Last Week’s report

Economic Reports

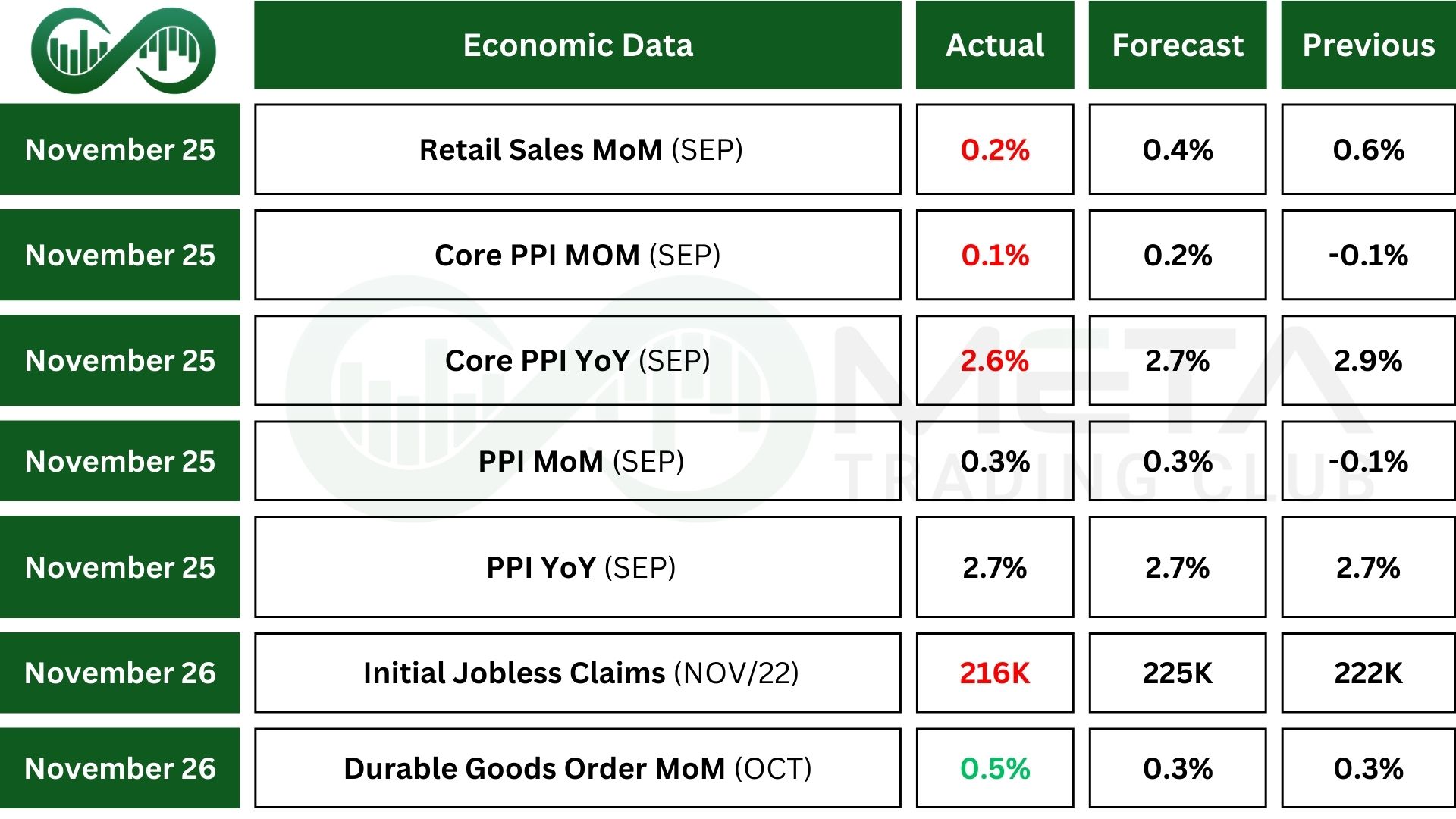

In September 2025, U.S. Producer Prices Index rose 0.3%, bouncing back from a 0.1% drop the month before, in line with expectations. Food costs jumped 1.1% as higher meat prices outweighed cheaper vegetables. Energy prices also rebounded, up 3.5% due to gains in natural gas liquids and ethanol, pushing goods inflation to 0.9%, the highest in over a year. Compared with a year earlier, producer price inflation held steady at 2.7%.

Core U.S. producer prices, excluding food and energy, rose 0.1% in September 2025 after a 0.1% drop in August, coming in below forecasts of a 0.2% gain. Service prices were flat, while goods prices increased 0.9%, the strongest monthly rise in over a year. On an annual basis, core producer inflation slowed to 2.6%, the lowest since July 2024, down from a revised 2.9% in August and just under analyst expectations of 2.7%.

U.S. Retail Sales rose 0.2% in September 2025, the smallest gain in four months and below forecasts of 0.4%, after a 0.6% increase in August. Excluding food services, autos, building materials, and gasoline, sales slipped 0.1%, missing expectations of a 0.3% rise.

U.S. Durable Goods Orders rose 0.5% in September 2025, beating expectations after a strong 3% gain in August. Excluding transportation, orders rose 0.6%, while excluding defense they edged up just 0.1%. A key measure of business investment, non-defense capital goods excluding aircraft, climbed 0.9%, matching August’s pace.

Earnings Reports

Analog Devices

Analog Devices (ADI) reported strong results with revenue up 17% to $11 billion, net income rising 39% to $2.27 billion, and gross margin reaching 61.5%, supported by double‑digit growth across all markets.

Analysts remain upbeat, with several firms raising price targets in the range of $258 to $320, signaling confidence in ADI’s continued momentum. Also, ADI broke all time high resistance after its earnings were released.

Dell Technologies

Dell Technologies (DELL) reported record third-quarter earnings driven by surging demand for AI servers, strong growth in its Infrastructure Solutions Group (ISG), and improved margins.

Revenue rose 11% to $27 billion, with ISG sales up 24% and server/networking sales up 37%.

Diluted EPS hit $2.59, up 17% year over year, while gross margin climbed to $5.7 billion.

Dell received $12.3 billion in AI server orders this quarter, contributing to a $30 billion total for the year and an $18.4 billion backlog.

The company expects Q4 sales of $31–$32 billion and FY26 AI server revenue to exceed $25 billion. Dell also returned $1.6 billion to shareholders through buybacks, emphasizing operational flexibility amid rising costs.

Indices

Indices’ Weekly Performance:

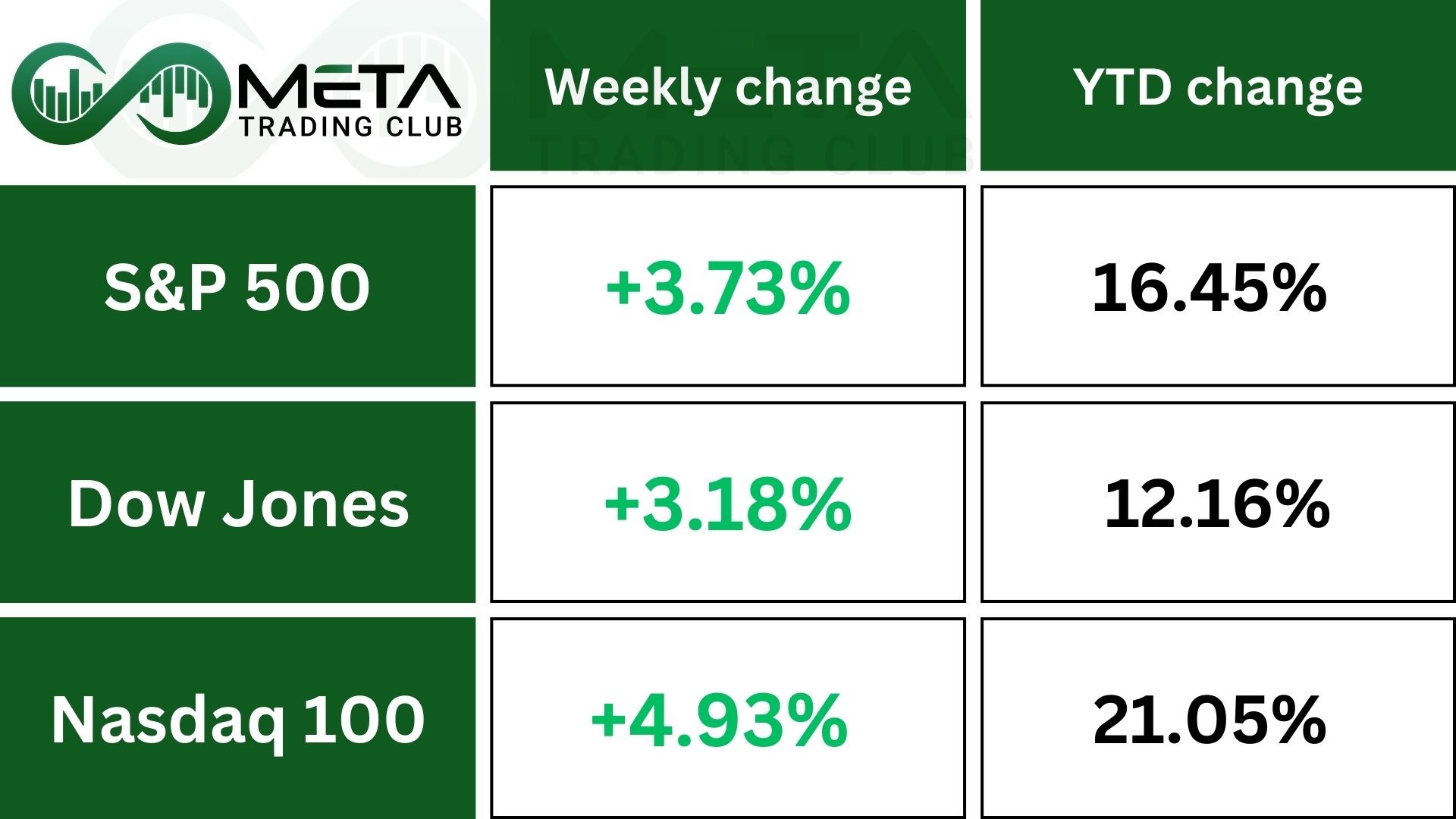

The S&P 500 and Dow Jones Industrial Average (DJI) both extended their win streaks to seven consecutive months, underscoring sustained investor optimism amid expectations of rate cuts and resilient corporate earnings.

However, the Nasdaq Composite (IXIC) broke its own seven-month winning streak, slipping modestly in November despite strong weekly gains.

This marks the S&P 500’s first seven-month win streak since August 2021, a period fueled by post-pandemic recovery and tech-led momentum. The Dow’s current run is its longest since a 10-month stretch that ended in January 2018, reflecting broad-based strength across industrials, financials, and consumer sectors.

Meanwhile, the Nasdaq’s last comparable streak also ended in January 2018, highlighting the index’s historical sensitivity to rate expectations and tech sector volatility.

The S&P 500 has built upward momentum over the past two weeks, breaking its short‑term downtrend line, with the MACD turning positive on the daily chart. A breakout above the 6850 resistances could pave the way for a move toward all‑time highs, though fading momentum may lead to a rejection at this level.

Stocks

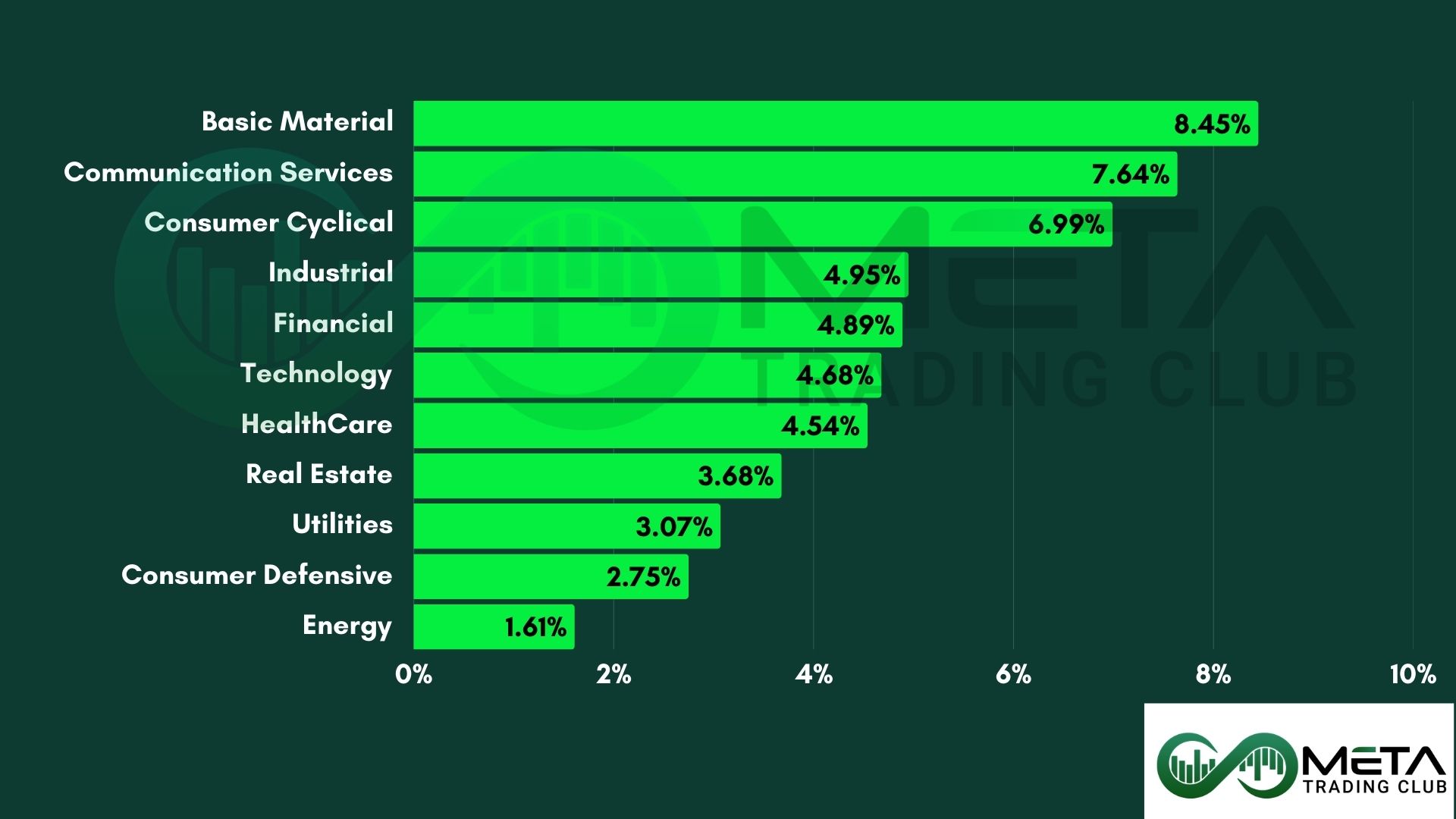

Sector’s Weekly Performance:

Nearly all S&P 500 (SPX) sectors advanced, though changes were relatively subdued.

- Basic Materials soared 8.45%. Top-performing sector, likely driven by commodity price strength and industrial demand.

- Communication Services surged 7.64%, boosted by media and digital ad platforms, possibly tied to AppLovin’s rally.

- Consumer Cyclical advanced 6.99% as retail and travel names rebounded on holiday spending and discretionary demand.

- Industrials gained 4.95%, benefited from infrastructure momentum and logistics recovery.

- Financial rose 4.89%, lifted by Robinhood and Coinbase gains, plus rate stability and ETF inflows.

- Technology climbed 4.68% as AI infrastructure and chip stocks (Broadcom, Intel, Micron) led the charge.

- Energy up 1.61%, lagged due to oil price softness and mixed inventory data.

Top Performers

Last week saw a remarkable stock market performance, with several companies standing out as top gainers:

- Robinhood Markets (HOOD): Surged 19.75% on opening new billion dollar market announcement, triggering passive index fund buying.

- Broadcom (AVGO): Soared 18.45% on AI infrastructure demand after Gemini 3 launch.

- Intel (INTC): Advanced 17.57% on bullish analyst upgrades, AI chip momentum, and Apple partnership speculation.

- Western Digital (WDC): Climbed 17.34% on AI-driven storage demand, NAND pricing recovery, and spin-off optimism.

- Seagate Technology (STX): Gained 16.51% on HAMR tech adoption, improving margins, and AI-related storage tailwinds.

- Marvell Technology (MRVL): Rose 15.41% on positive analyst commentary, insider buying, and strong AI networking exposure.

- AppLovin Corporation (APP): Up 15.23% on Axon Ads Manager launch, $3.2B buyback, and strong revenue growth.

- Analog Devices (ADI): Advanced 14.04% on strong earnings, upbeat guidance, and industrial/comms sector strength.

- Micron Technology (MU): Gained 14.01% on AI memory demand, DRAM/NAND price recovery, and multiple analyst upgrades.

- Coinbase Global (COIN): Rose 13.48% on crypto market rally, Bitcoin ETF inflows, and regulatory clarity from the GENIUS Act.

Commodity

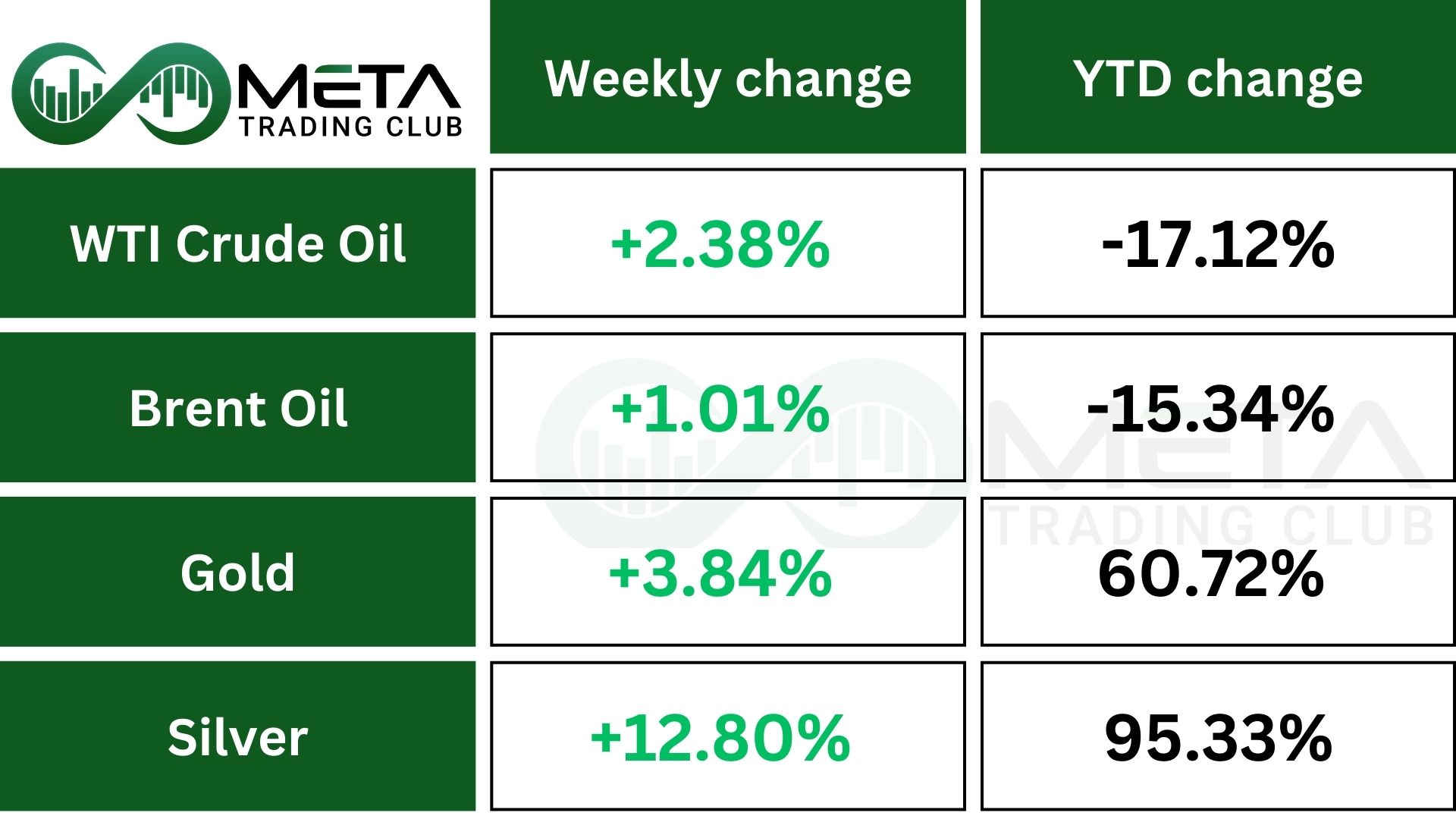

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Gold rose above $4,220 per ounce on Friday, hitting a one-month high and heading for its fourth straight monthly gain.

Traders are increasingly expecting a Fed rate cut in December, helped by weak economic data and dovish comments from Fed officials.

A possible replacement for Jerome Powell, also backed lower rates, raising the chance of a 25 basis point cut to over 80% and leading markets to price in three more cuts by the end of 2026.

Strong demand from central banks and ETF investors, along with falling real yields, is driving gold higher and could make this its best year since 1979.

Silver prices continued their rally, nearing a record $55 per ounce as supply shortages and expectations of further Federal Reserve rate cuts fueled demand.

Chinese inventories fell to their lowest in a decade after heavy shipments to London, while exports surged to an all‑time high of over 660 tonnes in October. With global uncertainty, looser monetary policy, and tightening supply, silver has repeatedly tested record highs.

Crude oil and gasoline prices climbed as a weaker dollar boosted energy markets and geopolitical tensions kept supply concerns elevated. The ongoing Russia‑Ukraine war, reduced Russian exports, and new sanctions have tightened supply, while Ukraine’s strikes on refineries cut up to 20% of Russia’s capacity.

Meanwhile, OPEC+ is expected to pause production increases in early 2026, and U.S. military activity in Venezuela adds further risk.

Despite OPEC revising Q3 balances to a surplus and U.S. production estimates rising, tanker storage hit a 2.25‑year high, underscoring the complex mix of supply and demand pressures driving oil prices.

Forex

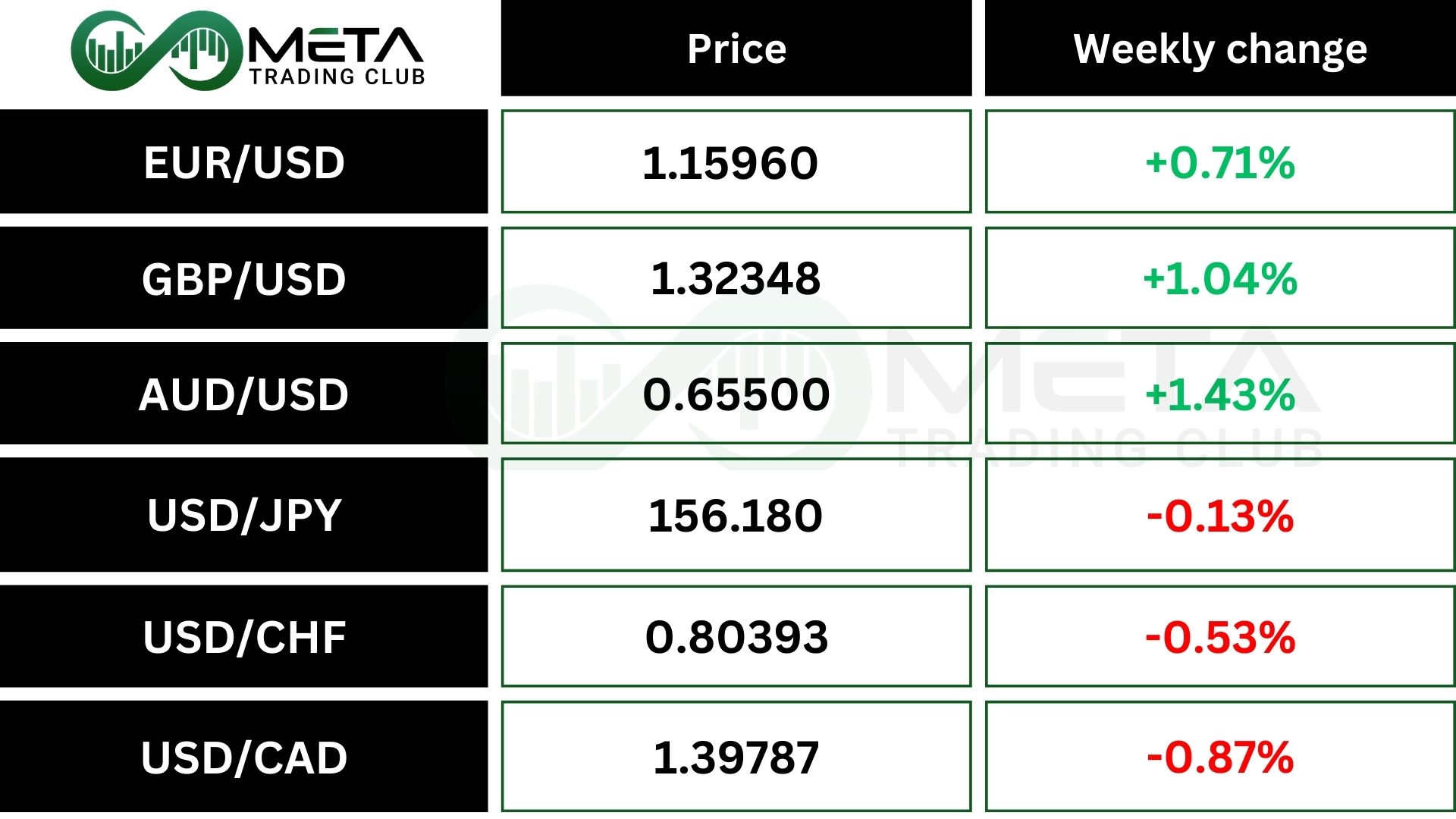

Weekly Performance of Major Foreign Exchange Pairs:

Last week, the Dollar Index (DXY) ended lower while gold prices rallied, as investors grew more confident that the Federal Reserve may cut interest rates soon.

The weaker dollar reduced demand for the currency, while expectations of easier monetary policy boosted safe‑haven assets like gold. This combination reflected shifting market sentiment, with traders positioning for potential Fed easing into year‑end.

Crypto

Bitcoin dropped after failing to stay above $90,000. Analysts say there isn’t a clear reason, but falling market volatility last week may have worried investors already cautious about the year-end outlook.

Bitcoin tumbled nearly 5% to around $85,500, extending its decline from October’s $126,000 peak amid heavy liquidations.

This move may validate a bearish technical pattern, with potential downside toward $70k.

Next Week’s Outlook

Economic Events

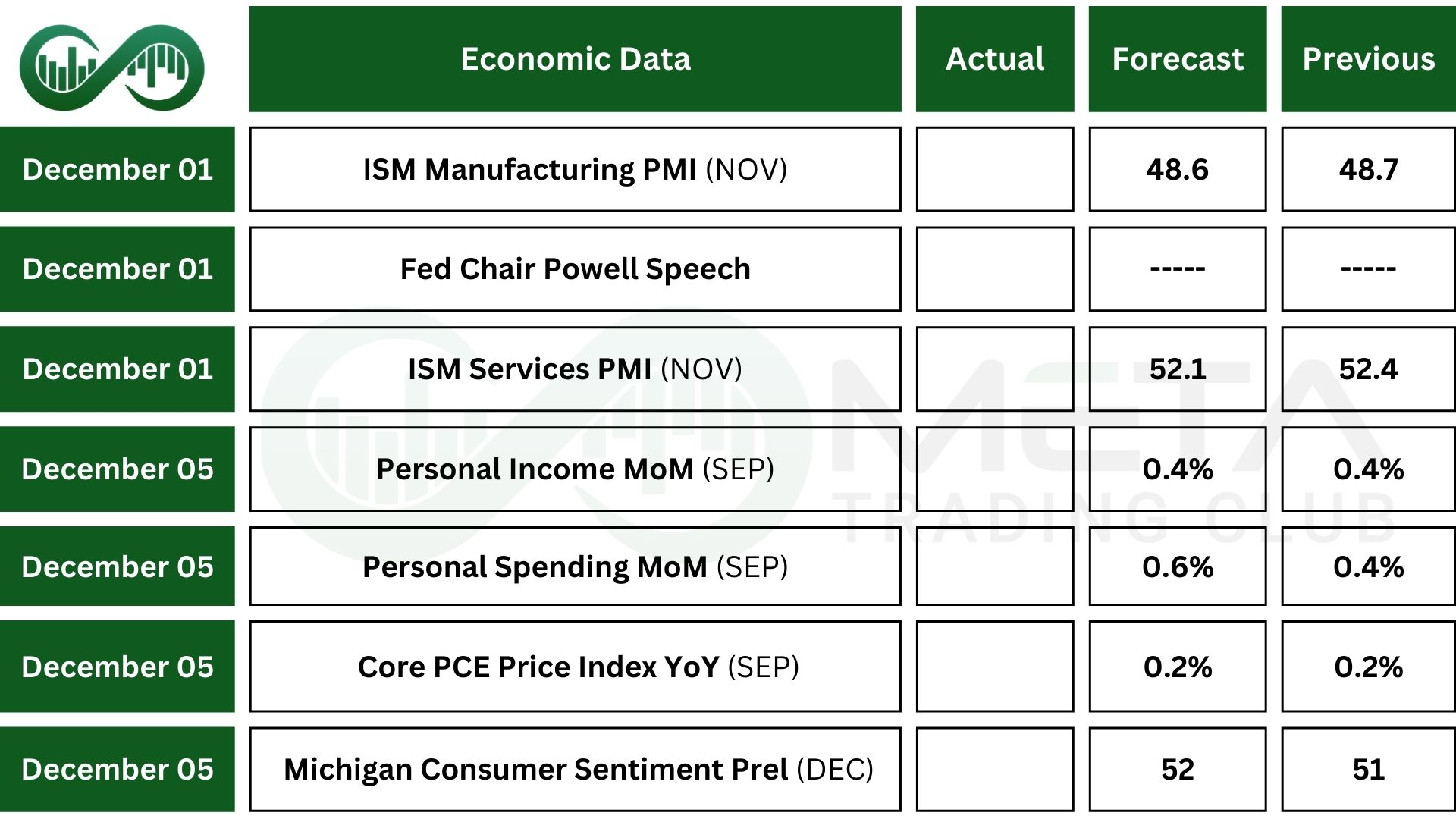

In the United States, market participants will closely monitor a new wave of economic data releases, including several reports that were previously delayed.

The September Personal Consumption Expenditures (PCE) report is anticipated to show a year-over-year increase of 2.8% in the headline PCE price index, the fastest pace since April 2024, and a monthly rise of 0.3%. Core PCE is expected to remain unchanged at 2.9% annually and 0.2% month-over-month.

Personal spending is projected to have grown by 0.4%, reflecting a deceleration from August’s 0.6% gain, while personal income growth is likely to have held steady at 0.4%.

The ISM Manufacturing PMI is forecast to indicate continued contraction in factory activity for November, whereas the Services PMI may reveal a modest slowdown in service-sector expansion.

The ADP employment report is expected to show that the private sector added approximately 20,000 jobs in November, down from 42,000 in October.

Preliminary data from the University of Michigan is likely to suggest an improvement in consumer sentiment, while industrial production is projected to have increased by 0.1% in September, consistent with the prior month.

Additional key releases include Challenger job cuts, changes in consumer credit, export and import price indices, and final readings of the S&P Global Purchasing Managers’ Indexes.

Earnings Events

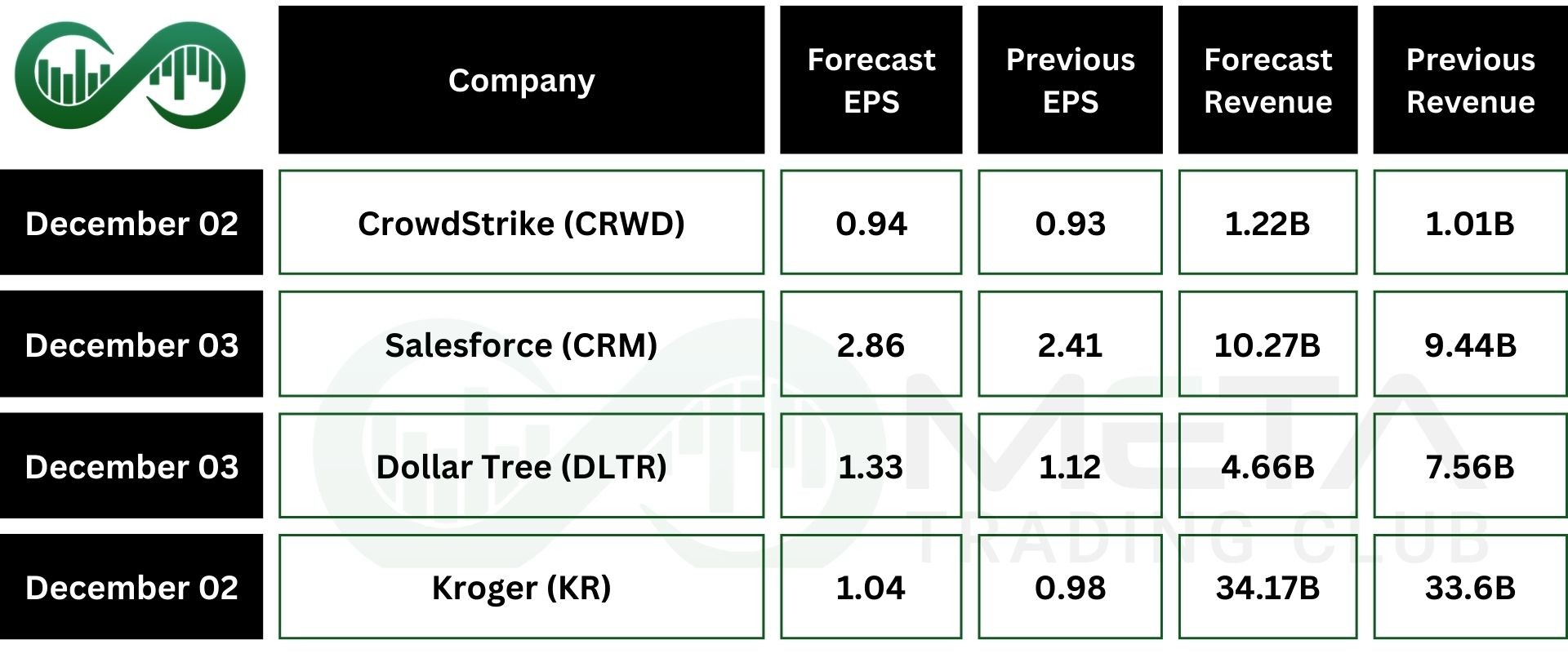

This week, earnings reports are due from CrowdStrike (CRWD), Dollar Tree (DLTR), Salesforce (CRM), and Kroger (KR).