Last Week’s report

Economic Reports

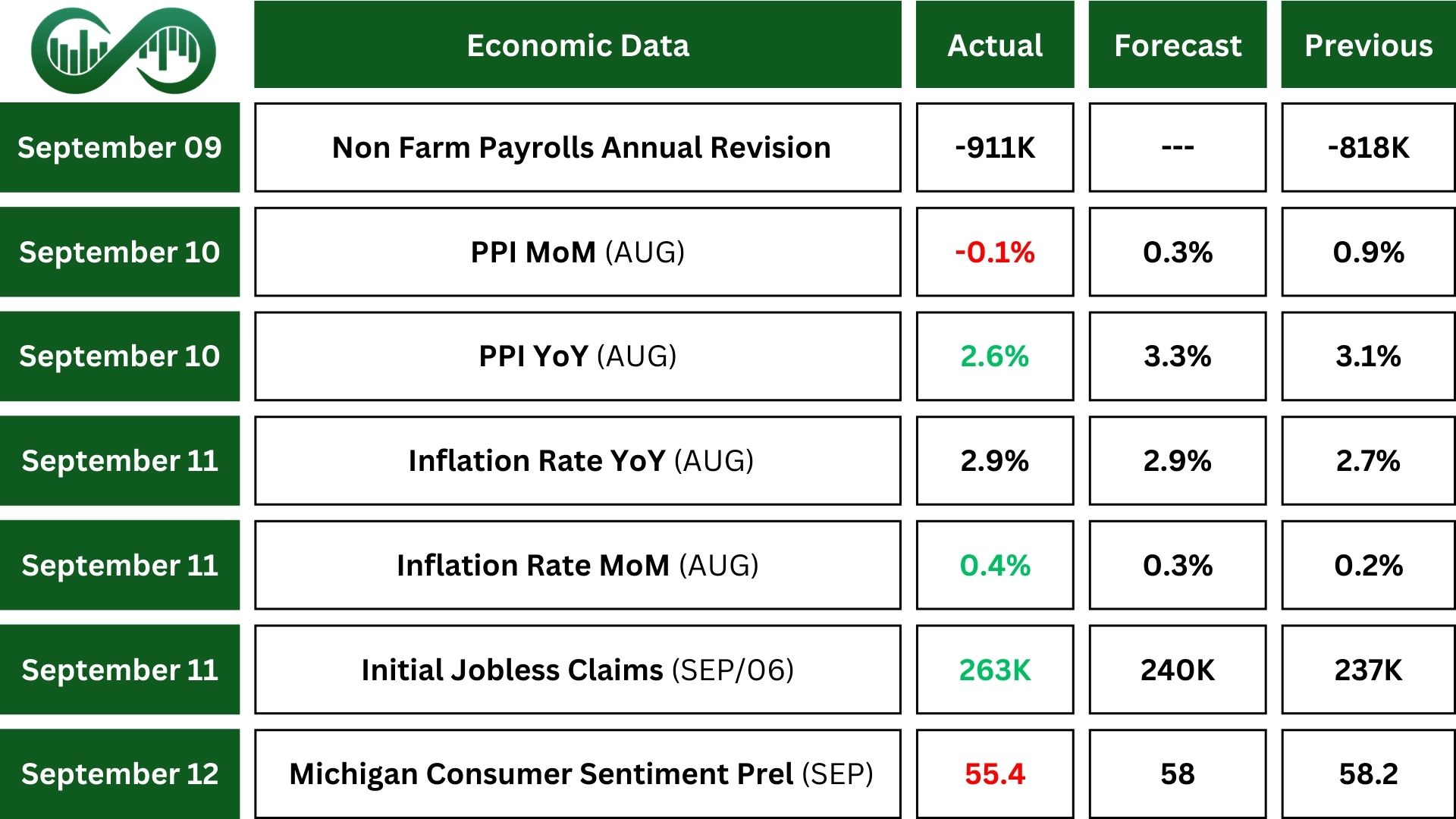

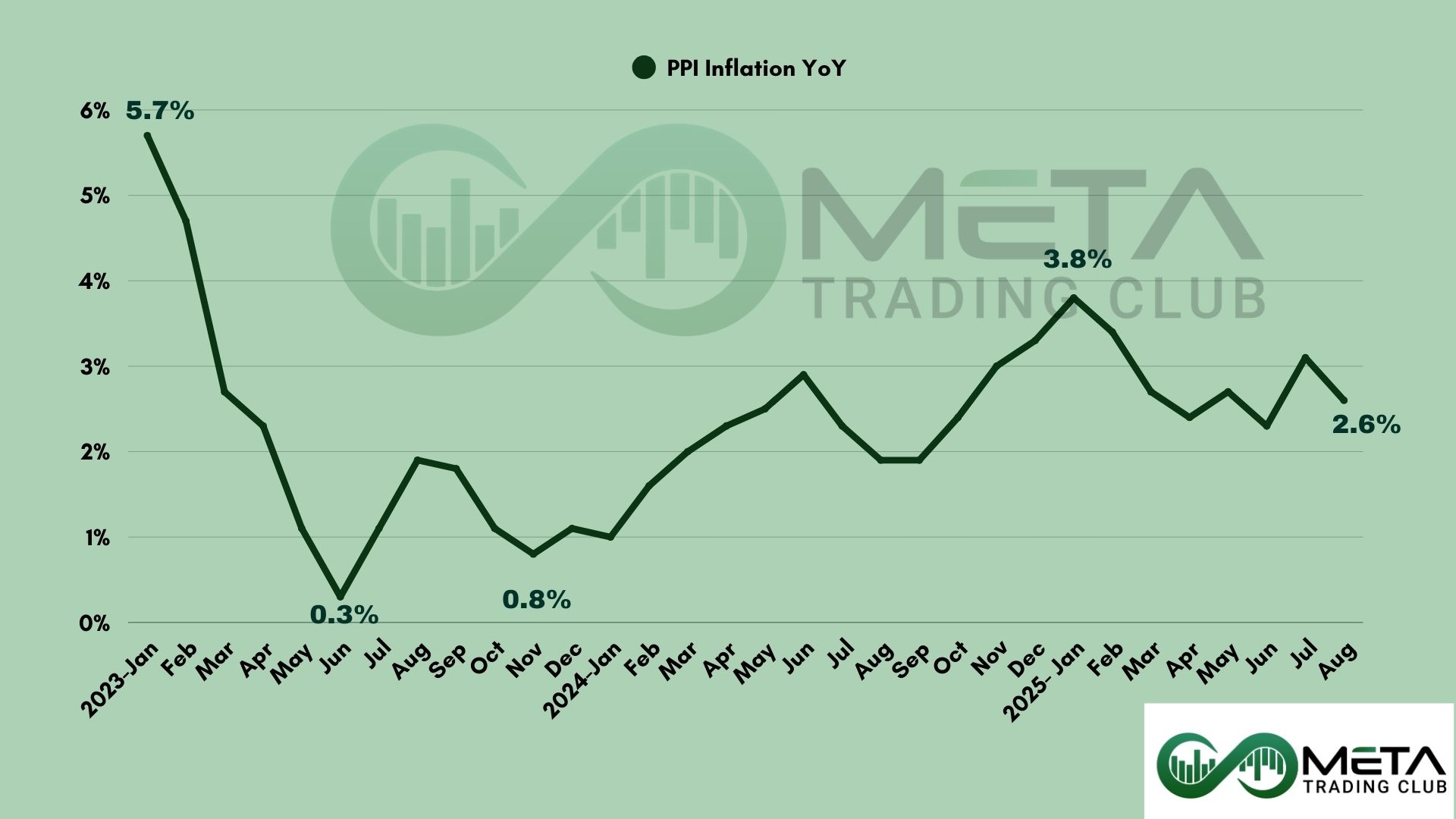

US Producer Prices (PPI) fell by 0.1% in August 2025, marking the first monthly decline in four months and coming in well below expectations. The drop was mainly driven by a sharp decrease in service costs. In contrast, goods prices edged up slightly. On a yearly basis, producer prices rose 2.6%, down from July’s revised 3.1%, while core prices also dipped more than expected.

Consumer Prices Index (CPI) in the US rose by 0.4% in August, marking the largest monthly increase since January and surpassing market expectation. The acceleration has sparked concerns that trade policies may be contributing to rising household costs. Also, core inflation, which excludes food and energy, rose 0.3% for the month, consistent with July’s pace and in line with forecasts.

US initial jobless claims rose sharply in early September, jumping by 27,000 to 263,000—the highest level since October 2021 and well above forecasts. This increase supports recent signs of a weakening labor market. The four-week average also climbed significantly, showing the biggest weekly rise since late 2020. Texas saw a notable spike in claims, while ongoing unemployment claims stayed just below expectations but remained elevated compared to recent years.

US Consumer Sentiment fell to 55.4 in September, its lowest since May and below expectations. While buying conditions for durable goods improved, concerns about inflation, jobs, and the economy dragged down other measures. Views on personal finances dropped by 8%, and tariffs remained a major worry for many.

The current conditions index slipped slightly, and future expectations fell more sharply. Inflation expectations for the next year stayed at 4.8%, while five-year outlooks rose to 3.9%.

Earnings Reports

Oracle

Oracle (ORCL) delivered a standout Q1 FY26 report, with revenue rising 12% to $14.9 billion and cloud services jumping 28% to $7.2 billion.

The company’s contract backlog soared 359% to $455 billion, signaling massive growth in future business.

Shares surged 31% as investors cheered Oracle’s aggressive cloud and AI strategy.

The company now forecasts cloud revenue to grow from $18 billion to $144 billion over four years, boosted by its upcoming AI database and expanding partnerships with Amazon, Google, and Microsoft.

Adobe

Adobe (ADBE) delivered a strong Q3 earnings report, beating expectations with $5.99 billion in revenue, up 11% year-over-year, and adjusted earnings of $5.31 per share. Solid profits and cash flow supported a raised full-year outlook.

AI-driven growth played a key role, with AI-influenced ARR surpassing $5 billion and AI-first ARR exceeding its $250 million target.

Adobe expects Q4 revenue around $6.1 billion, with full-year revenue projected up to $23.70 billion. EPS guidance expected $20.8 (non-GAAP), signaling continued momentum across its subscription-based business.

Indices

Indices’ Weekly Performance:

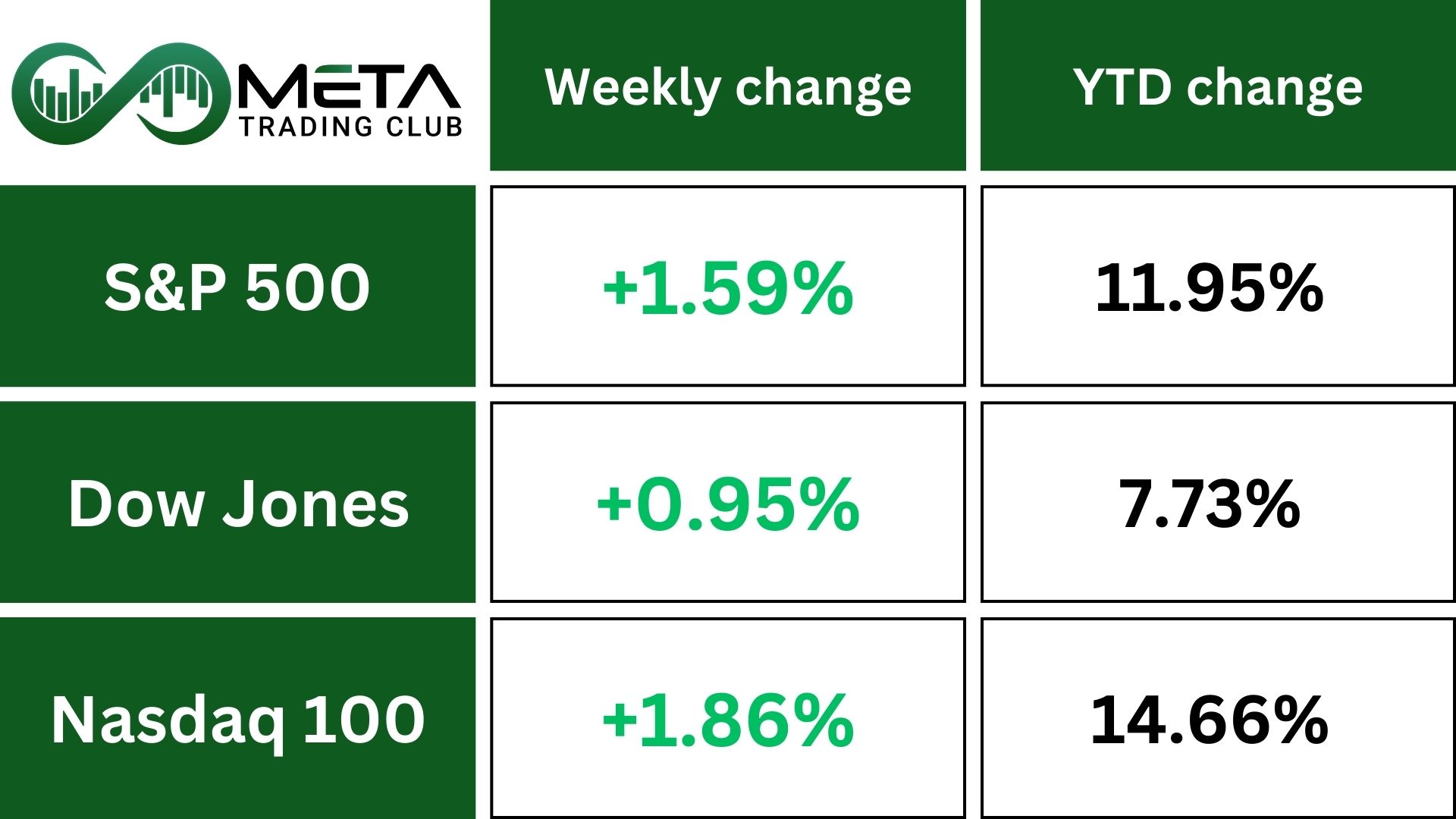

For the week, the S&P 500 rose 1.6%, its best week since early August. The Nasdaq gained 2%, and the Dow was up 1.1%, marking its first weekly increase in three weeks. All three major stock indexes reached new highs, with the Nasdaq setting a record at the end of each trading day.

Investors reacted to weaker job numbers and low inflation, which they see as signs that the Federal Reserve might lower interest rates next week. Most traders expect the Fed to cut rates by 0.25% at its meeting on September 17, though there’s a small chance of a bigger 0.5% cut based on current economic data.

Technology and consumer-focused stocks did well, while materials and health care stocks fell behind.

Stocks

Sector’s Weekly Performance:

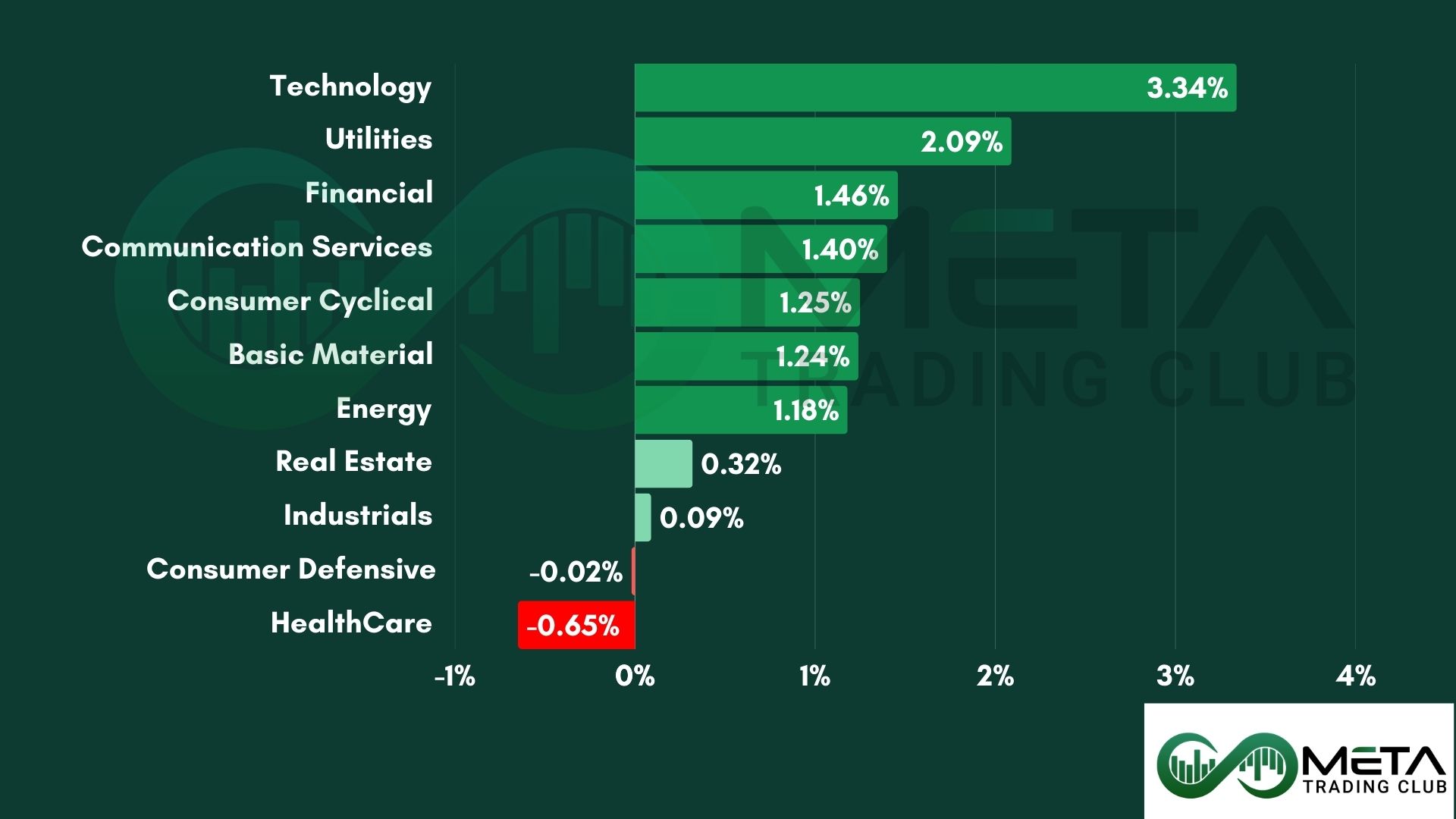

Most sectors moved higher, with Technology and Utilities leading the gains, while Healthcare saw a slight dip.

- Tech stocks rallied 3.3%, driven by Oracle’s nearly 26% surge to a record high on strong AI cloud momentum, which also boosted chipmakers. The semiconductor index jumped about 4% to an all-time high. However, Synopsys dropped 29% after disappointing quarterly results, and Apple edged lower after keeping prices steady on new products.

- Utilities rose 2%, helped by gains in data center power suppliers like Vistra and Constellation Energy, also lifted by Oracle’s performance.

- Communication Services added 1.4%, with Warner Bros Discovery soaring 56% for the week and Paramount Skydance climbing on reports of a possible bid. In contrast, Fox and News Corp declined following a succession announcement from the Murdoch family.

- Healthcare fell 0.65%, though vaccine makers Moderna and Pfizer fell after reports linking COVID shots to child deaths. Also, Fintech firm Klarna jumped after its IPO priced above range, capping the busiest week for new listings in over four years.

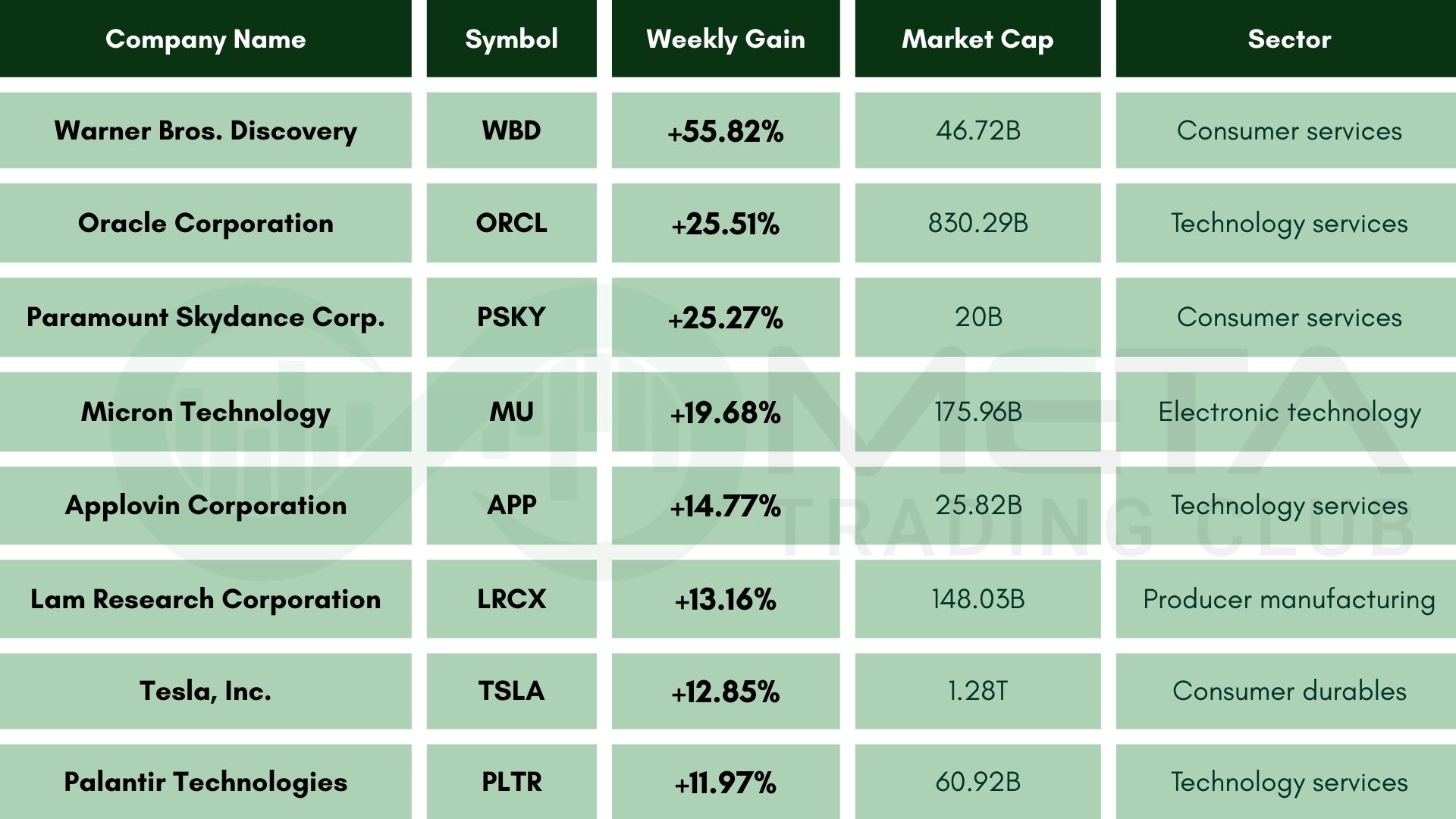

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- Warner Bros. Discovery (WBD): Surged 55.82% on the week amid takeover speculation and renewed interest in its streaming assets.

- Oracle (ORCL): Surged 25.51% announced massive growth in its cloud business in its earnings report.

- Paramount Skydance (PSKY): Surged 25.27% after reports of a potential bid to acquire Warner Bros Discovery, sparking investor excitement.

- Micron Technology (MU): Surged 19.68% due to optimism around AI-driven demand for memory chips and favorable earnings guidance.

- Applovin (APP): Surged 14.77% due to its upcoming inclusion in the S&P 500 index, which is set to take effect on September 22.

- Lam Research (LRCX): Surged 13.16% due to increased semiconductor equipment orders and sector-wide momentum.

- Tesla (TSLA): Surged 12.85% as expected to beat Q3 delivery forecasts as buyers rush to secure EV tax credits before they expire.

- Palantir Technologies (PLTR): Surged 11.97% due to its AI capabilities and a strategic partnership with Oracle.

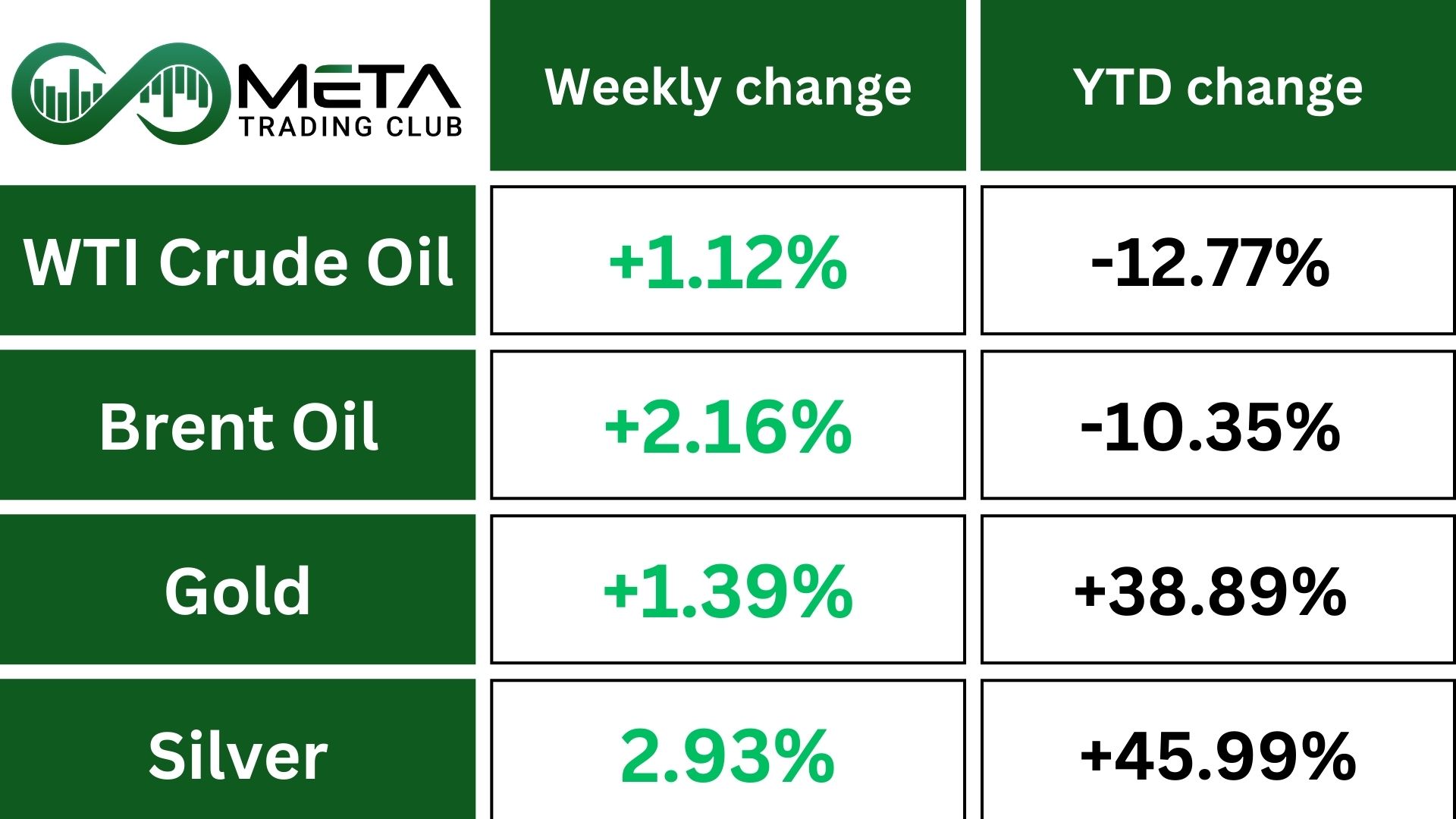

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold (XAU/USD) gained 1.5% for the week, staying near record highs as investors reacted to U.S. economic data that supports possible rate cuts.

Rising global tensions, including President Trump urging EU tariffs on China and India, escalating Middle East conflict, and Russian drones entering Polish airspace, also boosted gold’s appeal as a safe-haven asset.

Silver climbed 2.95% last week as investors sought safe-haven assets amid rising global uncertainty and inflation concerns. The rally was fueled by strong demand from both industrial and investment sectors, ongoing supply deficits, and support from a weaker dollar and falling bond yields—all of which made precious metals more attractive.

WTI Crude Oil prices surged by up to 2.6%, as anticipated US sanctions on Russian crude failed to materialize. Despite ongoing Ukrainian drone attacks that raised fears of supply disruptions, traders scaled back bullish positions heading into the weekend.

In response, the US floated the idea of urging G-7 nations to impose tariffs as high as 100% on Russian oil sold to China and India. Canada also moved to convene a meeting of finance ministers to explore further punitive measures.

However, the absence of immediate sanctions dampened market momentum. Additional downward pressure came from the International Energy Agency’s forecast of a record oil surplus in the coming year. Meanwhile, OPEC+ confirmed plans to gradually reintroduce idled barrels starting in October, though at a moderated pace.

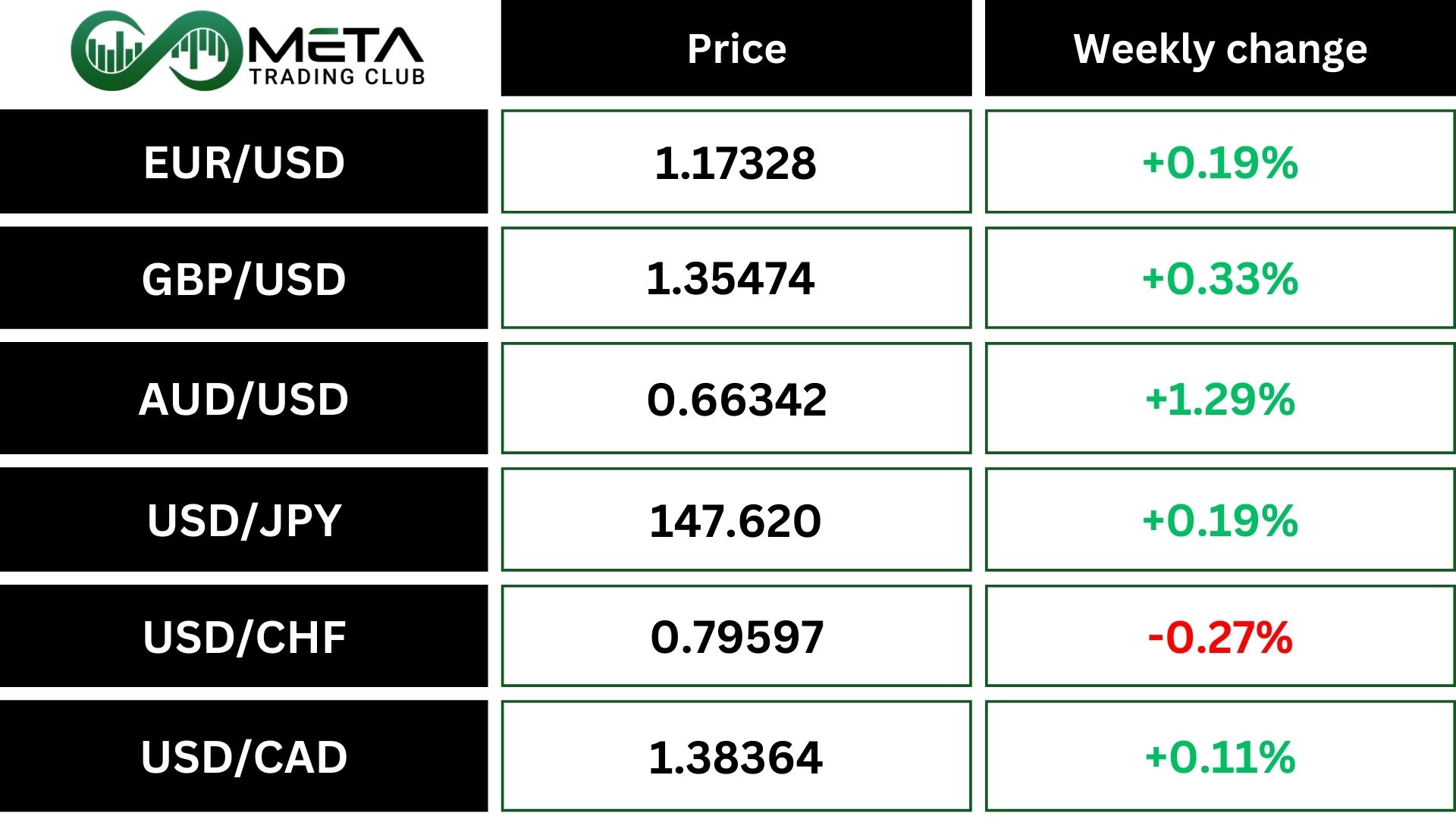

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The U.S. Dollar Index (DXY) is on pace to notch a 0.1% weekly decline, marking its second straight week in the red. This modest drop reflects growing expectations for a Federal Reserve rate cut, softening labor market data, and mixed inflation signals. Despite a brief rebound midweek, DXY remains below key technical levels, reinforcing a short-term bearish outlook.

EUR/USD edged up 0.19% last week, supported by softening U.S. dollar momentum and growing expectations for a Federal Reserve rate cut. The euro benefited from stable Eurozone inflation and cautious ECB policy signals, while geopolitical tensions and mixed U.S. data kept dollar bulls in check.

AUD/USD rose 1.29% last week, marking one of its strongest weekly performances in recent months. The Australian dollar gained momentum as the Bank of Australia may hold rates steady while the Federal Reserve leans toward cuts. The pair climbed to a multi-week high near 0.6647, supported by risk-on sentiment and a softer U.S. dollar backdrop.

USD/CHF fell 0.27% last week as the Swiss franc strengthened on safe-haven currency demand and growing geopolitical tensions. Investors favored the franc amid rising instability in Europe and Asia, while expectations for a Federal Reserve rate cut weighed on the U.S. dollar. The pair dipped toward 0.796, marking its second consecutive weekly decline.

Crypto

Bitcoin’s recovery this month began after dipping to a multi-week low of just over $107,000. Bulls defended that level and pushed BTC past $110,000, eventually testing $113,000 twice before breaking through on September 10.

The rally peaked at $116,700 over the weekend, but momentum stalled, and BTC now hovers just below $116,000. Despite macroeconomic tensions involving the U.S., Russia, and China, Bitcoin’s market cap remains above $2.3 trillion, with dominance climbing to 55.4%.

Altcoins movements were strong over the week, with Ethereum surged 7% and others like LINK, ADA, and TRX rose over 5%. The top gainers were Doge soared 23%, AVAX jumped 20% and Solana surged 19%.

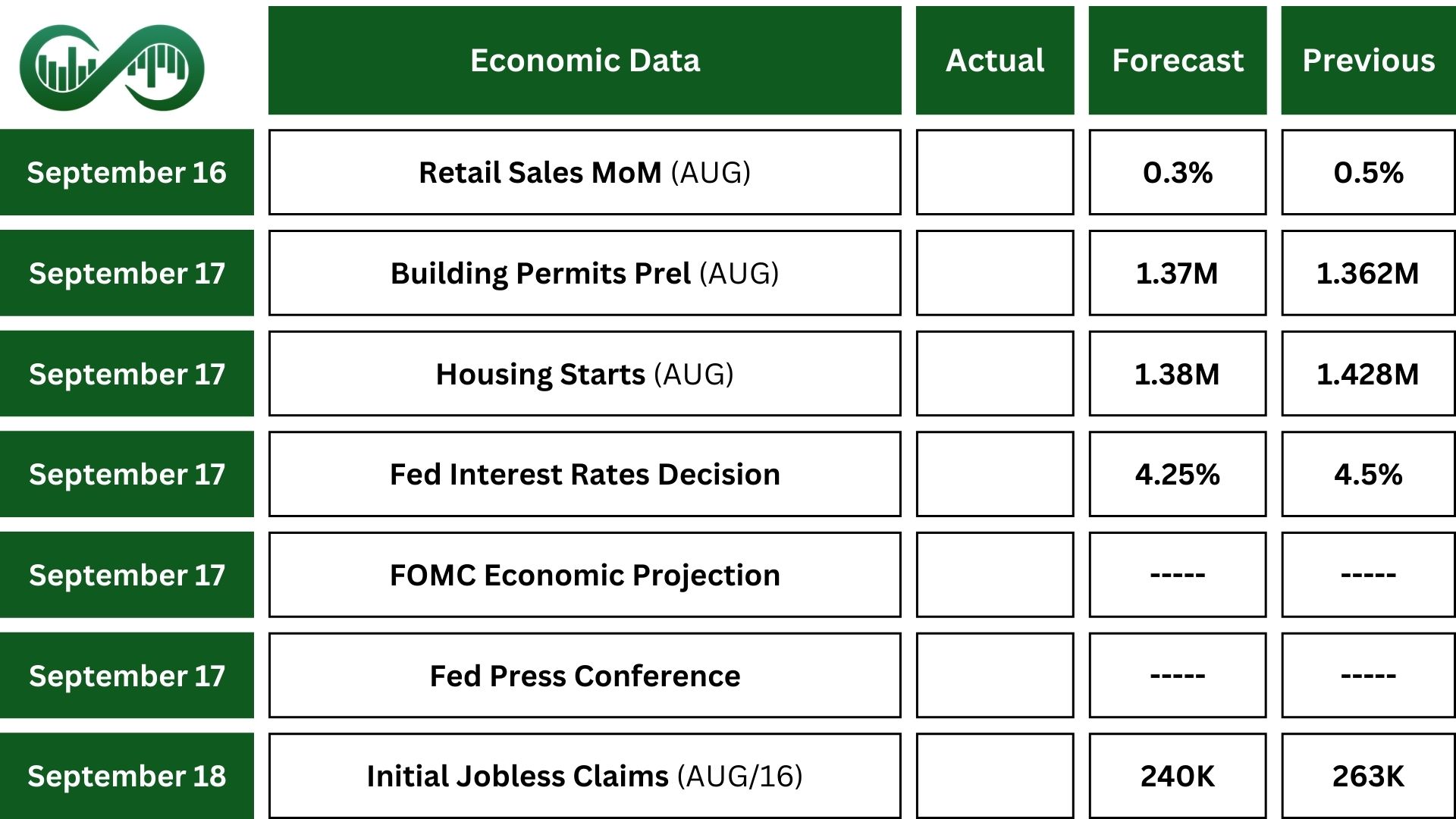

Next Week’s Outlook

Economic Events

This week market focus in the US is turning to the Federal Reserve’s upcoming policy decision, along with updated economic forecasts and Chair Powell’s remarks, which may offer clues about the trajectory of interest rates through the end of the year.

The Federal Open Market Committee is widely expected to lower the federal funds rate by 25 basis points to a range of 4% – 4.25%. Some investors are positioning for a more aggressive 50 basis point cut, which would mark the first rate reduction since December and bring rates to their lowest level since November 2022.

Recent economic indicators point to a faster-than-expected cooling in the labor market, while inflation remains relatively unaffected by tariff-related price pressures.

Retail sales are forecast to increase by 0.3% in August, continuing a three-month streak of gains. In contrast, industrial production appears to have stagnated.

Additional data releases on the horizon include foreign trade prices, housing starts, building permits, business inventories, the NAHB Housing Market Index, net long-term Treasury International Capital flows, and regional manufacturing reports from New York and Philadelphia. These figures will help shape expectations for future monetary policy and broader economic momentum.

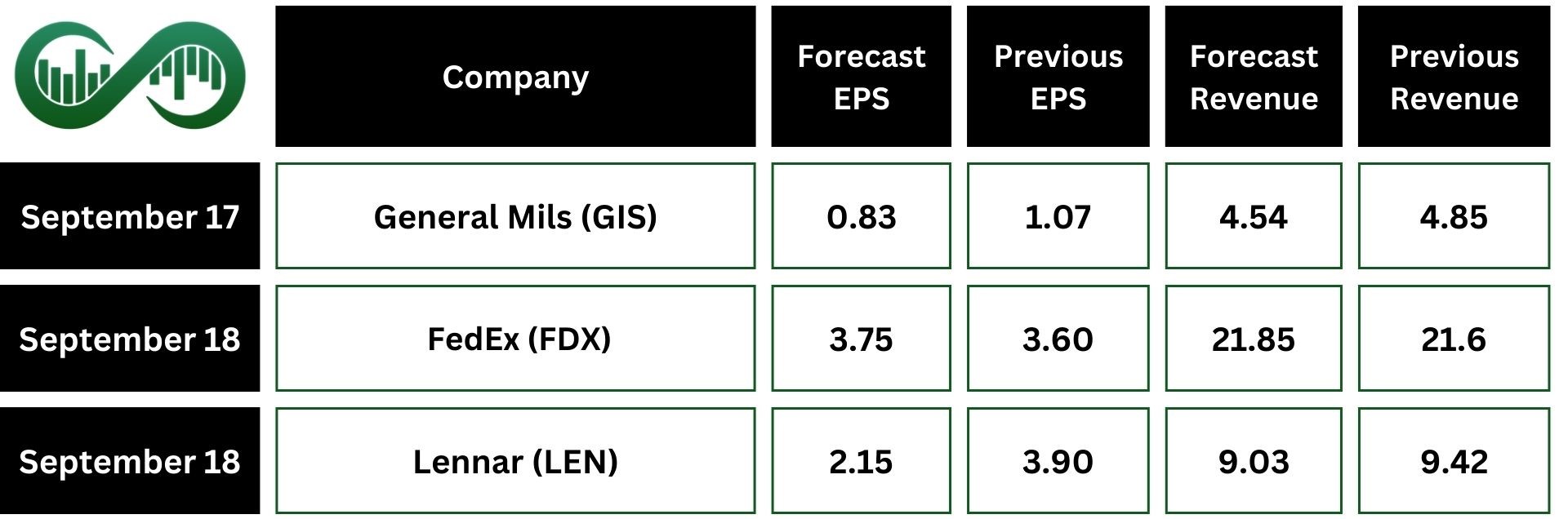

Earnings Events

This week’s earnings calendar includes key updates from FedEx (FDX).