Friday.

- Monster Beverage declared a two-for-one stock split. The real earnings catalyst is tomorrow: Delta Air Lines opens the airline read after a week of oil swings, and the SK Hynix US listing gives the semiconductor trade its next verdict.

NEXT SESSION SETUP

Friday, July 10 — SK Hynix Lists, Delta Opens the Airline Read

- The SK Hynix US listing debuts Friday — a direct test of whether Thursday’s memory-chip enthusiasm is real conviction or a one-day squeeze. It lands right as the semiconductor trade is trying to prove this week’s rebound can hold.

- Delta Air Lines reports before Friday’s open — the first real airline read after a week where a 5% oil spike and then a cooldown whipsawed the fuel-sensitive names. The guidance matters more than the print for the whole travel complex.

- Iran headlines stay the wild card: US forces struck for a second day and Trump kept the Strait of Hormuz threat live. Any re-escalation puts a bid back under crude and re-tests the inflation fear that oil’s cooldown just relieved.

Winners & Losers

Winners

| MU | +7.5% | Micron led the semiconductor surge after pledging up to $250 billion of US investment through 2035 — the single catalyst that sparked the whole chip rebound | |

| ON | +9.3% | ON Semiconductor was the biggest chip gainer as the whole complex rallied on the Micron-led enthusiasm and a China semiconductor bid | |

| AMD | +7.2% | Advanced Micro Devices jumped with the group as the Philadelphia Semiconductor Index rose about 4.6% to lead every major index higher |

Losers

| AZN | -8.0% | AstraZeneca sank nearly 8% after its heart-disease drug Wainua failed to meet its primary endpoint in a late-stage clinical trial — the day’s biggest single-stock casualty | |

| LEVI | -4.0% | Levi Strauss fell more than 4% despite beating on the top and bottom line — a beat that still sold off, a tell about stretched positioning | |

| GOOGL | -2.5% | Alphabet slid about 2.5% and was the single biggest drag on both the S&P and the Nasdaq as money rotated out of hyperscalers into hardware chips |

What It Sets Up For Tomorrow

Levels Into Tomorrow

- S&P 500 7,500 — THE PIVOT, RECLAIMED FROM BELOW. Surrendered Wednesday, won back Thursday with a 7,543 close. Hold above 7,500 Friday and the Iran oil shock reads as a one-day event; lose it again and the reclaim was a fake-out.

- S&P 500 7,610 — the record-chase zone from earlier this month. Reclaim 7,500 as support and broaden the leadership beyond chips, and this level is back on the table.

- S&P 500 7,400 — the line in the sand. Lose 7,500 and then the 7,480 area and this is the next real support; a break here turns a two-day chop into a genuine trend change.

Bull case: The chip rebound is the start of a broader recovery: oil stays cool, the SK Hynix listing confirms real memory-chip demand, the S&P holds 7,500 as support, leadership broadens beyond semis into software and cyclicals, and the tape grinds back toward the 7,610 record zone.

Bear case: Thursday’s rally proves to be a narrow, one-group squeeze: the semis fade after the SK Hynix debut, software stays heavy with Alphabet leading the drag, Iran re-escalates and puts a bid back under oil, and the S&P loses 7,500 again toward 7,400 as the reclaim fails.

What We’re Watching

- Breadth, not the headline number — does the advance broaden beyond semiconductors into software, financials and cyclicals, or does one group keep carrying the whole tape? That’s the difference between a trend and a squeeze.

- The SK Hynix US listing — the cleanest live read on whether Thursday’s memory-chip enthusiasm is durable demand or a one-session pop.

- Crude oil and Iran headlines — WTI cooling to $73.52 is what let equities rebound; any re-escalation that puts a bid back under oil re-tests the inflation fear that just eased.

Risks Into Tomorrow

- Narrow leadership — The rebound was carried by one group — semiconductors — while software and hyperscalers lagged and Alphabet led the drag. Index-level alignment came back with all four indices green, but a rally concentrated in a single sector has to broaden before it earns trust. One engine can lift the tape for a day; confirmation is when the whole market pulls with it.

- Iran remains live — US forces struck Iran for a second straight day and Trump kept the Strait of Hormuz threat alive. Oil’s cooldown to $73.52 is what let equities rebound — any re-escalation puts a bid back under crude and re-tests the inflation fear that just relieved the tape.

- Firm yields, hawkish Fed — The 10-year held near 4.55%, a two-week high, and gold slipped as the safe-haven bid faded. With the June minutes leaning hawkish, a floor under yields caps how far a risk-on rebound can run before higher-for-longer bites again.

Frequently Asked Questions

How did the S&P 500 close today?

On Thursday, July 9, 2026, the S&P 500 closed at 7,543.64 (+0.81%), with the VIX at 16.90. One day after the Iran oil shock knocked the Dow down 577, the tape flipped the script and did it on the back of a single group: semiconductors.

What drove the market today?

CHIPS LEAD THE REBOUND — MICRON’S $250B PLEDGE SPARKS A SEMI SURGE (Day) — Micron rose more than 7% after pledging up to $250 billion of US investment through 2035, and the whole complex followed: ON Semi +9.3%, AMD +7.2%, Applied Materials +7%, Broadcom +4.8%, the SOX up ~4.6%. That single group carried the Nasdaq up 1.3% and the S&P back over 7,500.

What levels matter for tomorrow?

S&P 500 7,500 — THE PIVOT, RECLAIMED FROM BELOW. Surrendered Wednesday, won back Thursday with a 7,543 close. Hold above 7,500 Friday and the Iran oil shock reads as a one-day event; lose it again and the reclaim was a fake-out. S&P 500 7,610 — the record-chase zone from earlier this month. Reclaim 7,500 as support and broaden the leadership beyond chips, and this level is back on the table. S&P 500 7,400 — the line in the sand. Lose 7,500 and then the 7,480 area and this is the next real support; a break here turns a two-day chop into a genuine trend change.

How does Meta Trading Club prepare for the next session?

We wrap every session and carry the read forward through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

New to this? Start with the free training.

Learn how we read the market before you risk a dollar — our free education library and ebook break down the fundamentals step by step.

Free education → Get the free ebookThe session’s over. The prep isn’t.

This is how MTC members close each day — wrap what happened, mark the levels, and carry one clean read into tomorrow. If you want to build that habit and qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process. It’s application-based — see if it’s a fit.

Explore the MTC Incubator → Apply nowSources: Yahoo Finance, CNBC, TheStreet, Investing.com, Benzinga and The Motley Fool closing data; Schwab and 24/7 Wall St. sector/mover coverage; Costco investor release and company filings — verified as of 4:30 PM ET July 9, 2026. For educational purposes only. Not financial advice.