Monday, July 6, 2026 · 4:30 PM ET · MTC Market Close

The first session back from the long weekend belonged to one group and one group only: the chips. Broadcom jumped 3.7% after agreeing to extend its custom-silicon deal with Apple through 2031, the semiconductor index (SOX) added 2.2% after two straight losing sessions, and the money chased AI hardware straight up — AMD +6.6% to 552.05, Astera Labs +10.7% to about 450 on a street-high Bank of America target, with Apple itself up 1.3%. That pulled the Nasdaq up 1.12% to 26,121.16 and the S&P 500 up 0.72% to 7,537.43 — reclaiming and holding above 7,500 for the first time after two sessions pinned beneath it. The Dow rose 0.29% to a record 53,055.91, briefly tapping 53,000 for the first time ever before fading off the highs. On the surface, records across the board. Underneath, the tape told a different story: declining stocks outnumbered advancers within the S&P by 1.3 to 1 even as the index rose, and volume was light — 16.8 billion shares versus a 23.4 billion 20-day average. This was a narrow, thin, chip-only rally. As one desk put it, a market that’s ‘leaving a lot of people out.’ The macro was quiet — ISM Services PMI came in at 54.0, matching expectations, with the employment sub-index back in expansion at 51.2. Microsoft fell nearly 1% after announcing it would cut roughly 4,800 jobs (2.1% of staff), and O’Reilly Automotive dropped 6.7% after Bloomberg reported a cash offer for Genuine Parts. Gold closed up 1.18% at 4,174.40, the VIX slipped to 15.57, and WTI eased toward $68 after OPEC+ agreed to a fifth straight monthly output hike. Tomorrow the calendar gets busy: SpaceX officially joins the Nasdaq-100 before the open — triggering an estimated $27 billion in passive buying — and Samsung reports preliminary Q2 results. FOMC minutes land Wednesday, and Delta and PepsiCo kick off earnings season later this week. Traders now price roughly 25% odds of a hike at the July 29 Fed meeting. The read is simple: the index says all-time highs, but breadth and volume didn’t confirm it. When price and its two witnesses disagree, you wait. No alignment, no trade.

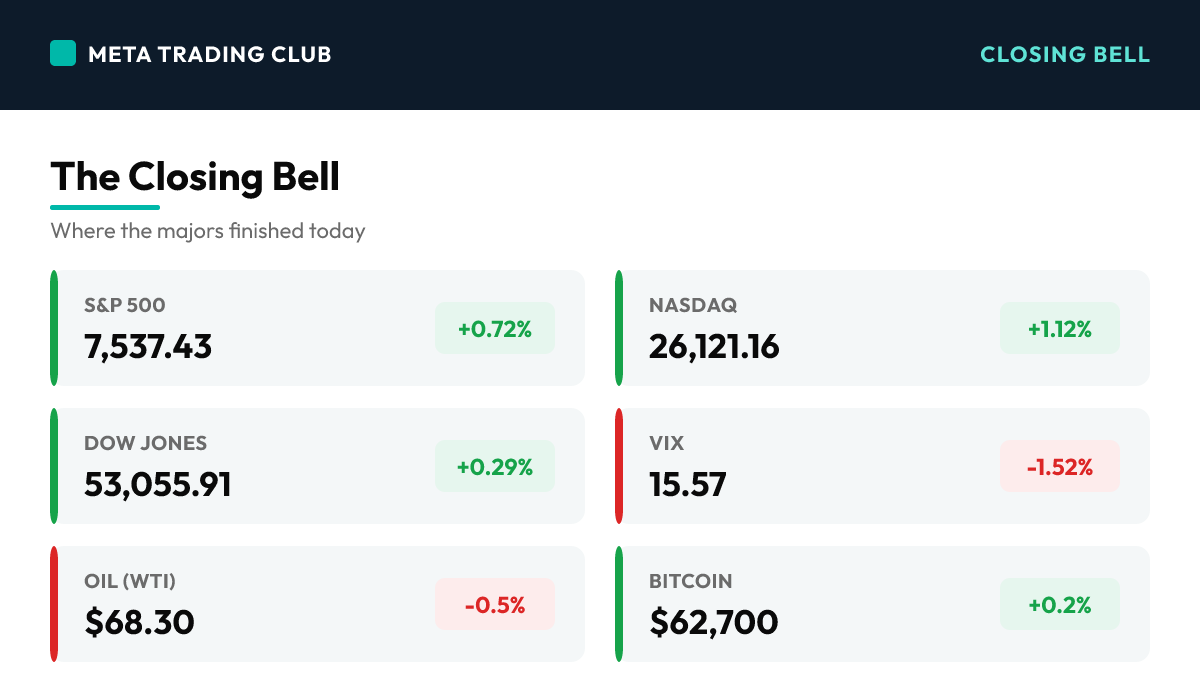

The Closing Bell

| Instrument | Close | Change | Note |

|---|---|---|---|

| S&P 500 | 7,537.43 | +0.72% | Rose 54 points to reclaim and hold above 7,500 for the first time after two sessions pinned beneath it — but decliners beat advancers 1.3-to-1 inside the index |

| Nasdaq | 26,121.16 | +1.12% | Led the tape, up 288 points as the semiconductor complex roared back — Broadcom +3.7% on the Apple deal, AMD +6.6%, Astera Labs +10.7% |

| Dow Jones | 53,055.91 | +0.29% | Rose 156 points to a record close, briefly tapping 53,000 for the first time ever before fading off the highs as chips did the heavy lifting elsewhere |

| Russell 2000 | 3,009.54 | +0.45% | Small caps ticked back above 3,000 but lagged the chip-driven megacaps — a modest gain that didn’t share the tech leadership |

| VIX | 15.57 | -1.52% | Slipped to the mid-15s as the holiday-week calm held; a low fear gauge alongside a narrow rally reads as complacency, not conviction |

| 10-Yr Yield | 4.49% | flat | Little changed near 4.5% as ISM Services matched expectations; FedWatch puts ~25% odds on a hike at the July 29 meeting, with FOMC minutes due Wednesday |

| Gold | $4,174.40 | +1.18% | Rose 49 dollars to extend its rebound above $4,100 as the soft-rate backdrop and a quiet dollar kept the metal bid into the new week |

| Oil (WTI) | $68.30 | -0.5% | Eased toward $68 after OPEC+ agreed to raise output for a fifth straight month — seven members adding a combined 188,000 bpd in August |

| Bitcoin | $62,700 | +0.2% | Extended its weekend rally to hold above $62,000, steady alongside gold as the risk-on chip bid carried through the crypto tape |

Today’s Charts

Daily candlestick charts with 20/50/200-day moving averages — the index majors, the day’s biggest mover on each side, and the leading sector ETF.

Charts: Finviz (daily). Levels and overlays update through the next session.

Sector Scoreboard

What Drove The Day

The first cash session after the July 4 break had exactly one engine, and it was the semiconductors. Broadcom set the tone premarket by agreeing to extend its custom-chip partnership with Apple through 2031, and the stock closed up 3.7% while Apple added 1.3%. From there the AI-hardware bid did the rest: the Philadelphia Semiconductor Index (SOX) rose 2.2% after two straight down sessions, AMD surged 6.6% to 552.05, and Astera Labs jumped 10.7% to roughly 450 after Bank of America lifted its target to a street-high 450 on AI-infrastructure confidence. The S&P 500 information technology sector climbed 1.3% and effectively carried the whole index. The Nasdaq led at +1.12% to 26,121.16, the S&P 500 rose 0.72% to 7,537.43 — reclaiming 7,500 and holding above it for the first time after being pinned beneath the round number for two sessions — and the Dow rose 0.29% to a record 53,055.91, briefly touching 53,000 for the first time before drifting off the high. But the internals refused to confirm the headline. Declining stocks outnumbered advancing ones within the S&P 500 by about 1.3 to 1 even as the index closed green, and volume was thin at 16.8 billion shares against a 23.4 billion 20-day average — the holiday hangover meets a rally concentrated in a handful of names. ‘This is a market that’s leaving a lot of people out,’ said Jake Dollarhide of Longbow Asset Management. ‘If you’re not in certain tech names, if you’re not in semiconductors, then you’re basically missing the entire rally.’ The macro stayed in the background: ISM Services PMI printed 54.0, matching expectations, with the employment sub-index back in expansion at 51.2. The day’s soft spots came from single names — Microsoft slipped nearly 1% after saying it would cut about 4,800 jobs, roughly 2.1% of its workforce, with desks reading the layoffs as a signal it can’t fund its AI capex and show a return at the same time; O’Reilly Automotive fell 6.7% after Bloomberg reported a cash offer to buy Genuine Parts, which dropped about 3%; and Solstice Advanced Materials sank 12.2% after agreeing to acquire Element Solutions for $14.5 billion. SpaceX dipped 1% on heavy volume ahead of its Nasdaq-100 inclusion tomorrow. Cross-asset, gold closed up 1.18% at 4,174.40, the VIX eased to 15.57, WTI slipped toward $68 after OPEC+ approved a fifth straight monthly supply increase, and Bitcoin held above $62,000. Traders now see roughly a 25% chance of a 25-basis-point hike at the July 29 Fed meeting, and the FOMC minutes Wednesday will show how seriously the committee weighed that path. The setup into tomorrow is loud: SpaceX joins the Nasdaq-100 before the open with an estimated $27 billion of passive buying, Samsung reports preliminary Q2 results, and earnings season opens later in the week with Delta and PepsiCo. The lesson of the day is an old one dressed up in record highs: when the index prints a new high but breadth and volume don’t come along, the move isn’t confirmed. No alignment, no trade.

MAJOR HEADLINES AND CATALYSTS

Top Market-Moving Stories

- CHIPS ROAR BACK — BROADCOM EXTENDS APPLE DEAL THROUGH 2031 (Day) — Broadcom jumped 3.7% after agreeing to extend its custom-silicon partnership with Apple through 2031, and the whole AI-hardware complex followed: SOX +2.2% after two down sessions, AMD +6.6%, Astera Labs +10.7% on a street-high BofA target. The IT sector’s 1.3% gain carried the S&P and Nasdaq.

- S&P RECLAIMS 7,500, DOW PRINTS A RECORD — BUT BREADTH DIDN’T CONFIRM (Day) — The S&P rose 0.72% to 7,537.43 to hold above 7,500 for the first time in three sessions and the Dow closed at a record 53,055.91, yet declining stocks beat advancers 1.3-to-1 and volume was light at 16.8B vs a 23.4B average. Records on the screen, weakness underneath.

- MICROSOFT CUTS 4,800 JOBS, O’REILLY BIDS FOR GENUINE PARTS (Day) — Microsoft fell nearly 1% after announcing it would cut about 2.1% of its workforce, with desks reading it as a capex-versus-returns signal. O’Reilly dropped 6.7% on a reported cash offer for Genuine Parts (-3%), and Solstice sank 12.2% on a $14.5B deal for Element Solutions.

Fed and Macro Context

- ISM Services PMI printed 54.0 for June, matching expectations, with the employment sub-index climbing back into expansion at 51.2 — a steady-but-unremarkable read that kept the 10-year near 4.5% and left the rate picture unchanged into the FOMC minutes.

- Following last week’s soft jobs report, traders now price roughly a 25% chance of a 25-basis-point hike at the July 29 meeting, per CME FedWatch. Fed Governor Christopher Waller said forward guidance can be a ‘valuable tool’ but problematic when used inflexibly; the June meeting minutes are due Wednesday.

- Cross-asset stayed calm and risk-on: gold +1.18% to 4,174.40, VIX down to 15.57, Bitcoin holding above $62,000, and WTI easing toward $68 after OPEC+ approved a fifth straight monthly output increase of 188,000 bpd for August.

Single-Stock Standouts

- The AI-hardware bid was broad within its lane — AMD +6.6% to 552.05, Astera Labs +10.7% to about 450 on a street-high BofA target, Broadcom +3.7% on the Apple deal, and Apple +1.3% — while Micron and other memory names firmed after last week’s unwind.

- SpaceX dipped about 1% on heavy volume, most of it in the closing seconds, ahead of its Nasdaq-100 inclusion tomorrow that is expected to force roughly $27 billion of passive buying (about $4.3B from QQQ alone).

- GrabAGun (PEW) spiked 23% on strong digital sales, while Honeywell spinoff Solstice fell 12.2% on its Element Solutions acquisition — the day’s clearest reminder that acquirers usually pay for the deal on announcement day.

AFTER-HOURS EARNINGS SPOTLIGHT

Tonight’s Slate

- A light post-close slate on the first day back — no major earnings after the bell. The next catalysts arrive tomorrow with Samsung’s preliminary Q2 results and, later in the week, the unofficial start of earnings season from Delta Air Lines and PepsiCo.

- Expectations into the season are high: analysts model aggregate S&P 500 Q2 earnings growth near 24% year over year, with the tech sector projected to jump roughly 65% — the bar that today’s chip rally is pricing in advance.

NEXT SESSION SETUP

Tuesday, July 7 — SpaceX Joins the Nasdaq-100

- SpaceX officially enters the Nasdaq-100 before Tuesday’s open, triggering an estimated $27 billion of index-fund buying (about $4.3B from QQQ) into a stock with less than 10% of its shares freely floating — a mechanical bid that can distort the tape at the open.

- Samsung reports preliminary Q2 results and SK Hynix is set to debut on the Nasdaq later this week — the memory complex stays in focus after today’s chip-led rally. Watch whether the semiconductor bid broadens or stays penned in the AI-hardware leaders.

- FOMC MINUTES WEDNESDAY, JULY 8 — the first look at how seriously the committee weighed a hike before last week’s soft jobs data. With markets pricing ~25% odds for July 29, a hawkish tone in the minutes is the clearest risk to a rally already thin on breadth.

Winners & Losers

Winners

| AMD | +6.6% | Led the megacap chip bid to 552.05 as investors chased AI hardware into a strong expected Q2 tech season; the SOX gained 2.2% after two down sessions | |

| ALAB | +10.7% | Astera Labs jumped to about 450 after Bank of America lifted its target to a street-high 450 on AI-infrastructure confidence — up 170% year to date | |

| AVGO | +3.7% | Broadcom rose on agreeing to extend its custom-chip partnership with Apple through 2031 — the day’s defining catalyst that set the tone for the whole complex |

Losers

| ORLY | -6.7% | O’Reilly Automotive tumbled after Bloomberg reported it sent a cash offer to buy Genuine Parts; the target GPC fell about 3% on the report | |

| SOLS | -12.2% | Solstice Advanced Materials sank after agreeing to acquire Element Solutions for $14.5 billion — the acquirer paid for the deal on announcement day | |

| MSFT | -1.0% | Microsoft slipped after announcing it would cut about 4,800 jobs (2.1% of staff); desks read the layoffs as a capex-versus-return signal on its AI spend |

What It Sets Up For Tomorrow

Levels Into Tomorrow

- S&P 500 7,500 — THE PIVOT, NOW FROM ABOVE. After two sessions pinned beneath it, the index reclaimed 7,500 and closed at 7,537. Hold it as support Tuesday and the record chase toward the June 2 all-time high near 7,610 stays live.

- S&P 500 7,610 — the record-high zone from June 2. The index sits about 1% below it; a breadth-confirmed push through here would be the first new closing high in over a month.

- S&P 500 7,480 — losing the reclaimed 7,500 shelf and slipping back under here turns the chip rally into a failed breakout and puts the two-session pin back in control of the tape.

Bull case: The chip leadership broadens, SpaceX’s Nasdaq-100 inclusion adds a mechanical bid, and breadth finally catches up to price — the S&P holds 7,500 as support and pushes toward the June 2 record near 7,610 as earnings season opens with the projected 24% growth intact.

Bear case: The 1.3-to-1 decline breadth and light volume are the tell, not the noise — the rally stays penned in a few chip names, a hawkish tone in Wednesday’s FOMC minutes revives the July 29 hike bet, and the S&P loses the reclaimed 7,500 to fall back into its multi-session range under the round number.

What We’re Watching

- Market breadth — does the advance-decline line finally confirm the index highs, or does the rally stay narrow and chip-only? This is the single biggest question into Tuesday.

- SpaceX Nasdaq-100 inclusion at Tuesday’s open — the ~$27B mechanical bid and thin float can distort the index open; watch for a spike-and-fade.

- FOMC minutes Wednesday and the start of earnings (Delta, PepsiCo) — the macro and micro catalysts that decide whether the record tape gets confirmation or a reality check.

Risks Into Tomorrow

- Breadth divergence — The S&P and Nasdaq printed strong gains and the Dow a record, but declining stocks outnumbered advancers 1.3-to-1 and volume was light at 16.8B vs a 23.4B average. A narrow, thin rally concentrated in a few chip names is the classic setup where the index masks broad weakness.

- Concentration risk in the AI-chip trade — The entire market’s gain came from the semiconductor and AI-hardware complex — Broadcom, AMD, Astera Labs. When one lane carries the whole tape, a single disappointment in that group (or a hawkish rate surprise) can reverse the index faster than the breadth suggests.

- FOMC minutes and the July 29 hike bet — Markets price ~25% odds of a hike at the July 29 meeting after last week’s soft jobs. Wednesday’s minutes reveal how hawkish the new-Chair committee ran before that data — a hawkish read is the cleanest threat to a rally already lacking breadth confirmation.

Frequently Asked Questions

How did the S&P 500 close today?

On Monday, July 6, 2026, the S&P 500 closed at 7,537.43 (+0.72%), with the VIX at 15.57. The first session back from the long weekend belonged to one group and one group only: the chips.

What drove the market today?

CHIPS ROAR BACK — BROADCOM EXTENDS APPLE DEAL THROUGH 2031 (Day) — Broadcom jumped 3.7% after agreeing to extend its custom-silicon partnership with Apple through 2031, and the whole AI-hardware complex followed: SOX +2.2% after two down sessions, AMD +6.6%, Astera Labs +10.7% on a street-high BofA target. The IT sector’s 1.3% gain carried the S&P and Nasdaq.

What levels matter for tomorrow?

S&P 500 7,500 — THE PIVOT, NOW FROM ABOVE. After two sessions pinned beneath it, the index reclaimed 7,500 and closed at 7,537. Hold it as support Tuesday and the record chase toward the June 2 all-time high near 7,610 stays live. S&P 500 7,610 — the record-high zone from June 2. The index sits about 1% below it; a breadth-confirmed push through here would be the first new closing high in over a month. S&P 500 7,480 — losing the reclaimed 7,500 shelf and slipping back under here turns the chip rally into a failed breakout and puts the two-session pin back in control of the tape.

How does Meta Trading Club prepare for the next session?

We wrap every session and carry the read forward through the MTC Alignment Engine — bias, level, reaction, confirmation, execution, targets. No alignment, no trade. Learn the full process inside the MTC Incubator.

New to this? Start with the free training.

Learn how we read the market before you risk a dollar — our free education library and ebook break down the fundamentals step by step.

Free education → Get the free ebookThe session’s over. The prep isn’t.

This is how MTC members close each day — wrap what happened, mark the levels, and carry one clean read into tomorrow. If you want to build that habit and qualify your own A+ setups instead of chasing alerts, the MTC Incubator is mentorship and a repeatable process. It’s application-based — see if it’s a fit.

Explore the MTC Incubator → Apply nowSources: Reuters/Yahoo Finance closing data, TheStreet and Schaeffer’s market coverage, CME FedWatch, ISM — verified as of 4:30 PM ET July 6, 2026. For educational purposes only. Not financial advice.