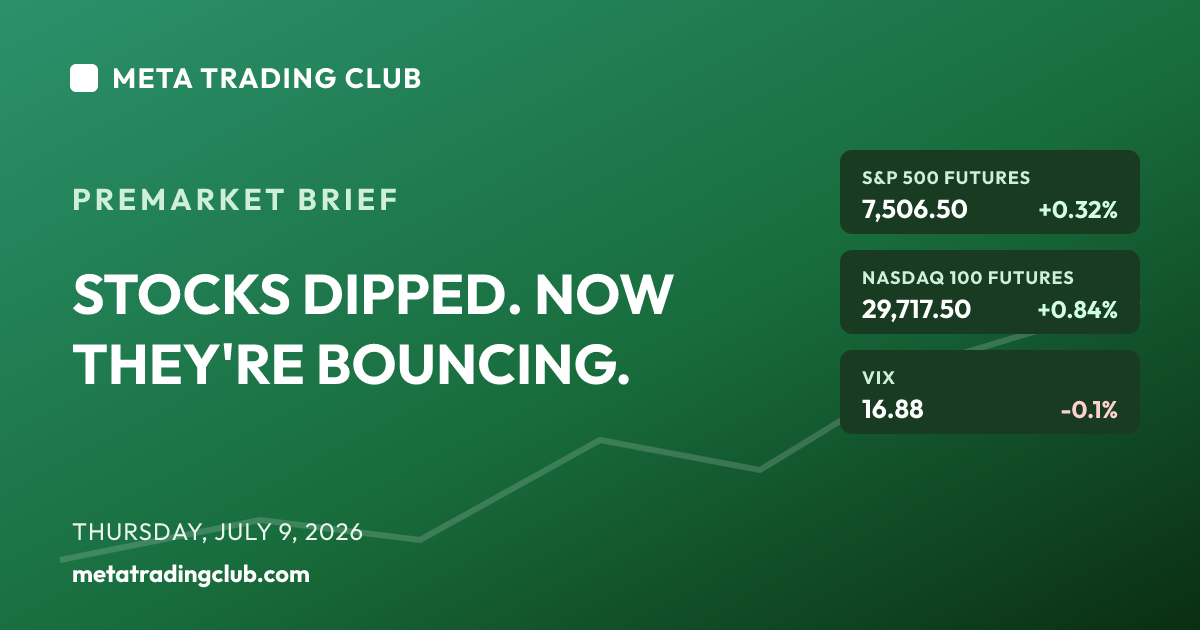

Thursday, July 9, 2026 · 8:45 AM ET · MTC Market Intelligence

Yesterday the tape blinked. Today it’s trying to bounce back — and the leadership is the tell. Wednesday, stocks sold off as the US-Iran conflict reignited: fresh US strikes on Iran overnight, Tehran targeting Gulf countries, Trump declaring the ceasefire “over” and saying he’s done negotiating. Oil ripped — Brent up more than 5% — and the 10-year yield spiked to 4.60%, its highest since May, on the inflation worry that comes with an energy shock. The S&P closed down 0.28% at 7,482.71, back under 7,500. This morning, futures are green and it’s growth leading the reclaim: Nasdaq-100 futures +0.84% at 29,717.50, S&P 500 futures +0.32% (~7,506), while Dow futures sit flat at 52,595 (-0.06%) and Russell 2000 futures +0.26% at 2,979.10. That’s a flip from earlier this week — the same chip and growth names that dragged the tape are now leading the bounce, with Marvell (MRVL) up 5.4% premarket. Cross-asset says cautious-but-calming: VIX back to 16.88 after popping above 18 intraday Wednesday, the 10-year easing slightly to 4.58%, WTI still bid at $74.49 (+1.3%), gold firm at $4,115, Bitcoin up 1.2% to $62,972. The macro read stays higher-for-longer: Wednesday’s June Fed minutes showed policymakers openly divided on rate cuts, and with oil back on the boil, that tone gets harder to soften. Today’s data is lighter — weekly jobless claims and existing home sales — and PepsiCo already reported a slight miss ($2.20 vs $2.21) with sales up 6.4%. The read: this is a reclaim attempt, and 7,500 is the line that decides if it’s real. Records don’t die on the first oil headline — they get tested, then they either reclaim the level or they don’t. If futures push SPX back above 7,500 and hold it with tech leading, buyers are stepping back into the record structure. If 7,500 rejects and oil keeps climbing, Wednesday’s dip becomes the start of something. No alignment, no trade.

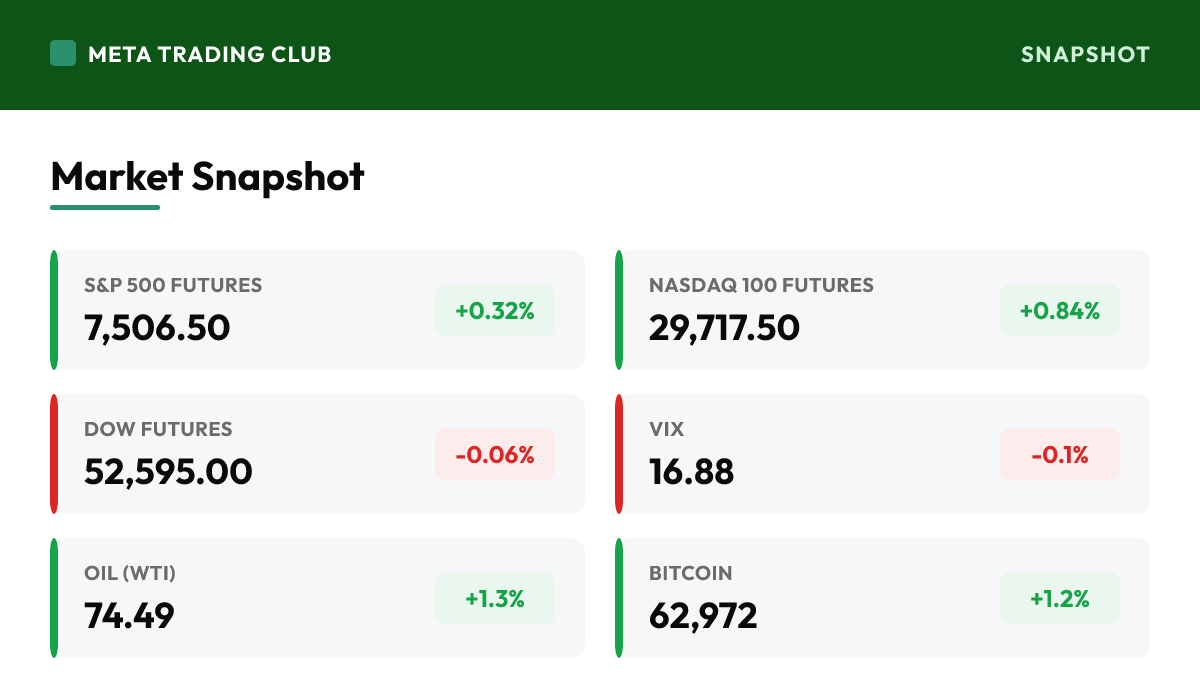

Market Snapshot

| Instrument | Level | Change | Note |

|---|---|---|---|

| S&P 500 Futures | 7,506.50 | +0.32% | Reclaiming the 7,500 line after Wednesday’s 7,482.71 close pushed the index back under it; a modest green print that says the tape is trying to absorb the oil shock rather than extend the drop. The whole session hinges on whether 7,500 holds as support again |

| Nasdaq 100 Futures | 29,717.50 | +0.84% | The leader this morning — a full flip from earlier this week when chips were the drag; growth stepping out front on a bounce day says the market is choosing to look past the Iran headline and the memory names are trying to stabilize with Marvell up 5.4% |

| Dow Futures | 52,595.00 | -0.06% | Flat and lagging the bounce — the mirror image of yesterday’s tape when blue chips did the cushioning; today value takes a back seat while growth leads, a normal rotation on a risk-on reclaim attempt |

| Russell 2000 Futures | 2,979.10 | +0.26% | Small caps modestly green, in line with the majors — no outsized divergence, which says this isn’t a broad risk-on stampede yet, just a measured attempt to steady after the dip. With the 10-year near 4.58%, the rate-sensitive corner still has a ceiling |

| VIX | 16.88 | -0.1% | Back in the high-16s after popping above 18 intraday Wednesday on the Iran strikes; the fear spike is already fading, which supports the reclaim. A push back toward 18-20 would say the war premium is biting again |

| 10-Yr Yield | 4.58% | — | Easing just off Wednesday’s 4.60% high — the highest since May — but still elevated as the oil spike keeps inflation worry alive; this is the leash on the bounce. Higher yields cap the same growth names trying to lead the reclaim |

| Oil (WTI) | 74.49 | +1.3% | Still bid at $74.49 after Wednesday’s surge on the Iran escalation and Trump calling the ceasefire over; the supply-shock premium is intact and this is the number that decides whether the inflation worry keeps pressing yields |

| Bitcoin | 62,972 | +1.2% | Up with the risk-on tone, leaning with the growth complex rather than acting as a safe haven; crypto is riding the bounce this morning, a passenger on the reclaim, not a driver |

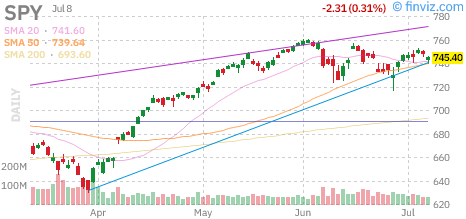

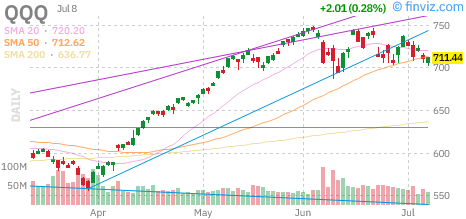

Charts to Watch

Daily candle charts with moving averages for the index proxies and today’s standout mover. Source: Finviz.

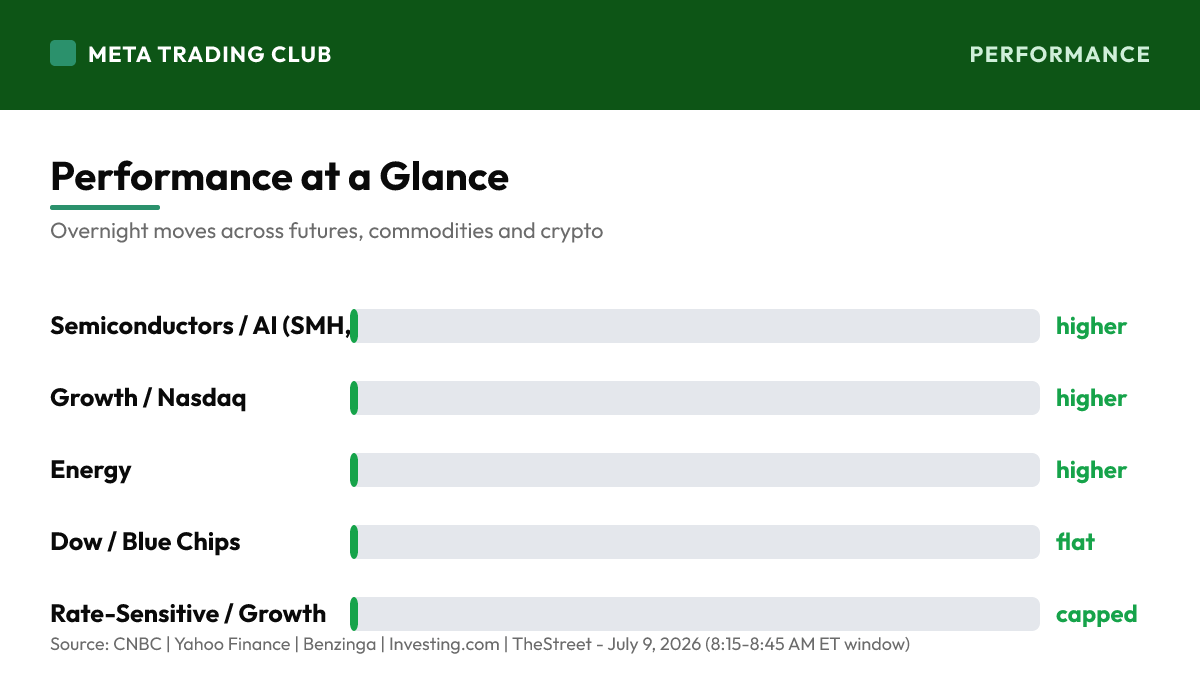

Performance at a Glance

Overnight & Global Markets

Read the leadership, because the leadership is the story. Wednesday the tape sold off on a real catalyst — the US-Iran conflict reignited, oil ripped, and the 10-year spiked to 4.60% — and the S&P closed back under 7,500 at 7,482.71. This morning futures are green, and the important part is who’s leading: growth. Nasdaq-100 futures are up 0.84% while the Dow sits flat, a complete flip from earlier this week when chips were the anchor and blue chips did the cushioning. Marvell is up 5.4% premarket, memory and AI-hardware names are trying to steady, and that rotation back into growth on a bounce day tells you the market is choosing to look past the Iran headline for now. On the geopolitics: the US struck Iran again overnight after attacks near the Strait of Hormuz, Tehran is targeting Gulf countries, and Trump declared the ceasefire over and said he’s no longer negotiating. Brent jumped more than 5% Wednesday and WTI is still bid at $74.49 — the supply-shock premium is real and it’s not going away today. On rates: the oil move pushed the 10-year to a multi-week high near 4.58-4.60%, and Wednesday’s June Fed minutes showed policymakers openly divided on cuts, reinforcing a higher-for-longer read. So the setup is clean: a market that dipped on an oil-and-yield shock is trying to reclaim 7,500 with tech in front, while oil and the 10-year sit as the leash that can pull it back. Cross-asset is cooperating with the bounce — VIX back to 16.88 after touching 18 Wednesday, gold firm, Bitcoin up. The one thing to respect: this is a reclaim attempt, not a confirmed reversal. The market has to take back 7,500 and hold it. Let it prove the level before you trust the bounce — and let it reject 7,500 before you trust the fade.

MAJOR HEADLINES AND CATALYSTS

Top Premarket Stories

- The market is trying to bounce back from Wednesday’s dip, and tech is leading it. S&P futures are up 0.32% and Nasdaq-100 futures up 0.84% after the S&P closed down 0.28% at 7,482.71, back under 7,500. Growth out front on the reclaim — Marvell +5.4% premarket — is the tell: the same names that dragged the tape are now trying to steady it. Watch whether SPX takes back 7,500 and holds.

- The US-Iran conflict is still the wildcard. American forces struck Iran again overnight after attacks near the Strait of Hormuz, Tehran is targeting Gulf countries, and Trump declared the ceasefire over and said he’s done negotiating. Brent jumped more than 5% Wednesday and WTI is still bid at $74.49. The supply-shock premium is real — it’s why yields are elevated and why this bounce has a leash.

- Yields are the pressure point. The oil move pushed the 10-year to 4.60% Wednesday — the highest since May — before easing to 4.58% this morning. That’s the level that caps the growth-led bounce: higher yields hit the same long-duration names trying to lead the reclaim. If oil cools and the 10-year settles, tech gets room; if crude climbs and yields push higher, the bounce runs into a wall.

- The Fed backdrop turned less friendly. Wednesday’s June meeting minutes showed policymakers openly divided on the path for rates, reinforcing a higher-for-longer read — and with oil reigniting inflation worry, that hawkish tilt gets harder to walk back. The rate market is the macro tell all session: watch the 10-year alongside every move in crude.

Stock-Specific

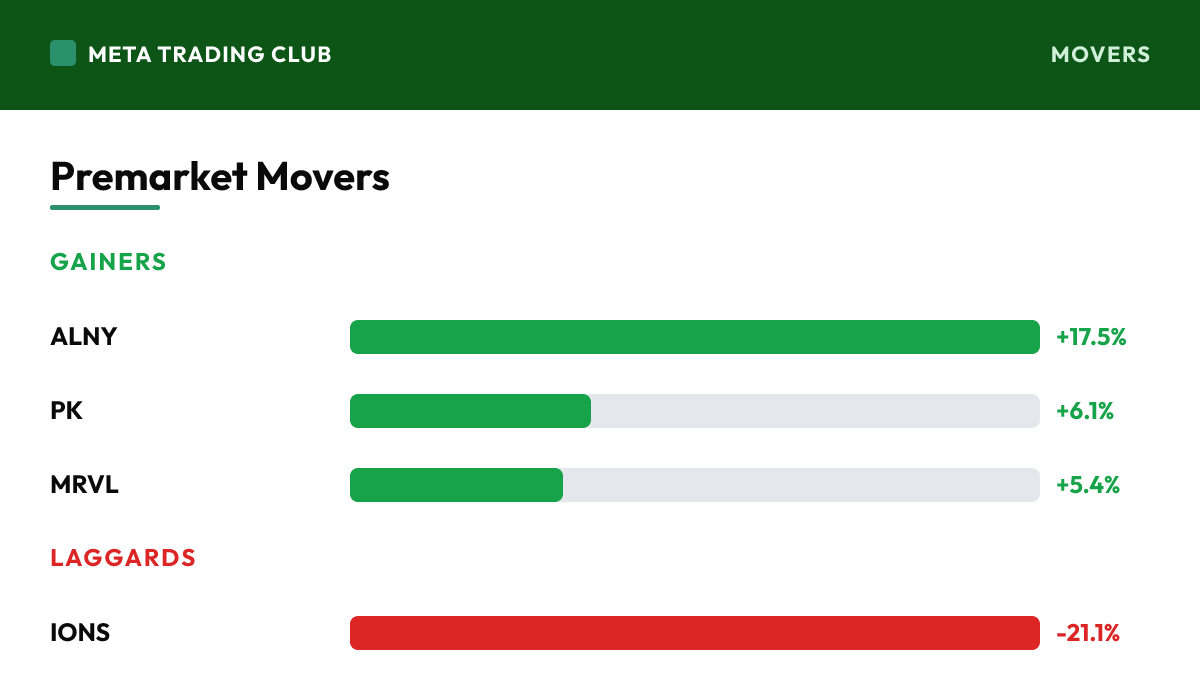

- Alnylam (ALNY) is the premarket standout, up 17.5% on positive clinical/pipeline news, while Marvell (MRVL) is up 5.4% as chips try to bounce and Park Hotels (PK) gains 6.1%. On a growth-led reclaim day, the leaders are biotech and semis — capital rotating back toward risk after Wednesday’s defensive session. Trade the leaders, but respect that a bounce isn’t a confirmed trend yet.

- Ionis (IONS) is the morning’s worst — down 21.1% after it and partner AstraZeneca said a Phase 3 heart-disease study failed to hit its primary goal; a clean binary event, not a tape signal. Levi Strauss (LEVI) is off ~6% despite beating on earnings, punished for narrow forward guidance. The lesson stands: a beat isn’t enough when the guide disappoints — the tape trades the outlook, not the print.

Global and Macro

- Today’s data is lighter than the headlines. Weekly jobless claims (prior 215K) and existing home sales are the scheduled releases — neither is likely to override the Iran story or the oil tape. In a session driven by geopolitics and rates, the economic calendar is background; the crude and bond markets are the read that matters.

- PepsiCo (PEP) opened Q2 earnings season with a slight miss — EPS $2.20 versus $2.21 expected — though net sales rose 6.4% to $24.18 billion and organic revenue grew 2.4%. A steady-not-spectacular print. Delta reports Friday and the big banks kick off next week, so the earnings tape stays light today and the session belongs to oil, yields, and the 7,500 reclaim.

TECHNICAL ANALYSIS

S&P 500 Key Levels

- SPX closed 7,482.71 Wednesday, back under the 7,500 line, and futures sit near 7,506 trying to reclaim it. That round number is the whole session: take it back and hold it and the bounce has structure; reject it and Wednesday’s dip gets a second leg. The reclaim only counts if it holds — a poke above 7,500 that fails intraday is a trap, not a signal. Let the level prove itself.

- Resistance: 7,540 (the recent futures shelf), then the 7,575-7,600 record zone overhead. Support: 7,480 (Wednesday’s close and the line futures are climbing off), then 7,460, then 7,420 (the breakout shelf and risk anchor). Two closes back under 7,420 would flip the read from dip-buy to distribution — until then, the uptrend structure is still intact.

- Bias: constructive but unconfirmed. The bounce is led by growth, VIX is fading off Wednesday’s spike, and futures are reclaiming 7,500 — that’s the makings of a dip-buy. But oil at $74.49 and the 10-year at 4.58% are the leash. Trade the reaction at 7,500, anchor risk at 7,480, and don’t trust the bounce until the level holds and yields cooperate.

Sector and Sentiment

- The leadership rotation is the constructive tell. Chips and growth led the drop earlier this week and are now leading the bounce — Marvell +5.4%, Nasdaq-100 futures +0.84% versus a flat Dow. When the group that dragged the tape starts leading it higher, that’s early evidence the pullback is being bought, not the start of a bigger unwind. Watch whether the semis hold their gains into the cash open.

- VIX at 16.88, back down after touching 18 intraday Wednesday, says the fear spike was a reaction, not a regime change. The options market is pricing the Iran headline as a shock to absorb, not a crisis to hedge. A push back toward 18-20 on new escalation would flip that read — but for now, falling vol supports the reclaim.

- The 10-year at 4.58% is the ceiling on the whole move. The oil spike lifted yields to a multi-week high, and higher rates cap the exact growth names trying to lead this bounce. If crude cools and yields settle, tech gets room to run the reclaim; if oil climbs and the 10-year breaks above 4.60%, the rate pressure and the war premium start reinforcing each other again.

TODAY’S ECONOMIC CALENDAR

Key Releases (ET)

- The scheduled data is light: weekly jobless claims (prior 215K) at 8:30 AM and existing home sales later in the morning. Neither is a tape-mover in a session dominated by the Iran story and the oil tape. Note the numbers, but the read today comes from crude and the 10-year, not the economic prints.

- The 10-year near 4.58% is the number to watch all session. It’s the swing factor: a move back down as oil cools relieves the growth-led bounce, while a push above Wednesday’s 4.60% high compounds the pressure on long-duration tech. In a headline-driven tape, the rate market is the macro read that decides whether the reclaim holds.

- Earnings season is opening slowly: PepsiCo already reported a slight miss this morning, Delta lands Friday, and the big banks kick off next week. Today’s US earnings calendar has no tape-mover after PEP, so the session belongs to the Iran headlines, the oil premium, and the 7,500 reclaim attempt.

Earnings Today

- PepsiCo (PEP) opened the Q2 season with a steady-not-spectacular print — EPS $2.20 versus $2.21 expected, net sales up 6.4% to $24.18 billion, organic revenue up 2.4%. A slight headline miss on solid top-line growth; not a tape-mover for the broad market, but a fair first read on consumer-staples demand. The real earnings weight comes Friday with Delta and next week with the banks.

- The standing lesson from this week’s tape: Levi’s beat on earnings and still fell ~6% on narrow guidance. When a company clears the bar and the stock drops, the market is telling you the good news was already priced and the forward guide is what matters. Respect what the tape does with the print, not just the print itself.

PREMARKET PLAYBOOK

Key Levels

- SPX 7,500 — the reclaim line and today’s whole story. Futures sit near 7,506, so the open question is whether the round number flips back to support after Wednesday’s close pushed the index under it. Hold above it and the growth-led bounce has structure; reject it and Wednesday’s dip gets a second leg. A poke above that fails intraday is a trap — let it hold before committing.

- SPX 7,420 — the prior breakout shelf and the risk anchor. As long as 7,420 holds, this is a pullback inside an uptrend and dips stay buyable. Two closes under it flip the read from dip-buy to distribution and open the door toward 7,400 and below.

- WTI and the 10-year — the confirmation pair for the bounce. If oil cools and yields settle back off 4.60%, the pressure on growth lifts and 7,500 reclaims easily. If crude keeps climbing and the 10-year breaks higher, the inflation-and-war combination presses the tape and the reclaim fails. Watch this pair before trusting any long.

Bull case: The dip gets bought. SPX reclaims 7,500 and holds it, tech keeps leading with the chip complex stabilizing (Marvell, memory), and oil’s spike fades as the initial Iran fear cools. The 10-year eases back off 4.60%, VIX drifts toward 15, and Wednesday’s selloff proves to be a one-day shock absorbed inside the uptrend. A market that reclaims a broken level with growth in front is showing the pullback was a buying opportunity, not a top.

Bear case: The bounce fails at 7,500. Oil keeps climbing as the Iran conflict escalates, the 10-year breaks above 4.60% on the inflation scare, and the growth-led reclaim rejects the round number. Chips roll back over, SPX loses 7,480 then 7,420, and VIX pushes back above 18. What looked like a dip-buy becomes a second leg down as the war premium and the rate pressure overwhelm the bounce.

What We’re Watching

- The 7,500 reclaim — futures are just above it and the whole session hinges on whether it flips back to support. This one level decides whether today is a dip-buy or a failed bounce. Let it prove itself as support before trusting any long.

- Chip and growth leadership — Marvell and the Nasdaq are leading the bounce. If the semis hold their premarket gains into the cash open, the reclaim has legs; if they fade, the leadership is hollow. Watch the group that’s supposed to be driving the move.

- Oil and the 10-year together — the macro leash. Crude cooling and yields settling clears the runway for the bounce; both climbing caps it and pressures growth. In a headline-driven session, this pair is the read that matters all morning.

Premarket Movers

Gainers

| ALNY | Alnylam Pharmaceuticals | +17.5% | The premarket standout, up 17.5% on positive pipeline/clinical news; a story-driven biotech run that ignores the macro tape — size it for the volatility it carries |

| PK | Park Hotels & Resorts | +6.1% | Up 6.1% premarket, a rare non-tech leader on a growth-led bounce day; single-name strength in the REIT/travel corner as risk appetite steadies |

| MRVL | Marvell Technology | +5.4% | Up 5.4% as chips try to lead the bounce back; the semi complex stabilizing after dragging the tape earlier in the week is the constructive tell of the morning |

Laggards

| IONS | Ionis Pharmaceuticals | -21.1% | Tumbled 21.1% after it and partner AstraZeneca said a Phase 3 heart-disease study failed its primary goal; a clean binary drug-trial event, not a read on the broad tape |

| LEVI | Levi Strauss | -6.1% | Off ~6% despite beating on earnings, punished for narrow forward guidance; the classic ‘good print, cautious guide’ reaction — the tape trades the outlook, not the beat |

| PEP | PepsiCo | -0.1% | Roughly flat after a slight Q2 miss ($2.20 vs $2.21) with net sales up 6.4%; a steady staples print that neither moved the stock much nor the broad market |

Risks Into the Open

- Primary risk: the oil shock deepens. The Iran escalation put a war premium back into crude, and if the conflict widens or Strait of Hormuz supply is genuinely threatened, the inflation channel hits yields and stocks together — and caps the growth-led bounce. Watch WTI: a run further above $74.49 turns a headline into a macro problem the reclaim can’t survive.

- Secondary risk: yields break higher. The 10-year at 4.58% is just off Wednesday’s 4.60% multi-week high, and a divided Fed plus hot oil could push it above that. Higher rates hit the exact long-duration names trying to lead the bounce, so a rate break would pull the rug on the reclaim. The bond market is the swing factor all session.

- Constructive: the bounce is led by the right group. Growth and chips — the drag earlier this week — are out front on the reclaim, VIX is fading off its Wednesday spike, and futures are back above 7,500. As long as SPX holds the reclaim with tech leading, this reads as a dip being bought inside an uptrend, not the start of a bigger unwind.

Frequently Asked Questions

Where are S&P 500 futures trading ahead of the open?

Ahead of Thursday, July 9, 2026, S&P 500 futures are at 7,506.50 (+0.32%), with the VIX near 16.88. Yesterday the tape blinked. Today it’s trying to bounce back — and the leadership is the tell. Wednesday, stocks sold off as the US-Iran conflict reignited: fresh US strikes on Iran overnight, Tehran targeting Gulf countries, Trump declaring the ceasefire “over” and saying he’s done negotiating. Oil ripped — Brent up more than 5% — and the 10-year yield spiked to 4.60%, its highest since May, on the inflation worry that comes with an energy shock. The S&P closed down 0.28% at 7,482.71, back under 7,500. This morning, futures are green and it’s growth leading the reclaim: Nasdaq-100 futures +0.84% at 29,717.50, S&P 500 futures +0.32% (~7,506), while Dow futures sit flat at 52,595 (-0.06%) and Russell 2000 futures +0.26% at 2,979.10. That’s a flip from earlier this week — the same chip and growth names that dragged the tape are now leading the bounce, with Marvell (MRVL) up 5.4% premarket. Cross-asset says cautious-but-calming: VIX back to 16.88 after popping above 18 intraday Wednesday, the 10-year easing slightly to 4.58%, WTI still bid at $74.49 (+1.3%), gold firm at $4,115, Bitcoin up 1.2% to $62,972. The macro read stays higher-for-longer: Wednesday’s June Fed minutes showed policymakers openly divided on rate cuts, and with oil back on the boil, that tone gets harder to soften. Today’s data is lighter — weekly jobless claims and existing home sales — and PepsiCo already reported a slight miss ($2.20 vs $2.21) with sales up 6.4%. The read: this is a reclaim attempt, and 7,500 is the line that decides if it’s real. Records don’t die on the first oil headline — they get tested, then they either reclaim the level or they don’t. If futures push SPX back above 7,500 and hold it with tech leading, buyers are stepping back into the record structure. If 7,500 rejects and oil keeps climbing, Wednesday’s dip becomes the start of something. No alignment, no trade.

What is the biggest catalyst for the market today?

The market is trying to bounce back from Wednesday’s dip, and tech is leading it. S&P futures are up 0.32% and Nasdaq-100 futures up 0.84% after the S&P closed down 0.28% at 7,482.71, back under 7,500. Growth out front on the reclaim — Marvell +5.4% premarket — is the tell: the same names that dragged the tape are now trying to steady it. Watch whether SPX takes back 7,500 and holds.

What key levels should traders watch today?

SPX 7,500 — the reclaim line and today’s whole story. Futures sit near 7,506, so the open question is whether the round number flips back to support after Wednesday’s close pushed the index under it. Hold above it and the growth-led bounce has structure; reject it and Wednesday’s dip gets a second leg. A poke above that fails intraday is a trap — let it hold before committing. SPX 7,420 — the prior breakout shelf and the risk anchor. As long as 7,420 holds, this is a pullback inside an uptrend and dips stay buyable. Two closes under it flip the read from dip-buy to distribution and open the door toward 7,400 and below. WTI and the 10-year — the confirmation pair for the bounce. If oil cools and yields settle back off 4.60%, the pressure on growth lifts and 7,500 reclaims easily. If crude keeps climbing and the 10-year breaks higher, the inflation-and-war combination presses the tape and the reclaim fails. Watch this pair before trusting any long.

How does Meta Trading Club approach the market open?

We qualify every setup through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

Trade with a system, not signals.

This is exactly how MTC members read the open — bias, level, reaction, confirmation, execution. If you want to learn to qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process.

Apply for the Incubator → Learn moreSources: CNBC | Yahoo Finance | Benzinga | Investing.com | TheStreet – July 9, 2026 (8:15-8:45 AM ET window). For educational purposes only. Not financial advice.