Wednesday, June 17, 2026 · 4:30 PM ET · MTC Market Close

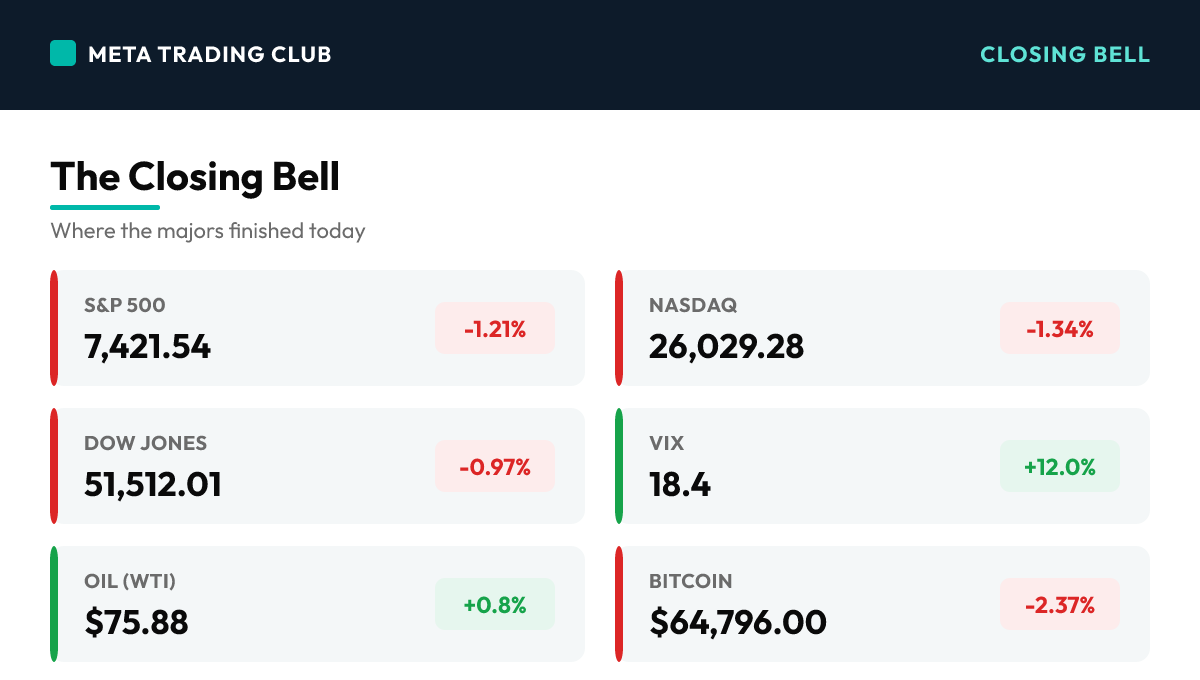

The Fed held — and the market still broke. The FOMC kept rates at 3.50-3.75% in Kevin Warsh’s first decision as Chair, but the updated dot plot did the damage: nine of eighteen members now pencil in a rate HIKE by year-end, a sharp reversal from March’s projected cut, and traders moved to fully price one quarter-point hike for 2026. Equities sold into the close and finished at the lows — the Nasdaq fell 1.34% to 26,029.28, the S&P 500 dropped 1.21% to 7,421.54, and the Dow gave back 0.97% to 51,512.01, surrendering Tuesday’s record. The 10-year yield jumped nearly 7bps to 4.50% and the VIX popped ~12% to ~18.4. Semiconductors took the brunt — Intel -8.5%, AMD -7.3%, Micron -6.2%, Broadcom -4.4%, Nvidia -2.4% — as profit-taking met a higher-rate repricing. The bright spot: yield-sensitive financials, with JPMorgan +3.72% and Visa +2.83% bucking the tape. Tomorrow is about digesting the new Fed path, with jobless claims the only notable macro print.

The Closing Bell

| Instrument | Close | Change | Note |

|---|---|---|---|

| S&P 500 | 7,421.54 | -1.21% | Fell 90.9 pts and closed at the session low as the hawkish dot plot repriced the rate path |

| Nasdaq | 26,029.28 | -1.34% | Worst of the majors (-353 pts) — semis and mega-cap tech led the post-Fed slide |

| Dow Jones | 51,512.01 | -0.97% | Gave back 504 pts, surrendering Tuesday’s record close; financials cushioned the drop |

| Russell 2000 | — | -0.74% | Small caps slipped with the tape; no confirmed closing level in this window |

| VIX | 18.4 | +12.0% | Popped off the mid-16s as the Fed surprise jolted volatility — still below the 20 stress line |

| 10-Yr Yield | 4.50% | +6.9 bps | Jumped to 4.497% as the dot plot’s hike bias drove the bond selloff |

| Gold | $4,348.00 | -0.14% | Held near recent levels; a stronger dollar and higher yields capped the safe-haven bid |

| Oil (WTI) | $75.88 | +0.8% | Steadied after Tuesday’s crash as the market digested the Iran ceasefire and Hormuz reopening |

| Bitcoin | $64,796.00 | -2.37% | Fell with risk assets as higher yields and a hawkish Fed pressured the crypto complex |

Today’s Charts

Daily candlestick charts with 20/50/200-day moving averages — the index majors, the day’s biggest mover on each side, and the leading sector ETF.

Charts: Finviz (daily). Levels and overlays update through the next session.

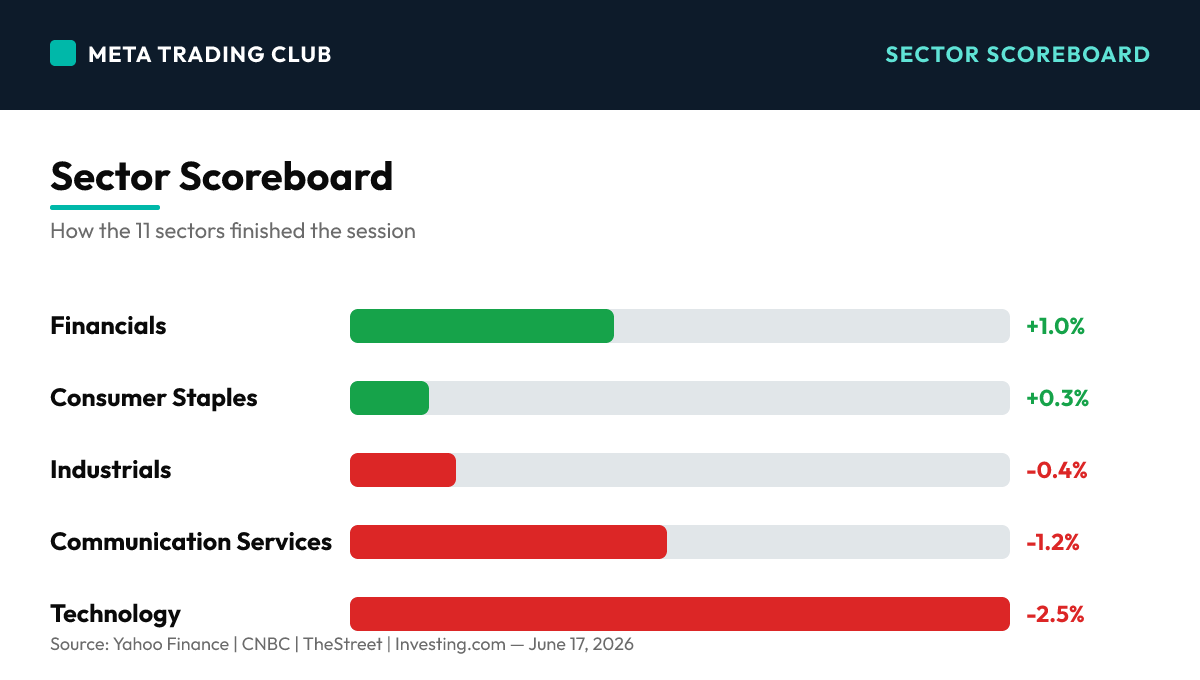

Sector Scoreboard

What Drove The Day

Wednesday was a textbook case of the decision mattering less than the projections. The FOMC left the federal funds rate unchanged at 3.50-3.75% — exactly as the ~97% priced-in odds implied — in Kevin Warsh’s first meeting as Chair. But the updated Summary of Economic Projections flipped the script: nine of eighteen participants now see a rate HIKE by the end of 2026, a stark reversal from March, when the median dot showed a cut. With the labor market firming and inflation running at its hottest in three years, traders rapidly moved to fully price one quarter-point hike for the year. The reaction was immediate and one-directional into the close. The Nasdaq Composite dropped 353.53 points (-1.34%) to 26,029.28, the S&P 500 fell 90.90 points (-1.21%) to 7,421.54, and the Dow Jones gave back 504.56 points (-0.97%) to 51,512.01, erasing Tuesday’s record. The Russell 2000 eased 0.74%. The bond market told the story: the 10-year yield jumped roughly 7 basis points to 4.50%, and the VIX popped about 12% to the high-18s as the rate-cut trade got repriced in real time. Semiconductors absorbed the worst of it as a strong recent rally met a higher-for-longer message — Intel sank 8.5%, AMD 7.3%, Micron 6.2%, Broadcom 4.4%, and Nvidia 2.4%. The standout exception was financials: higher yields are a tailwind for bank margins, and JPMorgan (+3.72%), Visa (+2.83%), and 3M (+2.15%) closed green against a red tape. No major earnings were confirmed after 4:05 PM ET — mid-June sits between reporting seasons. The setup into Thursday is clean: the trend just took a real shot, and the market has to decide whether this is a one-day repricing or the start of a deeper digestion of a higher-for-longer Fed.

MAJOR HEADLINES AND CATALYSTS

Top Market-Moving Stories

- FED HOLDS, DOTS GO HAWKISH — The FOMC kept rates at 3.50-3.75% in Warsh’s first decision, but nine of eighteen members now project a HIKE by year-end (March showed a cut). Traders moved to fully price one quarter-point hike for 2026 — the single catalyst behind the selloff.

- SEMIS WRECKED (Day) — Chips led the slide as a hot rally met a higher-for-longer message: Intel -8.5%, AMD -7.3%, Micron -6.2%, Broadcom -4.4%, Nvidia -2.4%. Technology was the worst-performing sector on the day.

- FINANCIALS BUCK THE TAPE (Day) — Higher yields are a tailwind for banks. JPMorgan (+3.72%), Visa (+2.83%), and 3M (+2.15%) closed green against a broadly red market — the day’s only real pocket of strength.

Fed and Macro Context

- Warsh’s first presser did little to settle it — The new Chair noted no participant felt the need to hike today, but the projections spoke louder than the words. Stocks hit session lows into the close as the market absorbed the shift in the path.

- 10-Year Yield 4.50% (+6.9 bps) — The bond market repriced fast: yields jumped and the VIX popped ~12% to the high-18s. Higher rates and a firmer dollar pressured both growth equities and Bitcoin (-2.37% to ~$64.8K).

What Changed

- The rate-cut trade is on hold — Hotter inflation (a three-year high, lifted partly by Middle East energy) and a firming labor market gave the Fed cover to drop March’s projected cut. The market spent months leaning dovish; today it had to re-anchor.

- Rotation, not capitulation — Money moved toward yield-sensitive financials and defensives rather than rushing the exits entirely. The structure took a hit, but the move was orderly — a repricing, not a panic.

AFTER-HOURS EARNINGS SPOTLIGHT

Earnings Reported After 4:05 PM ET Today

- Light post-close slate — No major earnings confirmed after 4:05 PM ET today. Mid-June sits between the Q1 and Q2 reporting seasons, so the post-close tape is quiet. The catalyst tonight is macro: the market digesting the new Fed dot plot.

Regular Session Highlights — Day-Session Movers

- INTC -8.5% / AMD -7.3% / MU -6.2% (Day) — The semiconductor complex took the worst of the post-Fed repricing as a strong recent rally unwound into higher rates.

- JPM +3.72% / V +2.83% (Day) — Financials were the standout, with higher yields seen as a margin tailwind for banks. The clearest example of money rotating rather than fleeing.

- NVDA -2.4% / AVGO -4.4% (Day) — Even the mega-cap chip leaders gave ground, dragging the Nasdaq to the bottom of the majors and erasing recent gains.

TOMORROW’S SETUP — THURSDAY JUNE 18, 2026

Key Economic Releases (ET)

- 8:30 AM — Initial Jobless Claims: The week’s marquee labor read. With the Fed citing a firming job market as cover for its hawkish tilt, a low claims print reinforces higher-for-longer; a jump would soften it and could spark a relief bid.

- 8:30 AM — Philadelphia Fed Manufacturing Index (June): A timely regional activity gauge. A strong number adds to the no-cut case; a soft one feeds the slowdown debate the Fed is now weighing.

- Post-Fed digestion is the real driver — The tape spends Thursday processing the dot plot. Watch whether yields hold above 4.50% and whether the chip selloff stabilizes or extends.

Earnings and Events

- Light earnings slate — Mid-June stays quiet for corporate reports. With no heavyweight prints due, the tape remains macro-driven as it re-anchors to a higher-for-longer Fed.

- Fed speakers in focus — Post-meeting commentary from FOMC members can either reinforce or soften the hawkish read. Any dovish pushback against the dot plot would be a relief catalyst for risk.

MTC Framework for Thursday

- Higher timeframe bias: BULLISH but tested — The S&P closed at 7,421 after losing 7,500, the first real shot to the uptrend in weeks. Structure is still higher-highs on the weekly, but the daily just flashed a warning. Respect the level, don’t fight the tape.

- Key level: S&P 500 7,420 is the line. Hold above into Thursday = today was a one-day repricing, watch for a reclaim of 7,470. Lose 7,420 = the digestion deepens; next support sits near 7,380.

- Confirmation rule: Don’t fade or chase the open. Let the first reaction to jobless claims print and confirm before committing. The market is re-anchoring to a new Fed path — wait for the structure, never the headline. No alignment, no trade.

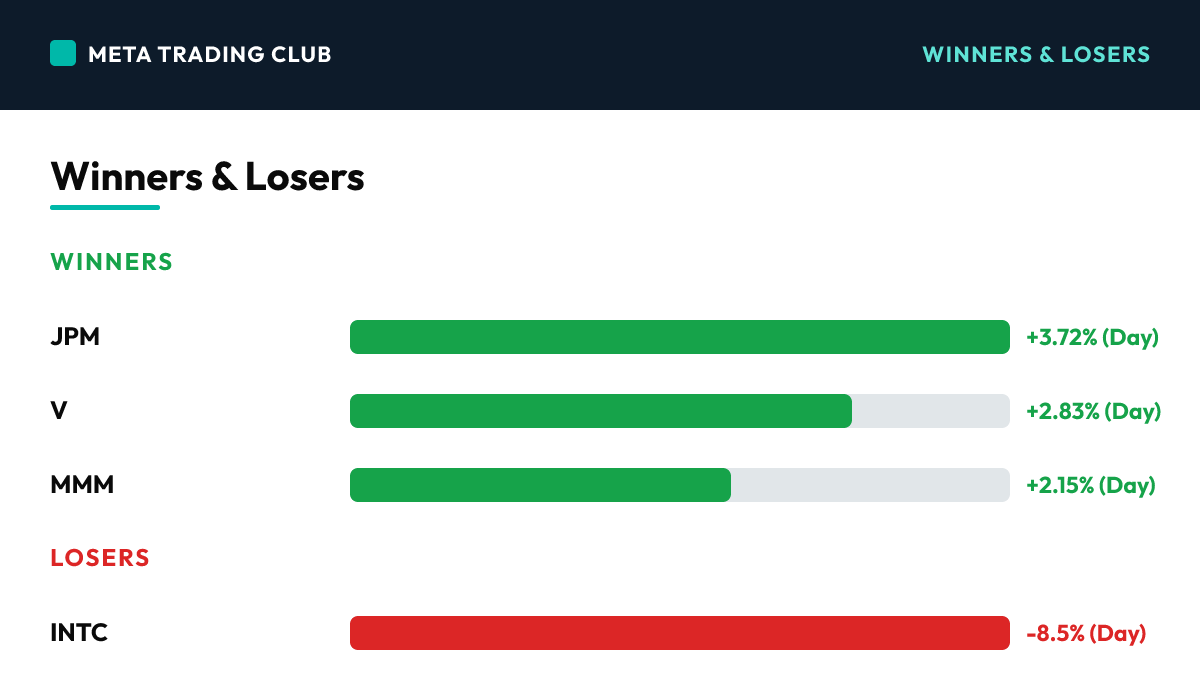

Winners & Losers

Winners

| JPM | JPMorgan Chase | +3.72% (Day) | Day Session — financials led as higher yields are seen as a margin tailwind for banks; the day’s strongest blue-chip |

| V | Visa | +2.83% (Day) | Day Session — payments and financials caught the rotation bid as money moved toward yield-sensitive names |

| MMM | 3M | +2.15% (Day) | Day Session — industrial bellwether bucked the broad selloff, closing green against a red tape |

Losers

| INTC | Intel | -8.5% (Day) | Day Session — worst of the chip complex as a strong recent rally unwound into the higher-for-longer Fed message |

| AMD | Advanced Micro Devices | -7.3% (Day) | Day Session — high-beta semi hammered in the post-Fed risk-off; profit-taking met the rate repricing |

| MU | Micron | -6.2% (Day) | Day Session — memory names slid hard as the semiconductor selloff led the Nasdaq lower |

What It Sets Up For Tomorrow

Levels Into Tomorrow

- SPX 7,420 — The new line in the sand after today’s break of 7,500. Hold above = one-day repricing, watch for a reclaim toward 7,470. Break below = digestion deepens; next support near 7,380.

- Nasdaq 26,000 — Round-number support right at today’s close. Hold = the semi selloff is profit-taking; lose it = the chip de-risking has further to run.

- VIX 18.4 — Below 20 = orderly repricing, not stress. A push above 20 = the market is treating the hawkish Fed as a regime change, not a one-day event.

Bull case: Today proves to be a one-day repricing. Jobless claims come in soft enough to keep a 2026 hike from feeling urgent, Fed speakers soften the dot-plot message, yields ease back off 4.50%, and the S&P holds 7,420 and reclaims toward 7,470 as dip-buyers step into the oversold semis.

Bear case: The market keeps re-anchoring to higher-for-longer. Yields push past 4.50%, the chip selloff extends, financials can’t carry the tape alone, and the S&P loses 7,420 toward the 7,380 zone as the dovish positioning of the last month continues to unwind.

What We’re Watching

- 10-Year yield vs 4.50% — the cleanest tell. Yields holding or pushing higher keeps pressure on growth/tech; a pullback under 4.45% would relieve the equity tape.

- Initial Jobless Claims, Thu 8:30 AM ET — the firming labor market is the Fed’s stated cover for the hawkish tilt. A jump in claims undercuts that story and could spark a relief bid.

- Semiconductor stabilization — does today’s chip wreck (INTC -8.5%, AMD -7.3%) find a floor, or does the de-risking accelerate? The semis are the high-beta tell for risk appetite.

Risks Into Tomorrow

- Hawkish Fed Repricing — The dot plot’s shift from a cut to a possible hike is the dominant risk. If yields keep climbing and the market re-anchors to higher-for-longer, the months-long dovish positioning has more to unwind, pressuring growth and tech.

- Semiconductor De-Risking — Today’s chip wreck (INTC -8.5%, AMD -7.3%, MU -6.2%) shows the highest-beta corner of the market unwinding fast. Whether semis find a floor or keep sliding is the key tell for broad risk appetite into Thursday.

- Rotation Cushions the Blow — Financials closing green (JPM +3.72%, V +2.83%) on higher yields shows money rotating rather than fleeing. An orderly repricing with leadership rotating beats a broad-based capitulation — a constructive sign even on a down day.

Frequently Asked Questions

How did the S&P 500 close today?

On Wednesday, June 17, 2026, the S&P 500 closed at 7,421.54 (-1.21%), with the VIX at 18.4. The Fed held — and the market still broke.

What drove the market today?

FED HOLDS, DOTS GO HAWKISH — The FOMC kept rates at 3.50-3.75% in Warsh’s first decision, but nine of eighteen members now project a HIKE by year-end (March showed a cut). Traders moved to fully price one quarter-point hike for 2026 — the single catalyst behind the selloff.

What levels matter for tomorrow?

SPX 7,420 — The new line in the sand after today’s break of 7,500. Hold above = one-day repricing, watch for a reclaim toward 7,470. Break below = digestion deepens; next support near 7,380. Nasdaq 26,000 — Round-number support right at today’s close. Hold = the semi selloff is profit-taking; lose it = the chip de-risking has further to run. VIX 18.4 — Below 20 = orderly repricing, not stress. A push above 20 = the market is treating the hawkish Fed as a regime change, not a one-day event.

How does Meta Trading Club prepare for the next session?

We wrap every session and carry the read forward through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

New to this? Start with the free training.

Learn how we read the market before you risk a dollar — our free education library and ebook break down the fundamentals step by step.

Free education → Get the free ebookTrade the next session with us live. Start your 7-day free trial →

The session’s over. The prep isn’t.

This is how MTC members close each day — wrap what happened, mark the levels, and carry one clean read into tomorrow. If you want to build that habit and qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process. It’s application-based — see if it’s a fit.

Explore the MTC Incubator → Apply nowSources: Yahoo Finance | CNBC | TheStreet | Investing.com — June 17, 2026. For educational purposes only. Not financial advice.