Last Week’s report

Economic Reports

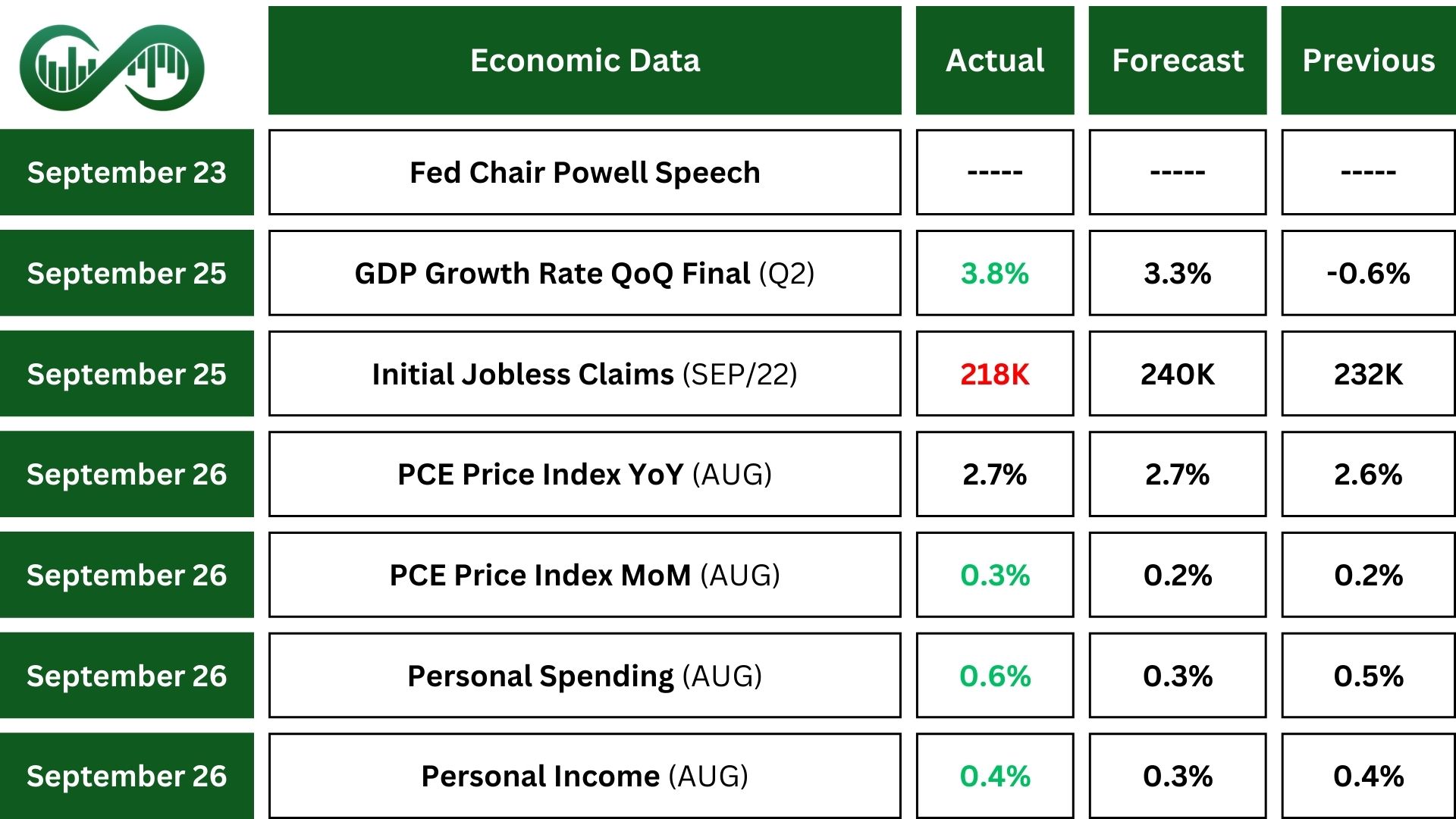

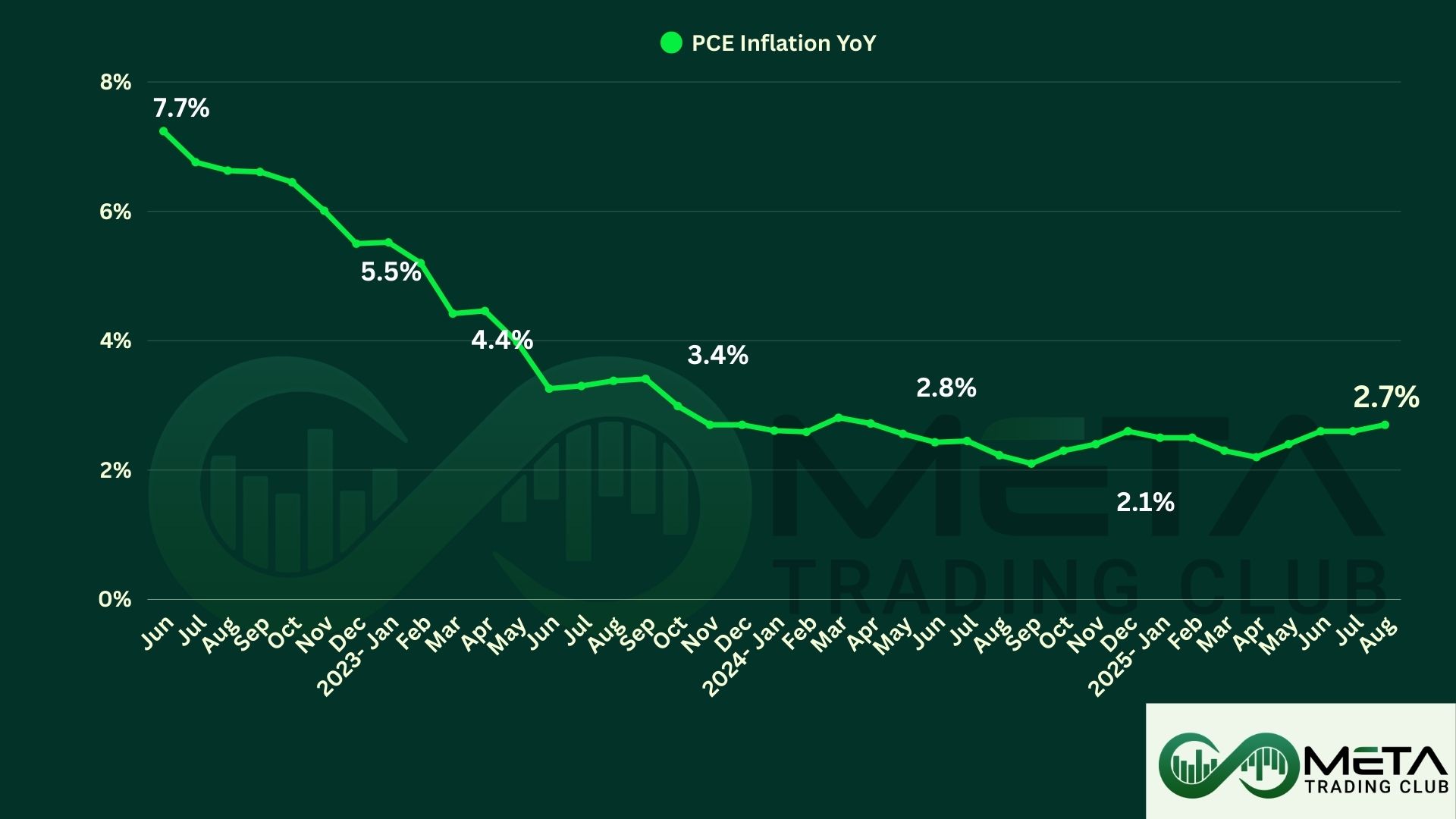

PCE

In August 2025, U.S. household income and spending continued to grow despite high interest rates and economic uncertainty.

Personal income rose 0.4%, while consumer spending jumped 0.6%, the biggest monthly increase in five months. Americans spent more on both services and goods, yet still maintained a steady savings rate of 4.6%.

Inflation remained stable, with the PCE price index rising 0.3% and core PCE (excluding food and energy) up 0.2%.

Year-over-year, headline inflation reached 2.7%, the highest in six months, while core inflation stayed at 2.9%, matching forecasts.

The report boosted market confidence thanks to strong spending and steady inflation. However, persistent price pressures in services may lead the Federal Reserve to delay further interest rate cuts.

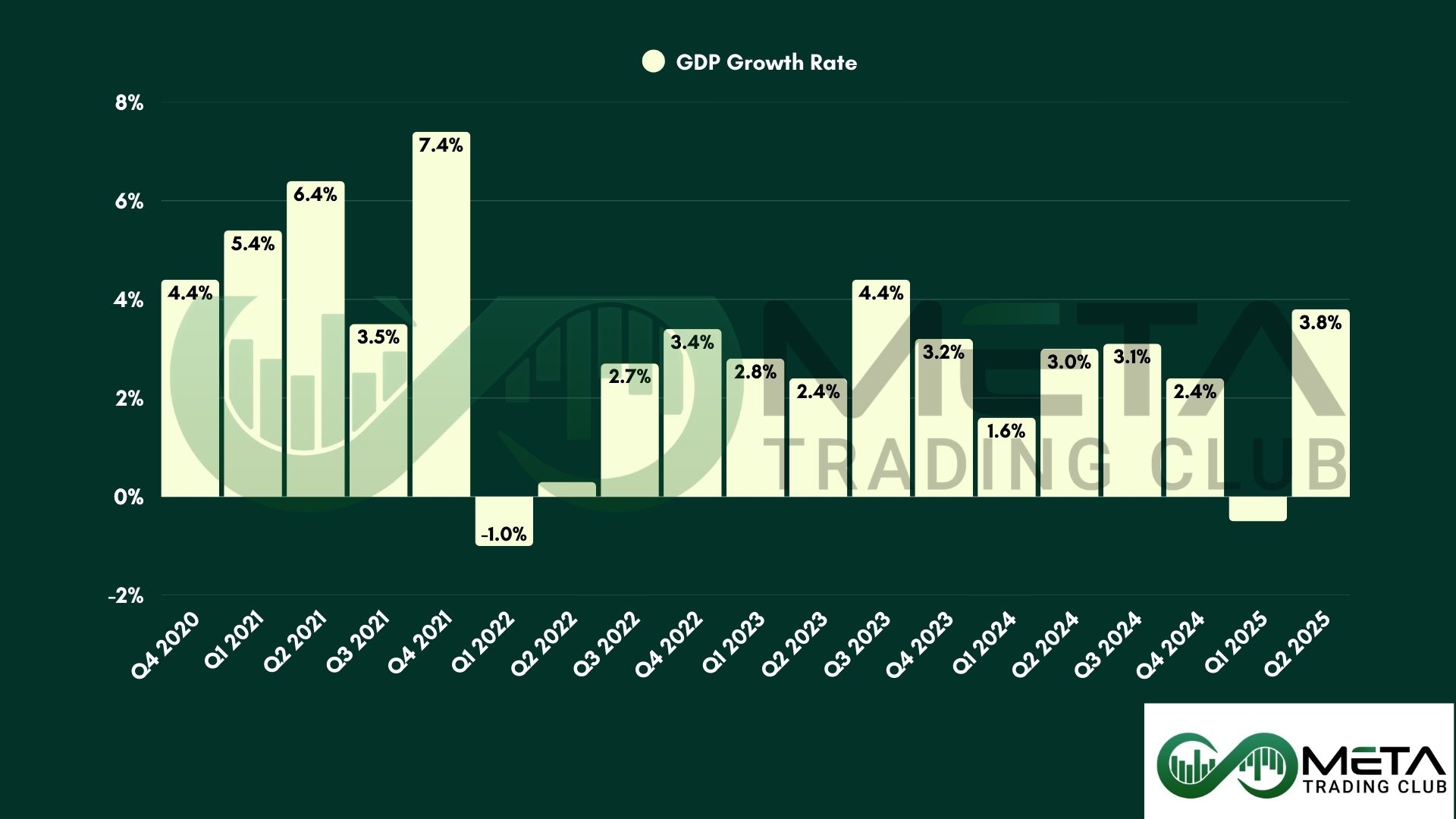

GDP

The final estimate for U.S. GDP in Q2 2025 showed strong growth of 3.8%, the best since late 2023 and a sharp rebound from Q1’s contraction.

The improvement was driven by higher consumer spending and fewer imports, with household demand stronger than earlier reports suggested. Spending on both goods and services rose..

Corporate profits increased by $6.8 billion, but were revised downward sharply, indicating weaker earnings momentum.

Overall, the report boosted market confidence and alleviated recession fears, although concerns about inflation and earnings could pressure rate-sensitive sectors. Investors may favor companies with strong pricing power and cost control.

Earnings Reports

Micron Technology

Micron (MU) delivered a strong performance in its fiscal Q4 2025, beating expectations and closing out a record-breaking year.

The company reported $11.32 billion in revenue, and Adjusted earnings came in at $3.03 per share, well above forecasts.

Micron also declared a quarterly dividend of $0.115 per share, payable in October.

Looking ahead, Micron expects Q1 2026 revenue of about $12.5 billion and earnings per share of $3.56 (GAAP), signaling continued momentum.

As the only U.S.-based memory manufacturer, Micron is seen as well-positioned to benefit from rising AI demand.

Costco Wholesale

Costco (COST) reported strong results for its fiscal Q4 2025 and full year. The company slightly beat expectations, with quarterly revenue and earnings coming in above forecasts.

Net sales rose 8% to $84.4 billion for the quarter, and net income reached $2.61 billion, or $5.87 per share.

E-commerce was a standout, growing over 15% annually, and membership fees rose 14% to $1.72 billion.

The company added 27 new warehouses, bringing its global total to 914, and executive memberships grew 9.3% to nearly 39 million.

Management noted that consumers are becoming more cautious with discretionary spending. This raised concerns about future growth in higher-margin categories, despite core value items and international sales remaining strong.

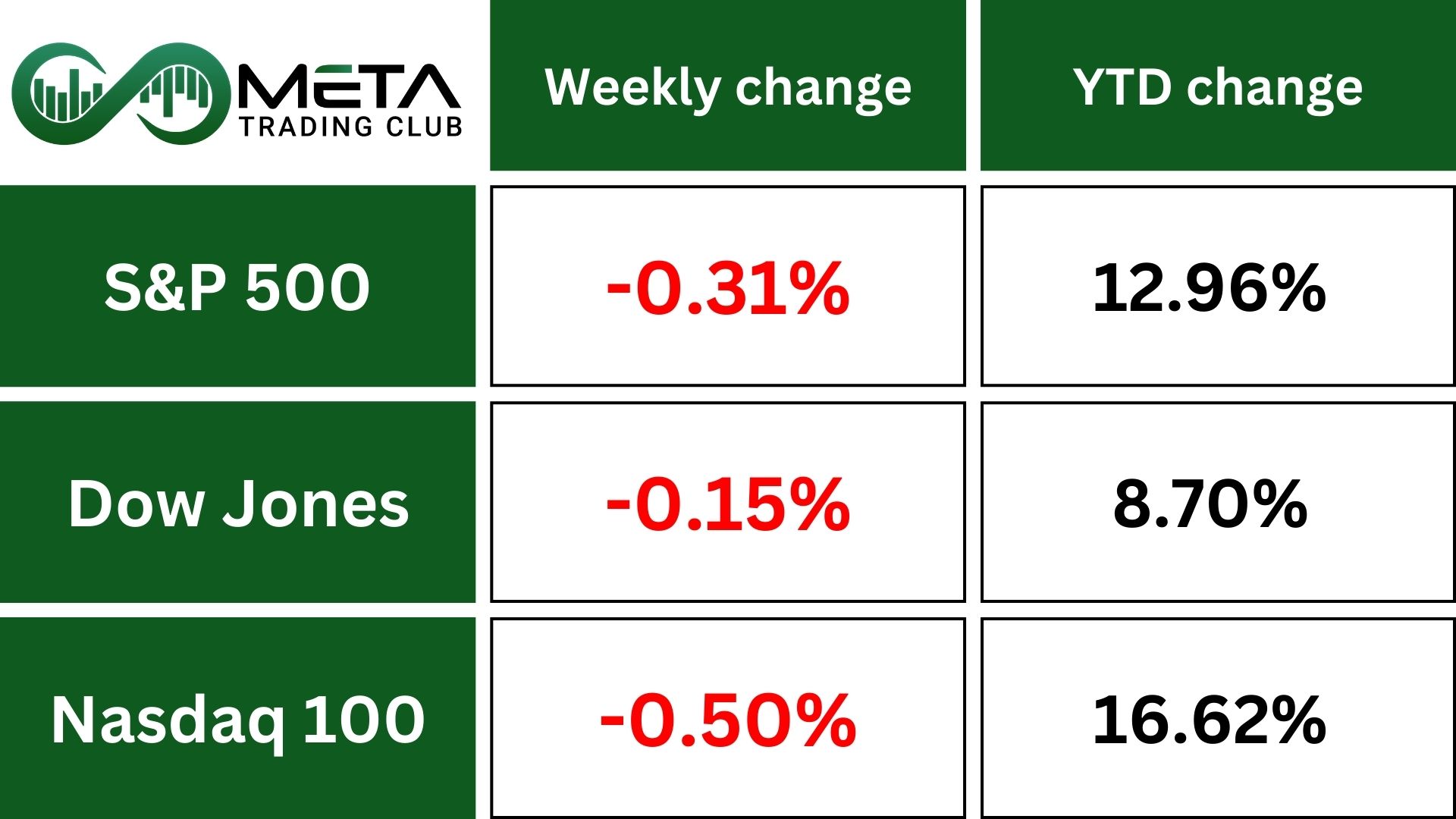

Indices

Indices’ Weekly Performance:

S&P 500 (SPX) fell 0.3%, ending its three-week winning streak. Strong economic data made investors doubt whether the Fed will cut interest rates again soon.

Dow Jones (DJI) slipped 0.1%, and Nasdaq (NDX) dropped 0.7%, both also ending three weeks of gains.

The S&P 500 and Nasdaq ended their three-week winning streaks as investors weighed strong economic data against expectations for further Fed rate cuts.

August’s PCE report showed inflation in line with forecasts, but personal income and spending came in stronger than expected.

The Fed cut rates last week and signaled more could follow, leaving markets uncertain about its next move. With quarter-end approaching and earnings season starting mid-October, volatility is expected.

Meanwhile, new import tariffs were announced by President Trump, including on heavy-duty trucks and tariffs on branded pharmaceuticals.

Stocks

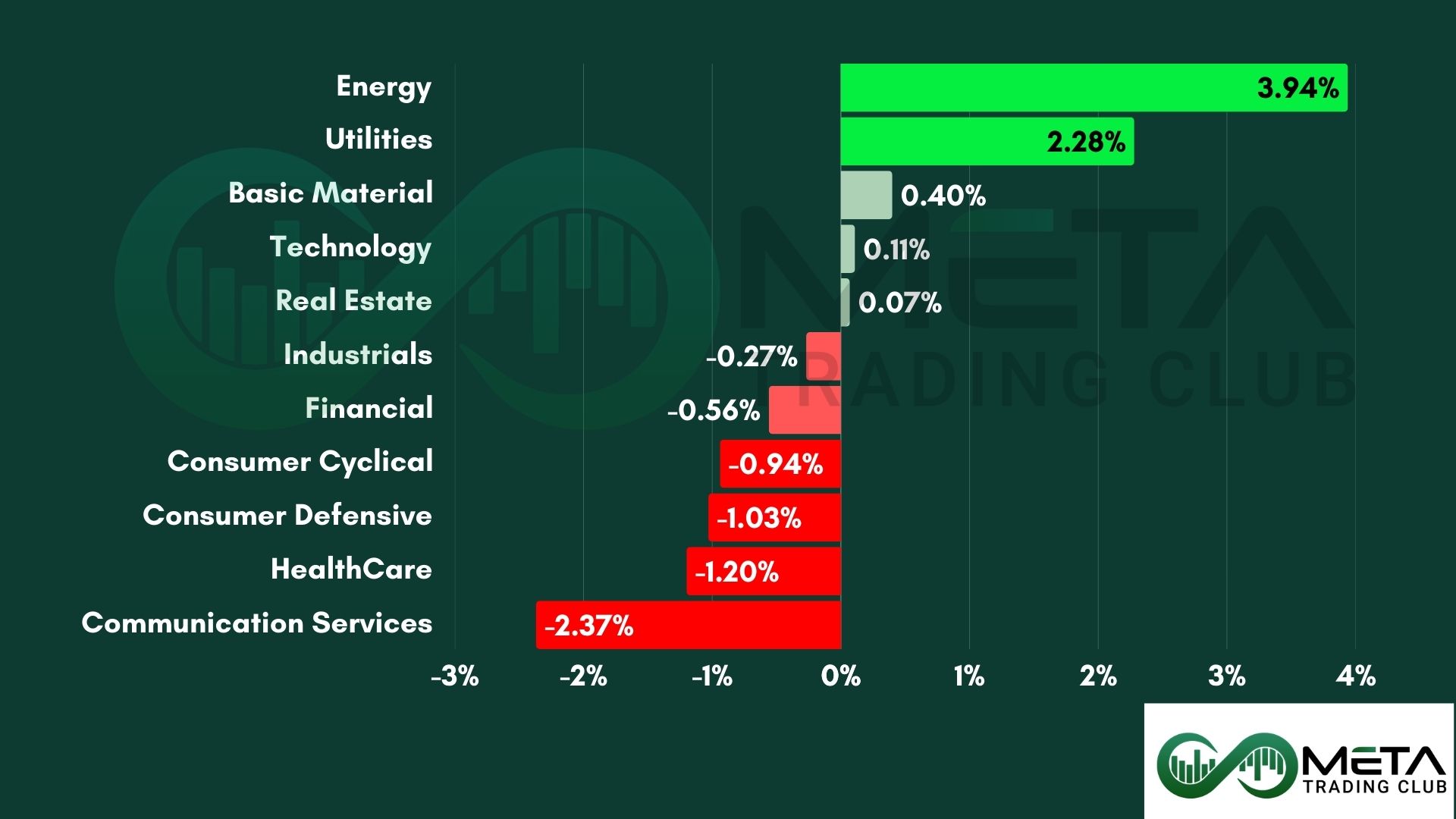

Sector’s Weekly Performance:

Most sectors pulled back this week, with Communication Services and Materials hit hardest. Energy stood out as the strongest performer.

Communication Services fell 2.4%.

- Match Group declined after Meta added new features to Facebook Dating. Meta also fell following reports that it may face EU charges for not properly moderating illegal content.

- Disney rose midweek as Jimmy Kimmel’s return to late-night TV boosted ratings to a 10-year high and drove social media engagement.

- Electronic Arts surged on Friday on reports of a potential take-private deal.

Consumer Discretionary dropped 1%.

- Carmax dropped 23% to a five-year low due to excess inventory and falling used-car prices, which hurt Q2 profits.

Consumer Staples declined 1%

- Kenvue slumped after President Trump linked Tylenol to autism.

- Costco dipped despite beating quarterly expectations, as investor response remained mixed.

Industrials edged down 0.3%

- Boeing edged higher after the FAA approved its request to issue airworthiness certificates for some 737 MAX and 787 aircraft.

Tech rose 0.1%

- Intel jumped 20% on reports it may receive investment from Apple.

- Nvidia hit a record high following news of a $100 billion investment in OpenAI.

- The Semiconductor Index rose about 1%.

- Apple gained on signs of strong early demand for the iPhone 17.

Materials rose 0.4%

- Freeport-McMoRan plunged nearly 20% for the week after declaring force majeure at its Grasberg mine in Indonesia and cutting copper and gold sales forecasts.

Energy surged 4%

- The sector rallied strongly, boosted by Russia’s decision to cut fuel exports after Ukraine attacked its energy infrastructure. It marked Energy’s best week since mid-June.

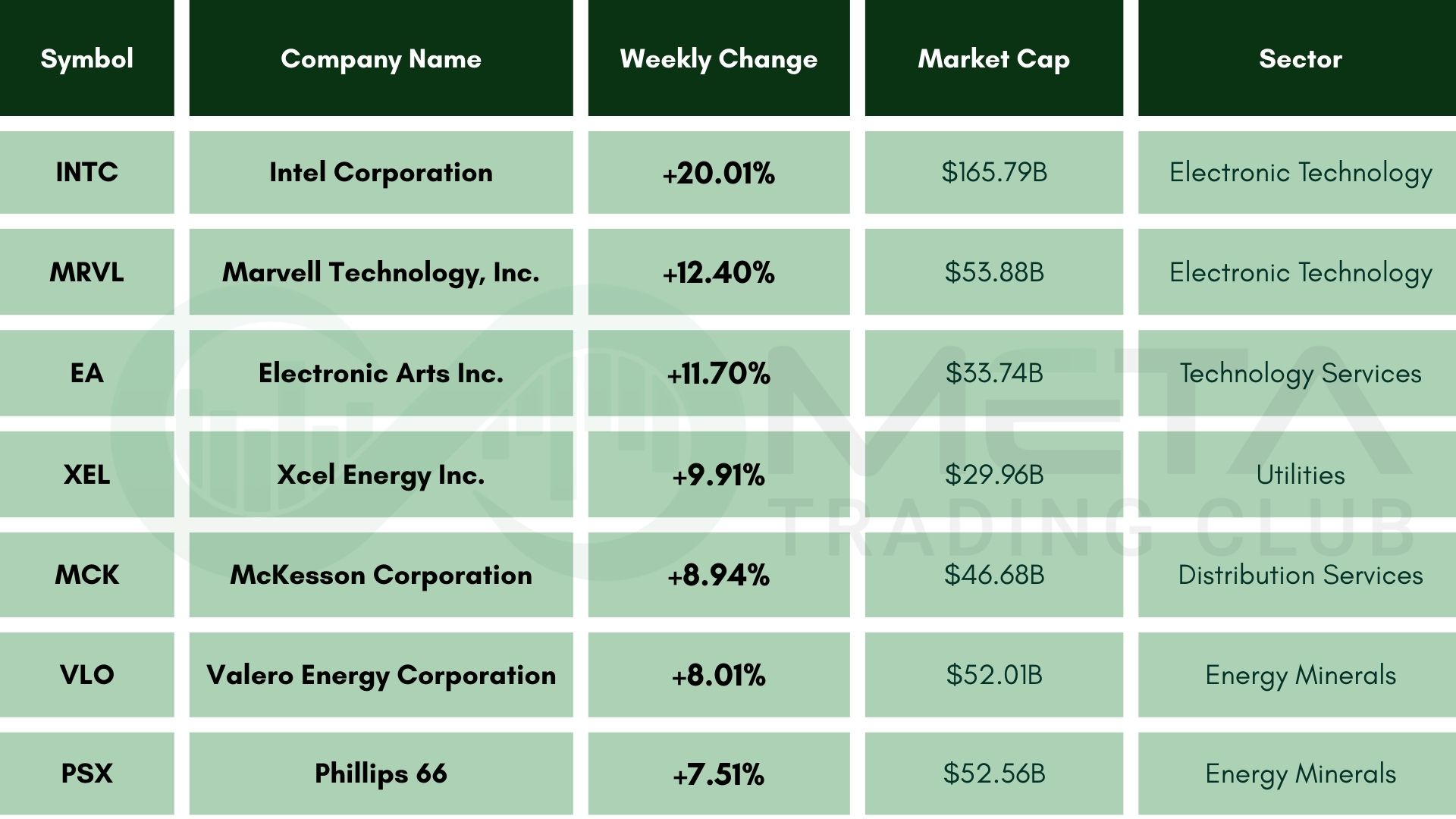

Top Performers

Last week saw a remarkable stock market performance, with several companies standing out as top gainers:

- Intel (INTC): Surged 20% after reports that Apple may invest in the company. The news follows recent funding from Nvidia, SoftBank, and the U.S. government.

- Marvell (MRVL): Gained 12.4% amid renewed optimism after $5B buyback plan and bullish sentiment on custom AI chips

- Electronic Arts (EA): Jumped 11.7% following reports of a potential $50B take-private deal led by Silver Lake and Saudi Arabia’s Public Investment Fund.

- Xcel Energy (XEL): Rose 9.9% after filing wildfire mitigation and net metering proposals, alongside quarterly rate adjustments.

- McKesson (MCK): Climbed 8.9% after raising its fiscal 2026 earnings forecast during Investor Day.

- Valero (VLO): Rallied 8% as oil prices rebounded. Russia’s fuel export cuts following infrastructure attacks in Ukraine tightened supply, lifting refining margins and energy stocks broadly.

- Phillips 66 (PSX): Gained 7%, driven by the macro energy catalysts, tightened supply, and rising crude prices, following geopolitical disruptions.

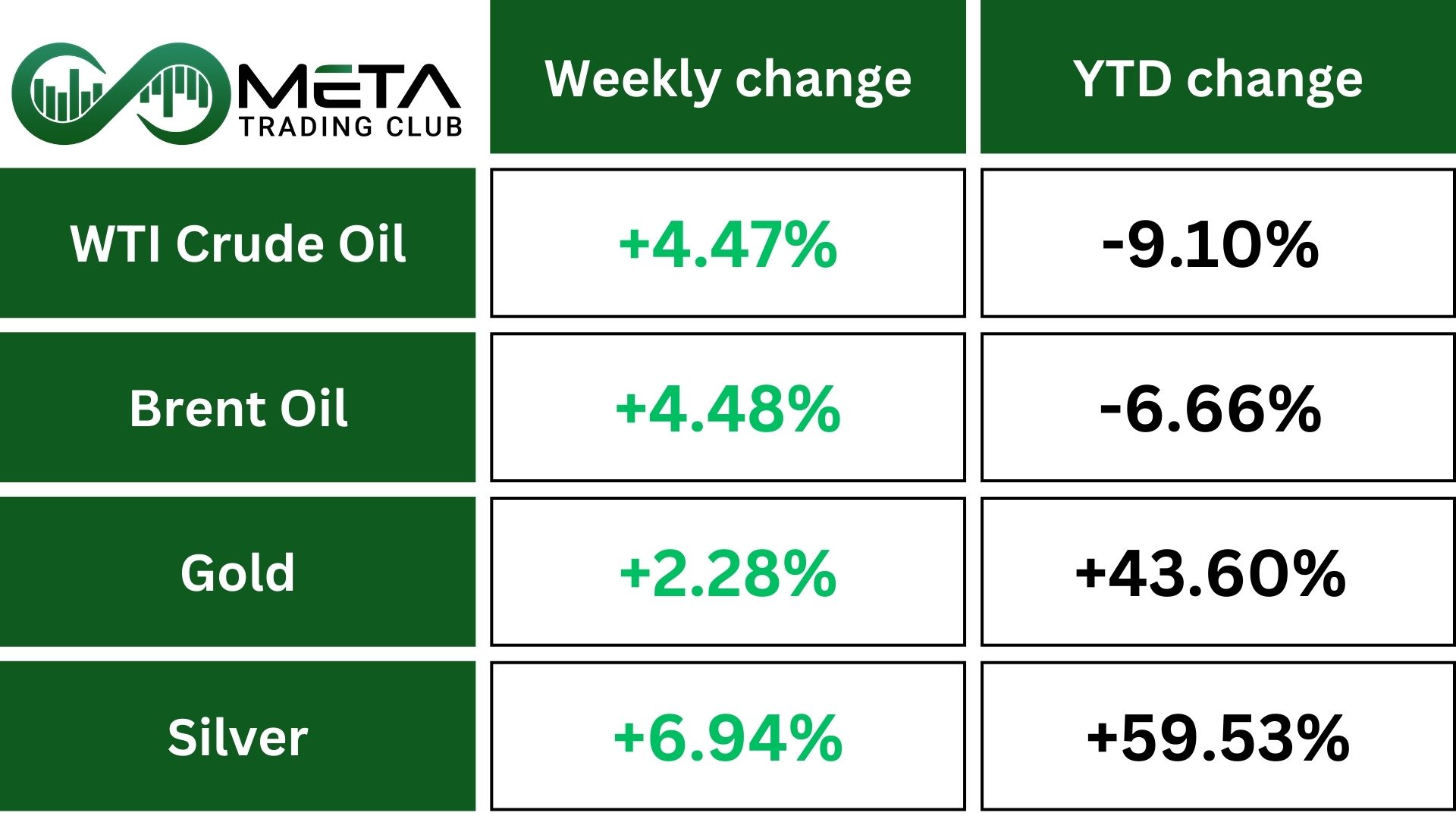

Commodity

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Gold

Gold stayed strong above $3,750 per ounce, close to its record high.

The metal set 2% weekly gain as investors sought safety despite rising Treasury yields and a stronger dollar.

Concerns grew after the U.S. announced new tariffs on medical goods and took a tougher stance on Russia, hinting Ukraine might regain lost territory.

Global buyers also turned to gold, worried about rising U.S. debt and risks to the Fed’s independence, with China’s central bank continuing to buy.

Silver

Silver ended the week up 6.9%, its biggest weekly gain since 2011.

Also, Silver climbed above $45 per ounce, reaching its highest level in 14 years. The jump came as investors expected lower real interest rates and faced limited physical supply, both of which boosted demand.

Industrial demand for silver is strong, mainly driven by solar panels, electric vehicles, and electronics. Total usage has passed 700 million ounces and keeps growing.

Supply isn’t keeping up because most silver comes as a byproduct from mining other metals like copper, lead, and zinc. In 2025, production rose slightly to about 844 million ounces, but it still couldn’t close the gap.

The Silver Institute expects a fifth straight year of shortage in 2025, with demand outpacing supply by over 100 million ounces, causing inventories to shrink.

Oil

Crude oil and gasoline prices jumped, their biggest weekly gain in over three months, up more than 4%.

The rise was driven by concerns over Russian supply as President Trump urged countries like Turkey and Hungary to stop buying Russian oil to pressure Russia over the war in Ukraine.

Tensions between Russia and NATO, along with Ukrainian attacks on Russian refineries and pipelines, further tightened global supply.

A weaker dollar and strong U.S. spending data also supported prices.

However, bearish factors include rising oil production in Iraq, lower demand from India, and more crude stored on tankers. OPEC+ plans a small production increase in October, continuing its gradual recovery from past cuts.

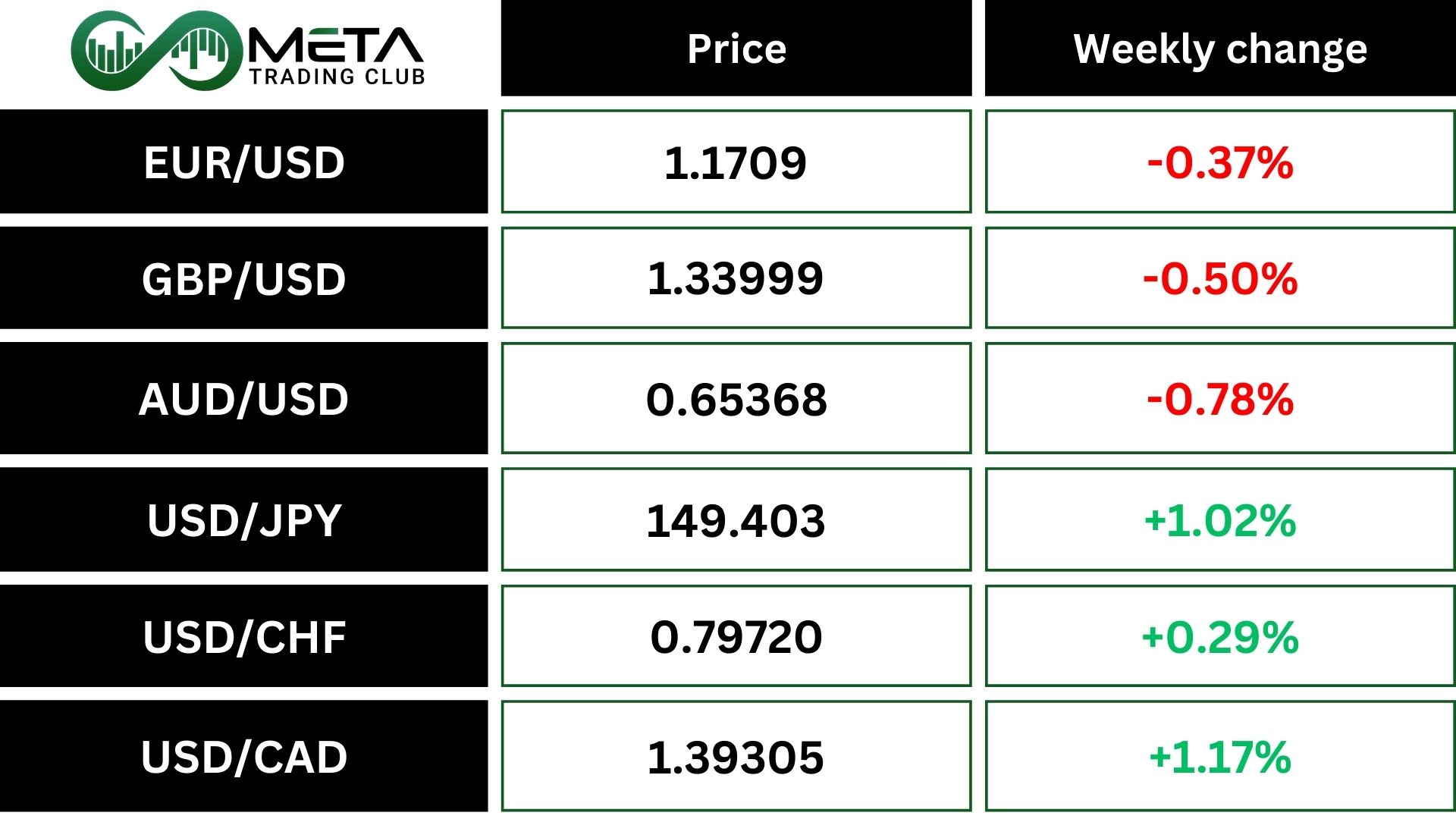

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The U.S. dollar is heading for its second straight week of gains, supported by strong economic data. Consumer spending rose more than expected in August, and inflation stayed steady, making investors less confident about upcoming interest rate cuts by the Federal Reserve.

The dollar gained against most major currencies, especially the Japanese yen, marking five weeks of upward movement. The euro and Swiss franc saw a slight loss against the dollar and were still weaker overall.

Fed officials gave mixed signals; some see room for rate cuts to protect jobs, while others believe inflation and unemployment risks are low. Traders now expect a smaller chance of a rate cut at the next Fed meeting.

Overall, the dollar remains strong due to solid U.S. growth, steady inflation, and cautious Fed policy.

Crypto

Bitcoin fell this week due to a combination of market, macroeconomic, and regulatory pressures.

Over $1.5 billion in leveraged long positions were wiped out starting September 21. Traders who bet on rising prices were forced to sell when Bitcoin dropped below key support levels, triggering a cascade of sell-offs across the market.

Institutional interest cooled off. Spot Bitcoin ETFs saw lower inflows, signaling reduced demand from big players. This weakened market confidence and added to the selling pressure.

Next Week’s Outlook

Economic Events

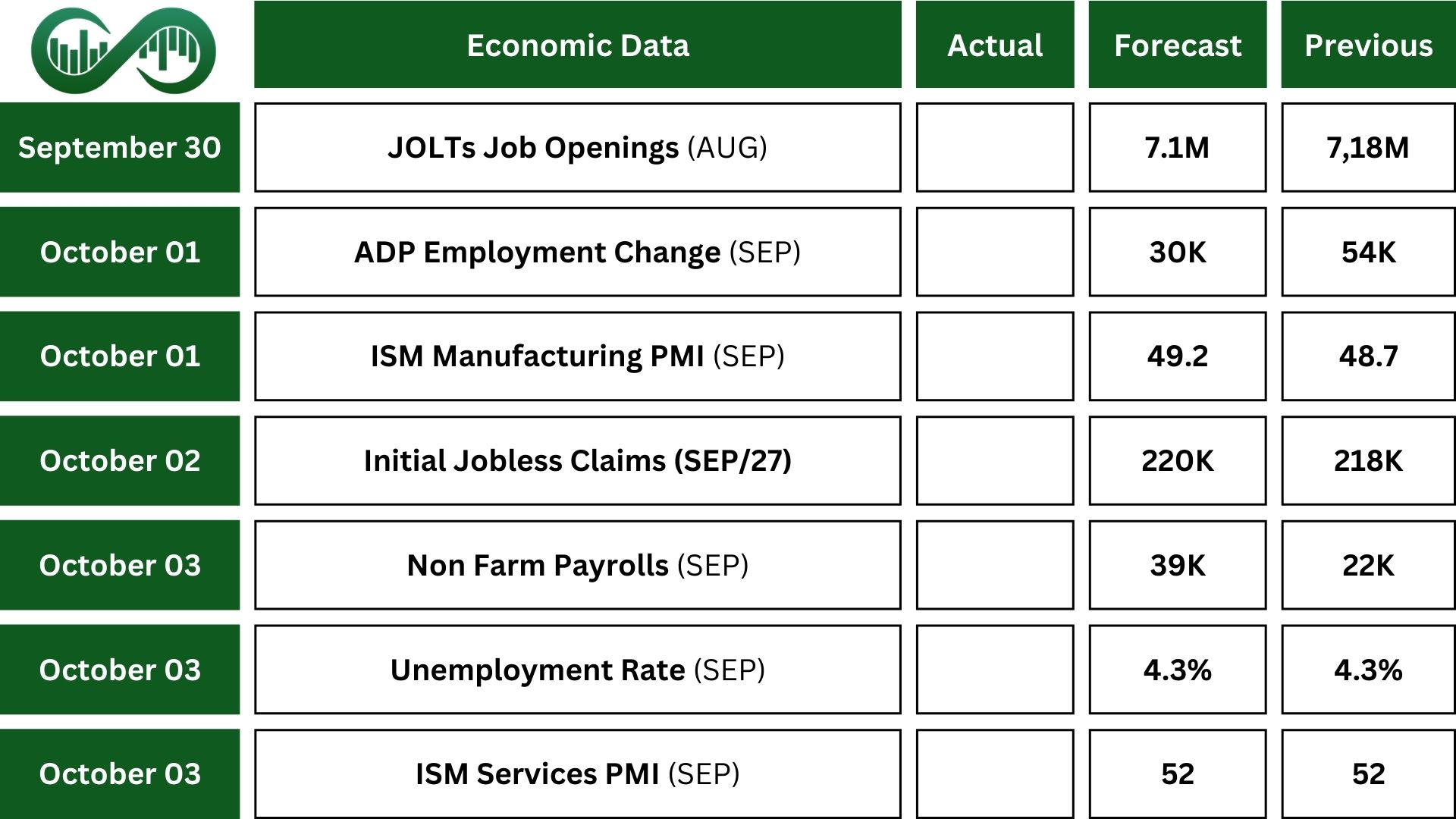

In the U.S., attention will center on fresh labor market data, following last month’s weaker-than-expected jobs report that sparked concerns about a faster slowdown.

September Non-Farm Payrolls are expected to rise by 39,000, an improvement from August’s 22,000, but still below earlier levels this year.

The Unemployment Rate is projected to stay at 4.3%, and average hourly earnings are likely to increase by 0.3%, matching the previous month.

Other key releases include JOLTS Job Openings, expected to dip to 7.1 million, the ADP report showing a modest gain of 30,000 private jobs (down from 54,000), and figures on job cuts.

Also, Manufacturing PMI is forecast to contract slightly less, while Services PMI should remain steady.

Markets will also track updates on consumer confidence, factory orders, home prices, construction spending, and regional Fed surveys.

Meanwhile, Investors will be watching comments from Federal Reserve officials for policy clues, along with developments in government funding talks ahead of a possible shutdown on October 1.

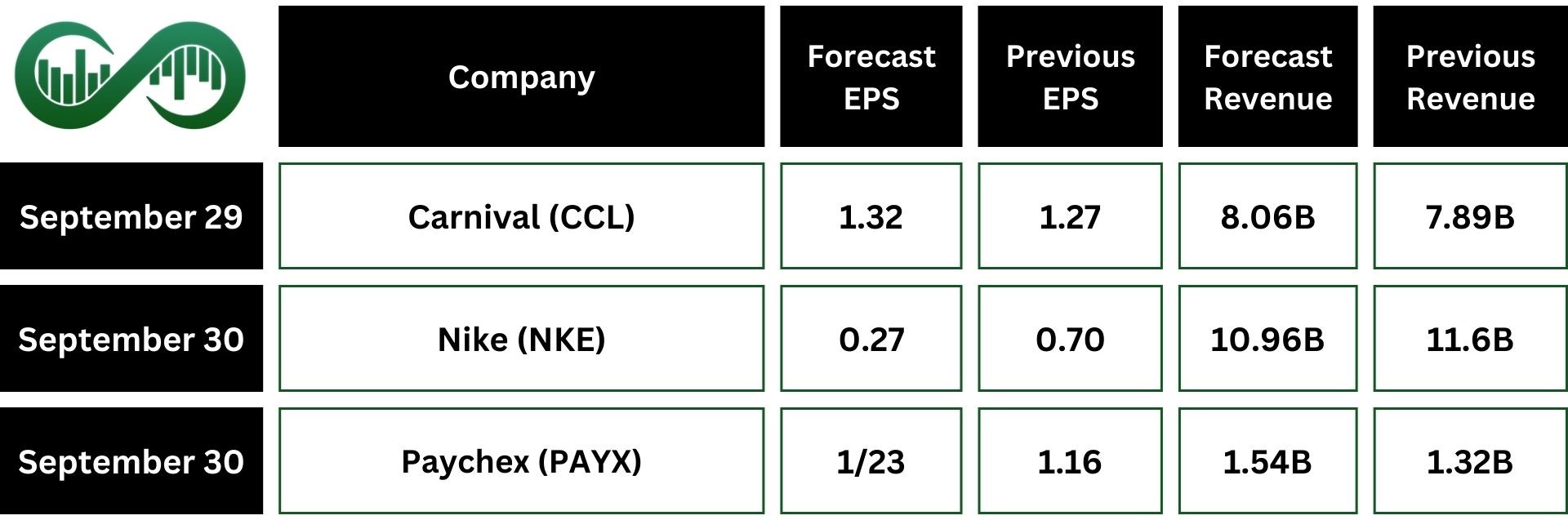

Earnings Events

This week’s earnings calendar includes key updates from Nike (NKE).