Last Week’s report

Economic Reports

Job Reports

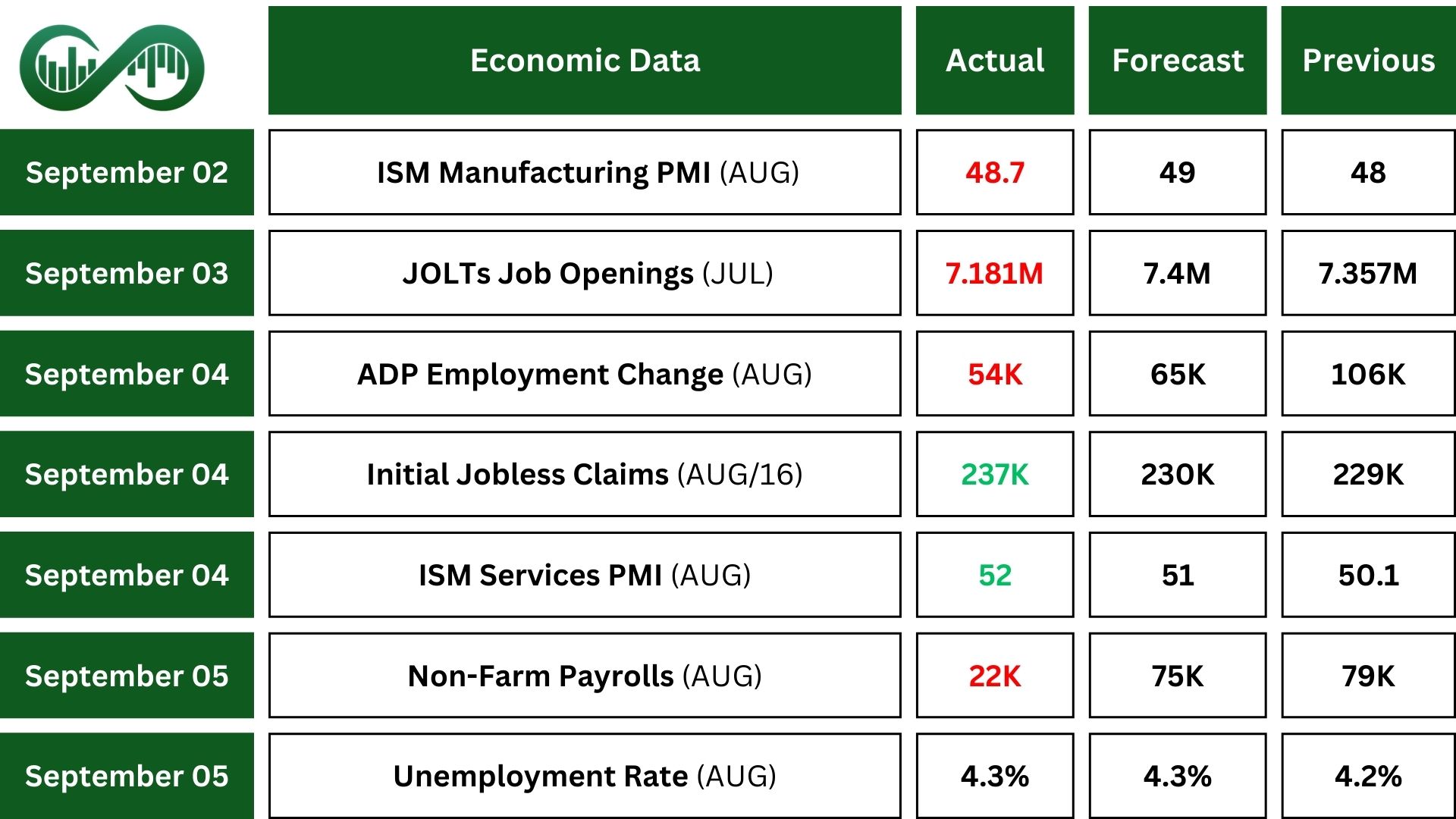

Job openings in the U.S. dropped sharply in July, falling by 176,000 to 7.18 million, marking the lowest level in nearly a year and missing expectations. The biggest declines were seen in healthcare, arts and entertainment, and mining.

U.S. job growth slowed in August, with nonfarm payrolls rising by just 22,000 far below July’s revised 79,000 and market expectations of 75,000.

This points to a cooling labor market. Most of the gains came from health care and social assistance, but they were offset by job losses in the federal government, due to spending cuts, and in industries like mining, wholesale trade, and manufacturing. Employment stayed mostly flat in other major sectors. Revisions to previous months showed that June and July had 21,000 fewer jobs than initially reported, adding to signs of weakening momentum.

The U.S. unemployment rate rose to 4.3% in August 2025, its highest level since late 2021, matching market expectations. The number of unemployed people grew by 148,000 to 7.38 million. At the same time, the overall labor force slightly expanded, pushing the participation rate up to 62.3% from a two-year low.

PMIs

U.S. manufacturing activity remained weak in August, with the ISM PMI rising slightly to 48.7 from 48.0 in July, still below the expected 49 and signaling contraction for the sixth month in a row. Production dropped sharply, but new orders improved somewhat. Employment continued to decline, though not as quickly. Inventories and backlogs shrank faster, showing softer demand. Input costs eased slightly but stayed high overall. Many businesses blamed tariffs for hurting conditions, pointing to higher costs, supply chain issues, and reduced competitiveness.

The U.S. services sector showed stronger growth in August, with the ISM Services PMI rising to 52 from 50.1 in July, its best reading in six months and better than expected. This improvement was fueled by faster increases in business activity, new orders, and inventories. Employment continued to shrink, the backlog of orders hit its lowest level in 16 years, and prices stayed high. Many businesses said tariffs were making things harder, with some rushing to stock up ahead of expected price hikes for the holiday season.

Earnings Reports

Salesforce

Salesforce (CRM) delivered strong second-quarter results, beating expectations with adjusted earnings of $2.91 per share and revenue of $10.24 billion.

The company saw solid growth across its cloud and AI services, especially in its Data Cloud and Agentforce platforms. Annual recurring revenue from these offerings surged 120% year-over-year to over $1.2 billion.

Despite the strong performance, investors reacted negatively to Salesforce’s cautious guidance for Q3. The company projected earnings in line with estimates, but its revenue forecast only matched the high end of expectations.

Broadcom

Broadcom (AVGO) had a strong third quarter, reporting better-than-expected earnings and announcing a major new customer order. The company earned $1.69 per share (adjusted), slightly above forecasts, and posted $15.95 billion in revenue, a 22% increase from last year.

Its partnership with OpenAI to develop custom AI chips is gaining attention, with the first chips expected to ship in 2026. This move is aimed at helping OpenAI reduce its reliance on suppliers like Nvidia.

Broadcom’s upbeat outlook sent its stock soaring over 10%. It expects fourth-quarter revenue to hit $17.4 billion, beating analyst estimates, and sees strong growth in AI-related sales next year.

Indices

Indices’ Weekly Performance:

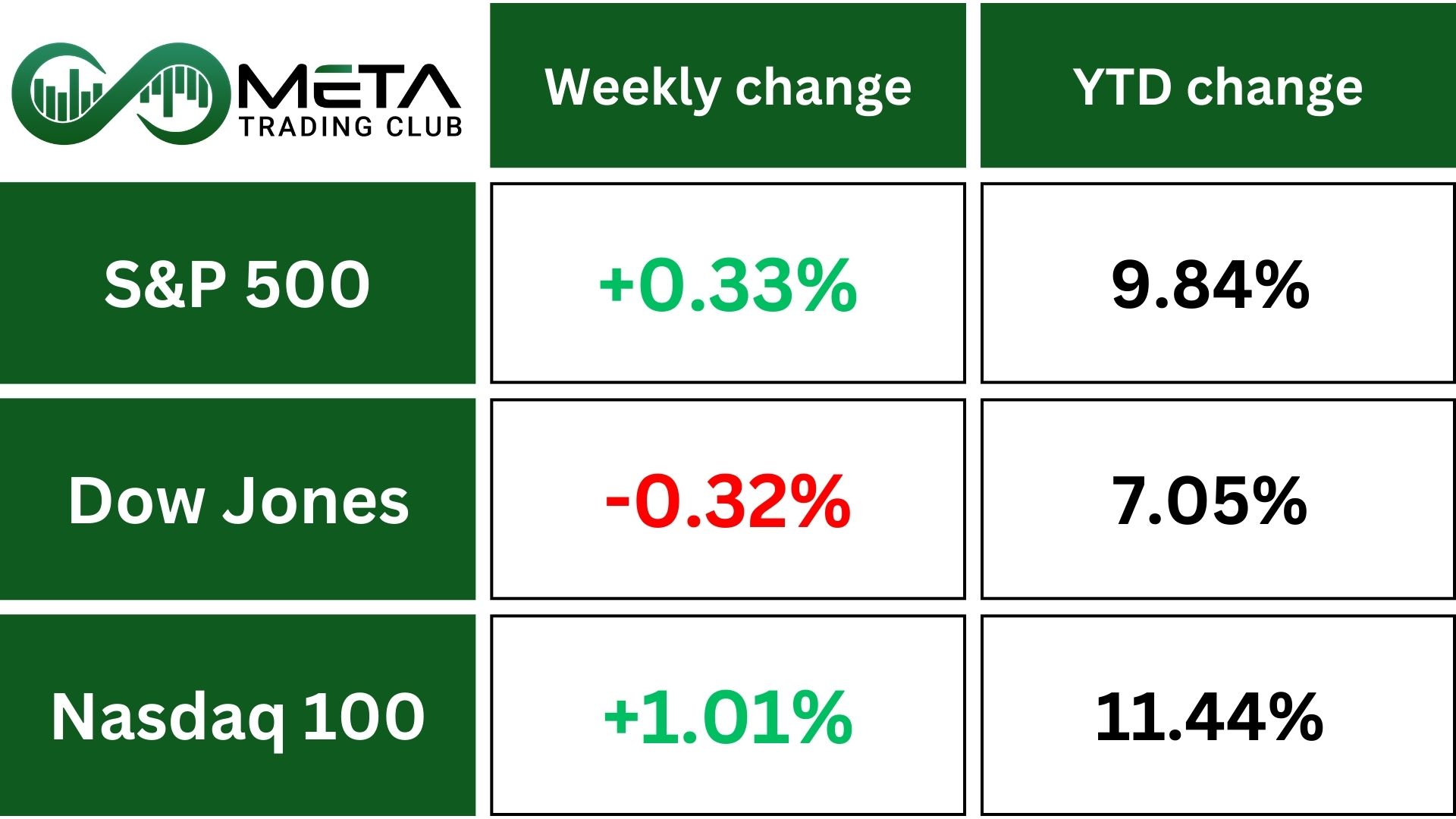

The S&P 500 edged up 0.3% this week, managing a modest gain despite growing concerns about an economic slowdown. Investors remain hopeful that the Federal Reserve may cut interest rates soon, but soft economic data and rising uncertainty have tempered that optimism.

Meanwhile, the Dow Jones Industrial Average slipped 0.3%, weighed down by weakness in financials and energy stocks. Big banks continued to struggle as cracks in the labor market widened, and falling oil prices dragged down energy shares.

In contrast, the Nasdaq surged 1.1%, powered by strength in tech and consumer discretionary stocks. Alphabet soared to a record high after sidestepping antitrust breakup demands, and Broadcom rallied on news of a $10 billion AI chip deal. Tesla also contributed to the Nasdaq’s gains, jumping on the announcement of a massive performance-based pay package for CEO Elon Musk. The tech-heavy index continues to benefit from investor enthusiasm around artificial intelligence and innovation, even as broader market sentiment remains mixed.

Technically, if SPX keeps losing RSI momentum and breaks its short-term uptrend line, it could drop further. But if the RSI downtrend breaks and the index clears the strong resistance near 6500, a sharp rally may follow.

Stocks

Sector’s Weekly Performance:

Only a few sectors stood out this week, with Communication Services and Consumer Discretionary leading the way, while Financials and Energy lagged behind. The overall market mood was mixed, and investor sentiment showed signs of growing pessimism.

- Communication Services surged by 4.1%, driven largely by Alphabet’s record-breaking performance. The company soared after successfully avoiding a forced breakup over antitrust concerns. Apple also saw gains, riding the wave of optimism across the tech sector.

- Consumer Discretionary rose 1%, thanks in part to Tesla’s rally following news of a massive $1 trillion performance-based pay package for CEO Elon Musk. U.S. homebuilders like D.R. Horton, Lennar, and Pultegroup climbed as bond yields dropped in response to a weak jobs report. However, not all companies in the sector fared well, Lululemon sank 17% for the week, hurt by disappointing U.S. sales and rising tariff costs.

- Consumer Staples edged up just 0.77%. Kraft Heinz fell after announcing plans to split into two separate companies, undoing a merger once backed by Berkshire Hathaway and 3G Capital. Constellation Brands, the maker of Corona beer, also declined after cutting its annual forecast due to soft demand. Meanwhile, Kenvue plunged following reports that RFK Jr. may link Tylenol use during pregnancy to autism.

- The Tech sector ticked down 1.2%. Broadcom made headlines with a $10 billion AI chip deal, reportedly involving OpenAI, helping the stock notch a 13% weekly gain. The semiconductor index rose 1.6%, but Salesforce slipped after issuing a weak revenue forecast, suggesting slower-than-expected returns from AI investments.

- Financials dropped 1% as cracks in the labor market widened. Big banks fell sharply on Friday, with the S&P 500 banks index down 2% for the week. Regional banks held steady, with only minor gains.

- Energy was the weakest sector, shedding 2.4%. The group declined as crude oil prices fell due to rising supply concerns and an unexpected increase in inventories.

Finally, investor confidence appears to be waning. The latest AAII survey shows a rise in pessimism among individual investors, reflecting growing uncertainty in the market.

Stock Market Weekly Performance:

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- Western Digital (WDC): Surged 14.5% on optimism around memory market recovery and potential restructuring or spin-off news.

- Broadcom (AVGO): Jumped 12.6% after strong earnings and news of a major AI chip partnership with OpenAI, plus bullish Q4 guidance.

- Seagate Technology (STX): Rose 12.4% alongside WDC due to improving demand for data storage and favorable analyst outlooks.

- Micron Technology (MU): Gained 10.3% on expectations of rising demand for high-bandwidth memory used in AI applications.

- Alphabet (GOOG): Hit 10.1% record highs after avoiding antitrust breakup and showing strength in cloud and advertising segments.

- Builders FirstSource (BLDR): Benefited 7.5% from falling yields post-jobs report, boosting housing affordability and construction outlook.

- Williams-Sonoma (WSM): Climbed 7.4% on strong earnings and continued demand for premium home furnishings.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold (XAU/USD) surged 4.02% last week, closing at a new record high. This marks its strongest weekly performance since April and reflects growing investor demand for safe-haven assets amid rising uncertainty over U.S. monetary policy.

The rally was fueled by expectations of interest rate cuts, with several Federal Reserve officials signaling support for easing measures as inflation shows signs of cooling. Political pressure on the Fed and resilient consumer spending have also contributed to the bullish sentiment. As a result, gold continues to attract buyers looking to hedge against economic volatility and policy shifts.

President Donald Trump announced changes to U.S. tariffs on Friday, removing country-based duties on several key metals, including graphite, tungsten, uranium, and gold bullion, while adding new tariffs on silicone products. The move reflects a shift in trade strategy, aiming to protect domestic industries while easing pressure on critical raw materials.

Forex

Weekly Performance of Major Foreign Exchange Pairs:

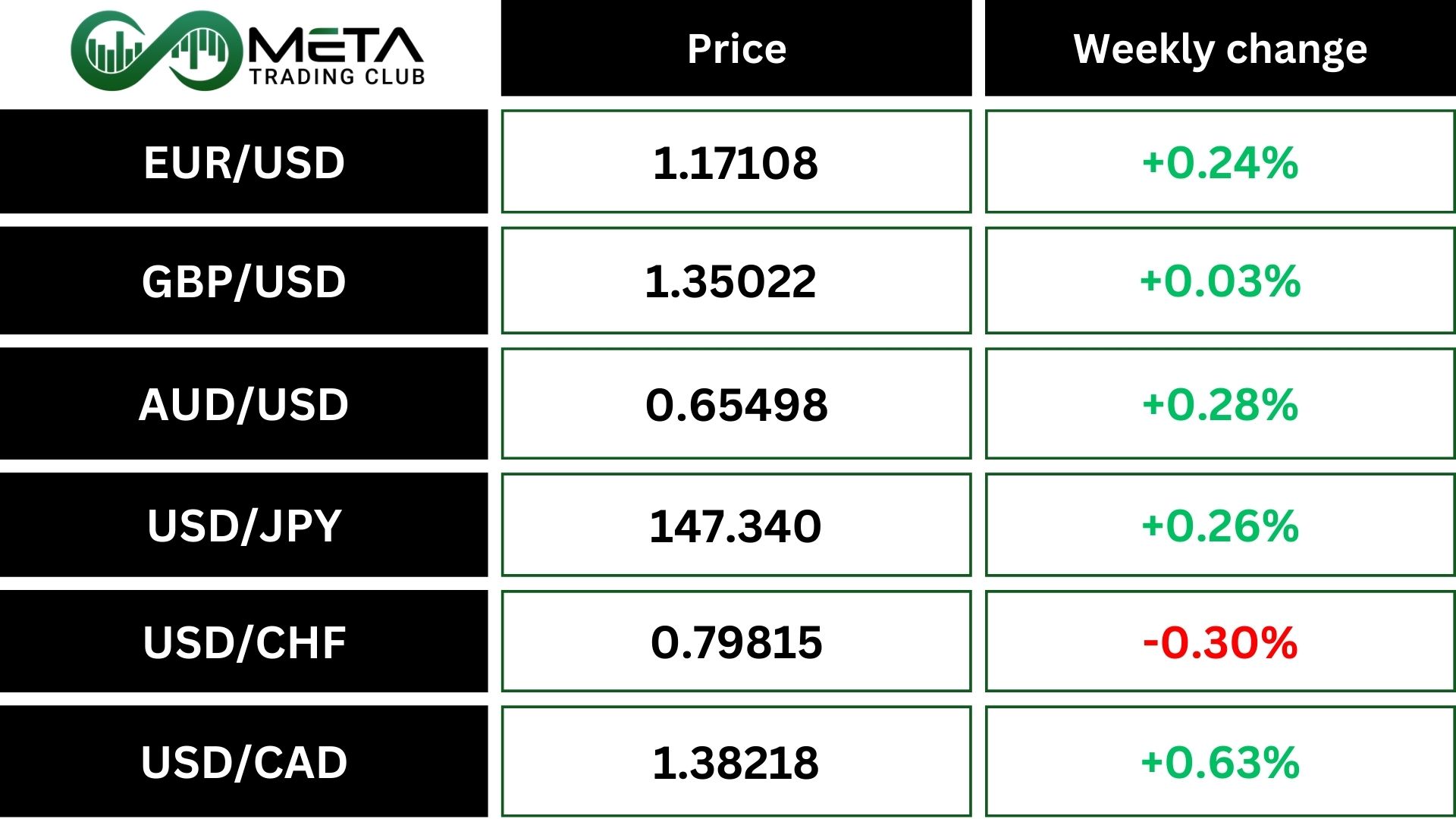

The U.S. Dollar Index (DXY) dropped 0.7% to a 1.5-month low last week, pressured by signs of a weakening labor market and growing expectations for Federal Reserve rate cuts before year-end. The disappointing jobs report reinforced views that the Fed may need to ease policy sooner, reducing the appeal of the dollar.

Adding to the pressure, Treasury yields fell sharply, both the 10-year yield and the 2-year yield declined by 7 basis points, landing at 4.09% and 3.52%, respectively. These lower yields narrowed the dollar’s interest rate advantage, further weighing on its performance against other major currencies.

- EUR/USD: The euro gained against the U.S. dollar, rising about 0.58%. This move was driven by weaker U.S. labor data and growing expectations for Fed rate cuts, which weighed on the dollar.

- USD/JPY: The dollar strengthened against the Japanese yen, climbing to a weekly high of 146.25. Despite soft U.S. data, the yen remained under pressure due to Japan’s ultra-loose monetary policy and widening interest rate differentials.

- GBP/USD: The British pound edged slightly higher, ending the week around 1.2620–1.3030. Sterling benefited from stable UK economic indicators and dollar weakness, though gains were modest amid cautious market sentiment.

Crypto

Crypto Market Weekly Performance:

Bitcoin showed a modest recovery heading into the weekly close, climbing back above $111,000 after briefly dipping on weak U.S. macroeconomic data. Bulls managed to hold the key $110,000 support level, which analysts view as a “promising” sign of strength. The price hit a local high of $111,369, gaining about 1% on the day.

However, the $112,000 level is seen as critical resistance, if bulls fail to break through, Bitcoin could face a deeper pullback. Fibonacci analysis suggests any drop may be limited to around 10%, with a “logical” bounce zone near $100,000. While some analysts are optimistic about a potential breakout, others warn that failure to reclaim resistance could trigger new lows.

Next Week’s Outlook

Economic Events

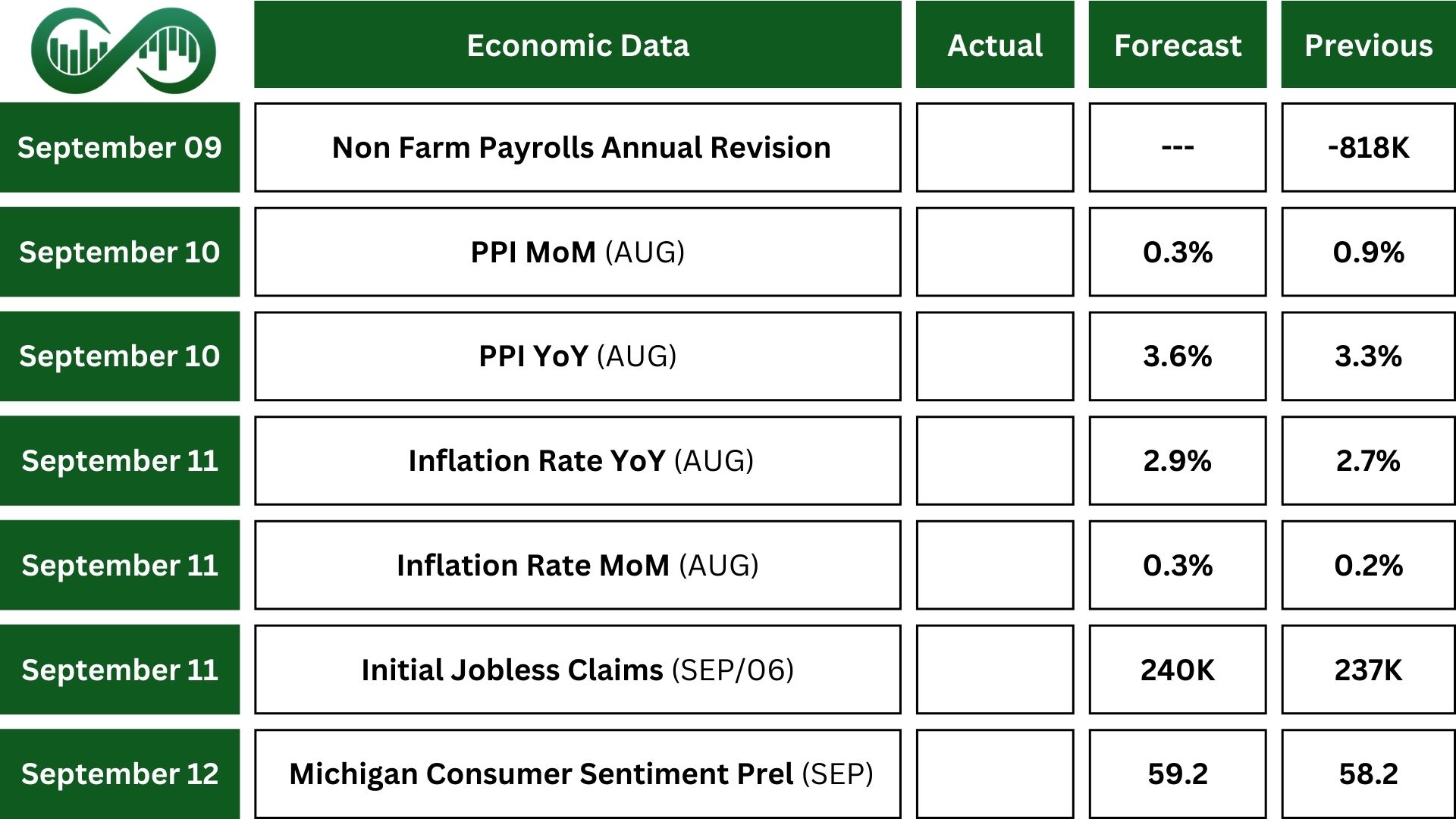

In the U.S., attention is turning to August’s inflation data to see how recent policy changes have affected prices. Consumer inflation is expected to rise to 2.9%, the highest since January, while core inflation is likely to stay above 3%. Producer prices are also expected to increase by 0.3% from the previous month.

With a weak jobs report already boosting expectations for a rate cut at the Fed’s September meeting, upcoming price data will play a key role in shaping interest rate decisions later this year. Labor market revisions for March 2025 will also be closely watched.

In addition, markets will look at the University of Michigan’s consumer sentiment index, which is expected to improve slightly, and its inflation expectations gauge to see if tariffs are changing household spending.

Other important releases include the NY Fed’s inflation outlook, the NFIB small business optimism index, and the monthly budget report.

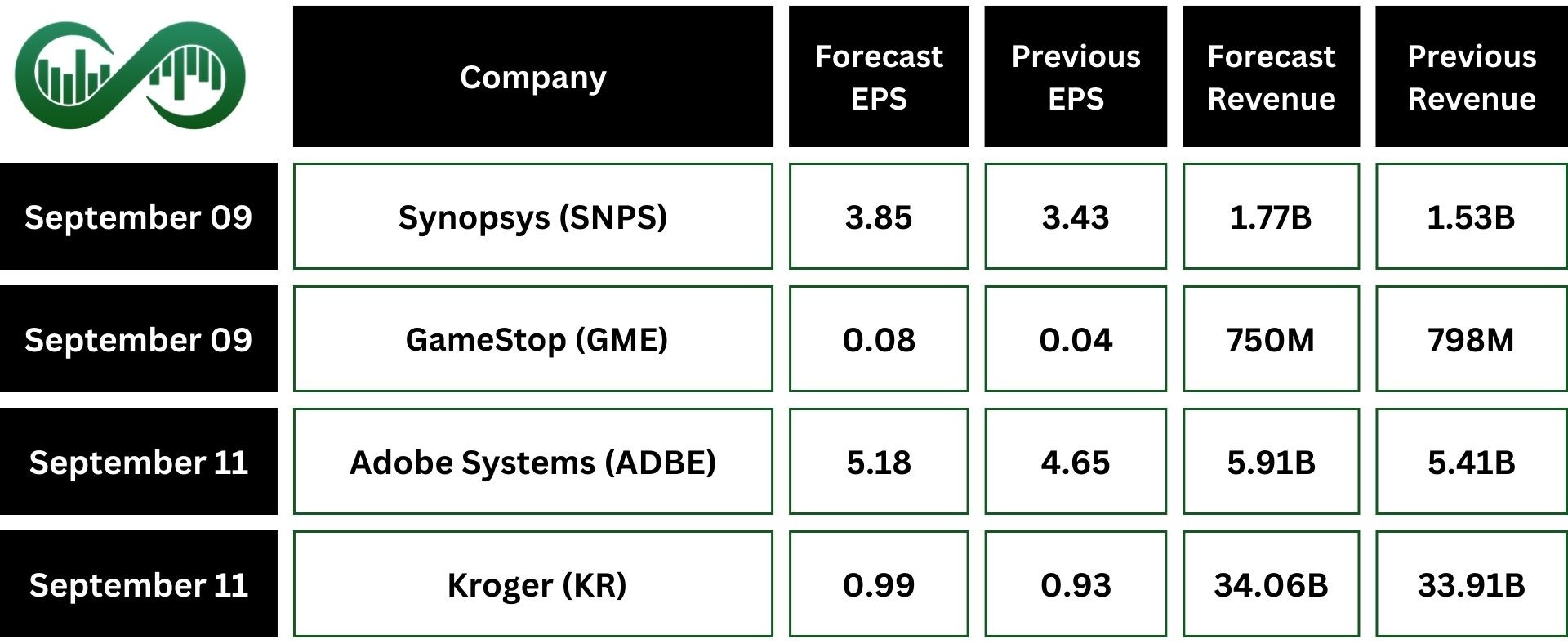

Earnings Events

This week’s earnings calendar includes key updates from Adobe and Kroger.