Last Week’s report

Economic Reports

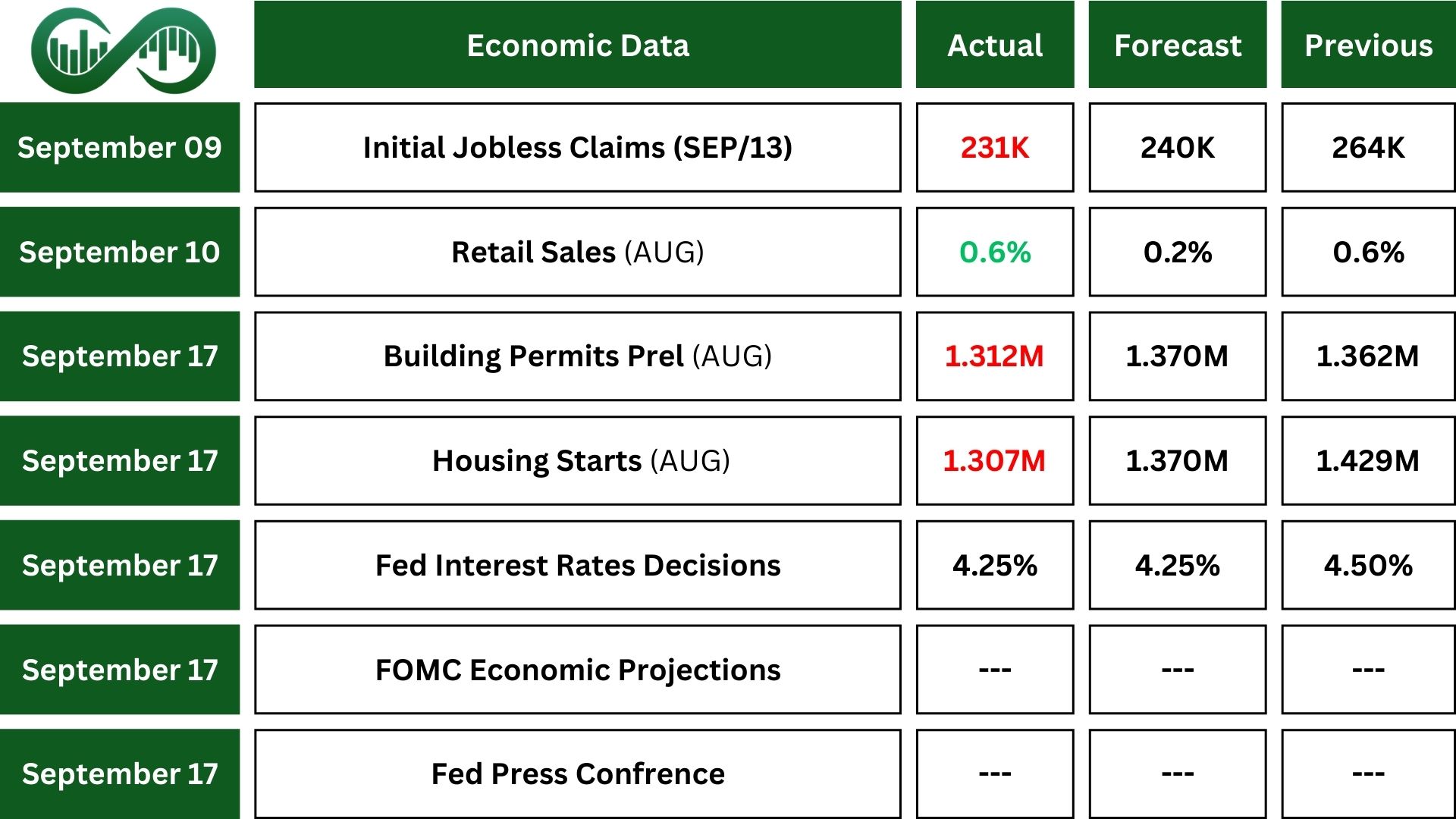

Retail Sales in the US rose by 0.6% in August, beating forecasts of just a 0.2% increase. This steady growth signals strong consumer demand heading into the fall.

Importantly, core retail sales jumped 0.7%. That’s stronger than both the previous month’s 0.5% gain and the expected 0.4%, suggesting solid momentum in consumer spending.

US housing starts fell sharply in August, dropping 8.5% from the previous month to an annual rate of 1.307 million units. That was well below market expectations of 1.37 million. This marks the fourth-lowest level since May 2020, highlighting ongoing weakness in the housing sector.

The decline reflects several challenges, including a large number of unsold new homes and a cooling labor market, which have outweighed the benefits of lower mortgage rates.

The Federal Reserve cut the federal funds rate by 25 basis points in September, bringing it down to a range of 4.00%–4.25%. This move was widely expected and marks the first rate cut since December. Interestingly, newly appointed Governor Stephen Miran voted against the decision, preferring a larger 50bps cut.

Alongside the rate change, the Fed released updated economic forecasts. Officials now expect to lower rates by another 50bps before the end of 2025, and by 25bps in 2026, slightly more than they projected back in June.

Growth expectations have improved: GDP is now forecast to grow 1.6% in 2025 (up from 1.4%).

Inflation projections were mixed. The headline PCE inflation rate remains at 3% for 2025, unchanged from June, but the 2026 forecast was raised to 2.6% from 2.4%. Core PCE inflation is still expected to be 3.1% in 2025, while the 2026 estimate was also revised up to 2.6% from 2.4%.

The unemployment rate forecast for 2025 remains at 4.5%, but the outlook for 2026 was slightly improved to 4.4% from 4.5%.

Earnings Reports

FedEx

FedEx (FDX) reported strong fiscal Q1 2026 results. Adjusted earnings of $3.83 per share and $22.24 billion in revenue, both beating expectations.

Operating performance improved thanks to solid U.S. domestic package growth and cost-cutting efforts, though a $16 million tax expense and rising labor costs weighed on results.

The company repurchased $0.5 billion in shares and held $6.2 billion in cash. Looking ahead, FedEx expects 4%–6% revenue growth and EPS growth, supported by $1 billion in cost savings and $4.5 billion in capital investments.

The spin-off of FedEx Freight is on track for June 2026.

Indices

Indices’ Weekly Performance:

Major US stock indexes posted solid gains last week, lifted by growing optimism over potential interest rate cuts from the Federal Reserve.

The S&P 500 rose 1.2%, marking its third straight weekly advance and reaching a new all-time closing high. The Dow added 1.1%, while the Nasdaq surged 2.2%, also hitting a record close.

Meanwhile, the small-cap Russell 2000 climbed 2.2%, achieving its first record-high finish since 2021, fueled by renewed rate-cut hopes.

In stocks, Nvidia announced a $5 billion investment in Intel, acquiring a 4% stake by purchasing common stock at $23.28 per share. The move signals a strategic partnership to co-develop custom chips for data centers and PCs.

The market responded strongly: Intel shares surged over 30%, and Nvidia rose, reflecting investor confidence in Intel’s turnaround and Nvidia’s broader manufacturing strategy.

Stocks

Sector’s Weekly Performance:

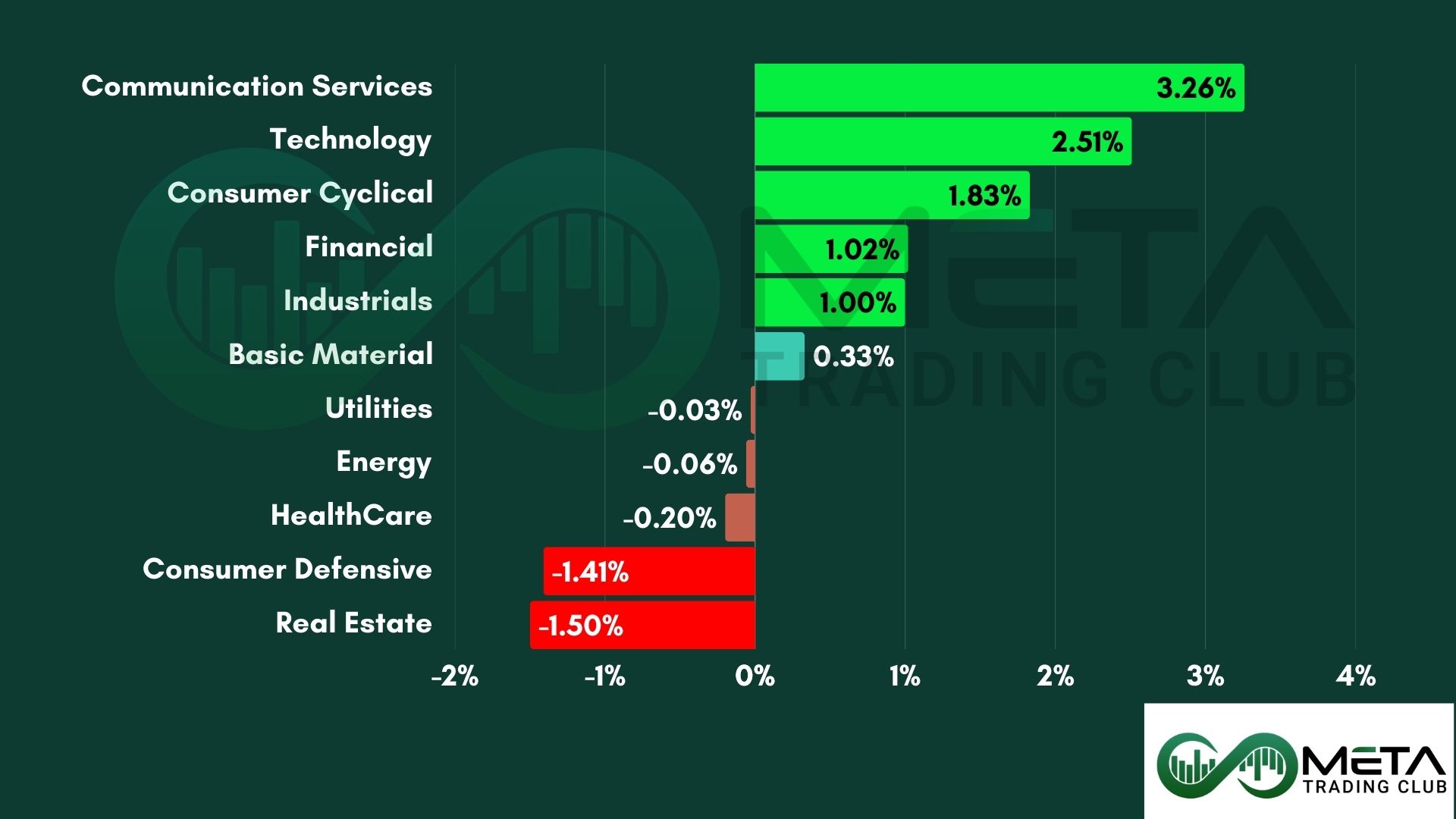

Only a few sectors saw strong gains last week, mainly Communication Services and Technology, while defensive stocks and bond-like sectors lagged.

- Communication Services jumped 3.2%, led by Alphabet (Google’s parent) which hit a $3 trillion market cap as excitement around AI continues to grow.

- Technology rose 2.5%. Intel surged 23% after Nvidia announced a $5 billion investment, sparking a rally in chip stocks, though AMD lost ground. The semiconductor index (SOX) climbed nearly 4%. Workday also gained after Elliott Management invested over $2 billion and backed its leadership.

- Consumer Discretionary was up 1.8%. Tesla rose after Elon Musk bought $1 billion worth of stock, signaling confidence in the company’s future.

- Industrials gained 1%. FedEx rose after posting strong Q1 earnings, helped by domestic deliveries and cost cuts. Uber slipped after Lyft announced a partnership with Alphabet’s Waymo to launch self-driving ride services in 2026.

- Financials edged up 1%, but FactSet dropped 20% after issuing a disappointing profit forecast.

- Materials slightly increase. Corteva declined after reports it may split its seeds and pesticide businesses, raising concerns about value dilution.

Top Performers

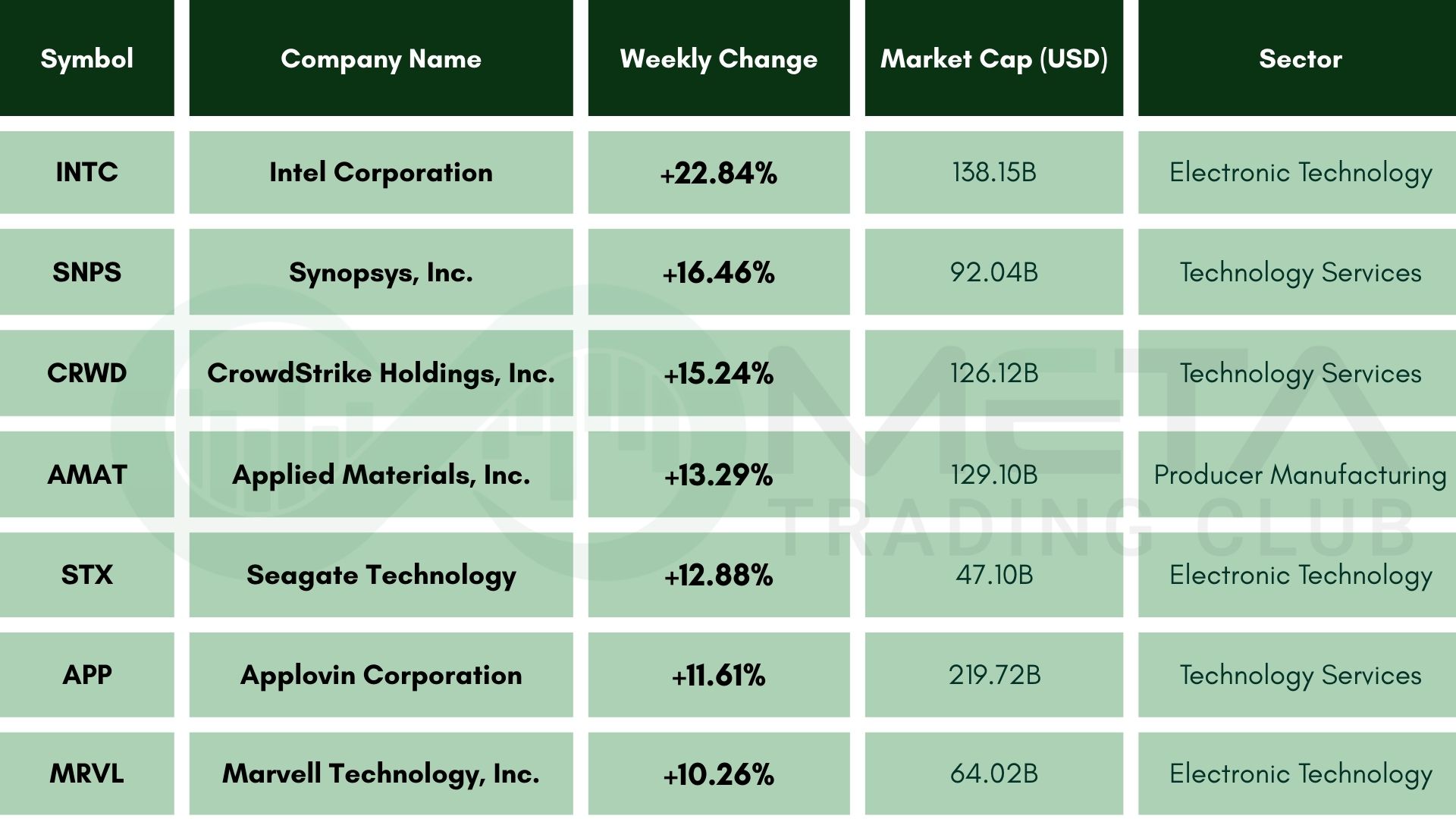

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- Intel (INTC): Surged 22.84% after Nvidia announced a $5 billion investment, acquiring a 4% stake at $23.28 per share.

- Synopsys (SNPS): Jumped 16.46% following strong demand for its chip design software and growing momentum in AI-driven semiconductor development.

- CrowdStrike (CRWD): Gained 15.24% as cybersecurity remains a top priority for enterprises.

- Applied Materials (AMAT): thanks to upbeat guidance and continued strength in semiconductor equipment sales.

- Seagate Technology (STX): Advanced 12.88% amid improving sentiment around data storage demand and cost-efficiency gains..

- Applovin (APP): Climbed 11.61% on strong ad tech performance and growing mobile app monetization.

- Marvell Technology (MRVL): Added 10.26% as investors welcomed its exposure to AI infrastructure and data center networking.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

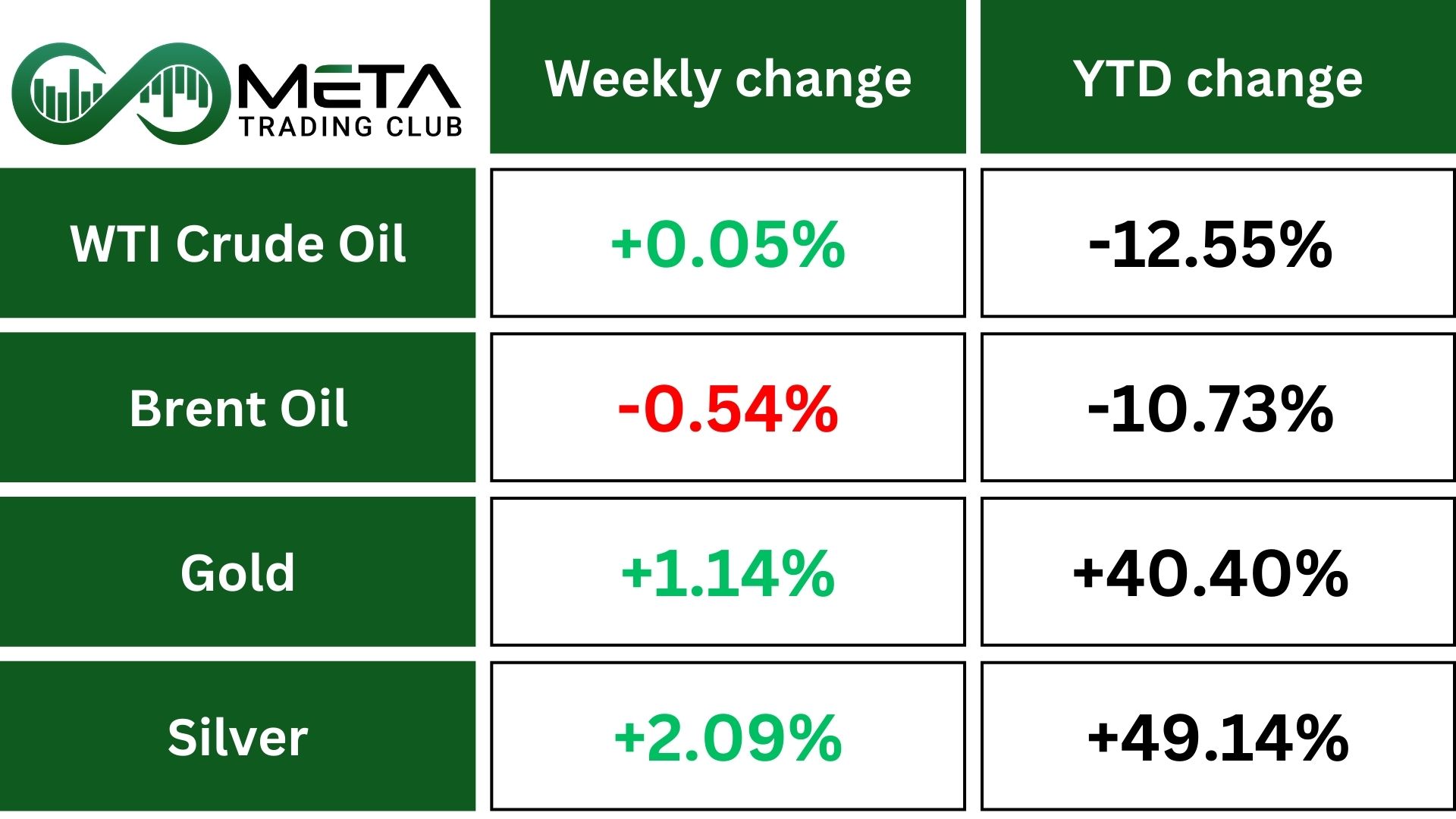

Gold (XAU/USD) remains up about 40% in 2025, supported by expectations of Fed easing, geopolitical tensions, and strong central bank buying.

Notably, Swiss gold exports to China surged 254% in August, highlighting robust international demand.

Silver surged 44% in 2025, reaching their highest level since 2011, driven by investor demand amid global trade shifts, a weaker U.S. dollar, and concerns over Federal Reserve independence.

While gold is also on track for its best year since 1979, silver may still be undervalued. The gold-to-silver ratio, currently around 90, suggests silver is relatively cheap compared to historical averages of 63 (50-year) and 70 (20-year). Silver’s role in semiconductors adds to its appeal, and as gold prices rise, more retail investors are turning to silver.

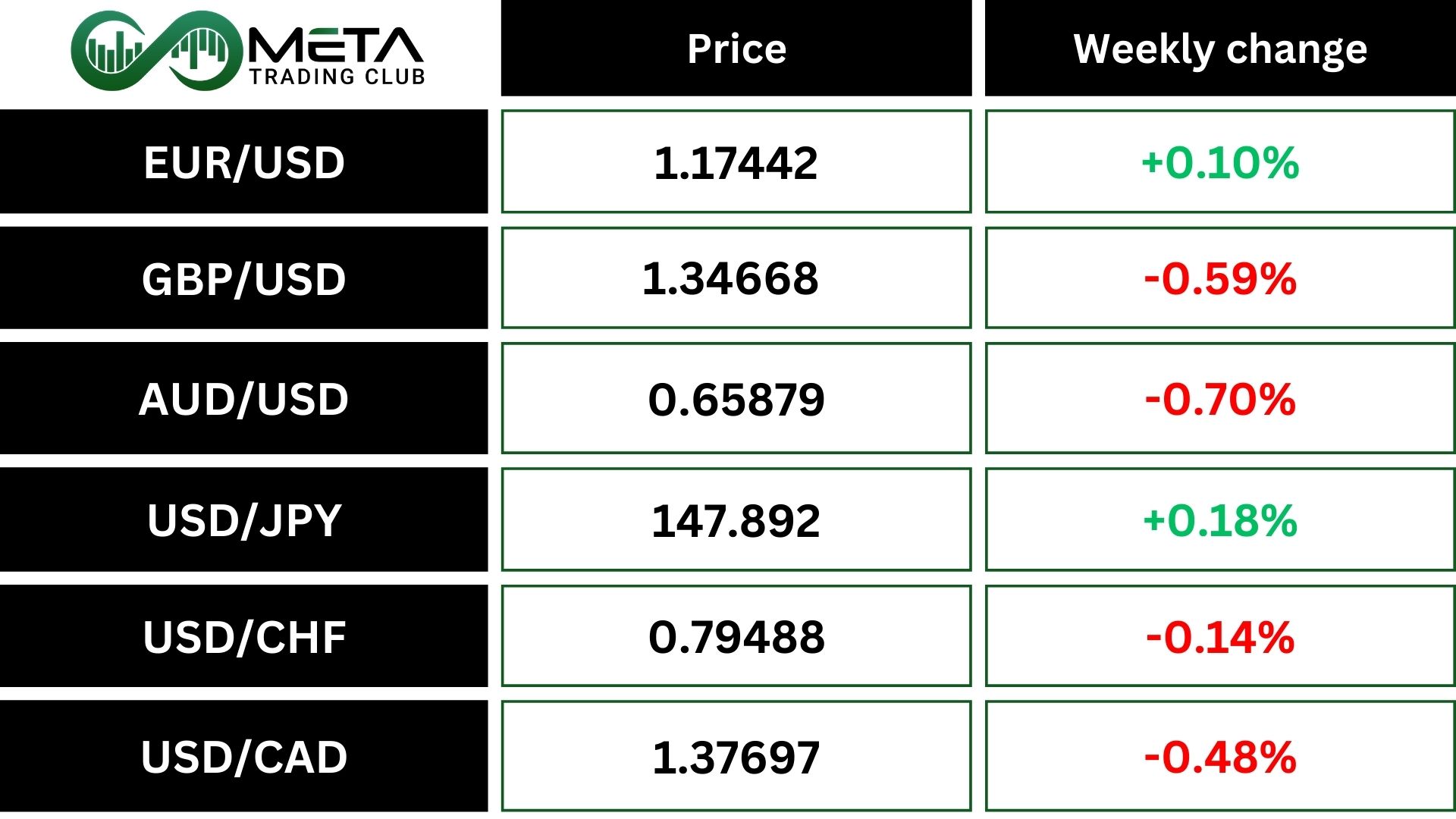

Forex

Weekly Performance of Major Foreign Exchange Pairs:

Dollar Index: The U.S. dollar recovered some ground after falling 1% earlier in the week. The initial drop came as markets anticipated aggressive rate cuts from the Federal Reserve.

However, Wednesday’s Fed decision delivered only a single rate cut and signaled a cautious approach going forward.

With the dollar under pressure before the Fed announcement, analysts now see room for a short-term rebound, viewing the recent move as temporary rather than a lasting trend.

USD/JPY: The Bank of Japan (BOJ) held its benchmark interest rate steady at 0.5%, triggering an initial surge in the yen. However, the currency later gave up gains, leaving the dollar slightly lower at 147.89 yen. BOJ Governor Kazuo Ueda signaled that further rate hikes are possible if the bank’s economic and inflation forecasts hold up, reinforcing a cautious but potentially hawkish stance.

GBP/USD: The British pound fell 0.6% to $1.3466, marking its steepest two-day drop since late July. The decline came after UK government borrowing exceeded official forecasts, raising concerns about the country’s fiscal stability.

Crypto

Bitcoin (BTC) remains in focus, with analysts seeing moderate risk but strong upside potential.

Active wallets have earned 3.5% over the past month and 16.1% over the past year, with some forecasts pointing to a path toward $120,000.

Social media buzz around the FOMC meeting surged to levels not seen since April, reflecting heightened trader attention to the Fed’s first rate cut in nearly two years.

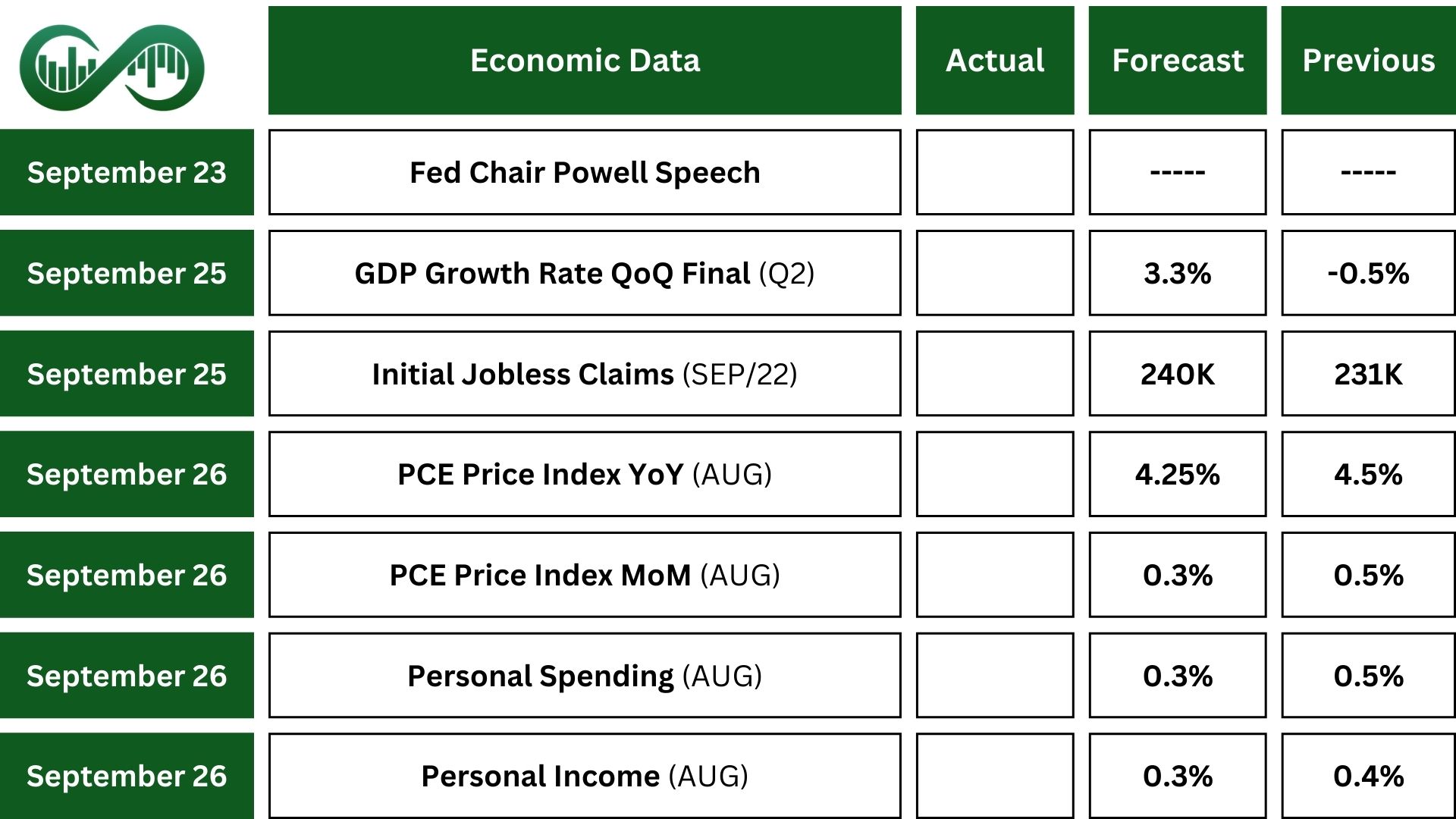

Next Week’s Outlook

Economic Events

This will be a busy week on economic data, with we’ll closely watch both policy signals and fresh data releases.

In the US, attention is on upcoming speeches by Federal Reserve officials to get a better sense of future interest rate decisions. One of the most anticipated events is Fed Chair Jerome Powell’s appearance at the Greater Providence Chamber of Commerce in 2025, which could offer important clues about the central bank’s policy direction for the rest of the year.

On the economic data front, several key reports are expected. These include Personal Income and Personal Spending figures. Also, the Fed’s preferred inflation measure, the PCE Price Index will come out. Economists predict that consumer spending will rise by 0.5% and personal income by 0.3% in August, marking the third consecutive month of growth.

Durable Goods Orders are projected to decline by 0.4%, a smaller drop compared to the previous two months. Meanwhile, the S&P Global flash PMI survey is likely to show a slowdown in private-sector activity for September, reflecting weaker business conditions.

Other important data releases include the final estimate of second-quarter GDP, the US current account balance, the Chicago Fed National Activity Index, advance trade figures for goods, wholesale inventories, and the University of Michigan’s final reading on consumer sentiment.

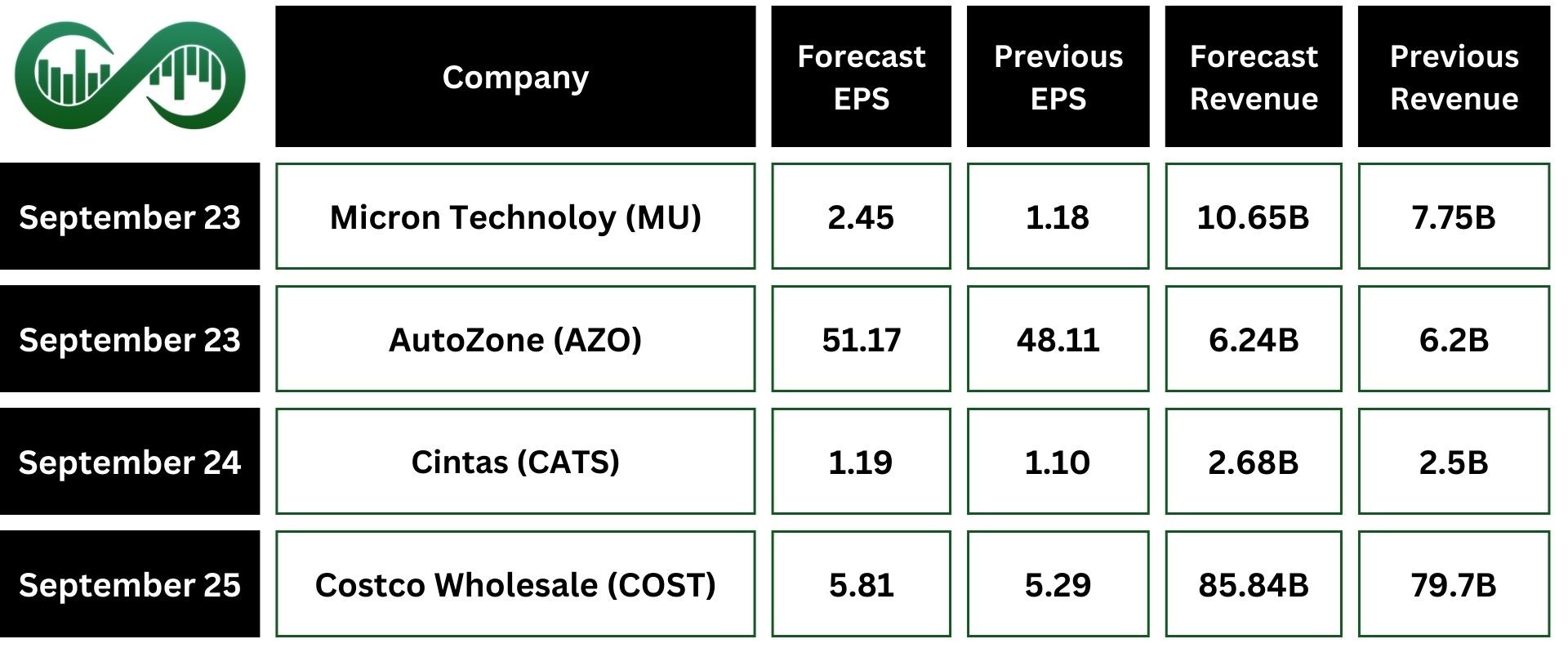

Earnings Events

This week’s earnings calendar includes key updates from Micron Technology (MU) and Costco Wholesale (COST).