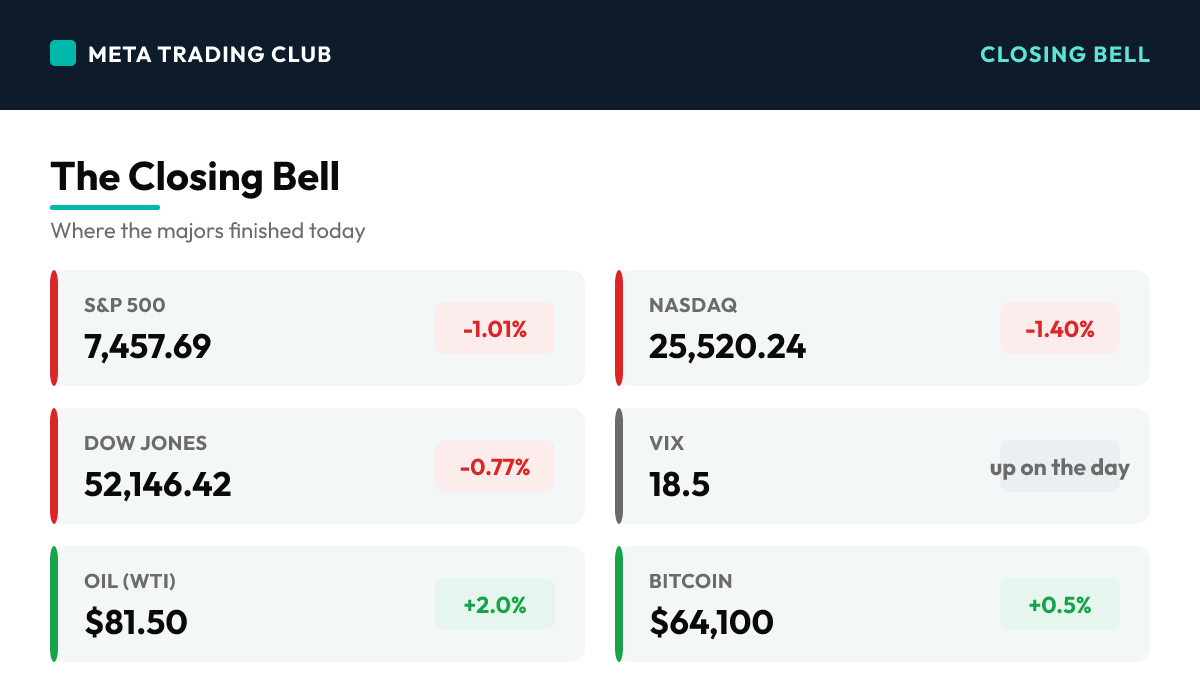

Friday, July 17, 2026 · 4:30 PM ET · MTC Market Close

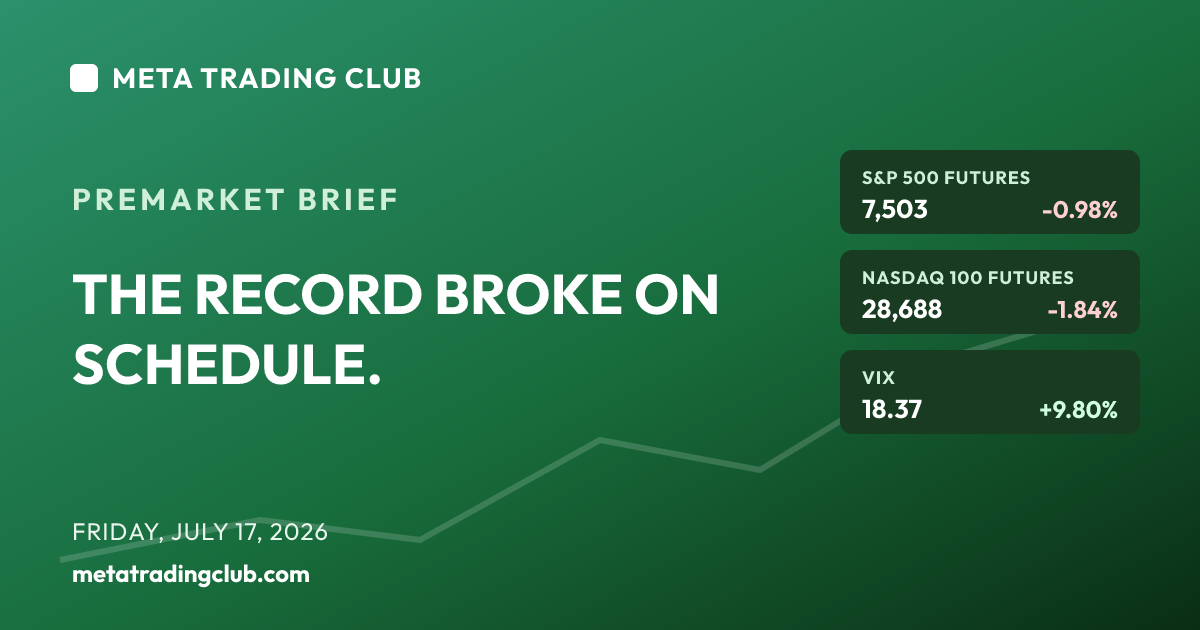

The crack became a break. What started midweek as a wobble in the chips turned Friday into a broad, all-red close and a losing week for every major index. The S&P 500 fell 1.01% to 7,457.69, the Nasdaq dropped 1.40% to 25,520.24, and the Dow lost 0.77% to 52,146.42 — and this time there was no green Dow to hide behind. Even the Russell 2000 slipped, down 0.39% to 2,962.99. Two things drove it. First, the semiconductor rout went from theme to correction: the PHLX Semiconductor Index is now roughly 20% off its highs, with Nvidia down about 3.8%, and AMD and Lam Research getting hit hard as the market keeps re-pricing whether the AI hyperscalers will spend at the pace this rally assumed. Second, Netflix — which reported after Thursday’s bell — cratered about 11% on soft forward guidance, the exact after-hours catalyst Thursday’s setup flagged, and it dragged Communication Services to the bottom of the board. The one place money did hide was the classic defensive corner: Consumer Staples and Utilities bucked the tape, Walmart added about 2%, and Travelers ripped roughly 6.4% on a clean earnings beat to lead the entire Dow. Health Care held firm with UnitedHealth up another 2.6%. So the rotation-into-defense that showed up Thursday is still running — it just couldn’t stop the broad tape from bleeding this time. Cross-asset told the same risk-off story with one loud exception. The VIX rose but stayed sub-20 near 18.5 — stressed, not panicked. The 10-year steadied around 4.56%, gold sat flat near $4,017, and Bitcoin held around $64,100. The exception is crude: WTI pushed up about 2% to roughly $81.50 as the Middle East conflict intensified and the Strait of Hormuz stayed a live risk — the one macro variable still leaning against disinflation and squarely on every desk’s mind. Here is the honest read. Thursday the whole game was 7,500 as the shelf that had to hold. Today it didn’t. The S&P closed at 7,457.69, its first finish below 7,500 in two weeks, with the semis in a full correction and Netflix confirming that this market will no longer pay up for growth it has to take on faith. So the level flips again. 7,500 is now overhead — the ceiling the bulls have to reclaim to prove Friday was a bear trap. Below it, 7,400 is the floor that decides whether this is a controlled pullback or the start of something deeper. Lose 7,400 with the chips still bleeding into next week’s megacap-tech earnings and the base that held all of June is gone. No alignment, no trade.

The Closing Bell

| Instrument | Close | Change | Note |

|---|---|---|---|

| S&P 500 | 7,457.69 | -1.01% | Closed below the 7,500 shelf for the first time in two weeks — the base that held all of June finally gave way. An all-red tape with no Dow cover, and the third down session in a row as the chip weakness spread from a single group into the whole index |

| Nasdaq | 25,520.24 | -1.40% | The weakest major again as the semiconductor rout hit correction — the PHLX Semiconductor Index is now ~20% off its highs, Nvidia -3.8%, with AMD and Lam Research hit hard. Netflix’s ~11% drop piled on. The AI-chip leadership that carried the rally is now its heaviest anchor |

| Dow Jones | 52,146.42 | -0.77% | No safe harbor this time. The Dow that closed green Thursday finished firmly red, down 406 points, dragged by Caterpillar -4.4% and Goldman -3.2% even as Travelers and Walmart tried to cushion it. Broad selling, not the tidy rotation of the prior session |

| Russell 2000 | 2,962.99 | -0.39% | Small caps outperformed on a relative basis but still closed red — the down-cap bid that led Thursday couldn’t fully offset the risk-off tone. The index slipped back under 2,970 as the whole board leaned lower into the weekend |

| VIX | 18.5 | up on the day | The fear gauge rose but held under 20 — enough to register a real correction in the chips and a losing week, not enough to signal a scramble. Stressed, not panicked: the tell of an orderly de-risking rather than a liquidation event |

| 10-Yr Yield | 4.56% | flat | Yields steadied near 4.56%, refusing to give the growth complex any relief — no flight-to-Treasuries rally even on a risk-off equity day, which kept the pressure squarely on the stretched tech multiples that led the drop |

| Gold | $4,017 | flat | Sat roughly flat despite the equity selloff and the hot Middle East headlines — a firm dollar and steady yields capped the haven bid again, a quiet non-confirmation on a day fear should have lifted it |

| Oil (WTI) | $81.50 | +2.0% | The loud exception. Crude pushed up about 2% above $81 as the Middle East conflict intensified and the Strait of Hormuz stayed a live risk — the one macro variable still leaning against disinflation and now adding an energy-cost headwind to a jittery tape |

| Bitcoin | $64,100 | +0.5% | Held near $64,100, barely green — steadier than the Nasdaq for once, but hardly a haven bid. Trading quietly as the equity complex did the selling, neither leading risk down nor catching a flight-to-safety flow |

Today’s Charts

Daily candlestick charts with 20/50/200-day moving averages — the index majors, the day’s biggest mover on each side, and the leading sector ETF.

Charts: Finviz (daily). Levels and overlays update through the next session.

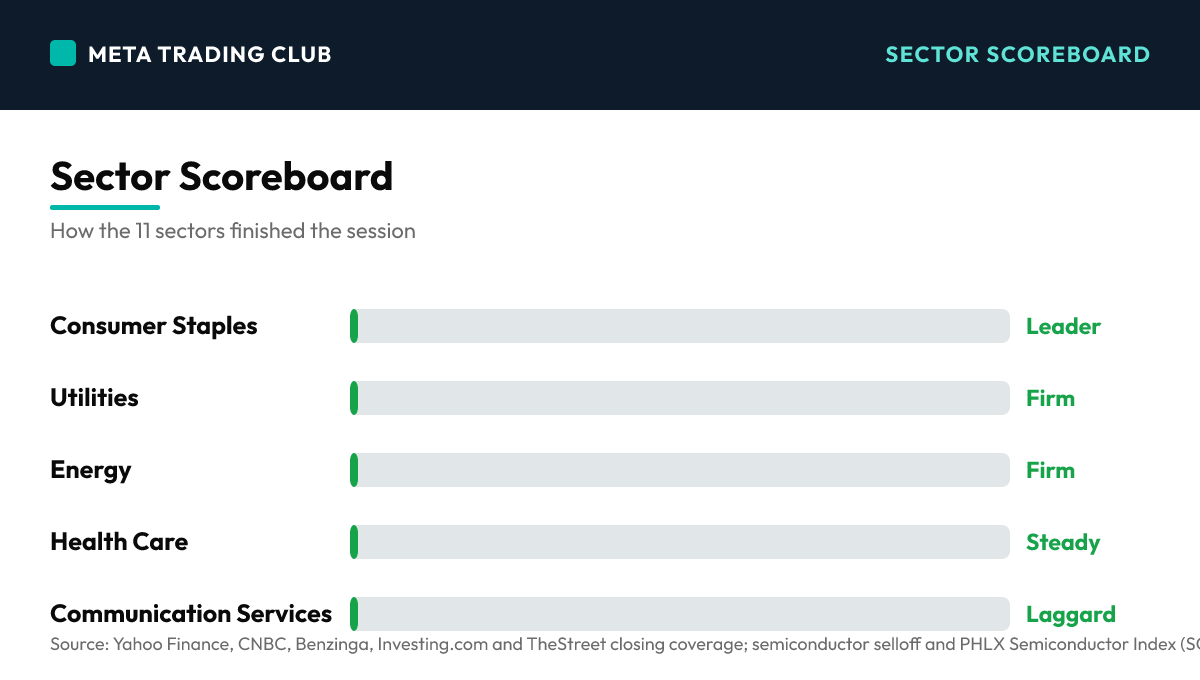

Sector Scoreboard

What Drove The Day

Friday was the session the market stopped pretending the chip weakness was contained. For two days the damage had been dressed up as rotation — green Dow, red Nasdaq, money simply moving from growth into defense. Today the disguise came off. Every major index closed red, every major index booked a weekly loss, and the semiconductor selloff crossed the line from a theme into a full correction, with the PHLX Semiconductor Index now roughly 20% below its highs. The S&P 500 fell 1.01% to 7,457.69, the Nasdaq dropped 1.40% to 25,520.24, the Dow lost 0.77% to 52,146.42, and even the Russell 2000 slipped 0.39% to 2,962.99. When small caps and the Dow go down with the Nasdaq, you are no longer looking at a rotation — you are looking at broad de-risking. The chips were the engine of the decline. Nvidia fell about 3.8%, and AMD and Lam Research were hit harder as investors kept re-pricing the core assumption of this entire rally: that AI hyperscaler capex would keep climbing without pause. Each session that assumption gets marked down a little more, and the group that led the market up all spring is now leading it lower with the most force. On top of the chip story sat Netflix, which had reported after Thursday’s close and collapsed about 11% Friday on soft forward guidance — precisely the after-hours catalyst Thursday’s setup had flagged. It dragged Communication Services to the bottom of the sector board and reinforced the week’s central lesson: this is a market that will no longer pay a premium for growth it has to take on faith. Not from the chipmakers, not from the streamer. Yet the defensive bid that surfaced Thursday did not disappear — it just couldn’t hold back the tide. Consumer Staples and Utilities were the only real green on the board. Travelers jumped roughly 6.4% on a clean earnings beat to lead the entire Dow, Walmart added about 2%, and UnitedHealth firmed another 2.6% to keep Health Care steady. The playbook was textbook risk-off: sell the expensive growth, hide in the reliable earnings. Cross-asset confirmed the character of the day, with one exception that keeps mattering. The VIX rose but stayed under 20 near 18.5 — real stress without panic. The 10-year steadied near 4.56% and refused to rally, denying the growth multiples any rate relief even on a down day for stocks. Gold sat flat near $4,017, a quiet non-confirmation of fear, and Bitcoin held around $64,100 without a haven bid. The exception was crude: WTI pushed up about 2% above $81 as the Middle East conflict intensified and the Strait of Hormuz stayed a live shipping risk — the one macro variable still leaning against the disinflation story and now stacking an energy-cost headwind on top of an already jittery tape. Put it together and the level that mattered has flipped for the second time this week. Thursday the shelf was 7,500 — the base defended for two weeks, the line that had to hold. Today it didn’t. The S&P closed at 7,457.69, its first finish below 7,500 in two weeks, with the semis in correction and Netflix confirming the tape’s message. So 7,500 is no longer support — it is resistance, the ceiling the bulls must reclaim to argue Friday was an overshoot and a bear trap. Below it, 7,400 becomes the real decision line. Hold 7,400 into next week and this reads as a controlled pullback inside an uptrend that had run hot. Lose 7,400 with the chips still bleeding into a heavy stretch of megacap-tech earnings, and the base that carried the whole June grind is gone — narrow strength that finally gave way to broad weakness.

MAJOR HEADLINES AND CATALYSTS

Top Market-Moving Stories

- THE CHIP ROUT HITS CORRECTION (Day) — The semiconductor selloff crossed from theme to correction, with the PHLX Semiconductor Index now roughly 20% off its highs. Nvidia fell ~3.8% and AMD and Lam Research were hit harder as the market kept re-pricing whether AI hyperscaler capex can keep climbing. The group that led the rally is now leading it lower.

- NETFLIX COLLAPSES ~11% ON SOFT GUIDANCE (Day) — Netflix, which reported after Thursday’s bell, sank about 11% Friday on a disappointing forward outlook — the exact after-hours catalyst Thursday’s setup flagged. It dragged Communication Services to the bottom of the board and underlined the week’s lesson: no premium for growth the market has to take on faith.

- ALL RED, LOSING WEEK — NO DOW COVER (Day) — Unlike the tidy green-Dow rotation of Thursday, every major index closed red Friday and booked a weekly loss. Even the Russell slipped. Money still hid in Staples, Utilities and Travelers, but the defensive bid couldn’t stop broad de-risking — the disguise of rotation finally came off.

Fed and Macro Context

- The 10-year yield steadied near 4.56% and refused to rally even on a risk-off equity day — no flight-to-Treasuries relief for the stretched growth multiples that led the drop, keeping the pressure squarely on high-beta tech into next week.

- Crude stayed the loud exception: WTI pushed up about 2% above $81 as the Middle East conflict intensified and the Strait of Hormuz remained a live shipping risk — an energy-cost headwind stacked on a jittery tape and the one macro theme still leaning against disinflation.

- Volatility rose but stayed contained: the VIX climbed toward 18.5 without breaking 20, and gold sat flat near $4,017 despite the selloff and hot geopolitics — a quiet non-confirmation of panic that frames Friday as orderly de-risking rather than a liquidation flush.

Single-Stock Standouts

- Travelers (TRV) was the day’s bright spot, up ~6.4% on a clean Q2 beat to lead the entire Dow. Walmart (WMT) added ~2% and UnitedHealth (UNH) firmed ~2.6% — the exact defensive-and-staples names that lead when a market rotates out of growth and reaches for reliable earnings.

- Nvidia (NVDA) fell ~3.8% as the semiconductor rout deepened into correction, with AMD and Lam Research (LRCX) hit harder — the AI-chip complex that led the rally now the heaviest drag for a third straight session on hyperscaler-capex skepticism.

- Netflix (NFLX) collapsed ~11% on soft guidance, the single sharpest move of the session, while Caterpillar (CAT) fell ~4.4% and Goldman Sachs (GS) dropped ~3.2% — cyclicals and growth punished together on a day the tape wanted to de-risk broadly.

AFTER-HOURS EARNINGS SPOTLIGHT

Tonight’s Slate

- LIGHT POST-CLOSE SLATE — Friday brought no major S&P names after the bell; the session’s story was written entirely in regular hours by the chips and by Netflix’s daytime collapse. The after-hours tape is quiet into the weekend, which puts the full weight of the read on Friday’s price action itself.

- The real earnings test is next week, not tonight. The Q2 megacap-tech slate ramps up — Alphabet headlines midweek, with Microsoft, Meta, Apple and Amazon clustered at month-end. Those prints will decide whether the AI-capex fear that gutted the chips this week is justified or overdone.

NEXT SESSION SETUP

Monday, July 20 — 7,400 Is the Floor, 7,500 Is the Ceiling

- The S&P starts Monday at 7,457, trapped between the 7,500 shelf it just lost and the 7,400 floor beneath it. The setup has flipped: 7,500 is now resistance to reclaim, 7,400 is support to defend. Hold 7,400 and this is a controlled pullback; lose it with the chips still bleeding and the June base is gone toward 7,300.

- The chips are still the tell. The SOX is ~20% off its highs — watch whether Nvidia, AMD and Lam Research find a floor Monday or keep leaking. If the semis stabilize, the pullback stays orderly; if they keep bleeding into next week’s megacap-tech earnings, the pressure spreads to the entire growth complex.

- Monday’s data slate is quiet, which hands the tape back to positioning and to oil. Watch crude — another leg higher on Middle East escalation stacks a fresh cost headwind — and watch whether the defensive bid in Staples, Utilities and Travelers-style earnings winners holds or fades on any bounce.

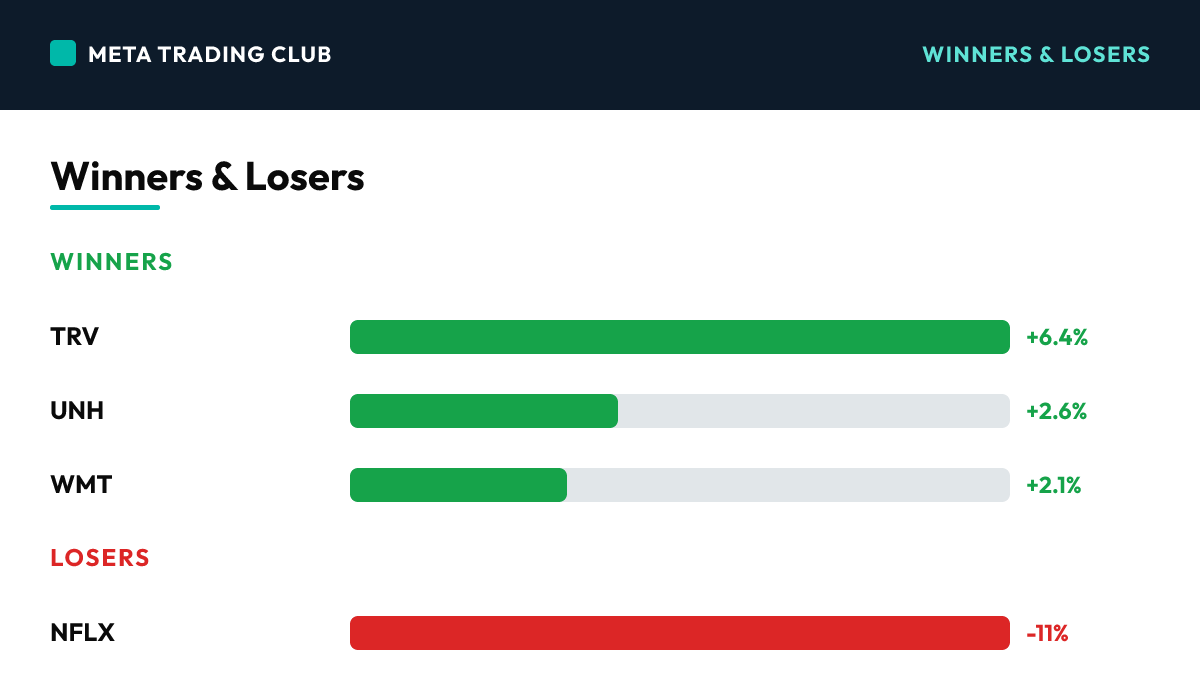

Winners & Losers

Winners

| TRV | +6.4% | Travelers was the day’s bright spot and the best stock in the Dow, jumping about 6.4% on a clean Q2 earnings beat — a defensive insurer rewarded for reliable results on exactly the kind of day the market pays up for certainty over growth | |

| UNH | +2.6% | UnitedHealth firmed another 2.6%, extending its defensive leadership into a second session and keeping Health Care steady — a safe-harbor name catching the rotation bid as money moved out of stretched tech and into reliable earners | |

| WMT | +2.1% | Walmart added about 2% as the staples bid broadened — a classic defensive winner on a risk-off day, the kind of recession-resistant name that leads when the market questions growth and reaches for steady cash flows |

Losers

| NFLX | -11% | Netflix collapsed about 11% on soft forward guidance — the sharpest move of the session and the exact after-hours catalyst Thursday’s setup flagged. A stock priced for perfection met an outlook that wasn’t good enough, dragging Communication Services to the bottom | |

| CAT | -4.4% | Caterpillar fell about 4.4%, the worst Dow component, as cyclicals were sold alongside growth on a day the tape wanted to de-risk broadly — industrial strength giving way to caution as the selloff widened beyond just the chips | |

| NVDA | -3.8% | Nvidia dropped about 3.8% as the semiconductor rout deepened into correction, with AMD and Lam Research hit harder — the AI-chip bellwether leading the group lower for a third straight session on hyperscaler-capex skepticism |

What It Sets Up For Tomorrow

Levels Into Tomorrow

- S&P 500 7,400 — THE FLOOR. Price closed at 7,457, about 60 points above it. This is the line that decides the character of the pullback. Hold it and Friday’s break of 7,500 reads as a controlled shakeout; lose it with the chips still in correction and the two-week base gives way toward 7,300 and the 50-day.

- S&P 500 7,500 — THE SHELF, NOW OVERHEAD RESISTANCE. The base that held for two weeks flipped to a ceiling Friday. Until the S&P reclaims 7,500 with the semis participating, the burden is on the bulls to prove the breakdown was a bear trap rather than the start of a broader unwind.

- S&P 500 7,300 — THE DOWNSIDE TARGET IF 7,400 GOES. Lose the floor and this is the next real support, near the 50-day, the level that would confirm the chip-led selloff has turned from pullback into correction. A clean break of 7,400 on continued chip weakness points here.

Bull case: The chips find a floor Monday, Netflix stays a contained single-name event, and Friday’s break of 7,500 proves to be an overshoot on a low-conviction summer Friday. The S&P reclaims 7,500, the defensive-earnings strength (Travelers, Walmart, UnitedHealth) broadens leadership beyond the megacaps, and next week’s megacap-tech prints justify the AI spend — turning this week’s fear into a buyable reset rather than a top.

Bear case: Semiconductors keep bleeding on AI-capex skepticism, the SOX correction deepens, and the megacap-tech earnings that start next week disappoint on guidance the way Netflix did. The S&P loses 7,400, the two-week base breaks, and the narrow-tape crack that started midweek becomes a full rotation-into-decline toward 7,300 and the 50-day — with oil adding a cost headwind on top.

What We’re Watching

- 7,400 — the floor is now the whole game. Hold it and Friday’s break of 7,500 is a controlled shakeout; lose it with the semis leaking and the June base breaks toward 7,300.

- The semiconductor group — the SOX is ~20% off its highs. Do Nvidia, AMD and Lam Research stabilize Monday, or does the AI-capex de-rate keep rolling through the market’s former leadership into a heavy earnings week?

- The defensive bid and oil — does the Staples/Utilities/Travelers strength hold and broaden, and does crude take another leg higher on Middle East escalation and stack a fresh cost headwind on an already cautious tape?

Risks Into Tomorrow

- The chip de-rate is now a correction, not a wobble — For three sessions the semiconductor selloff was framed as rotation; Friday it crossed 20% off the highs and became a correction. Nvidia -3.8%, AMD and Lam Research worse, and the group that led the entire rally is now its heaviest anchor. Until the chips find a floor, every bounce in the broad market is suspect — the market’s former engine has become its biggest risk.

- A market that won’t pay for faith-based growth — Netflix reported a fine quarter and still gapped down ~11% on guidance; the chips keep selling on the fear that AI capex slows. The through-line is a tape that has stopped paying a premium for growth it has to take on trust. That reflex shift — not any single print — is the real signal, and it puts every richly-valued name on the clock into next week’s megacap-tech earnings.

- 7,400 is now the whole game — The setup flipped again: Thursday it was 7,500 as the shelf that had to hold, and Friday it broke. Now 7,500 is resistance overhead and 7,400 is the floor beneath a 7,457 close. Hold 7,400 and this is a controlled pullback inside a hot uptrend; lose it with the semis still bleeding and Netflix-style guidance fear spreading, and the June base is gone toward 7,300 and the 50-day. The level is the entire read.

Frequently Asked Questions

How did the S&P 500 close today?

On Friday, July 17, 2026, the S&P 500 closed at 7,457.69 (-1.01%), with the VIX at 18.5. The crack became a break.

What drove the market today?

THE CHIP ROUT HITS CORRECTION (Day) — The semiconductor selloff crossed from theme to correction, with the PHLX Semiconductor Index now roughly 20% off its highs. Nvidia fell ~3.8% and AMD and Lam Research were hit harder as the market kept re-pricing whether AI hyperscaler capex can keep climbing. The group that led the rally is now leading it lower.

What levels matter for tomorrow?

S&P 500 7,400 — THE FLOOR. Price closed at 7,457, about 60 points above it. This is the line that decides the character of the pullback. Hold it and Friday’s break of 7,500 reads as a controlled shakeout; lose it with the chips still in correction and the two-week base gives way toward 7,300 and the 50-day. S&P 500 7,500 — THE SHELF, NOW OVERHEAD RESISTANCE. The base that held for two weeks flipped to a ceiling Friday. Until the S&P reclaims 7,500 with the semis participating, the burden is on the bulls to prove the breakdown was a bear trap rather than the start of a broader unwind. S&P 500 7,300 — THE DOWNSIDE TARGET IF 7,400 GOES. Lose the floor and this is the next real support, near the 50-day, the level that would confirm the chip-led selloff has turned from pullback into correction. A clean break of 7,400 on continued chip weakness points here.

How does Meta Trading Club prepare for the next session?

We wrap every session and carry the read forward through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

New to this? Start with the free training.

Learn how we read the market before you risk a dollar — our free education library and ebook break down the fundamentals step by step.

Free education → Get the free ebookThe session’s over. The prep isn’t.

This is how MTC members close each day — wrap what happened, mark the levels, and carry one clean read into tomorrow. If you want to build that habit and qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process. It’s application-based — see if it’s a fit.

Explore the MTC Incubator → Apply nowSources: Yahoo Finance, CNBC, Benzinga, Investing.com and TheStreet closing coverage; semiconductor selloff and PHLX Semiconductor Index (SOX) correction data; Netflix Q2 after-hours report and soft guidance; Travelers, UnitedHealth and Walmart mover data; Caterpillar, Nvidia, AMD and Lam Research declines; 10-year Treasury, VIX, gold, WTI crude and Bitcoin levels; Middle East conflict and Strait of Hormuz shipping risk; week-of-July-20 megacap-tech earnings preview — verified as of 4:30 PM ET July 17, 2026. For educational purposes only. Not financial advice.