Tuesday, July 14, 2026 · 8:45 AM ET · MTC Market Intelligence

Good news finally showed up — and the tape barely moved. June CPI landed cool at 8:30, headline inflation cooling to 3.5% year-over-year (well under the ~3.8-3.9% the Street looked for) and falling 0.4% on the month, dragged down by a 5.7% drop in energy prices. Then Q2 bank earnings opened with a bang: Goldman blew the doors off at $20.98 a share versus $14.48 expected, and JPMorgan and Bank of America both cleared the bar. On paper, that’s the dovish-inflation-plus-solid-banks combo bulls have been waiting for. And yet futures are mixed-to-soft — Dow -0.3%, S&P -0.2%, Nasdaq-100 barely green at +0.2%. Why? Three weights. One, oil won’t quit: WTI is up ~2% to ~$79.56 as Trump reinstates a naval blockade on Iranian shipping through the Strait of Hormuz and floats a 20% vessel fee — the geopolitical premium is sticky. Two, IBM cratered ~17% on weak preliminary Q2 numbers, a single-name gut-punch that reminds everyone earnings season cuts both ways. Three, the AI hyperscalers are wobbling — Microsoft and Oracle both down ~3% on capex and rate-path jitters — even as the semicap names (Applied Materials +5.3%, Teradyne +4.9%, Monolithic Power +4.5%) and Micron (+3%) catch a bid. Cross-asset, the tone is a measured de-risk, not a panic: VIX front-month sits near 17.5 (Friday spot was 15.02), the 10-year holds 4.58%, gold slid 2.4% to ~$4,015 as the cool print took some haven urgency off, and Bitcoin eased to ~$62,600. Here’s the map. The S&P closed Monday at 7,515.34 — right on top of 7,500, the line it has defended all last week. That level is now the whole ballgame: hold 7,500 with cool inflation and bank beats as fuel, and this is a base being built for another run at Friday’s 7,575 record. Lose it, and the message is that good news wasn’t enough — and the tape leaks toward 7,480 and the 7,420 breakout shelf. Core CPI is still sticky near 2.9%, oil is still the switch, and a 17% IBM air-pocket says respect the tape. Trade the reaction at 7,500, not the headline. No alignment, no trade.

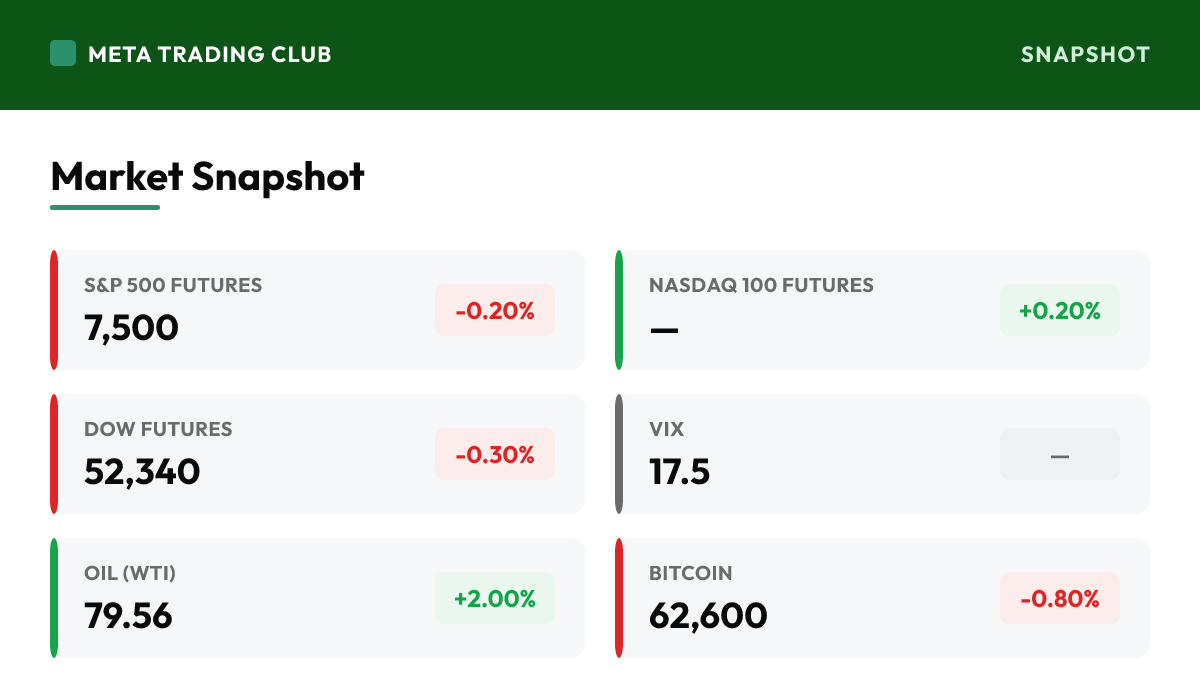

Market Snapshot

| Instrument | Level | Change | Note |

|---|---|---|---|

| S&P 500 Futures | 7,500 | -0.20% | Sitting just under Monday’s 7,515.34 close despite a cool CPI and bank beats — the good news isn’t lifting the tape. 7,500 is the line held all last week; hold it and a base builds, lose it and the week’s gains leak |

| Nasdaq 100 Futures | — | +0.20% | Barely green — semicap and Micron strength (AMAT +5.3%, Micron +3%) offset Microsoft and Oracle both down ~3% on AI-capex and rate jitters. A split inside the index rather than one-way conviction |

| Dow Futures | 52,340 | -0.30% | The softest major this morning — IBM down ~17% on weak preliminary Q2 numbers is a heavy single-name drag on the price-weighted index, more than offsetting the solid bank prints |

| Russell 2000 Futures | — | — | No clean premarket read; small-caps typically follow the S&P on a mixed, headline-driven open — treat the Russell as a follower today, not an independent tell |

| VIX | 17.5 | — | Front-month sits near 17.5 after Friday’s spot close of 15.02 — bid on the Iran-Hormuz escalation and the CPI/earnings double-header. Elevated but not crisis-level; watch it climb if crude keeps running |

| 10-Yr Yield | 4.58% | — | Holding near 4.58% — the cool CPI eases some rate-path pressure, but sticky core near 2.9% and rising oil keep yields firm. The number to watch as banks report on net interest margins |

| Oil (WTI) | 79.56 | +2.00% | Up ~2% to ~$79.56 as Trump reinstates a naval blockade on Iranian shipping through Hormuz and floats a 20% vessel fee. Crude is the switch — the geopolitical premium is sticky and it caps any relief rally |

| Gold | 4,014 | -2.40% | Slid 2.4% to ~$4,015 as the cool CPI took some haven urgency off the table; the pullback in the hedge fits a market treating the backdrop as a measured de-risk rather than a scramble for safety |

| Bitcoin | 62,600 | -0.80% | Eased to ~$62,600, down ~$490 on the day, leaning with the risk-off tilt as a risk asset rather than a haven — crypto is not catching the safety flows and is trading with growth this morning |

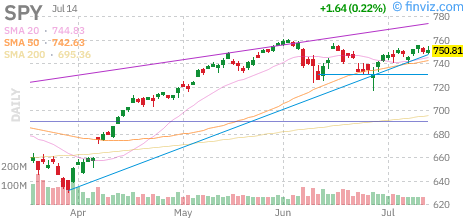

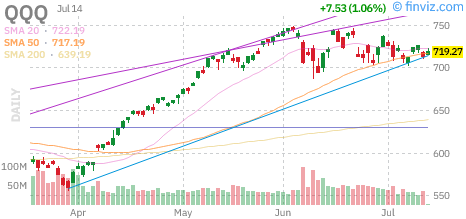

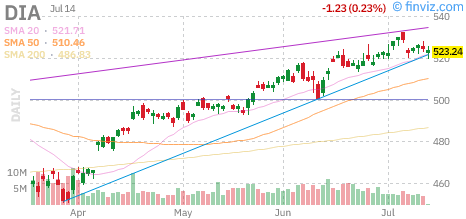

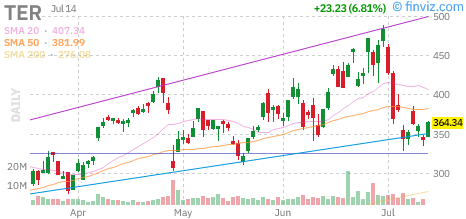

Charts to Watch

Daily candle charts with moving averages for the index proxies and today’s standout mover. Source: Finviz.

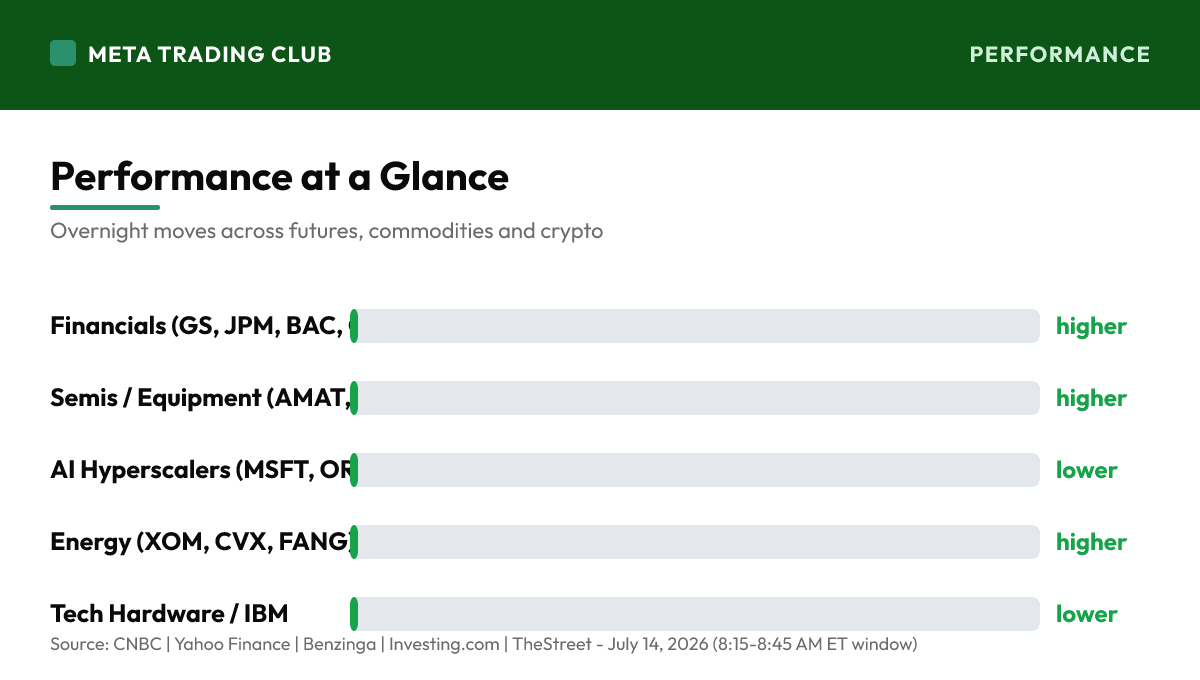

Performance at a Glance

Overnight & Global Markets

The setup this morning is a lesson in reactions. The market got exactly the fuel bulls have been asking for — a cool June CPI at 3.5% headline (below the ~3.8-3.9% Street estimate, dragged down by a 5.7% drop in energy) and a strong open to Q2 bank earnings, led by a Goldman blowout at $20.98 versus $14.48 expected, with JPMorgan and Bank of America both clearing the bar. That’s dovish inflation plus healthy financials, the combo that usually lifts a tape. And yet futures are mixed-to-soft: Dow -0.3%, S&P -0.2%, Nasdaq-100 only +0.2%. When good news can’t move the market, that’s the tell worth listening to. Three weights explain it. Oil is the first — WTI up ~2% to ~$79.56 as Trump reinstates a naval blockade on Iranian shipping through the Strait of Hormuz and floats a 20% vessel fee; the geopolitical premium is sticky and it caps relief. IBM is the second — down ~17% on weak preliminary Q2 numbers, a single-name air-pocket that drags the price-weighted Dow and reminds everyone earnings season cuts both ways. The AI hyperscalers are the third — Microsoft and Oracle both off ~3% on capex and rate-path jitters, even as the semicap complex (Applied Materials +5.3%, Teradyne +4.9%, Monolithic +4.5%) and Micron (+3%) catch a rotation bid. Cross-asset, nothing is screaming crisis: VIX front-month near 17.5 versus Friday’s spot 15.02, the 10-year steady at 4.58%, gold down 2.4% as haven urgency fades, and Bitcoin easing with the risk tone. That reads as a measured de-risk, not a flush — a market weighing genuinely good macro news against a sticky-core, oil-pressured, single-name-air-pocket backdrop. So the question for Tuesday isn’t whether the news was good. It was. The question is whether the tape can convert good news into a hold above 7,500 — or whether the muted reaction is telling you the buyers aren’t there at these levels yet.

MAJOR HEADLINES AND CATALYSTS

Top Premarket Stories

- June CPI came in cool. Headline inflation slowed to 3.5% year-over-year — below the ~3.8-3.9% the Street expected — and fell 0.4% on the month, dragged down by a 5.7% drop in energy prices. That’s the dovish print bulls wanted, but core is still sticky near 2.9%, keeping the Fed from declaring victory. The market’s muted reaction is the story.

- Q2 bank earnings opened strong. Goldman Sachs blew past estimates at $20.98 a share versus $14.48 expected (shares +1.4%), while JPMorgan ($6.14) and Bank of America ($1.21, revenue $31.7B) both beat. A firmer 10-year near 4.58% is a tailwind for margins. Financials are the one group with a real, earnings-driven catalyst this morning.

- IBM cratered ~17% on weak preliminary Q2 numbers — the single-name air-pocket of the session and a heavy drag on the price-weighted Dow. Ericsson fell ~10% and Apple slipped ~1% on a KeyBanc downgrade to underweight. Earnings season is cutting both ways, and the losers are a reminder to respect the tape.

- Oil is still the switch. WTI is up ~2% to ~$79.56 after Trump reinstated a naval blockade on Iranian shipping through the Strait of Hormuz and floated a 20% vessel fee. The geopolitical premium is sticky, it keeps yields firm despite the cool CPI, and it caps any relief rally the inflation print might otherwise fuel.

Stock-Specific

- The tech tape is split, not one-way. Microsoft and Oracle are both down ~3% on AI-capex and rate jitters, while the equipment and memory names run — Applied Materials +5.3%, Teradyne +4.9%, Monolithic +4.5%, Micron +3%. That’s a rotation inside tech, not a broad exit; read the leadership by group, not by the index headline.

- IBM (~-17%) is the single-name tell of the morning. A 17% gap on weak preliminary Q2 numbers shows how fast an earnings miss reprices a stock, and how much a price-weighted index like the Dow feels it. When the calendar is loaded, respect that any name can air-pocket — position size is the defense, not conviction.

Global and Macro

- This is a rare double-header: June CPI at 8:30 landed the same morning as the biggest Q2 bank prints. Fed Chair nominee Warsh’s congressional testimony is also on the docket, adding a rate-path wildcard. The scheduled catalysts are dense — but the tape’s read is coming from how it digests good news, not from any single headline.

- The Strait of Hormuz remains the macro override. With Trump reinstating an Iranian shipping blockade and a 20% vessel fee, crude can reprice on a single headline — and an oil-driven lift in inflation expectations is exactly what keeps the 10-year firm near 4.58% even after a cool CPI. Let oil and the rate market lead the read today.

TECHNICAL ANALYSIS

S&P 500 Key Levels

- SPX closed Monday at 7,515.34 — right on top of 7,500, the line it has defended all last week. This morning’s soft futures put the open back toward that level. 7,500 is now the whole ballgame: hold it with cool CPI and bank beats as fuel and a base is building; lose it and the message is that good news wasn’t enough.

- Below 7,500, the next shelves are 7,480 and then the 7,420 breakout floor. Above, 7,540 is the near-term reclaim and 7,575 is Friday’s record — now resistance-from-above the market has to earn back before the breakout is live again. Trade the reaction at 7,500; that’s the risk anchor for every decision today.

- Bias: cautious-constructive. The macro fuel is genuinely bullish — a cool print and strong banks — but the muted futures reaction, a 17% IBM air-pocket and sticky oil say the buyers aren’t confirming yet. That’s a market to trade off the level, not the headline. Let 7,500 and the 10-year confirm before leaning either way.

Sector and Sentiment

- Read the reaction, not the news. Cool CPI plus a Goldman blowout is the kind of setup that should lift a tape — and futures are mixed-to-soft. When good news can’t move the market, it usually means the good news was already priced, or a competing weight (oil, IBM, hyperscaler capex) is offsetting it. Both are true this morning.

- The rotation is the constructive tell underneath the soft headline. Semis equipment and Micron are bid while megacap AI wobbles, and financials lead on real earnings — money is moving between groups, not fleeing the market. That’s healthy churn, not liquidation, and it supports the 7,500 hold as long as breadth stays two-sided.

- VIX front-month near 17.5 versus Friday’s 15.02 spot says the options market is pricing a shock to absorb — the CPI/earnings double-header plus Iran — not a crisis to hedge into. Supportive for the 7,500 hold, but conditional on crude. A VIX that climbs through the high-teens with WTI still rising is the sign the tape has stopped absorbing.

TODAY’S ECONOMIC CALENDAR

Key Releases (ET)

- June CPI (8:30 AM) is the headline release and it landed cool — 3.5% headline, -0.4% on the month, with core still sticky near 2.9%. The number is dovish on its face, but the market’s muted reaction and firm 10-year say the sticky core and rising oil are the parts traders are weighting into the Fed’s next decision.

- Fed Chair nominee Kevin Warsh’s congressional testimony is the rate-path wildcard on the docket. Any signal on how he reads a cool-headline, sticky-core inflation backdrop against an oil-driven premium can move the 10-year — and the 10-year near 4.58% is the swing factor for both the growth trade and the bank margin story today.

- The 10-year near 4.58% is the number to watch all session. A cool CPI would normally pull yields down, but sticky core and a rising oil premium are holding them firm. Whether yields ease or grind higher from here decides whether the growth wobble (MSFT, ORCL) is a one-morning rotation or the start of real pressure on the highs.

Earnings Today

- The marquee event is the banks, all before the open: Goldman Sachs ($20.98 vs $14.48, a blowout), JPMorgan ($6.14), Bank of America ($1.21, revenue $31.7B), with Citigroup and Wells Fargo in the same window. The prints are strong and a firm 10-year helps margins — financials are the group with a genuine, confirmed catalyst this morning.

- The other side of the calendar is the warning: IBM down ~17% on weak preliminary Q2 numbers and Ericsson off ~10%. Earnings season delivers air-pockets as readily as beats, and a 17% gap in a Dow component is a live reminder that the loaded calendar this week can cut a portfolio both ways. Respect the tape and size accordingly.

PREMARKET PLAYBOOK

Key Levels

- SPX 7,500 — the line that matters. The market defended it all last week and Monday closed right on it at 7,515.34. This is the level that decides whether cool CPI and bank beats build a base or whether the muted reaction wins. Hold it and dips stay buyable toward a record retest; lose it and the week’s gains leak. React to it, don’t predict it.

- SPX 7,575 — Friday’s record, now resistance-from-above. With futures soft, the open sits well below the record close, so the market has to earn its way back through 7,540 first before the breakout is live again. A reclaim that holds re-arms the uptrend; a rejection says the good news wasn’t enough to clear the ceiling.

- Oil and the 10-year — the confirmation pair. WTI +2% on the Hormuz blockade and the 10-year firm at 4.58% are what’s keeping the cool CPI from lifting the tape. Crude cooling and yields easing would let the good news finally work; both staying firm keeps the ceiling on. Watch this pair before trusting any move at 7,500 or the record.

Bull case: Hold 7,500 with crude stalling and the 10-year easing, and the cool CPI plus the bank beats finally get to work — financials lead, the semis rotation broadens, and the S&P builds a base to retake 7,540 and then challenge Friday’s 7,575 record. A calm reaction to Warsh’s testimony and a settling oil price would confirm the good news was real fuel, not a fade.

Bear case: Lose 7,500 while WTI keeps running and the IBM-style air-pockets spread, and the muted reaction to genuinely good news becomes the whole message: the buyers aren’t there at these levels. A firm 10-year squeezing the hyperscalers, a broadening earnings-miss tape, and the week’s gains leak toward 7,480 and the 7,420 breakout shelf as the record slips further out of reach.

Premarket Movers

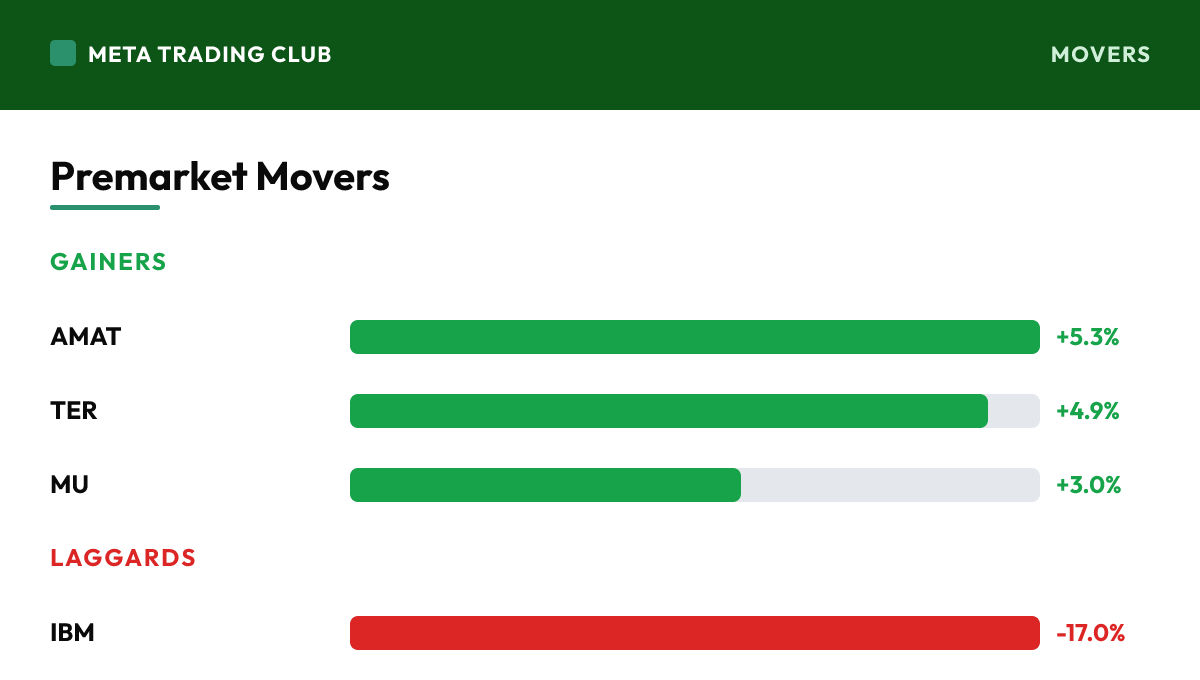

Gainers

| AMAT | Applied Materials | +5.3% | Leading the semicap bid as money rotates into equipment even while megacap AI wobbles; the sharpest large-cap tell that flows are moving within tech rather than out of it |

| TER | Teradyne | +4.9% | Riding the same semi-equipment rotation higher; the test-and-measurement names catch flows as investors reposition inside the AI-hardware complex this morning |

| MU | Micron Technology | +3.0% | Rebounding as investors eye a bottom in the memory trade after Monday’s chip-led selloff; a constructive tell that the semis corner is finding two-sided interest, not one-way selling |

Laggards

| IBM | IBM | -17.0% | The single-name air-pocket of the morning on weak preliminary Q2 numbers; a 17% gap in a Dow component is the heaviest weight on the price-weighted index and the clearest earnings warning of the session |

| MSFT | Microsoft | -3.0% | Off with the AI hyperscalers on capex and rate-path jitters; the crowded megacap growth trade gives back as investors reassess how much spending gets underwritten with the 10-year firm near 4.58% |

| ORCL | Oracle | -3.0% | Selling with Microsoft as the hyperscaler capex story wobbles; the megacap AI names are the soft spot in an otherwise two-sided tech tape this morning |

Risks Into the Open

- Primary risk: the market won’t rally on good news. A cool CPI and a Goldman blowout should lift the tape — and futures are soft. When genuinely bullish catalysts can’t move price, it usually means they were priced already or a competing weight is winning. Watch whether 7,500 holds; a failure on good news is the strongest bear tell there is.

- Secondary risk: oil keeps the ceiling on. WTI +2% on the Hormuz blockade is holding the 10-year firm near 4.58% even after a cool CPI, which squeezes the hyperscalers and caps the growth trade. If crude keeps climbing on headlines, the inflation relief gets neutralized and the pressure on the highs builds into the rest of the week.

- Constructive: the rotation is healthy, not a liquidation. Financials lead on real earnings, semis equipment and Micron are bid, and the selling is concentrated in single names (IBM) and the crowded megacap trade — not broad-based. As long as 7,500 holds and breadth stays two-sided, this reads as churn inside an uptrend, not a top.

Frequently Asked Questions

Where are S&P 500 futures trading ahead of the open?

Ahead of Tuesday, July 14, 2026, S&P 500 futures are at 7,500 (-0.20%), with the VIX near 17.5. Good news finally showed up — and the tape barely moved. June CPI landed cool at 8:30, headline inflation cooling to 3.5% year-over-year (well under the ~3.8-3.9% the Street looked for) and falling 0.4% on the month, dragged down by a 5.7% drop in energy prices. Then Q2 bank earnings opened with a bang: Goldman blew the doors off at $20.98 a share versus $14.48 expected, and JPMorgan and Bank of America both cleared the bar. On paper, that’s the dovish-inflation-plus-solid-banks combo bulls have been waiting for. And yet futures are mixed-to-soft — Dow -0.3%, S&P -0.2%, Nasdaq-100 barely green at +0.2%. Why? Three weights. One, oil won’t quit: WTI is up ~2% to ~$79.56 as Trump reinstates a naval blockade on Iranian shipping through the Strait of Hormuz and floats a 20% vessel fee — the geopolitical premium is sticky. Two, IBM cratered ~17% on weak preliminary Q2 numbers, a single-name gut-punch that reminds everyone earnings season cuts both ways. Three, the AI hyperscalers are wobbling — Microsoft and Oracle both down ~3% on capex and rate-path jitters — even as the semicap names (Applied Materials +5.3%, Teradyne +4.9%, Monolithic Power +4.5%) and Micron (+3%) catch a bid. Cross-asset, the tone is a measured de-risk, not a panic: VIX front-month sits near 17.5 (Friday spot was 15.02), the 10-year holds 4.58%, gold slid 2.4% to ~$4,015 as the cool print took some haven urgency off, and Bitcoin eased to ~$62,600. Here’s the map. The S&P closed Monday at 7,515.34 — right on top of 7,500, the line it has defended all last week. That level is now the whole ballgame: hold 7,500 with cool inflation and bank beats as fuel, and this is a base being built for another run at Friday’s 7,575 record. Lose it, and the message is that good news wasn’t enough — and the tape leaks toward 7,480 and the 7,420 breakout shelf. Core CPI is still sticky near 2.9%, oil is still the switch, and a 17% IBM air-pocket says respect the tape. Trade the reaction at 7,500, not the headline. No alignment, no trade.

What is the biggest catalyst for the market today?

June CPI came in cool. Headline inflation slowed to 3.5% year-over-year — below the ~3.8-3.9% the Street expected — and fell 0.4% on the month, dragged down by a 5.7% drop in energy prices. That’s the dovish print bulls wanted, but core is still sticky near 2.9%, keeping the Fed from declaring victory. The market’s muted reaction is the story.

What key levels should traders watch today?

SPX 7,500 — the line that matters. The market defended it all last week and Monday closed right on it at 7,515.34. This is the level that decides whether cool CPI and bank beats build a base or whether the muted reaction wins. Hold it and dips stay buyable toward a record retest; lose it and the week’s gains leak. React to it, don’t predict it. SPX 7,575 — Friday’s record, now resistance-from-above. With futures soft, the open sits well below the record close, so the market has to earn its way back through 7,540 first before the breakout is live again. A reclaim that holds re-arms the uptrend; a rejection says the good news wasn’t enough to clear the ceiling. Oil and the 10-year — the confirmation pair. WTI +2% on the Hormuz blockade and the 10-year firm at 4.58% are what’s keeping the cool CPI from lifting the tape. Crude cooling and yields easing would let the good news finally work; both staying firm keeps the ceiling on. Watch this pair before trusting any move at 7,500 or the record.

How does Meta Trading Club approach the market open?

We qualify every setup through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

Trade with a system, not signals.

This is exactly how MTC members read the open — bias, level, reaction, confirmation, execution. If you want to learn to qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process.

Apply for the Incubator → Learn moreSources: CNBC | Yahoo Finance | Benzinga | Investing.com | TheStreet – July 14, 2026 (8:15-8:45 AM ET window). For educational purposes only. Not financial advice.