Friday, July 10, 2026 · 4:30 PM ET · MTC Market Close

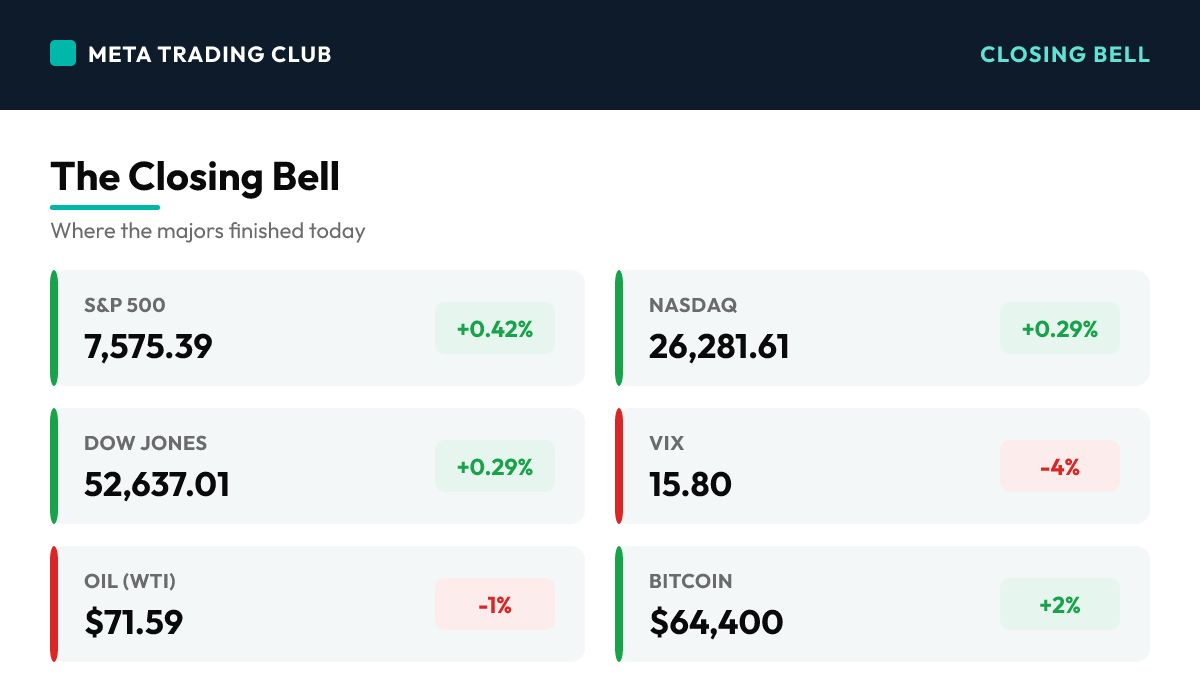

The market closed out a winning week, but it did it the same way it has done it all month: with a handful of giants carrying a tape that never broadened. The S&P 500 rose 0.42% to 7,575.39, the Nasdaq added 0.29% to 26,281.61, and the Dow gained 149.60 points (+0.29%) to 52,637.01 — three green indices that erased the Iran oil-shock damage from earlier in the week and left the S&P sitting roughly 35 points below its 7,610 record. The engine had a name, and it was megacap tech. Meta ripped about 6% to cap its best week since early 2024 after detailing plans to bring 14 gigawatts of AI compute online by 2027 and shipping its Muse Spark 1.1 model. Nvidia added around 4%. And the week’s marquee event delivered: SK Hynix debuted on the US market and popped roughly 13%, opening near $170 against a $149 offer price and raising about $26.5 billion in the largest foreign listing in US history — a loud confirmation of the memory-chip demand story. But underneath those headline prints, the market told a quieter, more honest story. Small caps went nowhere — the Russell 2000 finished roughly flat — and the equal-weight S&P lagged the cap-weighted index, the textbook signature of a rally where a few names do all the work. Delta opened the airline earnings season with a clean beat, adjusted EPS of $1.56 against a $1.48 estimate on revenue up 19% to $19.76 billion, and even raised its full-year guidance — yet the stock slipped about 1% as higher fuel costs pressured margins and net income fell 25%. A beat that still sells off is a tell about positioning. Cross-asset, the tone was calm: WTI eased to $71.59, gold slipped to about $4,115, Bitcoin firmed above $64,000, the VIX drifted near 15.8, and the 10-year held around 4.55%. So the week ends green and the record is in sight — but the lesson is the same one this tape keeps repeating: narrow strength is not the same as confirmation. Until the average stock joins the giants, a push toward 7,610 is a move worth respecting, not trusting. Alignment you can trade is alignment across the whole tape, and this tape still hasn’t given it.

The Closing Bell

| Instrument | Close | Change | Note |

|---|---|---|---|

| S&P 500 | 7,575.39 | +0.42% | Closed a winning week about 35 points below the 7,610 record, erasing the week’s Iran oil-shock damage — but the push higher was carried by a handful of megacaps, not the broad tape |

| Nasdaq | 26,281.61 | +0.29% | Led by Meta’s ~6% surge and Nvidia’s ~4% gain; the megacap platforms did the lifting while the SK Hynix debut lit up the memory-chip trade |

| Dow Jones | 52,637.01 | +0.29% | Added 149.60 points to fully recover the prior week’s oil-shock drop — a steady, broad-index green print even with leadership concentrated at the top |

| Russell 2000 | 2,991.00 | flat | Small caps went nowhere while megacap tech ripped — the clearest sign that Friday’s strength never left the top of the tape and breadth stayed thin |

| VIX | 15.80 | -4% | Fear gauge drifted toward the mid-15s as the Iran scare faded into the rearview and equities closed a calm, grinding week |

| 10-Yr Yield | 4.55% | flat | Held near 4.55% as calm oil and a quiet macro session kept yields range-bound ahead of next week’s CPI print and the start of bank earnings |

| Gold | $4,115.00 | -0.6% | Slipped modestly as the risk-on tone and steady yields sapped the safe-haven bid heading into the weekend |

| Oil (WTI) | $71.59 | -1% | Eased below $72 as the market fully looked past the week’s Iran headlines — the crude cooldown that let equities close the week green |

| Bitcoin | $64,400 | +2% | Firmed above $64,000 as risk appetite held into the close and the de-risking tone from the week’s geopolitical scare faded |

Today’s Charts

Daily candlestick charts with 20/50/200-day moving averages — the index majors, the day’s biggest mover on each side, and the leading sector ETF.

Charts: Finviz (daily). Levels and overlays update through the next session.

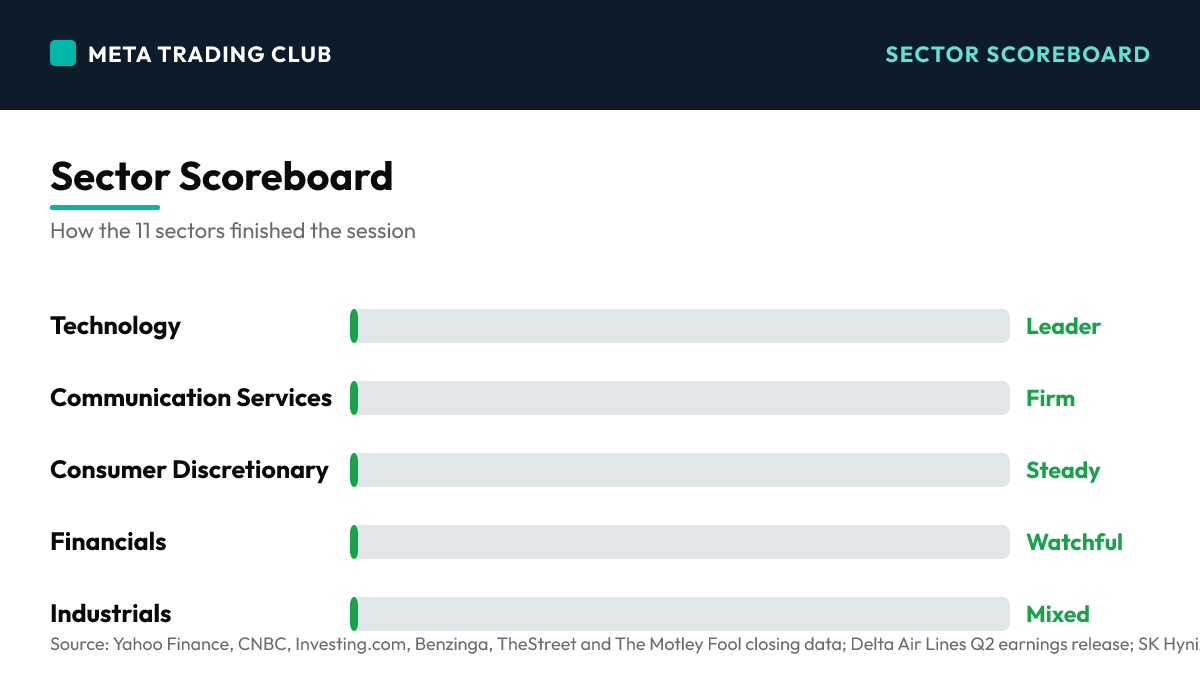

Sector Scoreboard

What Drove The Day

Friday was a quiet, constructive close to a winning week — and a near-perfect example of the tape’s defining problem. The S&P 500 rose 0.42% to 7,575.39, the Nasdaq added 0.29% to 26,281.61, and the Dow gained 149.60 points (+0.29%) to 52,637.01, leaving all three major indices green and the S&P about 35 points shy of its 7,610 record. On the surface, that is a strong week: the market fully erased the damage from the Iran oil shock that had rattled it days earlier. But look at what carried it. Meta was the story of the day and the week, rallying roughly 6% to cap its best week since early 2024 after laying out plans to bring 14 gigawatts of AI compute online by 2027 and releasing its Muse Spark 1.1 model — a one-two punch of infrastructure ambition and product cadence that reignited the AI-platform trade. Nvidia rode alongside it, up about 4%. And the week’s headline event delivered exactly what the bulls wanted: SK Hynix debuted on the US market and popped roughly 13%, opening near $170 against its $149 offer price, raising about $26.5 billion in what stands as the largest foreign listing in US history. That is a genuine, loud confirmation of memory-chip demand. Yet the recap has to name the catch, because it is the whole point: the strength was narrow. The Russell 2000 finished roughly flat — small caps simply did not participate — and the equal-weight S&P lagged the cap-weighted index, which is the textbook fingerprint of a market where a few giants do all the work while the average stock treads water. Delta Air Lines put an exclamation point on the breadth problem. It opened airline earnings season with a clean beat: adjusted EPS of $1.56 versus a $1.48 estimate, revenue up 19% to $19.76 billion, and management even raised full-year guidance to a $6.50–$7.50 range. And the stock fell about 1%, as higher fuel costs squeezed margins and net income dropped 25% to $1.6 billion. A beat that still sells off is a tell about stretched positioning. Cross-asset, everything else stayed calm: WTI eased to $71.59, gold slipped about 0.6% to roughly $4,115 as the safe-haven bid faded, Bitcoin firmed above $64,000, the VIX drifted toward the mid-15s, and the 10-year Treasury held near 4.55% into next week’s CPI print and the start of Q2 bank earnings. So the week ends green with the record in view — but the market has not answered the one question that matters. A rally powered by Meta, Nvidia and a single blockbuster IPO is a rally worth respecting; it is not yet one worth trusting. The difference is breadth. Until the small caps, the equal-weight index, and the rest of the tape join the giants, the drive toward 7,610 is a move riding on a narrow base. One engine — even a very powerful one — can pull the market to the doorstep of a record. Confirmation is when the whole market walks through it.

MAJOR HEADLINES AND CATALYSTS

Top Market-Moving Stories

- META LEADS A WINNING WEEK — AI-PLATFORM TRADE ROARS BACK (Day) — Meta rallied about 6% to cap its best week since early 2024 after detailing plans to bring 14 gigawatts of AI compute online by 2027 and shipping its Muse Spark 1.1 model. Nvidia added ~4% alongside it. The megacap platforms carried the S&P to within ~35 points of its 7,610 record.

- SK HYNIX DEBUTS, POPS ~13% — LARGEST FOREIGN US LISTING EVER (Day) — SK Hynix opened near $170 against a $149 offer, jumping roughly 13% and raising about $26.5 billion — the biggest foreign listing in US history and a loud confirmation of the memory-chip demand story that had been the week’s key question.

- THE CATCH — BREADTH STAYED NARROW (Day) — Underneath the green indices, the Russell 2000 finished roughly flat and the equal-weight S&P lagged the cap-weighted index. A few giants did all the work while the average stock treaded water — strong prints, thin participation.

Fed and Macro Context

- The macro backdrop stayed calm into the weekend: WTI eased to $71.59 as the market fully looked past the week’s Iran headlines, the VIX drifted toward the mid-15s, and Bitcoin firmed above $64,000 — a clean risk-on close with the geopolitical scare in the rearview.

- The 10-year Treasury held near 4.55% and gold slipped about 0.6% to roughly $4,115 as the safe-haven bid faded — yields range-bound and coiling ahead of next week’s CPI print, the next real read on the inflation path.

- The calendar is the story into next week: Q2 bank earnings season opens and the June CPI report lands — the two catalysts that will test whether the megacap-led grind can finally broaden or whether the narrow tape persists.

Single-Stock Standouts

- Meta was the clear leader, up ~6% on its 14GW AI-compute roadmap and Muse Spark 1.1 release, with Nvidia ~+4% riding the AI-platform enthusiasm — the two names that did the heavy lifting for the whole tape.

- SK Hynix (SKHY) popped ~13% on its US debut, opening near $170 versus a $149 offer and raising ~$26.5 billion — the largest foreign US listing on record and a direct confirmation of the memory-chip demand trade.

- Delta (DAL) fell about 1% despite a clean beat — adjusted EPS $1.56 vs $1.48 est., revenue +19% to $19.76B, and raised full-year guidance — as higher fuel costs pressured margins and net income fell 25%. A beat that still sells off is a positioning tell.

AFTER-HOURS EARNINGS SPOTLIGHT

Tonight’s Slate

- A light Friday post-close slate — no major after-hours earnings tonight. The day’s earnings story was Delta’s pre-market print, which opened airline season with a beat and raised guidance but still slipped ~1% on fuel-cost pressure, a cautionary read for the fuel-sensitive travel complex.

- The real earnings catalyst is next week: Q2 bank earnings season opens, giving the market its first broad read on financials and the health of the consumer and credit — the kind of wide-participation test that a narrow, megacap-led tape has been avoiding.

NEXT SESSION SETUP

Monday, July 13 — Record in View, Breadth on Trial

- The S&P starts Monday about 35 points below its 7,610 record after a winning week. The setup is simple: a broad, participatory push takes out the record cleanly; another megacap-only grind runs into the same thin-breadth wall that has capped every rally this month.

- Q2 bank earnings season opens the week — the first real test of financials, credit and the consumer. This is exactly the kind of wide-participation catalyst that could either broaden the tape or expose how narrow the leadership has become.

- The June CPI print lands as the macro anchor. With the 10-year holding near 4.55%, a hot number puts a bid back under yields and pressures the megacap multiples doing all the lifting; a cool one clears the runway toward the record.

Winners & Losers

Winners

| META | +6% | Meta led the tape and capped its best week since early 2024 after detailing plans for 14 gigawatts of AI compute by 2027 and releasing its Muse Spark 1.1 model — the single biggest engine of the winning week | |

| NVDA | +4% | Nvidia rode the AI-platform enthusiasm higher alongside Meta, the second megacap doing the heavy lifting as the memory-chip trade got its confirmation | |

| SKHY | +13% | SK Hynix popped on its US debut, opening near $170 versus a $149 offer and raising ~$26.5 billion — the largest foreign listing in US history and a loud confirmation of memory-chip demand |

Losers

| DAL | -1% | Delta slipped despite a clean beat — adjusted EPS $1.56 vs $1.48 est., revenue up 19% to $19.76B, and raised full-year guidance — as higher fuel costs squeezed margins and net income fell 25%. A beat that still sells off is a tell about positioning | |

| IWM | flat | Small caps (Russell 2000) went nowhere while megacap tech ripped — the Russell finished roughly flat, the clearest single sign that Friday’s strength never left the top of the tape | |

| RSP | flat | The equal-weight S&P lagged the cap-weighted index — when the average stock treads water while the benchmark climbs, a handful of giants are doing all the work. That’s the definition of narrow |

What It Sets Up For Tomorrow

Levels Into Tomorrow

- S&P 500 7,610 — THE RECORD CEILING. Price sits ~35 points below it after a winning week. Break it on broad participation — small caps and the equal-weight index joining — and the breakout is real; tag it on megacaps alone and it’s a lower-quality push prone to fade.

- S&P 500 7,500 — THE RECLAIMED SHELF, NOW SUPPORT. Won back earlier in the week and defended into Friday’s close. As long as this holds, the uptrend structure stays intact and dips are buyable.

- S&P 500 7,400 — the line in the sand. Lose 7,500 and this is the next real support; a break here turns the winning week into a genuine trend question rather than a routine pullback.

Bull case: The megacap strength broadens: bank earnings come in clean, June CPI cools, small caps and the equal-weight index finally join the leaders, the S&P holds 7,500 as support and pushes through 7,610 on real participation, and the record falls on a broad-based breakout worth trusting.

Bear case: The tape stays narrow: Meta and the megacaps can’t carry the whole market alone, bank earnings or a hot CPI print expose the thin breadth, the S&P stalls just under 7,610 and rolls back toward 7,500, and a failed record-chase confirms this was a giants-only rally the rest of the market never confirmed.

What We’re Watching

- Breadth, not the index number — do the small caps (Russell 2000) and the equal-weight S&P finally join the megacaps, or does a handful of giants keep carrying the whole tape into the record? That’s the difference between a breakout and a bull trap.

- Q2 bank earnings — the first wide-participation read on financials, credit and the consumer, and the cleanest test of whether leadership can broaden beyond tech.

- The June CPI print — with the 10-year near 4.55%, a hot number pressures the megacap multiples doing the lifting; a cool one clears the path toward the 7,610 record.

Risks Into Tomorrow

- Narrow leadership — The winning week was carried by Meta, Nvidia and a single blockbuster IPO while small caps went flat and the equal-weight index lagged. Three green indices, but a rally concentrated in a few giants has to broaden before it earns trust. One engine can pull the tape to the doorstep of a record; confirmation is when the whole market walks through it.

- Record-ceiling resistance — The S&P sits ~35 points below its 7,610 record. A push through on megacaps alone is a lower-quality breakout prone to fade; a break on broad participation is the real thing. The quality of the move matters more than the fact of it — watch breadth, not just the print.

- A loaded week ahead — Q2 bank earnings season opens and the June CPI print lands next week — the two catalysts that will test whether the megacap-led grind can broaden. With the 10-year near 4.55%, a hot CPI puts a bid back under yields and pressures the very multiples doing all the lifting.

Frequently Asked Questions

How did the S&P 500 close today?

On Friday, July 10, 2026, the S&P 500 closed at 7,575.39 (+0.42%), with the VIX at 15.80. The market closed out a winning week, but it did it the same way it has done it all month: with a handful of giants carrying a tape that never broadened.

What drove the market today?

META LEADS A WINNING WEEK — AI-PLATFORM TRADE ROARS BACK (Day) — Meta rallied about 6% to cap its best week since early 2024 after detailing plans to bring 14 gigawatts of AI compute online by 2027 and shipping its Muse Spark 1.1 model. Nvidia added ~4% alongside it. The megacap platforms carried the S&P to within ~35 points of its 7,610 record.

What levels matter for tomorrow?

S&P 500 7,610 — THE RECORD CEILING. Price sits ~35 points below it after a winning week. Break it on broad participation — small caps and the equal-weight index joining — and the breakout is real; tag it on megacaps alone and it’s a lower-quality push prone to fade. S&P 500 7,500 — THE RECLAIMED SHELF, NOW SUPPORT. Won back earlier in the week and defended into Friday’s close. As long as this holds, the uptrend structure stays intact and dips are buyable. S&P 500 7,400 — the line in the sand. Lose 7,500 and this is the next real support; a break here turns the winning week into a genuine trend question rather than a routine pullback.

How does Meta Trading Club prepare for the next session?

We wrap every session and carry the read forward through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

New to this? Start with the free training.

Learn how we read the market before you risk a dollar — our free education library and ebook break down the fundamentals step by step.

Free education → Get the free ebookThe session’s over. The prep isn’t.

This is how MTC members close each day — wrap what happened, mark the levels, and carry one clean read into tomorrow. If you want to build that habit and qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process. It’s application-based — see if it’s a fit.

Explore the MTC Incubator → Apply nowSources: Yahoo Finance, CNBC, Investing.com, Benzinga, TheStreet and The Motley Fool closing data; Delta Air Lines Q2 earnings release; SK Hynix US listing coverage; sector and mover data — verified as of 4:30 PM ET July 10, 2026. For educational purposes only. Not financial advice.