Last Week’s report

Economic Reports

PMIs

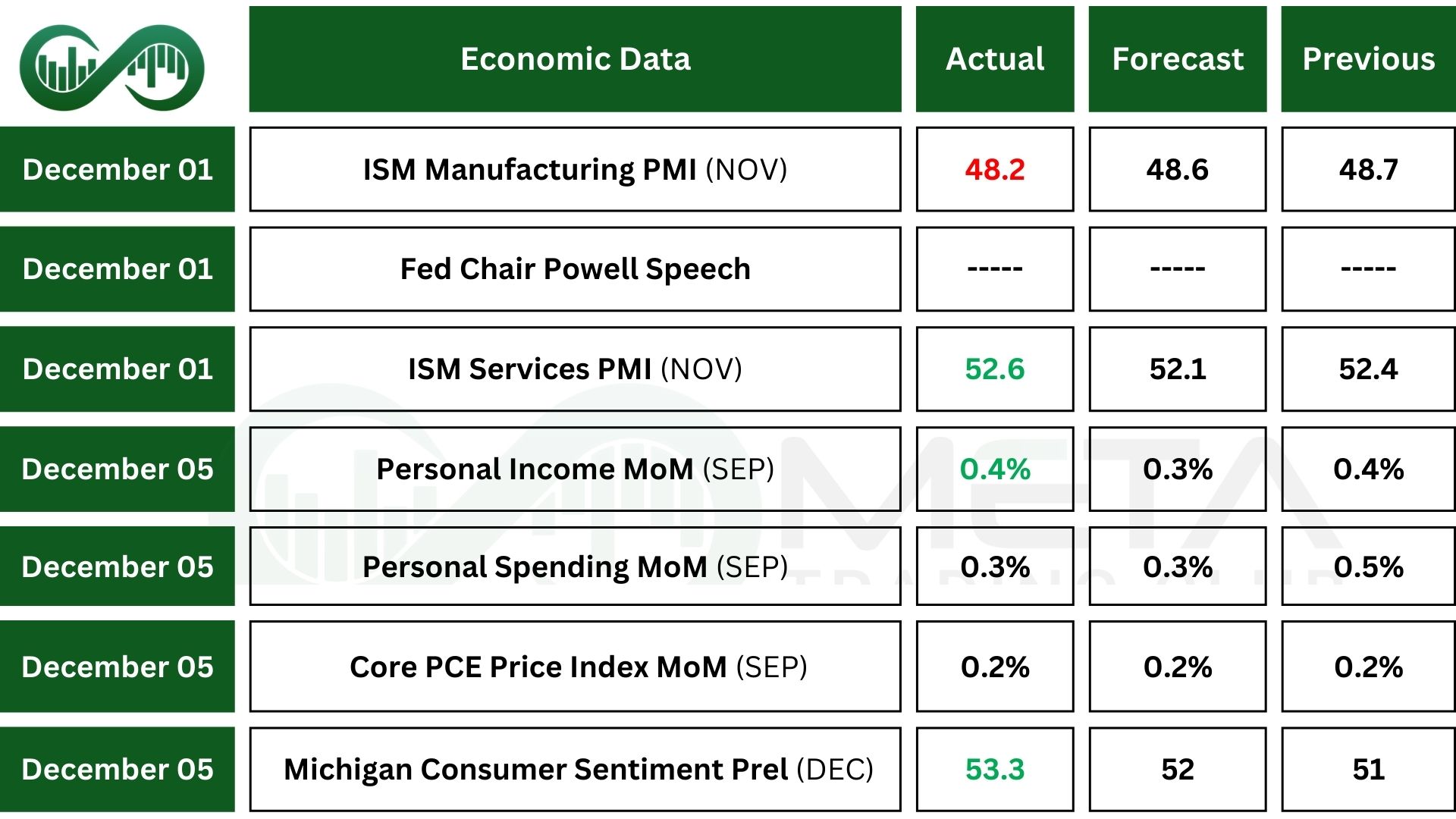

U.S. Manufacturing PMI slipped to 48.2 in November, signaling its ninth straight month of contraction and the weakest in four months. New orders, supplier deliveries, and employment fell further, while price pressures rose and backlogs shrank. Production improved slightly, but overall, more than half of the sector’s GDP remained in contraction.

This means factories are struggling, with fewer new jobs and rising costs, showing manufacturing is still under pressure.

The U.S. Services PMI rose slightly to 52.6 in November, the strongest growth in nine months and above forecasts. Business activity and backlogs improved, but employment stayed weak, and supplier delays reflected shutdown and tariff impacts. Price pressures eased to their lowest in seven months.

The services sector is showing signs of recovery, but jobs and supply chains remain under strain.

Jobs Report

In November, U.S. employers announced 71,321 job cuts, up from a year earlier, though fewer than October’s. The biggest layoffs came from telecom (mainly Verizon). Overall, job cuts this year reached 1.17 million, the highest since 2020, while hiring plans slowed to just over 9,000.

This shows companies are cutting more jobs than they are creating, signaling tougher times for workers and fewer new opportunities.

U.S. Initial Jobless Claims dropped to 191k in late November, the lowest since September 2022, marking a fourth straight weekly decline and beating expectations. Continuing claims also eased slightly, and federal employee claims fell after a brief rise during the government shutdown. Despite fewer layoffs, slower hiring keeps unemployment insurance levels higher than in past recoveries.

This shows fewer people are losing jobs, but finding new ones is still harder than before.

Inflation

The U.S. PCE Price Index rose 0.3% in September, with goods prices climbing faster while services slowed. Annual headline inflation ticked up to 2.8%, the highest since April 2024, while core inflation eased slightly to 2.8%.

U.S. Personal Income rose 0.4% in September, its fourth straight monthly gain, driven by higher wages and asset income. Disposable income grew more slowly at 0.3%, while real disposable income barely increased at 0.1%.

U.S. Personal Spending rose 0.3% in September, adding $65.1 billion, mostly from services like housing, health care, and food. Goods spending barely grew, with higher energy costs offset by declines in cars, clothing, and recreational items.

These signals a strained consumer environment: households are prioritizing necessities, leaving limited room for discretionary spending.

Consumer sentiment

U.S. Michigan Consumer Sentiment rose to 53.3 in December, the first improvement in five months and above expectations. People, especially younger consumers, felt better about personal finances, while inflation expectations eased, though labor market views stayed weak and price outlooks uncertain.

This signals confidence is slowly recovering but worries about jobs and future costs still weigh on households.

Earnings Reports

CrowdStrike

CrowdStrike (CRWD) Q3 2026 results slightly beat expectations with $1.23B in revenue (up 22% YoY) and EPS of $0.96.

The company posted record cash flow and raised its full‑year outlook, driven by strong demand for its Falcon platform, new AI‑powered products, and major partnerships with AWS, NVIDIA, and CoreWeave.

While non‑GAAP profits hit records, GAAP losses widened, creating some stock volatility even as analysts raised price targets.

Salesforce

Salesforce (CRM) delivered strong Q3 2026 results with $10.3B in revenue, up 9% year-over-year, and subscription revenue of $9.7B, up 10%.

Profitability improved with higher margins and record cash flow, while the company returned $4.2B to shareholders.

Growth was driven by rapid adoption of Agentforce and Data 360, which together reached $1.4B in ARR, alongside the completed Informatica acquisition.

Salesforce raised its full-year guidance to $41.45–$41.55B, signaling confidence in continued momentum. Investor sentiment was positive, lifting CRM shares after earnings released.

Indices

Indices’ Weekly Performance:

U.S. stocks ended the week with modest gains. All three major indexes closed higher, with the S&P 500 and Nasdaq marking their fourth straight daily advance as investors welcomed steady inflation, consumer spending, and sentiment data.

The S&P 500 came close to a new record but stayed just below its October 28 peak. Meanwhile, the Dow Jones Transportation Average extended its rally to 10 consecutive sessions, its longest winning streak since August 2020.

Stocks

Sector’s Weekly Performance:

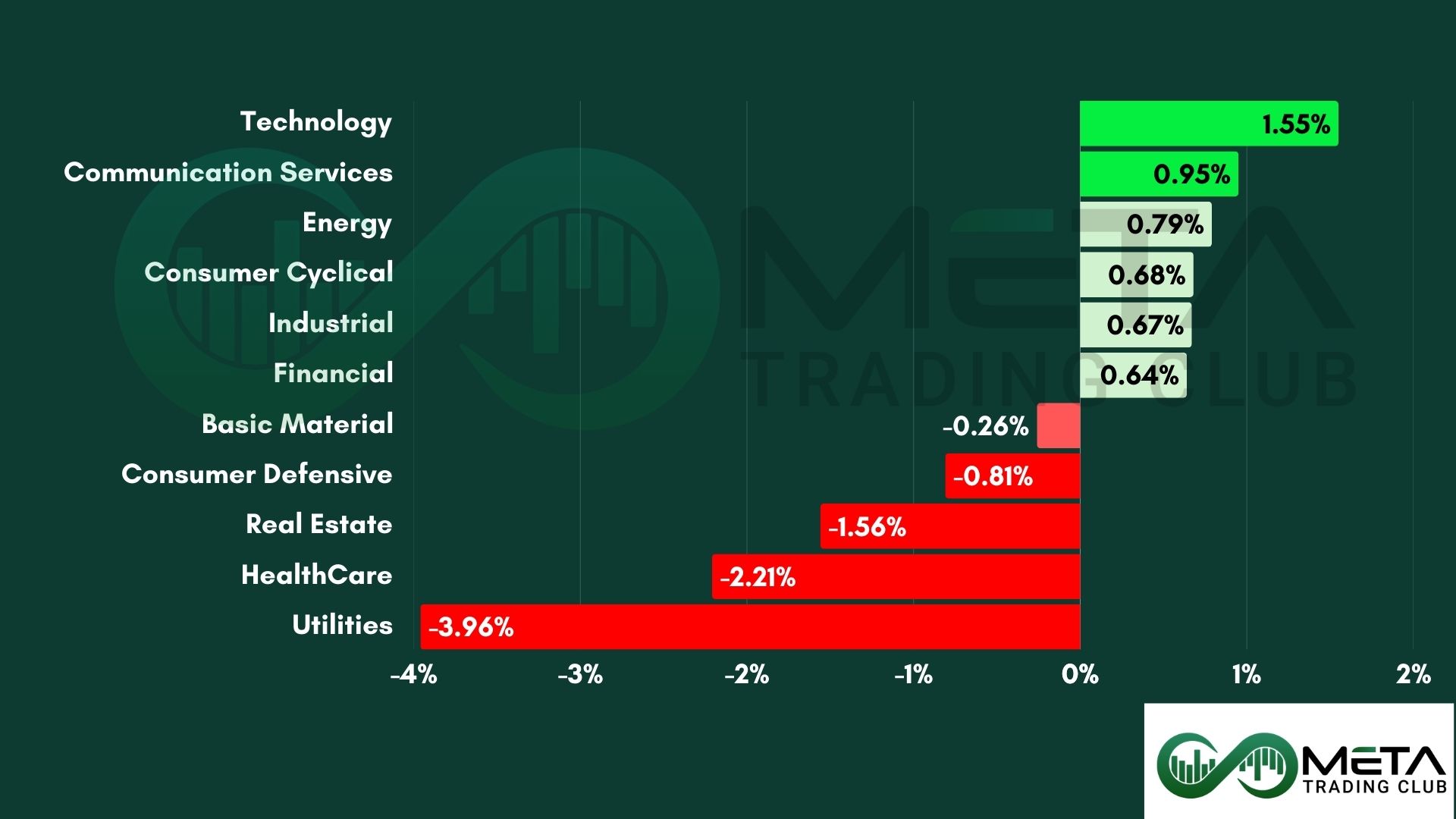

Last week’s market action reflected a risk-on rotation, with investors favoring growth sectors like Technology and Communication Services. Defensive areas such as Utilities and HealthCare lagged, as expectations for lower interest rates and stronger economic momentum shifted capital toward high-beta plays.

Technology led the market, fueled by semiconductors, cloud software, and AI momentum.

- Technology led the market with a 1.55% gain, driven by strength in semiconductors, cloud software, and AI infrastructure. This gain was followed by NXP Semiconductors, Applovin, Salesforce, Synopsys.

- Communication Services rose 0.95%, boosted by media consolidation headlines and record highs in streaming stocks. Warner Bros. Discovery rose following reports of Netflix’s $72B deal to acquire its TV, film studios, and streaming division.

- Energy posted a 0.79% gain amid stable crude prices and renewed interest in clean energy plays.

- Real Estate declined 1.56%, pressured by mixed housing data and lingering rate sensitivity.

- HealthCare dropped 2.21%, weighed down by policy uncertainty after vaccine advisers revised birth-dose recommendations.

- Utilities fell sharply 3.96% as investors rotated out of defensive names amid rate-cut optimism.

Top Performers

Last week saw a remarkable stock market performance, with several companies standing out as top gainers:

- NXP Semiconductors (NXPI): Surged 17% on broad-based growth, margin resilience, and innovation momentum driving a strong outlook and long-term targets.

- Applovin (APP): Soared 15.4% after announcing record ad revenue and launching new AI-driven optimization tools for mobile marketers.

- DoorDash (DASH): Gained 13.4% on increased holiday delivery volumes and expanded partnerships with major retailers.

- Salesforce (CRM): Jumped 13% after beating earnings estimates and unveiling new AI-powered CRM features at Dreamforce.

- Synopsys (SNPS): Rose 11.6% on optimism around semiconductor design demand and ahead of its upcoming earnings release.

- Marvell Technology (MRVL): Advanced 10.7% after projecting faster growth in its data center segment.

- Warner Bros. Discovery (WBD): Up 8.6% following reports of Netflix’s $72B deal to acquire WBD.

- Texas Instruments (TXN): Climbed 8.4% on signs of recovery in industrial and automotive chip orders.

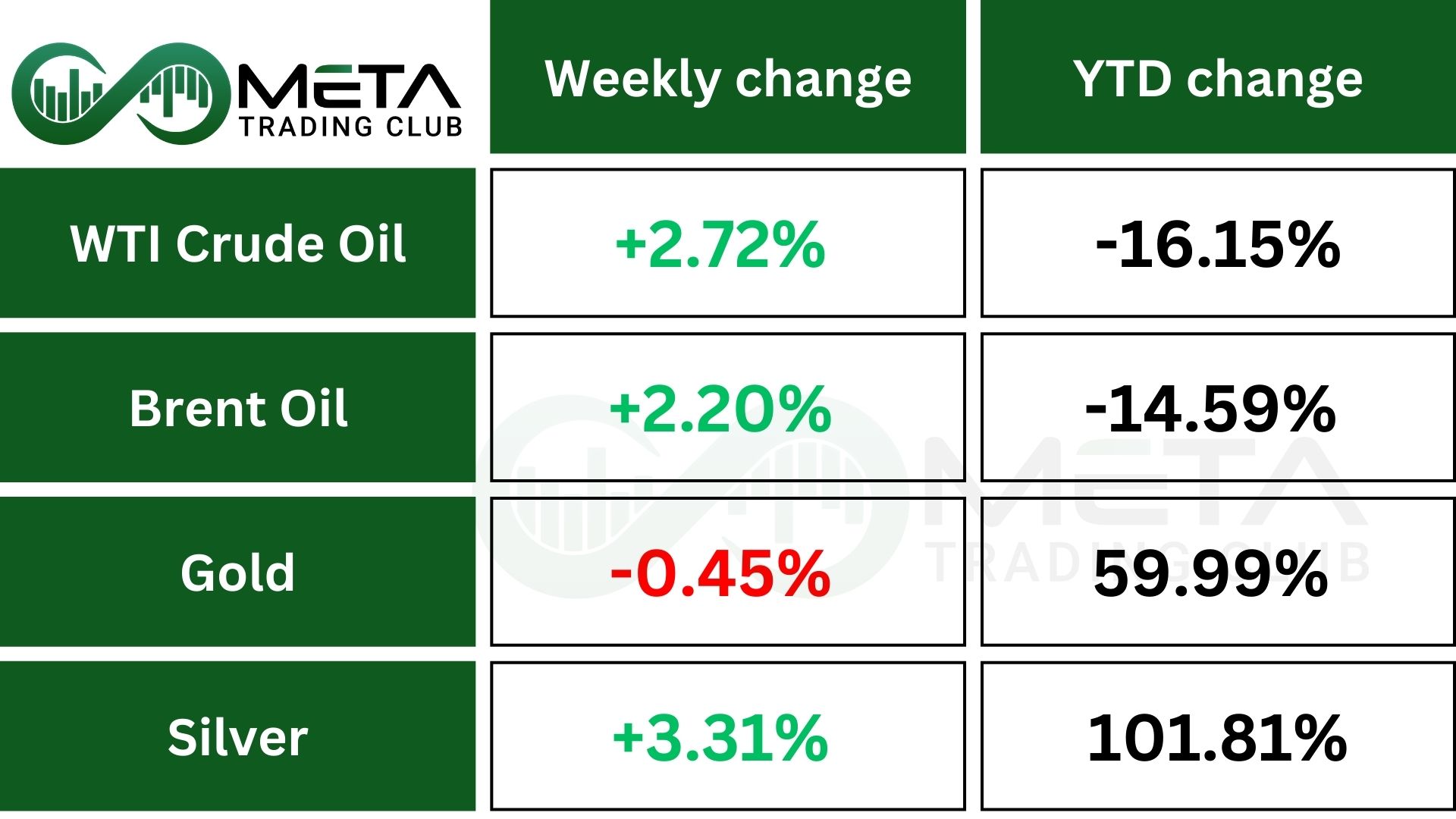

Commodity

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Metals

Gold stayed flat last week but has surged over 60% this year, its strongest run-in decades. Adjusted for inflation, it’s more expensive than ever, raising questions of a bubble versus a lasting shift.

The rally is unusual because gold is rising even as interest rates and bond yields climb. Analysts link this to central banks buying record amounts of gold, over 1,000 tones annually for three years, after the U.S. seized Russian reserves in 2022, prompting a search for assets immune to political risk.

Silver rebounded above $59, close to record highs. The recovery came after profit‑taking earlier in the week but was quickly reversed as fresh data strengthened expectations of a near‑term Fed rate cut. Softer inflation readings from the PCE index and weak labor signals (including falling private payrolls and rising layoffs) boosted demand for non‑yielding metals like silver.

This white metal has rallied 100% so far this year, fueled by supply deficits and its designation on the U.S. critical minerals list.

Energy

Crude oil prices ended higher, with crude hitting a 2‑week high. Prices were supported by ongoing war concerns in Ukraine, which keep sanctions on Russian energy exports in place.

Also, U.S. natural gas futures up 70% since mid-October, driven by strong export demand and winter cold forecasts. Europe confirmed plans to phase out Russian LNG by 2027, while U.S. exports surged 40% in November. Utilities also began seasonal withdrawals, slightly above expectations.

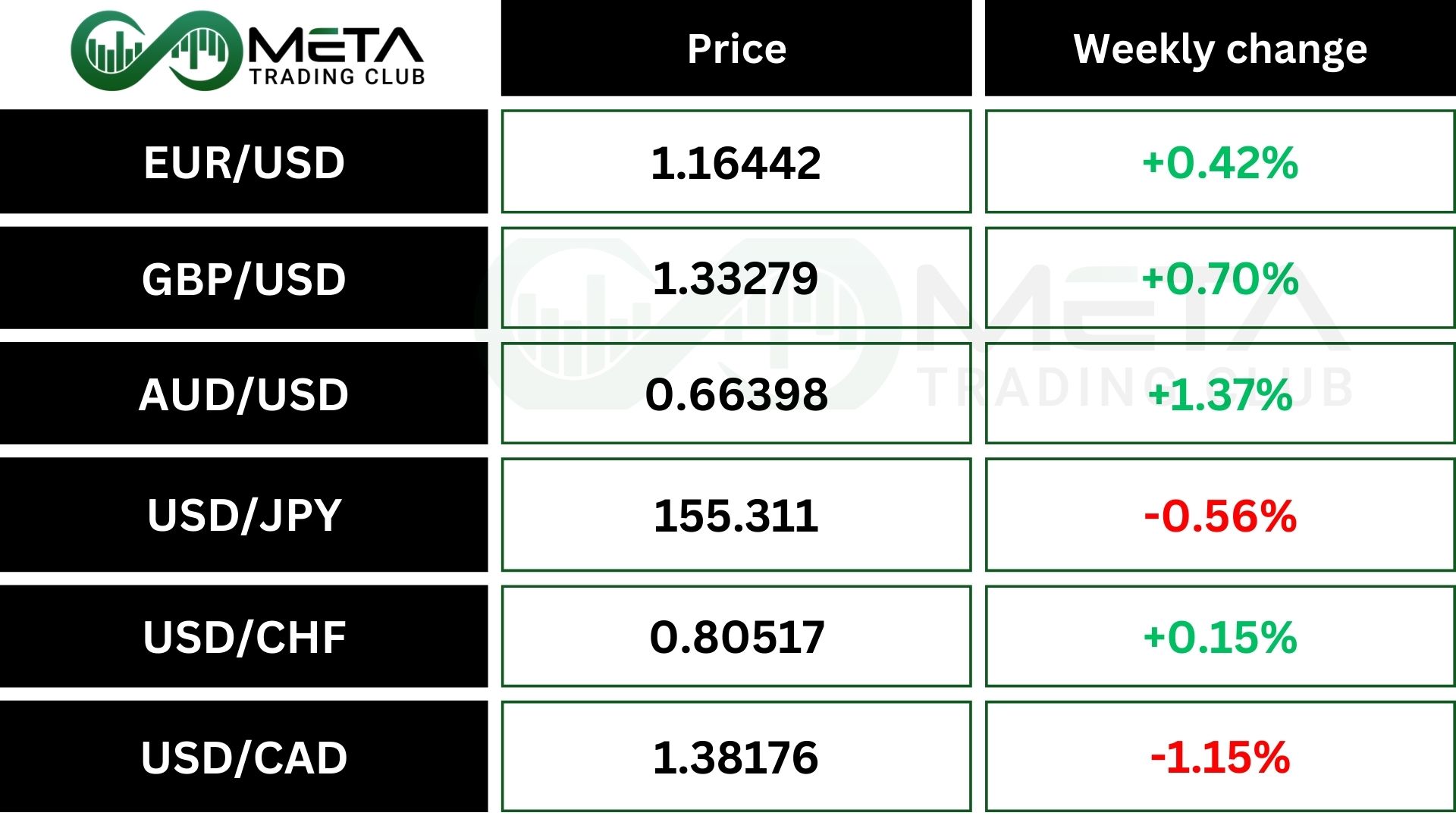

Forex

Weekly Performance of Major Foreign Exchange Pairs:

Last week, the Dollar Index (DXY) marking a 0.5% weekly loss as traders await next week’s Fed meeting. Markets are pricing a 90% chance of a rate cut.

The dollar index stayed below 99, its lowest in a month, as traders expect the Fed to cut rates in December. Weak labor data, high unemployment claims, and dovish Fed comment reinforced the case for a 25bps cut.

Meanwhile, the ECB is likely to keep rates steady due to inflation risks, while the Bank of Japan signaled a hike this month, highlighting diverging global monetary policies.

- EUR/USD: The euro closed to its three‑month average and within a narrow range. Recent strength has been supported by a weaker U.S. dollar, but geopolitical tensions, particularly the war in Ukraine and softer German factory orders pose risks.

- USD/JPY: The yen firmed to 155.34 per dollar, reflecting expectations that the Bank of Japan may raise rates in Dec. 19. This would mark a significant policy shift, as the yen has long been the funding currency for carry trades.

- GBP/USD: Sterling is holding near 1.33, its strongest level since late October. However, the Bank of England remains split ahead of its Dec. 18 meeting: hawks warn of persistent inflation, while doves point to slowing growth and a softer labor market

Crypto

Bitcoin trading activity has dropped sharply alongside its price correction. Spot trading volume (the amount of Bitcoin bought and sold for immediate delivery) fell heavily in November as Bitcoin lost 17.5% of its value.

Binance, which handles more than half of Bitcoin’s spot trades, saw volume plunge from $198B in October to $156B in November (a 21% decline).

Altcoins remain weak while Bitcoin dominates. Bitcoin holds nearly 60% of the market, and despite losing momentum, altcoins have not gained. The Altcoin Season Index is at 20 (down from 83 last year), showing the market is still heavily tilted toward Bitcoin. Sentiment is also poor and investors are cautious and avoiding new positions.

Altcoins have lagged all year, and even though Bitcoin is down almost 29% from its October high, money has not shifted into altcoins.

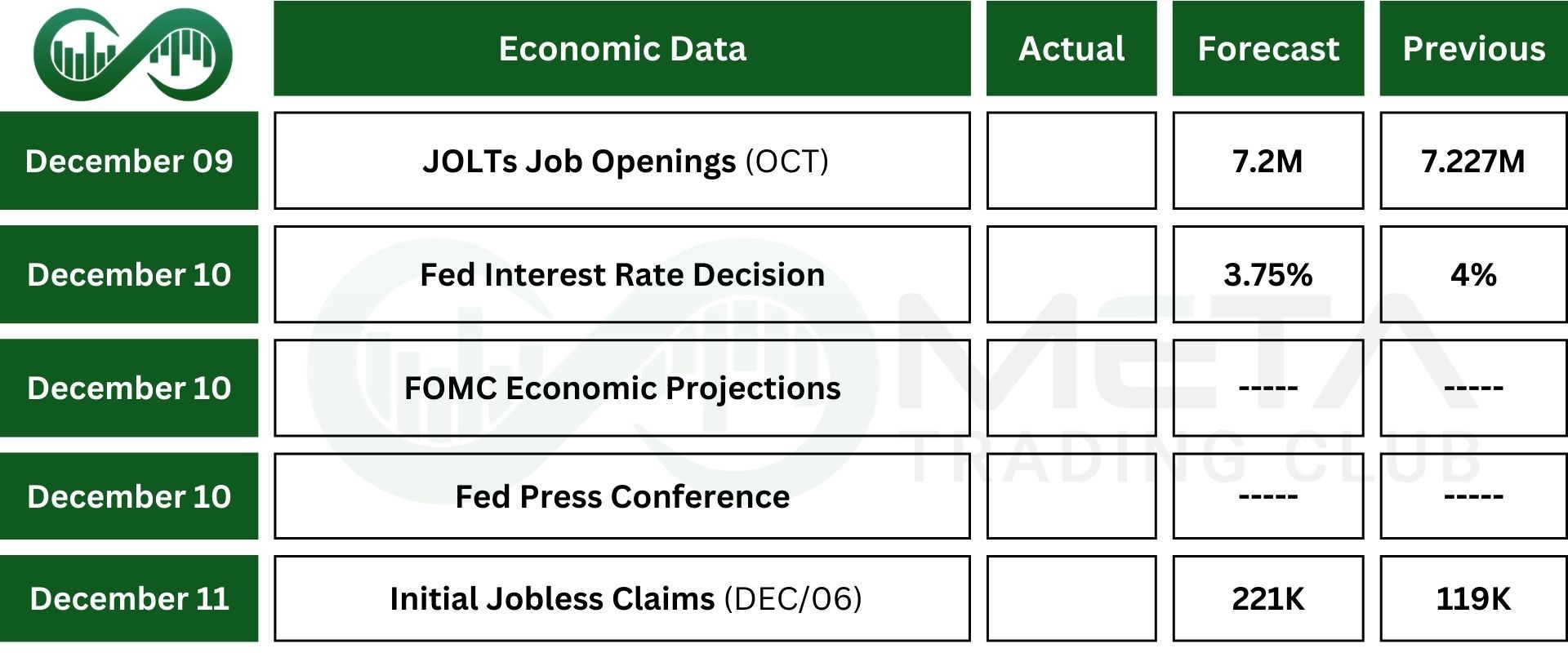

Next Week’s Outlook

Economic Events

This week, U.S. markets will turn focus to the Federal Reserve’s final policy meeting of the year and the release of updated economic projections. Policymakers are widely expected to deliver a third straight rate cut on Wednesday, with futures pricing an 87% chance of a 25bps reduction and anticipating two to three more cuts in 2026 as labor market conditions soften.

Fed Chair Jerome Powell’s comments will be closely watched for signals on future policy.

Attention will also fall on a backlog of key economic reports delayed by the government shutdown. These include JOLTs job openings for September and October and wholesale inventories likely up 0.1%.

Additional releases feature the Q3 Employment Cost Index, November’s federal budget statement, consumer inflation expectations, the NFIB Business Optimism Index, and weekly labor indicators such as initial jobless claims and the ADP employment report.

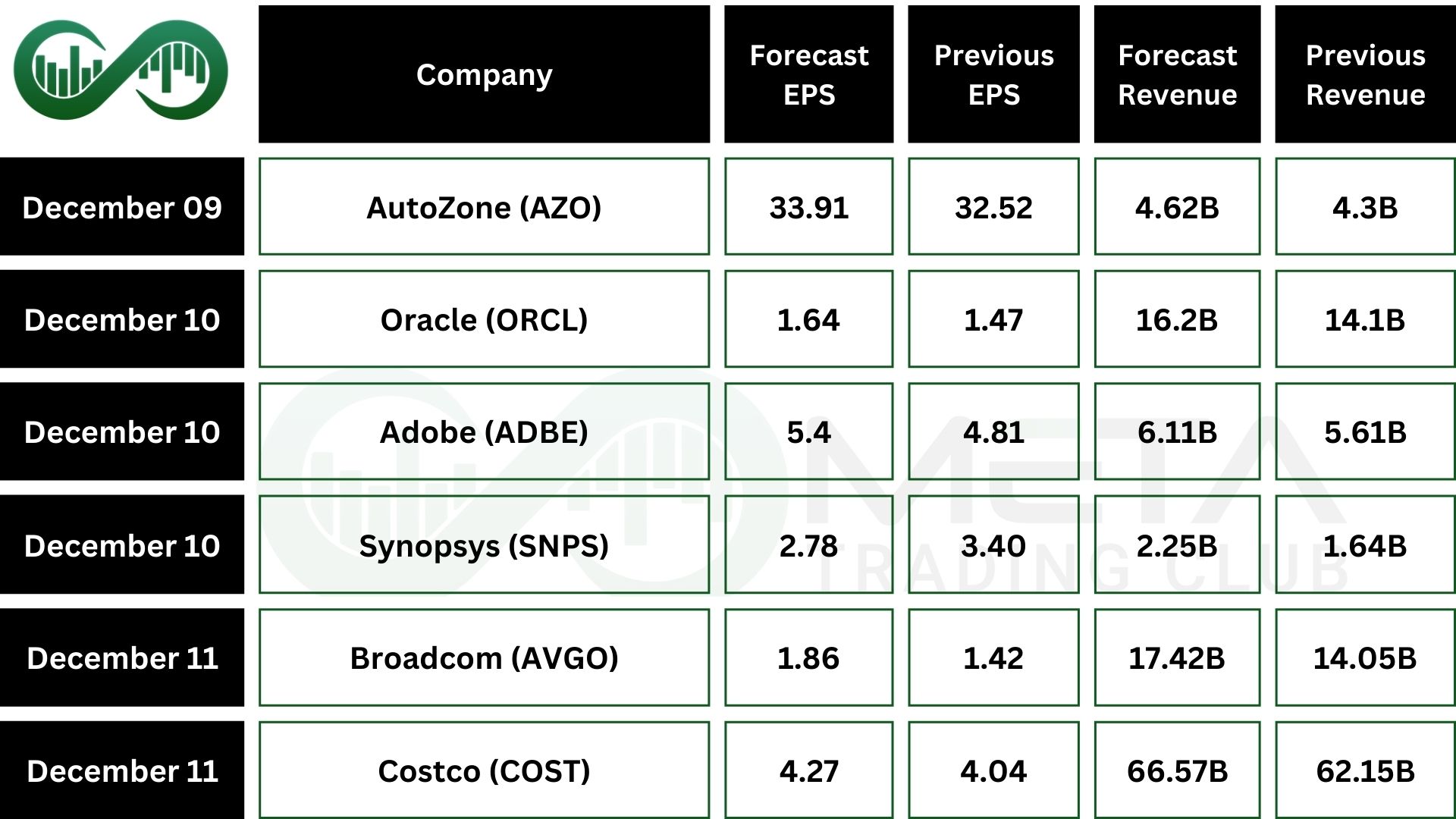

Earnings Events

On the corporate side, Broadcom (AVGO) and Oracle (ORCL) are set to announce quarterly earnings, adding further weight to a pivotal week for markets.