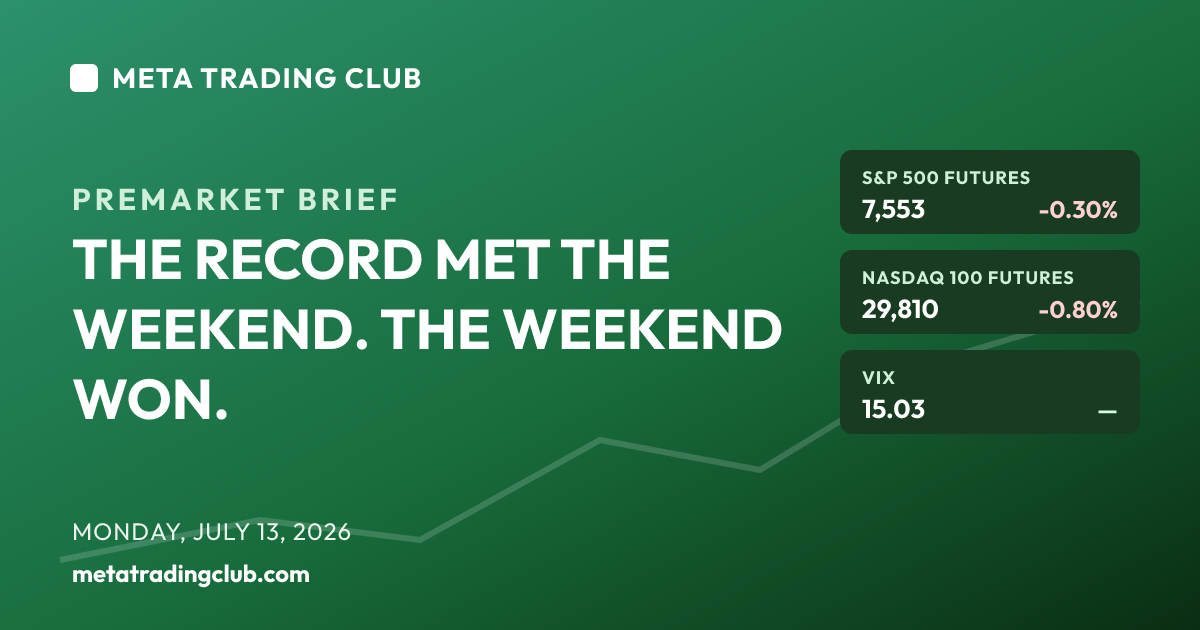

Monday, July 13, 2026 · 8:45 AM ET · MTC Market Intelligence

The record close met the weekend, and the weekend won. Friday the S&P finished at a fresh record 7,575.39 (+0.4%), the Dow at 52,637.01 and the Nasdaq at 26,281.61 — a clean, calm end to a winning week. Then the Middle East reopened the risk. Over the weekend the U.S. renewed strikes near the Strait of Hormuz, Iran retaliated against U.S. allies including Kuwait, Jordan and Qatar, and Trump told the NATO summit the ceasefire is “over.” That single shift flipped the tape: WTI is up about 4.2% to ~$74.41 (Brent ~$79), energy is leading, and futures are pulling back off the record — S&P futures -0.3%, Dow -0.1%, and Nasdaq-100 the worst at -0.8% as the AI/memory trade sells. SK Hynix, which popped ~13% on its Nasdaq debut Friday, is down ~8% premarket, dragging Micron and Sandisk with it as investors re-underwrite the AI-memory story. Cross-asset, the tone is a risk-off tilt, not a panic: VIX went out Friday at 15.03 and is likely bid on the open, the 10-year sits near 4.58%, gold holds ~$4,070 as a hedge, and Bitcoin eased to ~$63,020. The leadership tells the whole story — energy up (Chevron ~+2%, Exxon ~+1.5%, Diamondback ~+3%), chips down — a textbook geopolitical rotation out of growth and into the oil complex. The week ahead is loaded: bank earnings start (JPMorgan, Goldman, Citi, Wells Fargo), then JNJ and UnitedHealth, with CPI Tuesday and PPI midweek; Fastenal reports this morning and Treasury Budget lands at 2:00 PM. The map for the week is simple. Friday’s 7,575 record is now resistance-from-above after the gap lower, and 7,500 — the line the market held all last week — is the level that matters. Hold 7,500 and this is a geopolitical dip inside an uptrend. Lose it and the week’s gains start leaking toward 7,480 and 7,420. Oil is the switch; watch crude and the 10-year before you trust anything. No alignment, no trade.

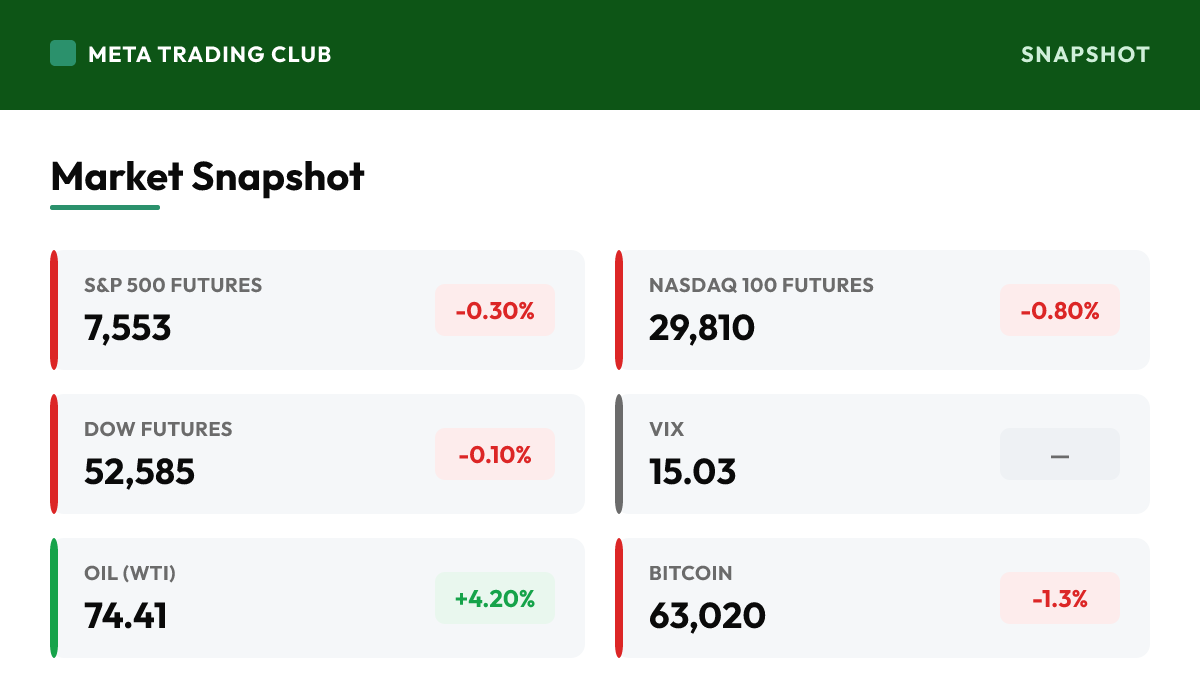

Market Snapshot

| Instrument | Level | Change | Note |

|---|---|---|---|

| S&P 500 Futures | 7,553 | -0.30% | Pulling back off Friday’s record 7,575.39 close as the weekend Iran escalation reprices risk; a controlled fade, not a flush. The record is now resistance overhead and 7,500 is the line that matters below |

| Nasdaq 100 Futures | 29,810 | -0.80% | The worst of the majors — the AI/memory trade is being re-underwritten. SK Hynix down ~8% after Friday’s debut pop is dragging Micron and Sandisk; growth gives back the most when oil and geopolitics lead |

| Dow Futures | 52,585 | -0.10% | The most resilient index this morning — with energy leading and growth selling, value and blue chips cushion the tape. A classic risk-off rotation shows up as the Dow holding while the Nasdaq drops |

| Russell 2000 Futures | — | — | No clean premarket read; small-caps typically lag on a geopolitical, oil-driven risk-off open, so treat the Russell as a follower of the S&P today rather than an independent tell |

| VIX | 15.03 | — | Went out Friday at 15.03 and is likely bid on the open as the Iran headlines return; still low in absolute terms — the market is pricing a shock to absorb, not a crisis, but watch it climb if crude keeps running |

| 10-Yr Yield | 4.58% | — | Sitting near 4.58% — the number to watch all week. An oil spike that lifts inflation expectations pushes yields up and squeezes growth; CPI Tuesday and PPI midweek make this the macro swing factor |

| Oil (WTI) | 74.41 | +4.20% | The story of the morning — up ~4.2% to ~$74 (Brent ~$79) after the U.S.-Iran escalation near the Strait of Hormuz over the weekend. Crude is the switch: it’s lifting energy and pressuring growth, and it can reprice on a single headline |

| Gold | 4,070 | — | Holding near $4,070 as a geopolitical hedge; the haven bid is measured rather than a scramble, which fits a market treating the escalation as a contained shock for now |

| Bitcoin | 63,020 | -1.3% | Eased to ~$63,020, down with the risk-off tilt and trading as a risk asset, not a haven; crypto is leaning with growth this morning rather than catching the safety flows going into gold |

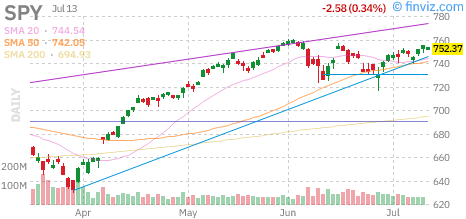

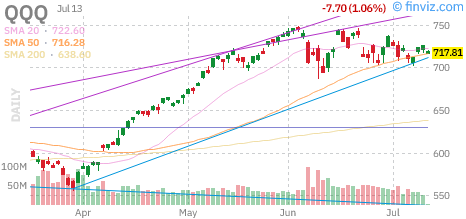

Charts to Watch

Daily candle charts with moving averages for the index proxies and today’s standout mover. Source: Finviz.

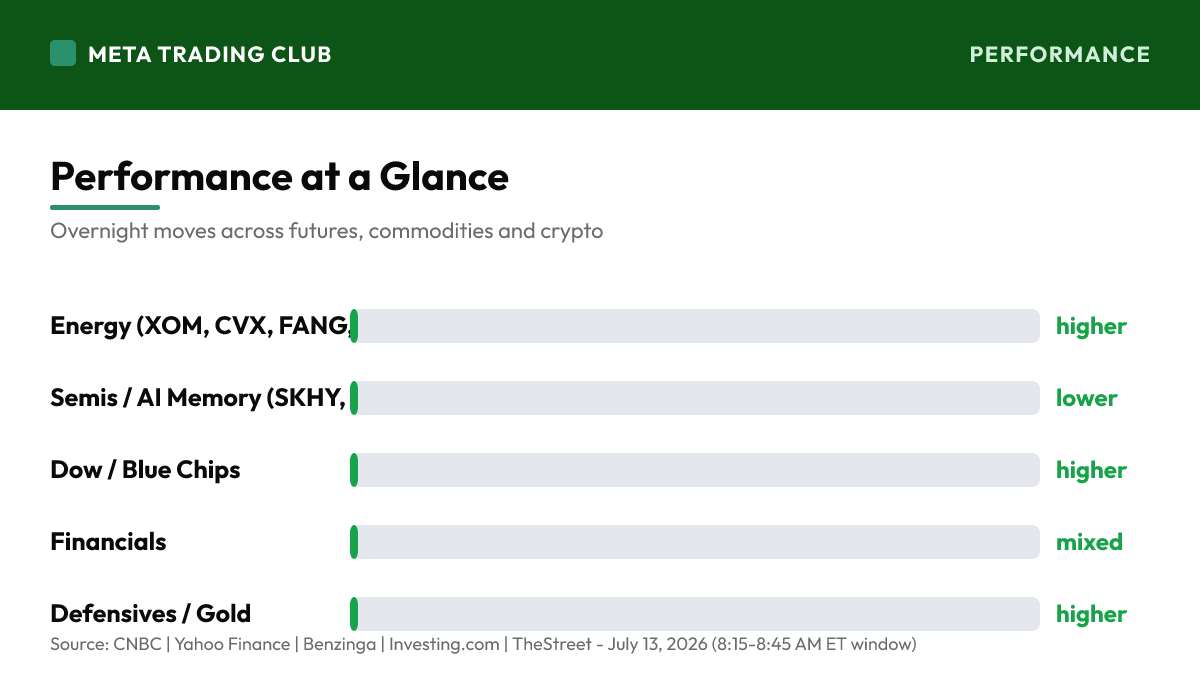

Performance at a Glance

Overnight & Global Markets

The question changed over the weekend. Friday the tape was pressing new highs — the S&P closed at a record 7,575.39, the Nasdaq and Dow both green, VIX at 15.03, the whole picture calm. Then geopolitics reset the board. The U.S. renewed strikes near the Strait of Hormuz, Iran hit back against allies in Kuwait, Jordan and Qatar, and the ceasefire Trump had floated is now, in his words, “over.” That flipped the tape from “can it extend the record” to “can it hold the trend through an oil shock.” This morning the answer is being written in two places: crude and chips. WTI is up ~4.2% toward $74, and energy is the clear leadership — Chevron ~+2%, Exxon ~+1.5%, Diamondback ~+3%, Occidental and APA firm. On the other side, the AI/memory trade is the funding source: SK Hynix, up ~13% on its Nasdaq debut Friday, is down ~8% premarket, pulling Micron and Sandisk lower as investors reassess how much of the AI-hardware move was momentum. That split — energy bid, growth sold — is a textbook geopolitical rotation, and Nasdaq-100 futures at -0.8% versus the Dow at -0.1% is the cleanest tell of it. Cross-asset, nothing is screaming crisis: VIX is low and only likely bid, the 10-year sits near 4.58%, gold holds ~$4,070 without a scramble, and Bitcoin eased with the risk tone. That combination reads as a controlled repricing, not a panic — the market is discounting a contained shock while it waits to see whether crude keeps climbing. The calendar raises the stakes: bank earnings kick off the week (JPMorgan, Goldman, Citi, Wells Fargo), JNJ and UnitedHealth follow, and CPI Tuesday plus PPI midweek land right as oil is pushing on inflation expectations. So the setup for Monday is a market stepping back from a record on a real catalyst, with a clean support line just below. This is not a green light and not a top — it’s a test of whether 7,500 still holds when the reason to sell is genuine.

MAJOR HEADLINES AND CATALYSTS

Top Premarket Stories

- The weekend reignited the Iran risk and flipped the tape. The U.S. renewed strikes near the Strait of Hormuz, Iran retaliated against allies (Kuwait, Jordan, Qatar), and Trump told the NATO summit the ceasefire is “over.” Futures are pulling back off Friday’s record — S&P -0.3%, Dow -0.1%, Nasdaq-100 -0.8% — as the market reprices a real supply-shock catalyst.

- Oil is the whole story this morning. WTI is up ~4.2% to ~$74.41 and Brent to ~$79 on the Hormuz escalation, and energy is the clear leadership — Chevron ~+2%, Exxon ~+1.5%, Diamondback ~+3%. Crude is the switch that’s lifting the oil complex and pressuring growth at the same time; watch it before trusting any bounce.

- The AI/memory trade is the funding source. SK Hynix, up ~13% on its Nasdaq debut Friday, is down ~8% premarket, dragging Micron and Sandisk lower as investors re-underwrite the AI-hardware move. Nasdaq-100 futures at -0.8% versus the Dow at -0.1% is the cleanest read on the rotation out of growth and into energy.

- The backdrop still isn’t crisis-priced. VIX went out Friday at 15.03 and is only likely bid, the 10-year sits near 4.58%, gold holds ~$4,070 without a scramble, and Bitcoin eased with the risk tone. This reads as a controlled, orderly repricing of a contained shock — supportive as long as crude doesn’t keep running and force the hedges to widen.

Stock-Specific

- Energy leads, chips lag. Chevron (~+2%), Exxon (~+1.5%) and Diamondback (~+3%) are bid with crude, while SK Hynix (~-8%), Micron and Sandisk sell as the memory trade unwinds part of Friday’s debut euphoria. Same market, opposite directions — read the leadership by catalyst, not by the index headline.

- SK Hynix (SKHY) is the single-name tell of the session. A ~13% debut pop Friday and a ~8% give-back Monday is a reminder that a hot listing trades on momentum first and fundamentals second; when the macro turns risk-off, the newest, most-crowded trade is the first to be sold. Watch whether the memory complex stabilizes or keeps bleeding.

Global and Macro

- The week is front-loaded with catalysts. Bank earnings start (JPMorgan, Goldman, Citi, Wells Fargo), then JNJ and UnitedHealth; CPI lands Tuesday and PPI midweek — both arriving just as oil pushes on inflation expectations. Fastenal reports this morning and Treasury Budget (June) is due at 2:00 PM ET. Plenty to move the tape after today’s geopolitical open.

- The Strait of Hormuz is the macro variable that overrides the calendar. With crude repricing on headlines, the 10-year near 4.58% becomes the swing factor: an oil-driven jump in inflation expectations can push yields up and squeeze growth into the CPI print. Let crude and the rate market lead the read today — the scheduled data is secondary to the escalation.

TECHNICAL ANALYSIS

S&P 500 Key Levels

- SPX closed Friday at a record 7,575.39, and this morning’s ~0.3% futures fade puts the open back below that print. That flips 7,575 from a level to reclaim into resistance-from-above — the market has to earn its way back to the record before the breakout is back in play. Until then, the record is the ceiling, not the base.

- The line that matters is 7,500 — the level the S&P held all last week. Hold it on this geopolitical pullback and the uptrend is intact and the dip stays buyable. Lose it and hold under it and the week’s gains start leaking toward 7,480, then the 7,420 breakout shelf. This is the risk anchor for every decision today.

- Bias: cautious. A record close met a real catalyst, and the tape is stepping back on rising oil and a chip-led growth sell. That’s a healthy test, not a top — but it’s not a green light either. Trade the reaction at 7,500, don’t predict it; anchor risk there, and let crude and the 10-year confirm before you lean either way.

Sector and Sentiment

- Read the rotation, not the index. Energy is bid on the oil spike while AI/memory is sold — a textbook geopolitical rotation out of growth and into the supply-shock beneficiary. The Nasdaq-100 (-0.8%) versus the Dow (-0.1%) split is the tell: this is money moving between sectors, not a broad-based liquidation. Trade the leaders in each direction.

- VIX at 15.03 and only likely bid says the options market is treating the escalation as a shock to absorb, not a crisis to hedge into. That’s supportive for the 7,500 hold — but it’s conditional on crude. A VIX that climbs through the high-teens alongside a still-rising WTI would be the sign the market has stopped absorbing and started repricing.

- The 10-year near 4.58% is the pressure gauge on growth. An oil-driven lift in inflation expectations pushes yields up and hits the long-duration names hardest — exactly the corner already selling this morning. If crude cools and yields settle, the growth sell-off is a one-day rotation; if both keep climbing into CPI, the pressure on the highs builds.

TODAY’S ECONOMIC CALENDAR

Key Releases (ET)

- The scheduled data is light today, and the geopolitics override it. Treasury Budget (June) is due at 2:00 PM ET, but with crude repricing on Hormuz headlines, the tape’s read comes from oil and the 10-year, not the calendar. Note the print, but the escalation and the energy complex are the signal into the afternoon.

- The 10-year near 4.58% is the number to watch all session and all week. It’s the swing factor: an oil-driven jump in inflation expectations pushes yields up and squeezes growth right into Tuesday’s CPI and midweek PPI. In a headline-driven session, the rate market is the macro tell that matters most.

- The big week starts now — bank earnings kick off (JPMorgan, Goldman, Citi, Wells Fargo), then JNJ and UnitedHealth, with CPI Tuesday and PPI midweek. Today sets the tone: a geopolitical risk-off open into a calendar loaded with the prints that decide whether the record from Friday gets reclaimed or fades.

Earnings Today

- Fastenal (FAST) reports before the open — an early industrial-demand read that sets a tone ahead of the marquee bank prints later this week. As an industrial distributor, it’s a useful pulse on the real-economy backdrop underneath the geopolitical noise driving the index tape this morning.

- The main event is later this week: the money-center banks (JPMorgan, Goldman, Citi, Wells Fargo) open Q2 season, followed by JNJ and UnitedHealth. A firmer 10-year near 4.58% is a tailwind for bank margins, so the read on financials will come from the actual guides — not from today’s headline-driven open.

PREMARKET PLAYBOOK

Key Levels

- SPX 7,500 — the line that matters. The market held it all last week, and this is the level that decides whether today’s geopolitical pullback stays a dip inside an uptrend. Hold it and dips stay buyable; lose it and hold under it and the week’s gains leak toward 7,480 and 7,420. This is the risk anchor for every long today — react to it, don’t predict it.

- SPX 7,575 — Friday’s record, now resistance-from-above. The ~0.3% futures fade puts the open below the record close, so the market has to earn its way back before the breakout is live again. A reclaim that holds re-arms the uptrend; a rejection here is the sign the oil shock still has the tape on defense.

- Oil and the 10-year — the confirmation pair. WTI +4.2% and the 10-year near 4.58% are what’s pressuring growth this morning. Crude cooling and yields settling would turn the growth sell into a one-day rotation; both climbing into CPI keeps the ceiling on the highs. Watch this pair before trusting any move at 7,500 or the record.

Bull case: Hold 7,500 with the VIX contained and crude stalling, and this is a textbook geopolitical dip inside an intact uptrend — energy leadership cushions the index, the Dow holds, and the S&P sets up to reclaim Friday’s 7,575 record once the oil headline fades. A calm 10-year into CPI would confirm the growth sell was a one-day rotation, not a trend change.

Bear case: Lose 7,500 while WTI keeps running and the VIX climbs through the high-teens, and the geopolitical shock stops being absorbed and starts repricing the tape. A chip-led growth sell that broadens, an oil-driven jump in yields into Tuesday’s CPI, and the week’s gains leak toward 7,480 and the 7,420 breakout shelf — the record fades instead of getting reclaimed.

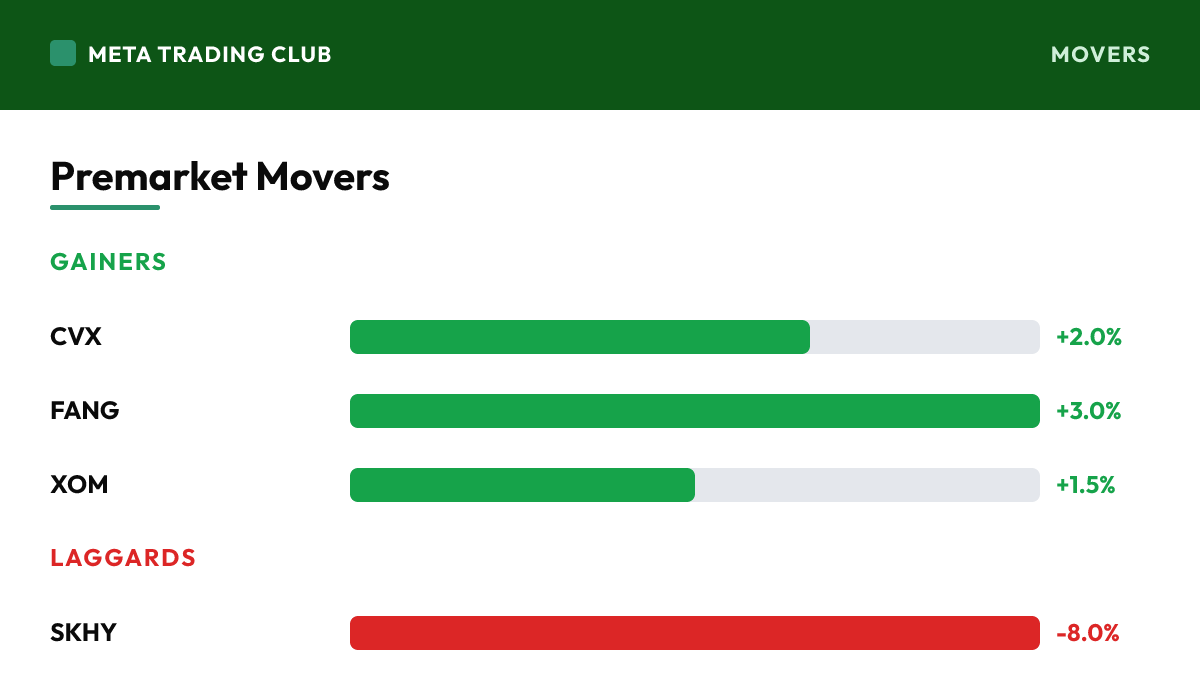

Premarket Movers

Gainers

| CVX | Chevron | +2.0% | Leading the energy complex as WTI jumps ~4.2% on the Iran-Hormuz escalation; the integrated majors are the cleanest large-cap way the tape expresses a supply-shock oil bid this morning |

| FANG | Diamondback Energy | +3.0% | Outrunning the majors — the higher-beta E&P names move more on a crude spike; Diamondback up ~3% is the sharper read on how hard the oil bid is running into the open |

| XOM | Exxon Mobil | +1.5% | Bid with crude on the geopolitical premium; a firm Exxon is the blue-chip anchor of the energy leadership that’s cushioning the Dow while growth sells |

Laggards

| SKHY | SK Hynix | -8.0% | Giving back most of Friday’s ~13% debut pop as the AI-memory trade unwinds on the risk-off open; the newest, most-crowded name is the first sold when geopolitics turns the tape defensive |

| MU | Micron Technology | -4.0% | Dragged lower with the memory complex as investors re-underwrite AI-hardware demand; the growth-heavy semis corner gives back the most when oil and geopolitics take the lead |

| SNDK | Sandisk | -4.0% | Selling with the memory group after leading it higher on Friday’s Hynix halo; the same names that ran on the debut are the ones unwinding as the AI trade cools this morning |

Risks Into the Open

- Primary risk: the oil spike keeps running. The Strait of Hormuz is the switch — with the U.S. and Iran exchanging strikes and the ceasefire declared “over,” crude can reprice higher on a single headline, lift yields, and squeeze growth further right into Tuesday’s CPI. Watch WTI as the variable that can turn a contained rotation into a broad risk-off move.

- Secondary risk: the chip sell broadens. Right now it’s memory down and energy up — a clean rotation. But Nasdaq-100 futures are already the worst major, and if the AI-hardware unwind spreads from Hynix and Micron into the broader semis and megacaps, the leadership that carried last week’s record hollows out and the 7,500 test fails.

- Constructive: the shock is still being absorbed, not repriced. VIX is low, gold’s hedge bid is orderly, the 10-year is steady near 4.58%, and the Dow is barely lower on energy strength. As long as that holds and 7,500 stays intact, this reads as a geopolitical dip inside an uptrend — a pullback to be bought once crude settles, not a top to sell.

Frequently Asked Questions

Where are S&P 500 futures trading ahead of the open?

Ahead of Monday, July 13, 2026, S&P 500 futures are at 7,553 (-0.30%), with the VIX near 15.03. The record close met the weekend, and the weekend won. Friday the S&P finished at a fresh record 7,575.39 (+0.4%), the Dow at 52,637.01 and the Nasdaq at 26,281.61 — a clean, calm end to a winning week. Then the Middle East reopened the risk. Over the weekend the U.S. renewed strikes near the Strait of Hormuz, Iran retaliated against U.S. allies including Kuwait, Jordan and Qatar, and Trump told the NATO summit the ceasefire is “over.” That single shift flipped the tape: WTI is up about 4.2% to ~$74.41 (Brent ~$79), energy is leading, and futures are pulling back off the record — S&P futures -0.3%, Dow -0.1%, and Nasdaq-100 the worst at -0.8% as the AI/memory trade sells. SK Hynix, which popped ~13% on its Nasdaq debut Friday, is down ~8% premarket, dragging Micron and Sandisk with it as investors re-underwrite the AI-memory story. Cross-asset, the tone is a risk-off tilt, not a panic: VIX went out Friday at 15.03 and is likely bid on the open, the 10-year sits near 4.58%, gold holds ~$4,070 as a hedge, and Bitcoin eased to ~$63,020. The leadership tells the whole story — energy up (Chevron ~+2%, Exxon ~+1.5%, Diamondback ~+3%), chips down — a textbook geopolitical rotation out of growth and into the oil complex. The week ahead is loaded: bank earnings start (JPMorgan, Goldman, Citi, Wells Fargo), then JNJ and UnitedHealth, with CPI Tuesday and PPI midweek; Fastenal reports this morning and Treasury Budget lands at 2:00 PM. The map for the week is simple. Friday’s 7,575 record is now resistance-from-above after the gap lower, and 7,500 — the line the market held all last week — is the level that matters. Hold 7,500 and this is a geopolitical dip inside an uptrend. Lose it and the week’s gains start leaking toward 7,480 and 7,420. Oil is the switch; watch crude and the 10-year before you trust anything. No alignment, no trade.

What is the biggest catalyst for the market today?

The weekend reignited the Iran risk and flipped the tape. The U.S. renewed strikes near the Strait of Hormuz, Iran retaliated against allies (Kuwait, Jordan, Qatar), and Trump told the NATO summit the ceasefire is “over.” Futures are pulling back off Friday’s record — S&P -0.3%, Dow -0.1%, Nasdaq-100 -0.8% — as the market reprices a real supply-shock catalyst.

What key levels should traders watch today?

SPX 7,500 — the line that matters. The market held it all last week, and this is the level that decides whether today’s geopolitical pullback stays a dip inside an uptrend. Hold it and dips stay buyable; lose it and hold under it and the week’s gains leak toward 7,480 and 7,420. This is the risk anchor for every long today — react to it, don’t predict it. SPX 7,575 — Friday’s record, now resistance-from-above. The ~0.3% futures fade puts the open below the record close, so the market has to earn its way back before the breakout is live again. A reclaim that holds re-arms the uptrend; a rejection here is the sign the oil shock still has the tape on defense. Oil and the 10-year — the confirmation pair. WTI +4.2% and the 10-year near 4.58% are what’s pressuring growth this morning. Crude cooling and yields settling would turn the growth sell into a one-day rotation; both climbing into CPI keeps the ceiling on the highs. Watch this pair before trusting any move at 7,500 or the record.

How does Meta Trading Club approach the market open?

We qualify every setup through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

Trade with a system, not signals.

This is exactly how MTC members read the open — bias, level, reaction, confirmation, execution. If you want to learn to qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process.

Apply for the Incubator → Learn moreSources: CNBC | Yahoo Finance | Benzinga | Investing.com | TheStreet – July 13, 2026 (8:15-8:45 AM ET window). For educational purposes only. Not financial advice.