Thursday, July 2, 2026 · 4:30 PM ET · MTC Market Close

The jobs report answered the rate-hike question — and split the tape in two. June payrolls printed just 57,000 against 115,000 expected, with May revised down to 129,000. Unemployment ticked down to 4.2%, but for the wrong reason: participation fell 0.3 points to 61.5%, the lowest since March 2021. Soft is soft — the ~29% rate-hike odds that had built into this month’s Fed meeting got buried at 8:30 AM, and the rate-relief trade fired instantly. The 2-year yield eased roughly 3.5 basis points to about 4.13%, gold ripped 2.3% back above $4,100 to $4,122.76 — one day after sealing its worst quarter since 2013 under $4,000 — and Bitcoin jumped more than 6% to reclaim $61,800. In equities, the money went two directions at once. The Dow surged 594.83 points, or 1.14%, to a record close at 52,900.07 behind Apple +4.8%, McDonald’s +4.1%, and Disney +3.8%, with financials, healthcare, and materials leading the rotation into traditional names. The Nasdaq fell 0.80% to 25,832.67 as the semiconductor unwind hit day two — Micron -7%, Marvell -10%, Applied Materials -10%, SanDisk -13% — after an overnight rout in Asian chip names (SK Hynix -14%, Samsung -9%). And the S&P 500 closed dead flat at 7,483.24, up a hundredth of a point, pinned 17 points under 7,500 as the Dow’s record and the Nasdaq’s bleed canceled each other out. Tesla was the single-stock story: down 8% to 391.28 despite record Q2 deliveries of 480,126 — up 25% year over year and well above consensus near 400K — because US demand fell roughly 20% after the EV-credit expiry and Europe’s +108% did the lifting. Classic sell-the-news. After the close the slate was light — holiday eve, no major reports. Markets are closed Friday for July 4th; the next session is Monday, July 6, with FOMC minutes Wednesday. A dead-flat index pinned under its round number heading into a three-day weekend is the market telling you it hasn’t decided. No alignment, no trade.

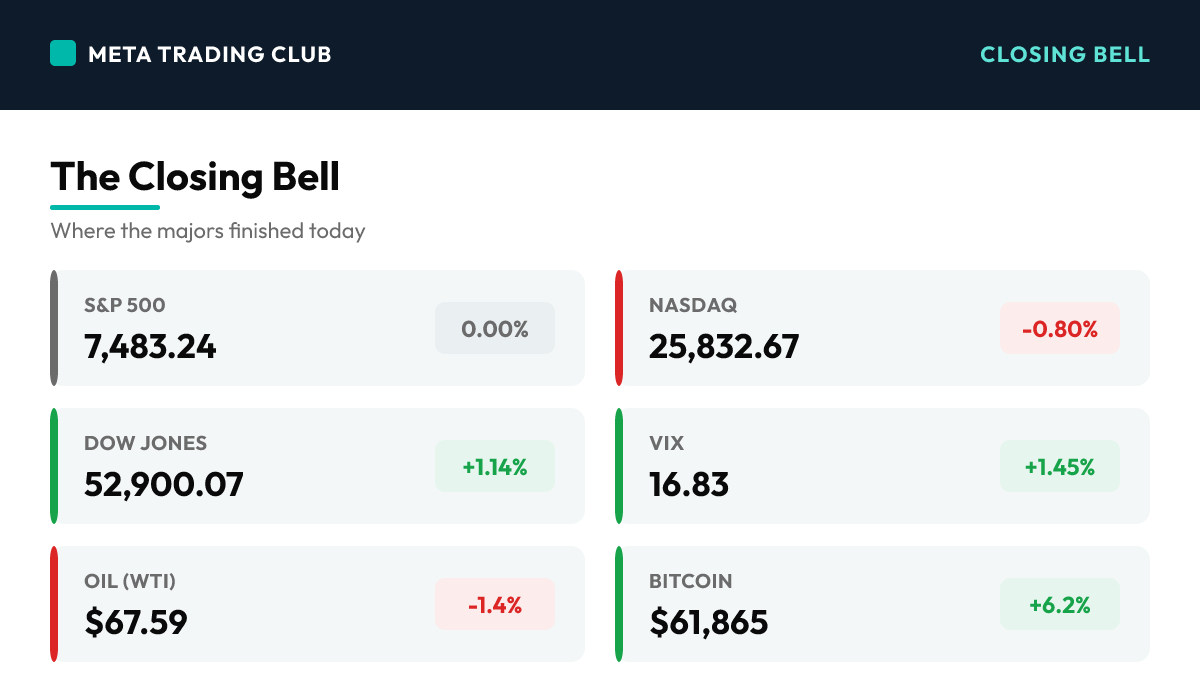

The Closing Bell

| Instrument | Close | Change | Note |

|---|---|---|---|

| S&P 500 | 7,483.24 | 0.00% | Closed dead flat — up a hundredth of a point — as the Dow’s record rally and the Nasdaq’s semiconductor bleed canceled out; still pinned 17 points under 7,500 |

| Nasdaq | 25,832.67 | -0.80% | Fell 207 points as the chip unwind hit day two — Micron -7%, Marvell -10%, Applied Materials -10%, SanDisk -13% — after an overnight rout in Asian semis |

| Dow Jones | 52,900.07 | +1.14% | Surged 594.83 points to a record close behind Apple +4.8%, McDonald’s +4.1%, and Disney +3.8% as soft jobs data fueled the rotation into traditional names |

| Russell 2000 | 2,980.05 | -1.08% | Small caps lagged despite the rate-relief bid, giving back Wednesday’s strength and slipping back below 3,000 into the holiday weekend |

| VIX | 16.83 | +1.45% | Ticked up modestly but stayed in the mid-16s — a two-sided tape with a record Dow and a bleeding Nasdaq reads as rotation, not fear |

| 10-Yr Yield | 4.49% | +1bp | The long end barely moved while the 2-year eased ~3.5bp to about 4.13% after the soft jobs print buried hike odds; bond market closed early at 2 PM |

| Gold | $4,122.76 | +2.3% | Ripped back above $4,100 one day after sealing its worst quarter since 2013 below $4,000 — the soft jobs print revived the rate-relief bid for the metal |

| Oil (WTI) | $67.59 | -1.4% | Slipped toward four-month lows as US-Iran denuclearization talks reportedly progressed, keeping supply-risk premium out of the barrel |

| Bitcoin | $61,865 | +6.2% | Jumped more than 6% to extend its reclaim of $60,000, moving in lockstep with gold as the rate-relief trade fired across hard and digital assets |

Today’s Charts

Daily candlestick charts with 20/50/200-day moving averages — the index majors, the day’s biggest mover on each side, and the leading sector ETF.

Charts: Finviz (daily). Levels and overlays update through the next session.

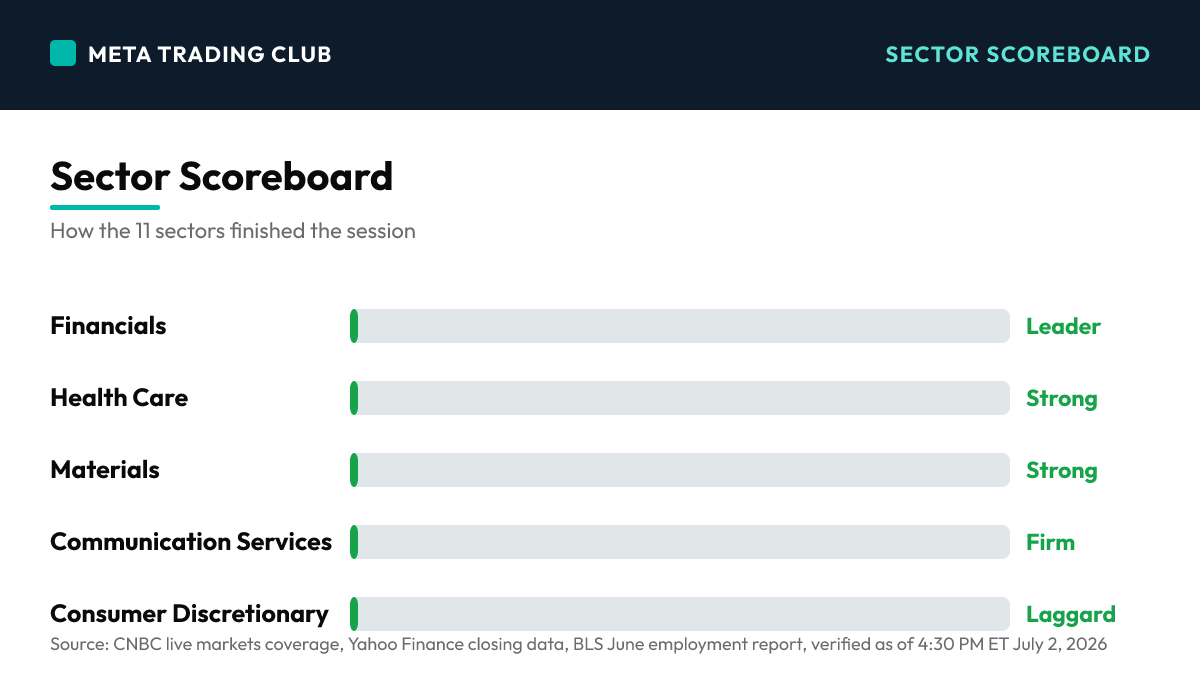

Sector Scoreboard

What Drove The Day

The 8:30 AM jobs print set the day’s script and the tape followed it to the close. June nonfarm payrolls rose just 57,000 against expectations near 115,000, with May revised down to 129,000. The unemployment rate ticked down to 4.2% versus 4.3% expected — but the decline came from the wrong side of the ledger: labor-force participation dropped 0.3 points to 61.5%, the lowest since March 2021. Under the hood the composition was soft too — leisure and hospitality shed 61,000 jobs, while healthcare (+22K), professional and business services (+36K), and social assistance (+25K) carried what growth there was. For a market that had priced roughly 29% odds of a rate HIKE at this month’s Fed meeting, the print was decisive: the hike case got buried, the 2-year yield eased about 3.5 basis points to around 4.13%, and the long end sat still with the 10-year near 4.49% into an early 2 PM bond-market close. The equity response was a clean split. The Dow ripped 594.83 points higher, 1.14%, to a record close at 52,900.07 — its leaders telling the rotation story plainly: Apple +4.8%, McDonald’s +4.1%, Disney +3.8%, with financials, healthcare, and materials the leading sectors. The Nasdaq went the other way, down 0.80% to 25,832.67, because the semiconductor unwind that started Wednesday got a second, heavier day: Micron fell another 7%, Marvell dropped 10%, Applied Materials lost 10%, and SanDisk collapsed 13%. The selling was seeded overnight in Asia, where SK Hynix fell 14% and Samsung 9% in a memory-complex rout. Yesterday’s line was that a second straight day of double-digit damage in the chip leaders would shift the read from rotation toward distribution — that second day just happened, and the question is now live. Caught in the middle, the S&P 500 closed at 7,483.24, higher by a hundredth of a point — dead flat, pinned 17 points below 7,500 for a second straight session. The single-stock story was Tesla, down 8% to 391.28 despite record Q2 deliveries of 480,126 vehicles — up 25% year over year and well above consensus near 400,000. The market sold the composition: US demand fell roughly 20% after the EV tax-credit expiry, and Europe’s +108% surge did the lifting. A blowout headline number met a deteriorating home market, and the stock paid for the difference. Cross-asset, the rate-relief trade was emphatic — gold surged 2.3% to $4,122.76, back above $4,100 one day after closing its worst quarter since 2013 under $4,000, silver held near $60.31, and Bitcoin jumped more than 6% to $61,865, extending Wednesday’s reclaim of $60K. Elsewhere, scooter operator Lime edged up 2.3% to $26.70 in its Nasdaq debut after raising $167 million, and ULA launched 29 satellites for Amazon’s Leo constellation. After the bell, the earnings slate was light — holiday eve, no major reports. Markets are closed Friday for Independence Day; the next session is Monday, July 6, with FOMC minutes due Wednesday, July 8. A flat index under its round number into a three-day weekend is a market that hasn’t chosen a direction — and pretending it has is how traders donate money. No alignment, no trade.

MAJOR HEADLINES AND CATALYSTS

Top Market-Moving Stories

- SOFT JOBS BURIES THE HIKE CASE, DOW PRINTS A RECORD (Day) — June payrolls rose just 57K vs 115K expected (May revised down to 129K), unemployment fell to 4.2% only because participation dropped to 61.5%, the lowest since March 2021. The ~29% rate-hike odds priced for this month’s Fed meeting collapsed, and the Dow surged 594.83 points (+1.14%) to a record 52,900.07.

- SEMI UNWIND HITS DAY TWO — DISTRIBUTION QUESTION NOW LIVE (Day) — Micron -7%, Marvell -10%, Applied Materials -10%, SanDisk -13% after an overnight Asian memory rout (SK Hynix -14%, Samsung -9%). Yesterday’s test was whether the chip selling would get a second day — it did, and the Nasdaq fell 0.80% to 25,832.67 while the rest of the tape rallied.

- TESLA -8% ON RECORD DELIVERIES (Day) — Q2 deliveries hit 480,126, up 25% year over year and well above consensus near 400K, but the stock fell 8% to 391.28 because US demand dropped roughly 20% post-EV-credit expiry and Europe’s +108% did the lifting. A blowout headline met a weakening home market — classic sell-the-news.

Fed and Macro Context

- The jobs print landed directly on the rate-hike debate and settled it for now — the 2-year yield eased ~3.5bp to about 4.13% while the 10-year held near 4.49% into an early 2 PM bond close. Composition was soft: leisure/hospitality -61K, with healthcare (+22K), professional services (+36K), and social assistance (+25K) carrying the growth.

- Fed Chair Kevin Warsh said Wednesday that “inflation risks have come down” — with May CPI at 4.2%, the highest readings since 2023, today’s soft payrolls give the Fed room to stay on hold rather than validate the hike chatter that built after Wednesday’s hot ISM print.

- The rate-relief trade fired across hard and digital assets — gold ripped 2.3% to $4,122.76, back above $4,100 one day after sealing its worst quarter since 2013, silver held near $60.31, and Bitcoin jumped more than 6% to $61,865, extending its reclaim of $60K.

Single-Stock Standouts

- The Dow’s leaders told the rotation story plainly — Apple +4.8%, McDonald’s +4.1%, and Disney +3.8% powered the record close as money rotated from extended chip winners into mega-cap quality and traditional names.

- Scooter operator Lime edged up 2.3% to $26.70 in its Nasdaq debut under ticker LIME after raising $167 million — a quiet but functioning IPO window even on a holiday-eve tape.

- ULA launched 29 satellites for Amazon’s Leo broadband constellation, and US-Iran denuclearization talks reportedly progressed — helping keep WTI near four-month lows at $67.59 with supply-risk premium out of the barrel.

AFTER-HOURS EARNINGS SPOTLIGHT

Tonight’s Slate

- A light night — holiday eve, no major earnings reports after the close. With markets shut Friday for July 4th, positioning squared up into the long weekend rather than around any post-close catalyst.

- The day’s defining ‘report’ came premarket from Tesla’s delivery numbers, not the earnings tape — 480,126 Q2 deliveries, +25% year over year, sold 8% on weak US composition. The reaction is the lesson: composition beats headline.

NEXT SESSION SETUP

Monday, July 6 — Back From the Long Weekend

- MARKETS CLOSED FRIDAY, JULY 3 for Independence Day — Monday, July 6 is the next session, and it opens on three days of accumulated headlines with the S&P pinned dead flat at 7,483.24, 17 points under 7,500. Gap risk cuts both ways after a long weekend.

- FOMC MINUTES WEDNESDAY, JULY 8 — the first read on how seriously the committee discussed the hike scenario before today’s soft jobs print buried it. ISM Services PMI also lands during the week, testing whether the services side confirms the cooling labor market.

- Watch the semis for day three — two straight days of heavy selling in Micron, Marvell, and the memory complex has shifted the question from rotation to possible distribution. Stabilization Monday keeps the bull structure intact; a third day of double-digit damage changes the character of the tape.

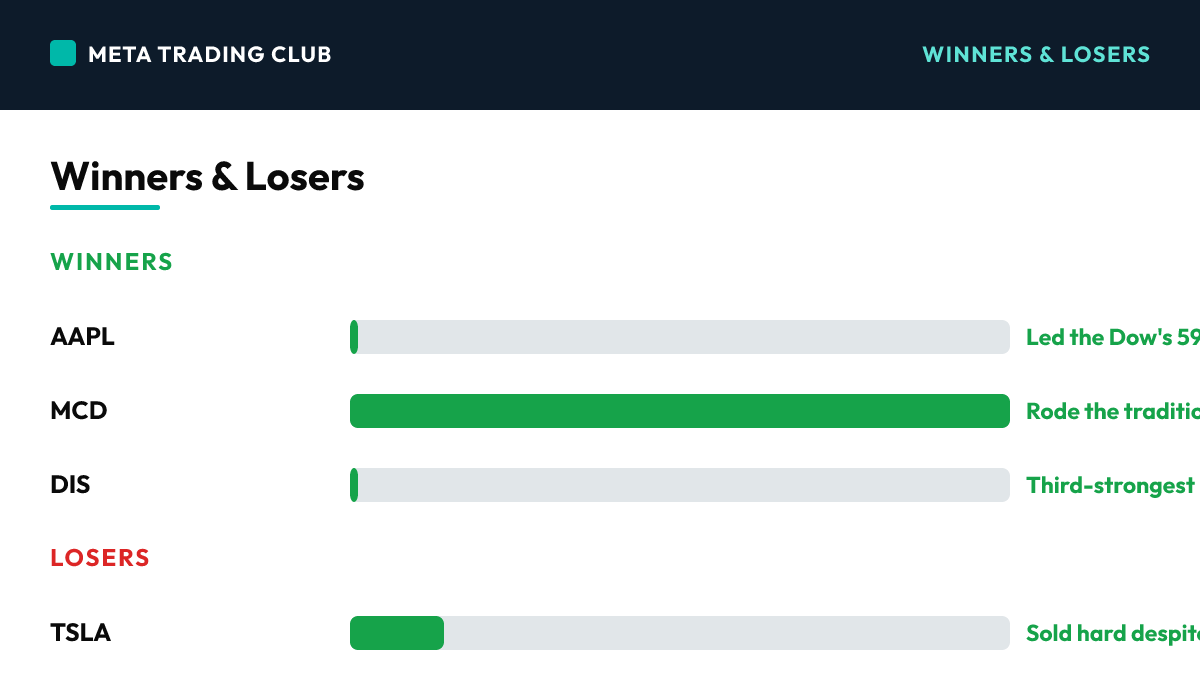

Winners & Losers

Winners

| AAPL | +4.8% | Led the Dow’s 594-point record rally as rotation money moved from extended chip winners into mega-cap quality on the soft jobs print | |

| MCD | +4.1% | Rode the traditional-economy rotation bid to help power the Dow’s record close at 52,900.07 | |

| DIS | +3.8% | Third-strongest Dow name as communication services held Wednesday’s rotation gains and defensive-growth got paid |

Losers

| TSLA | -8.0% | Sold hard despite record Q2 deliveries of 480,126 (+25% YoY) — US demand fell ~20% post-EV-credit expiry and the market sold the composition; closed 391.28 | |

| SNDK | -13.0% | Collapsed as the memory-complex rout went global — SK Hynix -14% and Samsung -9% overnight seeded day two of the US semi unwind | |

| MRVL | -10.0% | Double-digit damage on day two of the chip selloff alongside Applied Materials -10% and Micron -7% — the distribution question is now live |

What It Sets Up For Tomorrow

Levels Into Tomorrow

- S&P 500 7,500 — THE PIVOT. Two straight closes pinned 17 points under the round number. Reclaim and hold it Monday and the rotation thesis is confirmed with records back in play toward 7,550–7,600.

- S&P 500 7,440 — the downside shelf from the June consolidation. Losing it on a post-holiday gap turns the flat tape into a correction-of-the-rally move toward 7,400.

- Nasdaq 25,800 — the semi-unwind line. The Composite closed 33 points above it; a break on day three of chip selling would confirm distribution in the former leadership and pressure the whole tape.

Bull case: The soft jobs print keeps the Fed on hold, the semi complex stabilizes after two days of purging, and the record-setting Dow rotation broadens — the S&P reclaims 7,500 on Monday’s open and the second-half record chase resumes with financials, healthcare, and materials leading.

Bear case: The participation-rate deterioration reframes soft jobs as economic weakness rather than rate relief, the semi unwind gets a third day and confirms distribution, and a weekend headline gaps the tape below 7,440 on thin post-holiday liquidity — with the FOMC minutes Wednesday reviving the hike debate.

What We’re Watching

- Monday’s open after three days dark — gap direction and whether the S&P finally resolves its two-day pin at 7,483.

- Semis day three — Micron, Marvell, and the memory complex either stabilize (rotation) or extend (distribution). This is the tape’s biggest open question.

- FOMC minutes Wednesday, July 8, and ISM Services PMI — the macro calendar that decides whether the rate-relief trade in gold and Bitcoin keeps running.

Risks Into Tomorrow

- Participation-rate distortion — Unemployment fell to 4.2% only because 61.5% participation — the lowest since March 2021 — shrank the labor force. If markets reframe soft jobs as economic weakness rather than rate relief, the record-Dow rotation loses its foundation.

- Semi distribution watch — Two straight days of heavy selling in the chip complex (Micron, Marvell, AMAT, SanDisk all down 7–13%) after an 80%+ H1 run. Day three decides: stabilization keeps this as healthy rotation; a third day of double-digit damage confirms distribution in the market’s former leadership.

- Long-weekend gap risk — Markets are dark Friday through Sunday with the S&P pinned dead flat under 7,500. Three days of geopolitical and macro headlines will land on Monday’s open at once — and the FOMC minutes Wednesday can revive the hike debate the jobs print just buried.

Frequently Asked Questions

How did the S&P 500 close today?

On Thursday, July 2, 2026, the S&P 500 closed at 7,483.24 (0.00%), with the VIX at 16.83. The jobs report answered the rate-hike question — and split the tape in two.

What drove the market today?

SOFT JOBS BURIES THE HIKE CASE, DOW PRINTS A RECORD (Day) — June payrolls rose just 57K vs 115K expected (May revised down to 129K), unemployment fell to 4.2% only because participation dropped to 61.5%, the lowest since March 2021. The ~29% rate-hike odds priced for this month’s Fed meeting collapsed, and the Dow surged 594.83 points (+1.14%) to a record 52,900.07.

What levels matter for tomorrow?

S&P 500 7,500 — THE PIVOT. Two straight closes pinned 17 points under the round number. Reclaim and hold it Monday and the rotation thesis is confirmed with records back in play toward 7,550–7,600. S&P 500 7,440 — the downside shelf from the June consolidation. Losing it on a post-holiday gap turns the flat tape into a correction-of-the-rally move toward 7,400. Nasdaq 25,800 — the semi-unwind line. The Composite closed 33 points above it; a break on day three of chip selling would confirm distribution in the former leadership and pressure the whole tape.

How does Meta Trading Club prepare for the next session?

We wrap every session and carry the read forward through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

New to this? Start with the free training.

Learn how we read the market before you risk a dollar — our free education library and ebook break down the fundamentals step by step.

Free education → Get the free ebookThe session’s over. The prep isn’t.

This is how MTC members close each day — wrap what happened, mark the levels, and carry one clean read into tomorrow. If you want to build that habit and qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process. It’s application-based — see if it’s a fit.

Explore the MTC Incubator → Apply nowSources: CNBC live markets coverage, Yahoo Finance closing data, BLS June employment report, verified as of 4:30 PM ET July 2, 2026. For educational purposes only. Not financial advice.