Wednesday, July 1, 2026 · 4:30 PM ET · MTC Market Close

Q3 opened with a rotation, not a rout. One session after closing the best quarter since 2020 right at 7,500, the S&P 500 slipped 0.22% to 7,483.23 — losing the round number by about 16 points — while the Nasdaq fell 0.66% to 26,040.03 as the semiconductor complex that just led the tape got sold hard for profit-taking. Micron dropped 10.6% after nearly tripling in Q2, Intel fell 9%, and the AI-infrastructure names bled — CoreWeave -13.9%, Nebius -17%, Corning -13.6%. But this was not broad distribution: the Dow eased just 13.96 points to 52,305.24 after printing a fresh intraday record at 52,742.66, the Russell 2000 touched an intraday all-time high before closing down 0.39% at 3,012.59, and 32 S&P names hit 52-week highs against just 5 lows. The money didn’t leave — it moved. Communication services jumped 2.63% behind Meta’s 8.8% surge on a Bloomberg report it’s building a cloud business to sell excess AI compute, financials gained nearly 2%, and Reddit ripped 13.9%. The pressure point was rates: the 10-year jumped toward 4.48% after ISM manufacturing printed a hot 53.3 and markets priced roughly a 29% chance of a Fed rate HIKE this month — a possibility that was near zero weeks ago. Gold broke under $4,000, capping its worst quarter since 2013, while Bitcoin reclaimed $60,000 with a 2.8% bounce. After the close the earnings slate was light, with no major reports. The real event is Thursday morning: the June jobs report hits at 8:30 AM — pulled forward because markets are closed Friday for July 4th — and it lands directly on the rate-hike debate. The S&P sits just under 7,500 with a binary catalyst at the open. That is a wait-and-see tape. No alignment, no trade.

The Closing Bell

| Instrument | Close | Change | Note |

|---|---|---|---|

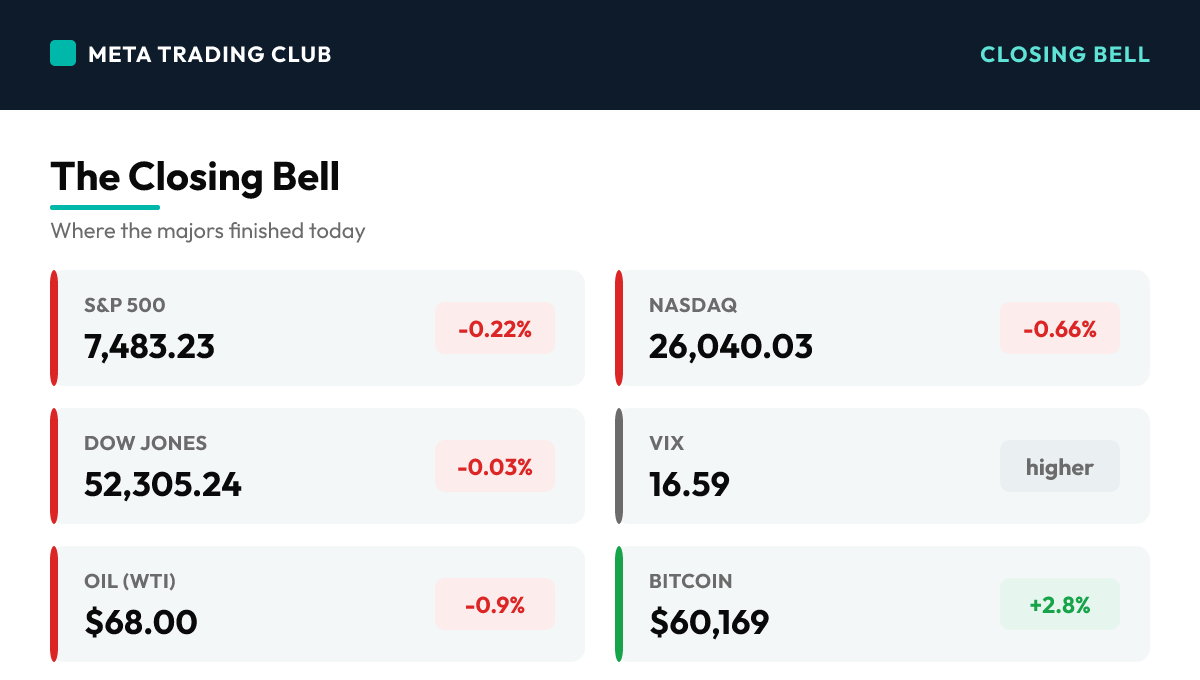

| S&P 500 | 7,483.23 | -0.22% | Slipped about 16 points below the 7,500 round number on day one of Q3 as semiconductor profit-taking offset strength in communication services and financials |

| Nasdaq | 26,040.03 | -0.66% | Lagged the majors as the chip complex got sold — Micron -10.6%, Intel -9%, Nvidia -1.3% — one session after semis led the quarter-end rally |

| Dow Jones | 52,305.24 | -0.03% | Eased just 13.96 points after printing a fresh intraday record at 52,742.66 — the value and financial complex held the tape together |

| Russell 2000 | 3,012.59 | -0.39% | Touched an intraday all-time high before fading; small caps closed H1 up 21%, their best first half since 1991 |

| VIX | 16.59 | higher | Ticked up modestly but stayed subdued in the mid-16s — the fear gauge read rotation, not panic, despite the chip-sector damage |

| 10-Yr Yield | 4.48% | higher | Jumped from the mid-4.3s after ISM manufacturing printed a hot 53.3 and markets priced roughly a 29% chance of a Fed rate hike this month |

| Gold | $3,990.70 | -1.2% | Broke under $4,000 and stayed there, capping its worst quarter since 2013 as rising yields and hike odds pressured the metal |

| Oil (WTI) | $68.00 | -0.9% | Slid to a fresh four-month low as supply stayed comfortable and Iran declined Qatar-hosted talks without escalation premium returning |

| Bitcoin | $60,169 | +2.8% | Reclaimed $60,000 with a 2.8% bounce after Tuesday’s break below the level — its first since 2024 — steadying the risk-appetite read |

Today’s Charts

Daily candlestick charts with 20/50/200-day moving averages — the index majors, the day’s biggest mover on each side, and the leading sector ETF.

Charts: Finviz (daily). Levels and overlays update through the next session.

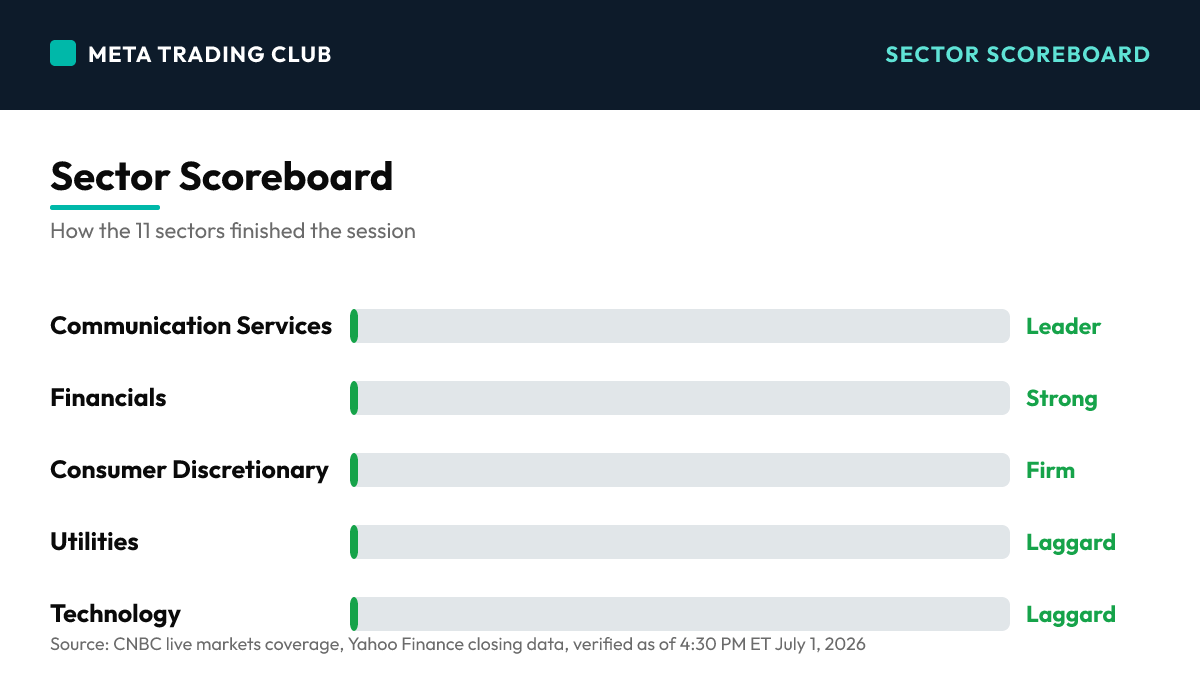

Sector Scoreboard

What Drove The Day

The first session of Q3 delivered exactly the re-test the quarter-end close invited — and the tape passed it in a way that demands a careful read. The headline damage was concentrated in one complex: semiconductors. Micron, which nearly tripled in the second quarter, dropped 10.6% to 1,032.28. Intel, up big into quarter-end, fell 9% to 127.06. Nvidia slipped 1.3%, and the AI-infrastructure trade bled hard — CoreWeave fell 13.9%, Nebius lost 17%, and Corning dropped 13.6%. That pressure dragged the Nasdaq down 0.66% to 26,040.03 and pushed the S&P 500 down 0.22% to 7,483.23, surrendering the 7,500 round number by about 16 points. But look under the index prints and the story changes. The Dow eased just 13.96 points to 52,305.24 — after setting a fresh intraday record at 52,742.66. The Russell 2000 touched an intraday all-time high before closing down 0.39% at 3,012.59, capping a 21% first half, its best since 1991. Breadth was constructive: 32 S&P names hit 52-week highs — Travelers, PNC, Live Nation, Monster, and Palo Alto among the all-time highs — against just 5 lows. Communication services surged 2.63% to lead the market, powered by Meta’s 8.8% rip to 612.91 on a Bloomberg report that the company is building a cloud business to sell its excess AI compute — a potential new revenue line on infrastructure it already owns. Reddit jumped 13.9%, ServiceNow gained 6.6% on a Guggenheim upgrade, and financials rose nearly 2%. That is rotation, not distribution: money moved from the most extended winners into new leadership rather than leaving the market. The pressure point was rates. The 10-year yield jumped toward 4.48% from the mid-4.3s after ISM manufacturing printed 53.3 — a sixth straight month of expansion, with new orders at 56 — and the morning’s soft ADP print of 98K faded from memory. By the close, fed funds futures priced roughly a 29% chance of a rate HIKE at this month’s Fed meeting, a scenario that was priced near zero just weeks ago. At Sintra, Fed and ECB officials publicly retreated from forward guidance, adding to the uncertainty. Cross-asset, gold broke below $4,000 and closed at $3,990.70, sealing its worst quarter since Q2 2013, while Bitcoin bounced 2.8% to reclaim $60,169 after Tuesday’s first break under $60K since 2024. Walmart fell 3.9% for a sixth straight decline, now down about 20% from its May high — a quiet warning from the consumer bellwether. After the bell, the earnings slate was light with no major reports, leaving the tape to focus on the real catalyst: the June jobs report, pulled forward to Thursday at 8:30 AM because markets are closed Friday for July 4th. It lands directly on the rate-hike debate — a hot print feeds the hike case and pressures the tape; a soft one buries it and likely reclaims 7,500. Holding an aggressive directional book into a binary macro print on a holiday-shortened week is exactly what the process says not to do. No alignment, no trade.

MAJOR HEADLINES AND CATALYSTS

Top Market-Moving Stories

- SEMIS GET SOLD HARD ON DAY ONE OF Q3 (Day) — The complex that led the best quarter since 2020 got hit with concentrated profit-taking: Micron -10.6% (after nearly tripling in Q2), Intel -9%, Nvidia -1.3%, CoreWeave -13.9%, Nebius -17%, Corning -13.6%. The Nasdaq fell 0.66% and the S&P slipped 0.22% to 7,483.23, losing the 7,500 round number by about 16 points.

- META RIPS 8.8% ON CLOUD-BUSINESS REPORT (Day) — Meta surged to 612.91 after Bloomberg reported the company is building a cloud business to sell its excess AI compute capacity — a potential new revenue stream on infrastructure it already owns. Communication services jumped 2.63% to lead the market, and Reddit ripped 13.9% alongside.

- RATE-HIKE ODDS HIT ~29% FOR THIS MONTH’S FED MEETING (Day) — The 10-year jumped toward 4.48% after ISM manufacturing printed a hot 53.3 (sixth straight month of expansion, new orders 56), and fed funds futures priced roughly a 29% chance of a HIKE at this month’s meeting — a scenario priced near zero weeks ago. At Sintra, Fed and ECB officials retreated from forward guidance.

Fed and Macro Context

- The morning and afternoon data told opposite stories — ADP private payrolls printed a soft 98K vs ~110K expected (down from 122K in May), but ISM manufacturing at 53.3 confirmed a sixth straight month of factory expansion, with the prices index cooling to 73 from 82.1 and new orders firm at 56. The bond market traded the ISM: yields jumped and hike odds climbed.

- Eurozone inflation came in at 2.8%, below the 3.0% estimate, and the yen slid to 162.68 — a fresh 40-year low — keeping the global policy divergence trade alive as central bankers at Sintra jointly stepped back from forward guidance.

- Gold broke under $4,000 and closed at $3,990.70 (-1.2%), sealing its worst quarter since Q2 2013; silver fell 2.6% to $57.91. Bitcoin moved the other way, bouncing 2.8% to reclaim $60,169 after Tuesday’s first break below $60K since 2024.

Single-Stock Standouts

- Walmart fell 3.9% to 108.82 — its sixth straight decline, now down roughly 20% from its May high. The consumer bellwether is quietly breaking down while the indexes sit near records; that divergence is worth respecting.

- Getty Images and Shutterstock scrapped their $3.7B merger after the UK CMA demanded remedies — Shutterstock collapsed 30%. General Mills jumped 6% on a clean Q4 beat ($0.95 vs $0.80) plus a $3B cost-savings plan through FY2030. Bending Spoons debuted at +39.7% ($40.50), and Progress Software gained 18% on its Q2 beat.

- Crypto-adjacent and high-beta names caught the rotation bid — MicroStrategy +7.4%, Robinhood +8.4%, Shopify +6.5% — as Bitcoin reclaimed $60K and risk appetite rotated rather than retreated.

AFTER-HOURS EARNINGS SPOTLIGHT

Tonight’s Slate

- A light night — no major earnings reports after the close. The tape gets a quiet evening ahead of the holiday-compressed week, leaving positioning to square up around one thing: Thursday morning’s jobs report.

- General Mills (reported this morning, +6% on the day) was the session’s cleanest earnings story: $0.95 EPS vs $0.80 expected plus a $3B cost-savings program through FY2030 — a reminder that execution still gets paid even in a rotating tape.

NEXT SESSION SETUP

Thursday, July 2 — The Compressed Catalyst

- JUNE JOBS REPORT — THURSDAY 8:30 AM ET (pulled forward; markets closed Friday for July 4th). This is the binary. It lands directly on a live rate-hike debate with ~29% odds priced for this month’s meeting. Hot print: hike case strengthens, yields extend, the 7,440 shelf gets tested. Soft print: hike case buried, 7,500 likely reclaimed.

- Thursday is a normal full session but effectively a half-liquidity, pre-holiday tape — expect the reaction to the print to be fast and potentially exaggerated in both directions before volume thins into the long weekend.

- Watch whether semiconductor selling continues or stabilizes — one day of profit-taking after an 80%+ H1 run is healthy rotation; a second straight day of double-digit damage in the leaders would start to look like distribution.

Winners & Losers

Winners

| META | +8.8% | Bloomberg report it’s building a cloud business to sell excess AI compute — new revenue line on infrastructure it already owns; closed 612.91 | |

| RDDT | +13.9% | Ripped alongside the communication-services surge as the rotation bid chased the sector’s new leadership; closed 197.76 | |

| NOW | +6.6% | Guggenheim upgrade powered ServiceNow to 105.80; Salesforce gained 4% on the same enterprise-software call |

Losers

| MU | -10.6% | Concentrated profit-taking after Micron nearly tripled in Q2 — the poster child of the semi unwind; closed 1,032.28 | |

| INTC | -9.0% | Gave back a chunk of its quarter-end surge as the chip complex got sold on day one of Q3; closed 127.06 | |

| WMT | -3.9% | Sixth straight decline, now ~20% off its May high — the consumer bellwether quietly breaking down; closed 108.82 |

What It Sets Up For Tomorrow

Levels Into Tomorrow

- S&P 500 7,500 — THE PIVOT. Tuesday’s quarter-end close and the round number the index just surrendered by 16 points. Reclaim and hold it after the jobs print and the rotation thesis is confirmed, opening the 7,550–7,600 zone.

- S&P 500 7,440 — the downside shelf from the June consolidation. Losing it after a hot jobs print puts the tape in correction-of-the-rally mode toward 7,400.

- 10-Year yield 4.50% — the rates line in the sand. A push through 4.5% on a hot jobs number pressures the equity multiple and feeds the hike debate directly.

Bull case: A soft or in-line jobs print buries the rate-hike case, yields retreat from 4.48%, and the S&P reclaims 7,500 with the new leadership (comm services, financials) intact — rotation confirmed, records back in play into the second half.

Bear case: A hot jobs print cements hike odds, the 10-year pushes through 4.5%, semi selling turns into a second day of distribution, and the S&P loses the 7,440 shelf on thin pre-holiday liquidity — fast downside with nobody home to buy it.

What We’re Watching

- June jobs report Thursday 8:30 AM ET — pulled forward, markets closed Friday for July 4th. The binary catalyst for the whole week.

- Whether Micron and Intel stabilize or extend losses — day two decides if this was rotation or the start of distribution.

- Meta follow-through above 600 and Walmart’s six-day slide — the new leader and the quiet consumer warning.

Risks Into Tomorrow

- The jobs print is binary on thin pre-holiday liquidity — the first move can run well past 7,500 or 7,440 before real positioning shows up. Let the level prove itself before acting.

- Rate repricing risk — hike odds at ~29% can swing violently on one number. A 10-year push through 4.50% pressures the equity multiple across the board, not just semis.

- Day-two distribution risk in semis — if Micron and Intel extend losses instead of stabilizing, today’s “healthy rotation” read flips fast. Walmart’s six-day slide is the quiet consumer warning underneath it.

Frequently Asked Questions

How did the S&P 500 close today?

On Wednesday, July 1, 2026, the S&P 500 closed at 7,483.23 (-0.22%), with the VIX at 16.59. Q3 opened with a rotation, not a rout.

What drove the market today?

SEMIS GET SOLD HARD ON DAY ONE OF Q3 (Day) — The complex that led the best quarter since 2020 got hit with concentrated profit-taking: Micron -10.6% (after nearly tripling in Q2), Intel -9%, Nvidia -1.3%, CoreWeave -13.9%, Nebius -17%, Corning -13.6%. The Nasdaq fell 0.66% and the S&P slipped 0.22% to 7,483.23, losing the 7,500 round number by about 16 points.

What levels matter for tomorrow?

S&P 500 7,500 — THE PIVOT. Tuesday’s quarter-end close and the round number the index just surrendered by 16 points. Reclaim and hold it after the jobs print and the rotation thesis is confirmed, opening the 7,550–7,600 zone. S&P 500 7,440 — the downside shelf from the June consolidation. Losing it after a hot jobs print puts the tape in correction-of-the-rally mode toward 7,400. 10-Year yield 4.50% — the rates line in the sand. A push through 4.5% on a hot jobs number pressures the equity multiple and feeds the hike debate directly.

How does Meta Trading Club prepare for the next session?

We wrap every session and carry the read forward through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

New to this? Start with the free training.

Learn how we read the market before you risk a dollar — our free education library and ebook break down the fundamentals step by step.

Free education → Get the free ebookThe session’s over. The prep isn’t.

This is how MTC members close each day — wrap what happened, mark the levels, and carry one clean read into tomorrow. If you want to build that habit and qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process. It’s application-based — see if it’s a fit.

Explore the MTC Incubator → Apply nowSources: CNBC live markets coverage, Yahoo Finance closing data, verified as of 4:30 PM ET July 1, 2026. For educational purposes only. Not financial advice.