Monday, July 13, 2026 · 4:30 PM ET · MTC Market Close

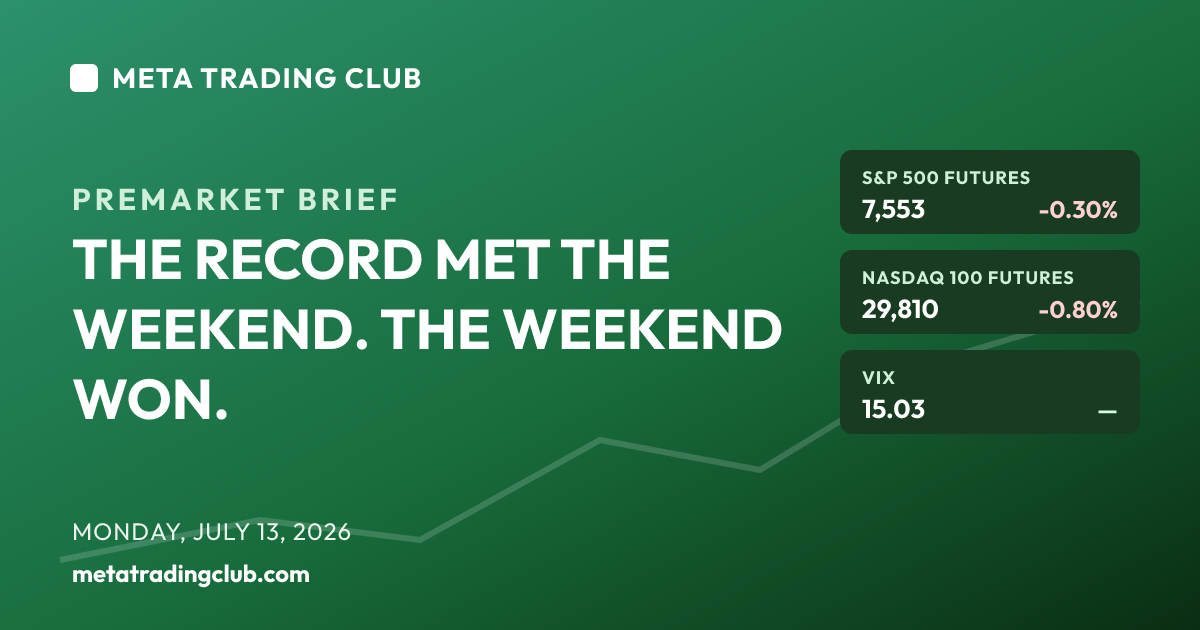

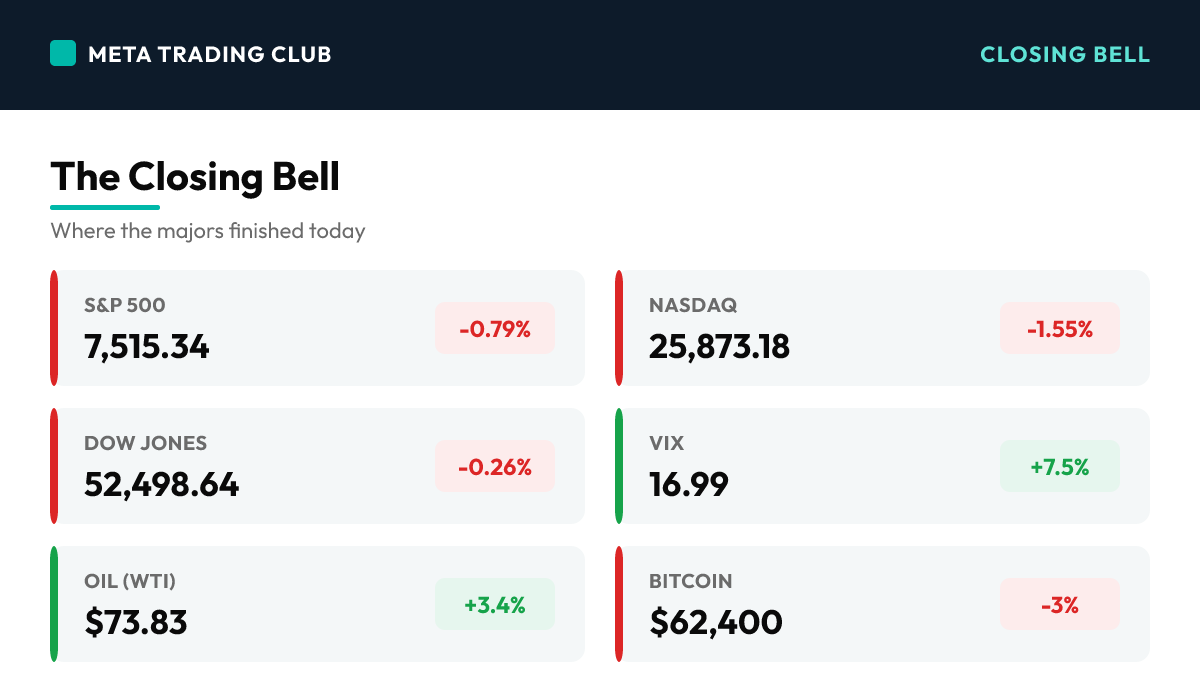

The record chase hit a wall, and the wall had a name: the Strait of Hormuz. Stocks pulled back to start the week after President Trump announced he was reinstating a blockade on Iranian shipping through the strait, sending crude spiking and knocking risk appetite out of exactly the corner of the market that had been carrying the whole tape. The S&P 500 fell 0.79% to 7,515.34, the Nasdaq dropped 1.55% to 25,873.18, and the Dow gave back 138.37 points (-0.26%) to 52,498.64 — a split-screen session where energy names cushioned the blue-chip index while semiconductors did the damage everywhere else. The engine of the June rally became Monday’s anchor. SK Hynix suffered its biggest one-day drop on record, falling roughly 15% in Seoul just two sessions after its blockbuster US debut and dragging the KOSPI down about 9%, and the memory-chip pain rolled straight across the tape: Micron slid about 5.4%, Western Digital fell 6.5%, SanDisk dropped near 7%, Intel lost 4.6%, AMD and Broadcom shed about 3% each, and even Nvidia gave back 1.7%. On the other side of the trade, the oil complex ripped. WTI jumped 3.4% to $73.83 as Exxon rose 4.4% to $145.04, Occidental gained 3.6%, and Chevron added 3.1% — Exxon adding fuel by pre-announcing that higher crude will boost Q2 upstream earnings by roughly $3.5–3.9 billion versus Q1. Cross-asset, the tape flipped defensive-but-not-panicked: the VIX popped about 7.5% to just under 17, the 10-year yield ticked up to 4.59%, gold slipped 1.2% to $4,072 as the dollar and yields firmed, and Bitcoin lost more than 3% to trade near $62,400. Here is the honest read: this is not the breadth thrust the bulls were waiting for — it is a rotation, not a rout. The exact same narrow leadership that carried the market to the doorstep of 7,610 is the leadership that got hit today, and the S&P is now sitting right on 7,500, the shelf it reclaimed and defended all last week. That level is the whole game into Tuesday, and Tuesday is loaded: June CPI at 8:30 AM ET and the first wave of Q2 bank earnings — JPMorgan, Citi, Wells Fargo, Goldman and Bank of America — all land before the bell, with new Fed Chair Kevin Warsh testifying to Congress the same day. A market that spent a month refusing to broaden just got a reason to test its foundation. Hold 7,500 into that gauntlet and the pullback is orderly rotation you can trade around; lose it, and the narrow tape’s crack becomes a trend question. No alignment, no trade.

The Closing Bell

| Instrument | Close | Change | Note |

|---|---|---|---|

| S&P 500 | 7,515.34 | -0.79% | Pulled back off the record chase and closed right on the 7,500 shelf it reclaimed last week — the geopolitical shock hit the exact megacap-tech leadership that had been carrying the tape, turning a narrow rally into a narrow pullback |

| Nasdaq | 25,873.18 | -1.55% | The worst of the three as the semiconductor complex led the drop — SK Hynix’s record decline rippled through Micron, Western Digital, Intel, AMD and Nvidia, hitting the AI-chip trade that had been the market’s single engine |

| Dow Jones | 52,498.64 | -0.26% | Cushioned by the energy surge — Exxon, Chevron and Occidental rallied on the oil spike and blunted the tech drag, the split-screen signature of a rotation rather than a broad-based sell |

| Russell 2000 | 2,973.05 | -0.60% | Small caps drifted lower with the tape but held up better than the Nasdaq — no chip exposure to punish, though still no sign of the broad participation the bulls have been waiting for |

| VIX | 16.99 | +7.5% | Fear gauge popped back toward 17 as the Iran headline and the chip rout woke up hedging demand — elevated and alert, but well short of a panic reading |

| 10-Yr Yield | 4.59% | +4 bps | Ticked higher as the oil spike revived inflation worry right into Tuesday’s CPI print — yields firming at the worst possible time for the stretched megacap multiples |

| Gold | $4,072.49 | -1.2% | Slipped despite the risk-off tone as firmer yields and a stronger dollar sapped the safe-haven bid — the classic tension when the shock is inflationary rather than deflationary |

| Oil (WTI) | $73.83 | +3.4% | The story of the day — jumped past $73 after Trump’s Strait of Hormuz blockade threat, dragging energy up and everything else down as the market repriced the geopolitical premium |

| Bitcoin | $62,400 | -3% | Lost more than 3% as risk appetite drained and the de-risking tone spread across assets — the crypto complex trading like the high-beta risk asset it is when geopolitics flares |

Today’s Charts

Daily candlestick charts with 20/50/200-day moving averages — the index majors, the day’s biggest mover on each side, and the leading sector ETF.

Charts: Finviz (daily). Levels and overlays update through the next session.

Sector Scoreboard

What Drove The Day

Monday was a rotation with a catalyst, and the catalyst was geopolitical. Before the open, President Trump announced he was reinstating a blockade on Iranian shipping through the Strait of Hormuz, and the market did exactly what a market does when a fifth of the world’s seaborne oil is suddenly in question: it bid crude and sold risk. The S&P 500 fell 0.79% to 7,515.34, the Nasdaq dropped 1.55% to 25,873.18, and the Dow gave back 138.37 points (-0.26%) to 52,498.64. But the index numbers hide the real character of the day, which was a violent split beneath the surface. The pain was concentrated in one place: semiconductors. SK Hynix — the memory-chip name that debuted on the US market to a 13% pop just two sessions earlier — suffered its single biggest one-day decline on record, crashing roughly 15% in Seoul and dragging South Korea’s KOSPI down about 9%. That shock rolled straight into every memory and AI-chip name: Micron fell about 5.4%, Western Digital dropped 6.5%, SanDisk slid near 7%, Intel lost 4.6%, AMD and Broadcom shed about 3% apiece, and even Nvidia — the tape’s anchor tenant — gave back 1.7%. The valuation air that had built up under the AI-chip trade for a month came out fast the moment sentiment turned. On the other side of the ledger, energy was the clear and only real winner. WTI crude jumped 3.4% to $73.83, and the oil majors ran with it: Exxon rose 4.4% to $145.04, Occidental gained 3.6% to $54.80, and Chevron added 3.1% to $181.88. Exxon poured on the move by pre-announcing that the higher crude prices should lift its Q2 upstream earnings by roughly $3.5–3.9 billion versus the first quarter — a fundamental kicker on top of the momentum. That energy strength is the whole reason the Dow held up while the Nasdaq bled; it is the fingerprint of a rotation, not a wholesale liquidation. Cross-asset, the tone was defensive but controlled. The VIX popped about 7.5% back toward 17 — awake, not alarmed. The 10-year Treasury yield ticked up to 4.59% as the oil spike revived the inflation conversation at the worst possible moment, one day before the June CPI report. Gold slipped 1.2% to $4,072 — an unusual move for a risk-off day, but a logical one when the shock is inflationary and yields are rising, sapping the metal’s appeal. And Bitcoin lost more than 3% to around $62,400, trading like the high-beta risk asset it always reveals itself to be when the geopolitical tape turns. So here is the recap that matters: the market did not broaden today, and it did not break either. It rotated — out of the exact narrow megacap-tech leadership that had carried it to the doorstep of a record, and into the one sector that benefits from the shock. The S&P is now sitting right on 7,500, the shelf it clawed back and defended through all of last week, and that level is the entire story into Tuesday. Because Tuesday is a gauntlet: the June CPI report drops at 8:30 AM ET, the first wave of Q2 bank earnings — JPMorgan, Citigroup, Wells Fargo, Goldman Sachs and Bank of America — all report before the open, and new Fed Chair Kevin Warsh begins his semi-annual testimony to Congress. A tape that spent a month refusing to prove its breadth is about to have its foundation tested by inflation data and the first hard read on the banks and the consumer. Hold 7,500 through that and today looks like healthy rotation you can trade around. Lose it, and the crack in the narrow tape becomes the trend question this market has been dodging all month.

MAJOR HEADLINES AND CATALYSTS

Top Market-Moving Stories

- STRAIT OF HORMUZ BLOCKADE THREAT SPIKES OIL, SINKS RISK (Day) — President Trump announced he was reinstating a blockade on Iranian shipping through the Strait of Hormuz before the open, sending WTI up 3.4% to $73.83 and flipping the tape defensive. Energy ripped, growth sold, and the record chase stalled with the S&P closing right on 7,500.

- SK HYNIX SUFFERS RECORD DROP, TORCHES THE CHIP TRADE (Day) — Just two sessions after its blockbuster US debut, SK Hynix crashed roughly 15% in Seoul — its biggest one-day fall on record — dragging the KOSPI down ~9% and rolling through every memory and AI-chip name: Micron -5.4%, Western Digital -6.5%, Intel -4.6%, Nvidia -1.7%. The month’s engine became the day’s anchor.

- ENERGY CUSHIONS THE DOW — ROTATION, NOT A ROUT (Day) — Exxon rose 4.4% to $145.04 after pre-announcing a $3.5–3.9B Q2 upstream earnings boost, with Occidental +3.6% and Chevron +3.1%. The energy strength blunted the tech drag and kept the Dow’s loss to just 0.26% — the clean signature of a sector rotation rather than a broad liquidation.

Fed and Macro Context

- The oil spike revived the inflation conversation at the worst possible moment: the 10-year yield ticked up to 4.59% one day before the June CPI report, and gold slipped 1.2% to $4,072 as firmer yields and a stronger dollar overpowered the usual safe-haven bid on a risk-off day.

- The VIX popped ~7.5% back toward 17 — a genuine wake-up in hedging demand, but still well short of a panic reading. Defensive positioning, not capitulation, was the signature of the close.

- Tuesday is the pivot: June CPI at 8:30 AM ET, the first wave of Q2 bank earnings before the open, and new Fed Chair Kevin Warsh’s inaugural semi-annual testimony to Congress — three macro catalysts stacked on a single session.

Single-Stock Standouts

- Exxon (XOM) led the tape, up 4.4% to $145.04 after pre-announcing that higher crude will boost Q2 upstream earnings by ~$3.5–3.9B versus Q1 — a rare fundamental catalyst layered on top of the oil-spike momentum. Occidental +3.6% and Chevron +3.1% rounded out the energy leadership.

- The memory complex was crushed: SanDisk fell ~7%, Western Digital -6.5%, Micron -5.4%, all tracking SK Hynix’s record ~15% Seoul drop. Intel -4.6%, with AMD and Broadcom -3% each — the AI-chip valuation air came out fast once sentiment turned.

- Nvidia (NVDA) gave back 1.7% — a relatively contained loss for the tape’s anchor, but a telling one: when even the leader can’t hold on a chip-selloff day, the market’s single engine is sputtering right into a loaded macro week.

AFTER-HOURS EARNINGS SPOTLIGHT

Tonight’s Slate

- A light Monday post-close slate — no major after-hours earnings tonight. The real earnings story sits at tomorrow’s opening bell, not this evening’s, so the after-hours tape stayed quiet as the market digested the day’s geopolitical shock.

- The catalyst is Tuesday pre-market: JPMorgan, Citigroup, Wells Fargo, Goldman Sachs and Bank of America all report Q2 results before the open — the first broad, wide-participation read on credit, the consumer and loan demand that a narrow, megacap-led tape has been avoiding all month.

NEXT SESSION SETUP

Tuesday, July 14 — 7,500 on Trial into a Triple Catalyst

- The S&P starts Tuesday sitting right on 7,500, the shelf it reclaimed and defended all last week. The setup is binary: hold it through the morning’s data and today reads as orderly rotation; lose it and the narrow tape’s crack becomes a genuine trend question with 7,400 the next real floor.

- June CPI lands at 8:30 AM ET — consensus is for headline to cool to ~3.9% year-over-year (from 4.2%) on a 10% drop in June gasoline, with core holding near 2.9%. But today’s oil spike is a live threat to that disinflation story, and yields at 4.59% are already leaning the wrong way.

- The first bank earnings — JPMorgan, Citi, Wells Fargo, Goldman, BofA — report before the open. This is the wide-participation catalyst the market has lacked: a clean read on financials could steady the tape and broaden leadership, or a soft one could pile onto the chip damage.

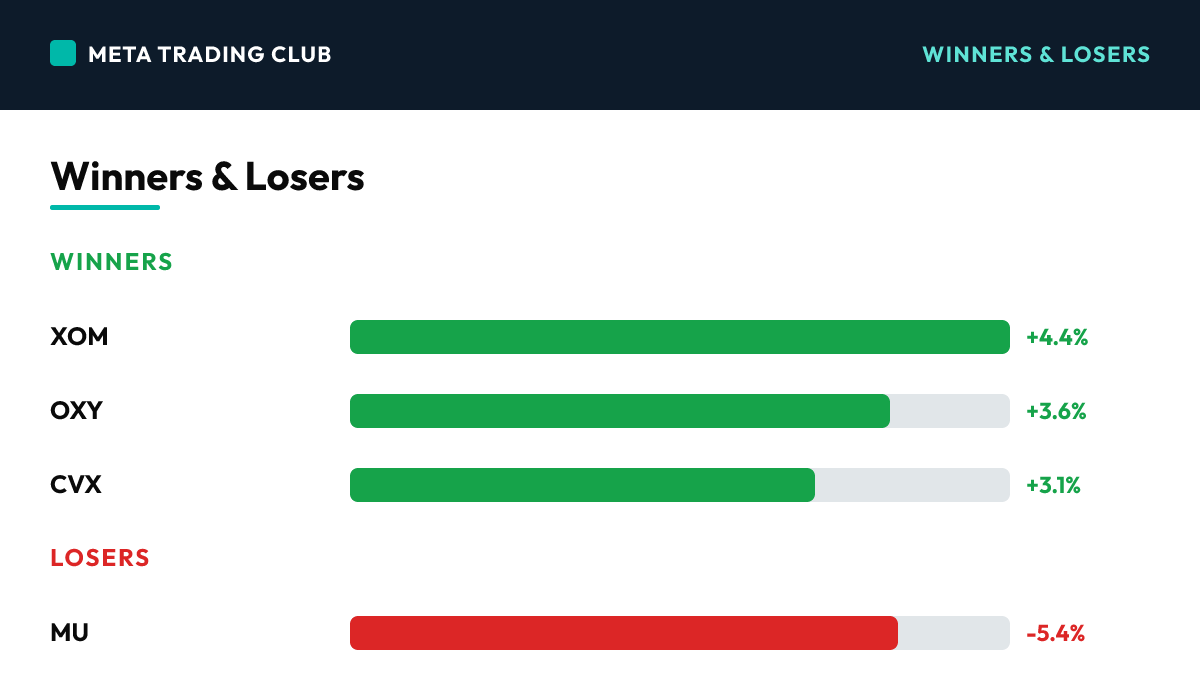

Winners & Losers

Winners

| XOM | +4.4% | Exxon led the entire tape after pre-announcing that higher crude will boost Q2 upstream earnings by ~$3.5–3.9B versus Q1 — a fundamental kicker on top of the 3.4% oil spike. Closed at $145.04, the single biggest engine on a red day | |

| OXY | +3.6% | Occidental rode the crude surge to $54.80 — high-beta leverage to the oil move made it one of the day’s cleanest geopolitical-premium winners | |

| CVX | +3.1% | Chevron added 3.1% to $181.88 as the oil majors caught the full Strait of Hormuz bid — steady large-cap energy strength that helped cushion the Dow |

Losers

| MU | -5.4% | Micron was the epicenter of the US memory-chip damage, tracking SK Hynix’s record ~15% Seoul drop lower — the AI-memory valuation air came out fast once the geopolitical shock flipped sentiment | |

| WDC | -6.5% | Western Digital fell hard alongside the memory complex as the SK Hynix rout and rising storage-glut worry hit the whole group — one of the day’s worst large-cap losers | |

| INTC | -4.6% | Intel led the broad semiconductor drop, extending the chip sector’s rough month as the US-Iran escalation and AI-spending selectivity hammered the group. AMD and Broadcom fell ~3% each alongside it |

What It Sets Up For Tomorrow

Levels Into Tomorrow

- S&P 500 7,500 — THE LINE THAT MATTERS. Price closed right on it. This is the shelf reclaimed and defended all last week, now the pivot into CPI and bank earnings. Hold it and the pullback is orderly rotation; lose it on the CPI/earnings reaction and the narrow-tape crack gets real.

- S&P 500 7,610 — THE RECORD CEILING, NOW FURTHER AWAY. Today’s drop pushed the record back to ~95 points overhead. It only comes back into play on a clean, broad recovery — and only if the chip complex stabilizes and breadth finally shows up.

- S&P 500 7,400 — THE NEXT REAL FLOOR. Lose 7,500 and this is where the buyers have to step in. A break here would turn a one-day rotation into a genuine trend question and put the whole June grind on trial.

Bull case: CPI cools as expected, the oil spike proves a headline rather than a trend, and the banks open Q2 season with clean beats — financials steady the tape, the chip selloff finds a floor, the S&P holds 7,500 and rotation broadens leadership beyond the wounded megacaps. A pullback that holds support and broadens is exactly the healthy reset the bulls needed.

Bear case: The oil spike sticks, a hot CPI print revives the inflation trade and pushes yields through 4.60%, and the banks disappoint or guide cautiously on credit. The chip damage spreads, the S&P loses 7,500 on the reaction, and the narrow leadership that carried the market all month unwinds toward 7,400 — the crack becomes the trend.

What We’re Watching

- The 7,500 line into the 8:30 AM CPI reaction — a hold through the print is orderly rotation; a decisive break turns the narrow-tape worry into a real trend question.

- The semiconductor complex — does SK Hynix’s record drop and the memory selloff find a floor Tuesday, or does the AI-chip de-rate keep bleeding into the tape’s only real engine?

- Bank earnings and the oil follow-through — clean bank beats plus a fading oil spike steadies everything; soft banks plus sticky crude and a hot CPI is the bear trifecta.

Risks Into Tomorrow

- Geopolitical oil shock — A single Strait of Hormuz headline repriced the entire tape in one session — crude +3.4%, energy up, growth down, yields up, gold and Bitcoin down. The market’s calm through June was built on the Iran risk fading; today was a reminder that geopolitical premium is never priced out, only priced down, and it can come back in an hour.

- The chip trade cracks — SK Hynix’s record drop torched the exact leadership — memory and AI chips — that carried the market to the edge of a record. When the single engine of a narrow rally de-rates this fast, the whole tape is exposed. Watch whether the semiconductor complex finds a floor or whether the valuation unwind has further to run.

- 7,500 into a triple catalyst — The S&P closed right on 7,500 the day before June CPI, the first bank earnings, and Fed Chair Warsh’s testimony all land in a single morning. With yields at 4.59% and an oil spike threatening the disinflation story, the level is the whole game — hold it and it’s rotation, lose it and it’s a trend question.

Frequently Asked Questions

How did the S&P 500 close today?

On Monday, July 13, 2026, the S&P 500 closed at 7,515.34 (-0.79%), with the VIX at 16.99. The record chase hit a wall, and the wall had a name: the Strait of Hormuz.

What drove the market today?

STRAIT OF HORMUZ BLOCKADE THREAT SPIKES OIL, SINKS RISK (Day) — President Trump announced he was reinstating a blockade on Iranian shipping through the Strait of Hormuz before the open, sending WTI up 3.4% to $73.83 and flipping the tape defensive. Energy ripped, growth sold, and the record chase stalled with the S&P closing right on 7,500.

What levels matter for tomorrow?

S&P 500 7,500 — THE LINE THAT MATTERS. Price closed right on it. This is the shelf reclaimed and defended all last week, now the pivot into CPI and bank earnings. Hold it and the pullback is orderly rotation; lose it on the CPI/earnings reaction and the narrow-tape crack gets real. S&P 500 7,610 — THE RECORD CEILING, NOW FURTHER AWAY. Today’s drop pushed the record back to ~95 points overhead. It only comes back into play on a clean, broad recovery — and only if the chip complex stabilizes and breadth finally shows up. S&P 500 7,400 — THE NEXT REAL FLOOR. Lose 7,500 and this is where the buyers have to step in. A break here would turn a one-day rotation into a genuine trend question and put the whole June grind on trial.

How does Meta Trading Club prepare for the next session?

We wrap every session and carry the read forward through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

New to this? Start with the free training.

Learn how we read the market before you risk a dollar — our free education library and ebook break down the fundamentals step by step.

Free education → Get the free ebookThe session’s over. The prep isn’t.

This is how MTC members close each day — wrap what happened, mark the levels, and carry one clean read into tomorrow. If you want to build that habit and qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process. It’s application-based — see if it’s a fit.

Explore the MTC Incubator → Apply nowSources: Yahoo Finance, CNBC, The Motley Fool, Benzinga, Investing.com and Schwab closing data; ExxonMobil Q2 upstream pre-announcement; SK Hynix / KOSPI selloff coverage; energy and semiconductor mover data; June CPI and Q2 bank-earnings previews — verified as of 4:30 PM ET July 13, 2026. For educational purposes only. Not financial advice.