Everyone’s buying Nvidia. Almost nobody’s buying the companies Nvidia buys from. That’s the mistake — and this week the market made the case for us.

In every gold rush, the miners get the headlines. The people who quietly got rich sold the picks and shovels. AI infrastructure suppliers are this cycle’s pick-and-shovel trade: every GPU cluster needs optics, cables, connectivity and cooling, and the companies supplying those parts are compounding while the crowd fights over the same seven mega-caps.

This was a volatile week to prove it. The Federal Reserve — in its first meeting under new Chair Kevin Warsh — held rates at 3.50–3.75% but turned hawkish, with the dot plot now leaning toward hikes in 2026 as May CPI hit a three-year high of 4.2%. Stocks sold off, then rebounded hard after the U.S. signed an interim peace deal with Iran, reopening the Strait of Hormuz and collapsing the oil and gold war premium. The rebound was led, once again, by AI infrastructure.

Why one layer down beats the front-page name

The edge in AI infrastructure suppliers isn’t found in the name everyone’s already talking about. It’s one layer down — in the verifiable supplier with a real, nameable demand link.

The three-layer stack

Layer 1 — the crowded GPU names everyone owns.

Layer 2 — the suppliers analysts already cover.

Layer 3 — the gold: the unglamorous input nobody thinks about.

A name only makes our report if it sells into a hot customer, stays under-covered, has real pricing power, and traces a verifiable demand link. No link, no pick.

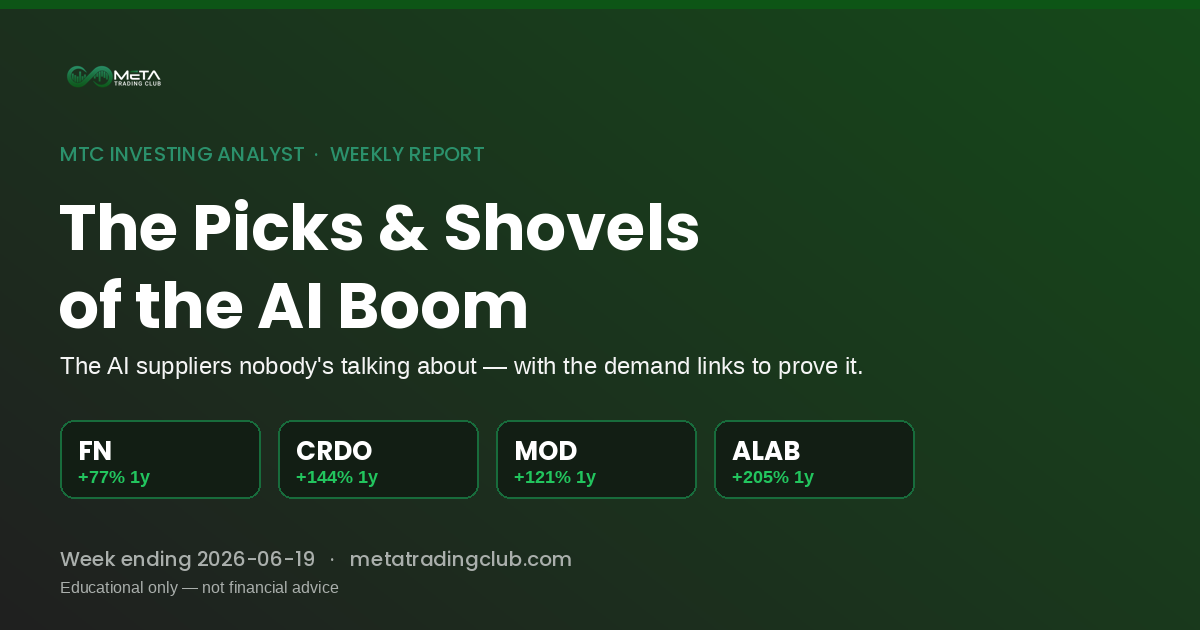

The four AI infrastructure suppliers on our radar

Fabrinet

Optics

Makes the high-precision optical transceivers (800G now, 1.6T next) that move data across an AI cluster.

Nvidia was 27.6% and Cisco 18.2% of FY25 revenue; the largest customer is over 30%. FY26 revenue tracking ~$4.55B (+33% y/y).

That same customer concentration cuts both ways — one design loss hurts, and Coherent is pushing in.

Attractive under $560. (~+77% over the past year.)

Credo Technology

Connectivity — cables

The “$300 purple cables” — Active Electrical Cables — wiring AI racks, where Credo holds ~88% share.

Largest customers are Microsoft and Amazon; three hyperscalers each contributed >10% of revenue last quarter. FY26 revenue ~$1.3B at ~49.6% operating margin.

~90% of revenue sits in the top 10 customers, and it leans on TSMC for wafers.

On a pullback under $260. (~+144% over the past year.)

Astera Labs

Connectivity — silicon

PCIe retimers, CXL switches and memory connectivity — the “plumbing” that keeps signals clean in big training clusters.

Structural demand from Google, AWS and Microsoft. Q1 2026 revenue $308M (+93% y/y); Q2 guided to $355–365M.

Rich valuation and direct sensitivity to hyperscaler capex timing.

Under $400. (~+205% over the past year.)

Modine Manufacturing

Cooling

An old-line radiator maker re-rating into a pure-play data-center thermal story.

A long-term agreement reserving over $4B of cooling products for 2027–2029. Data-center sales rose 158% y/y and crossed $400M in a quarter; FY26 sales $3.2B (+23%).

Execution on capacity, and industrial cyclicality if the buildout slows.

Under $285. (~+121% over the past year.)

What this means for investors

After an 8–23% week in many AI names, the front-page tickers are pricing perfection. Our posture: stay patient and lean into quality on dips, not strength. The better risk/reward sits with the suppliers that have contracted, nameable demand — bought near the entry levels above, not chased at the highs. Keep dry powder paid at 4%+, and respect that a Fed weighing hikes is a different game than a Fed cutting.

FAQ

What are “AI infrastructure suppliers”?

They are the companies that sell the physical components every AI data center needs — optical transceivers, high-speed cables, connectivity silicon, and cooling systems — rather than the GPUs themselves. They sit one layer down the supply chain from names like Nvidia.

Why invest in suppliers instead of Nvidia directly?

Suppliers often carry less hype, better-defended margins, and more room to re-rate. The demand is the same hyperscaler capex — it just flows to a company the crowd hasn’t crowded into yet. The trade-off is customer concentration risk, which should always be named.

Which AI infrastructure suppliers does MTC highlight this week?

Fabrinet (FN) in optics, Credo (CRDO) in active electrical cables, Astera Labs (ALAB) in connectivity silicon, and Modine (MOD) in data-center cooling — each with a verified link to a named hyperscaler customer.

What is a “demand link” and why does it matter?

A demand link is a named customer, contract, or capex line that flows to the supplier. It’s the difference between a story and a thesis. Every pick we publish must trace one — no link, no pick.

Trade the next session with us live. Start your 7-day free trial →

Learn to find these setups yourself.

The MTC Investing Analyst exists to build independent investors — not signal followers. Applications for the MTC Incubator are open.

Disclaimer: This article is for educational purposes only and is not financial, investment, tax, or legal advice. Meta Trading Club is not a registered investment adviser. Markets carry risk, including loss of principal. Entry levels are illustrative analytical reference points, not solicitations to buy or sell. Prices referenced are as of the close on 2026-06-18. Do your own research and consult a licensed professional before investing.