Last Week’s report

Economic Reports

Job Report

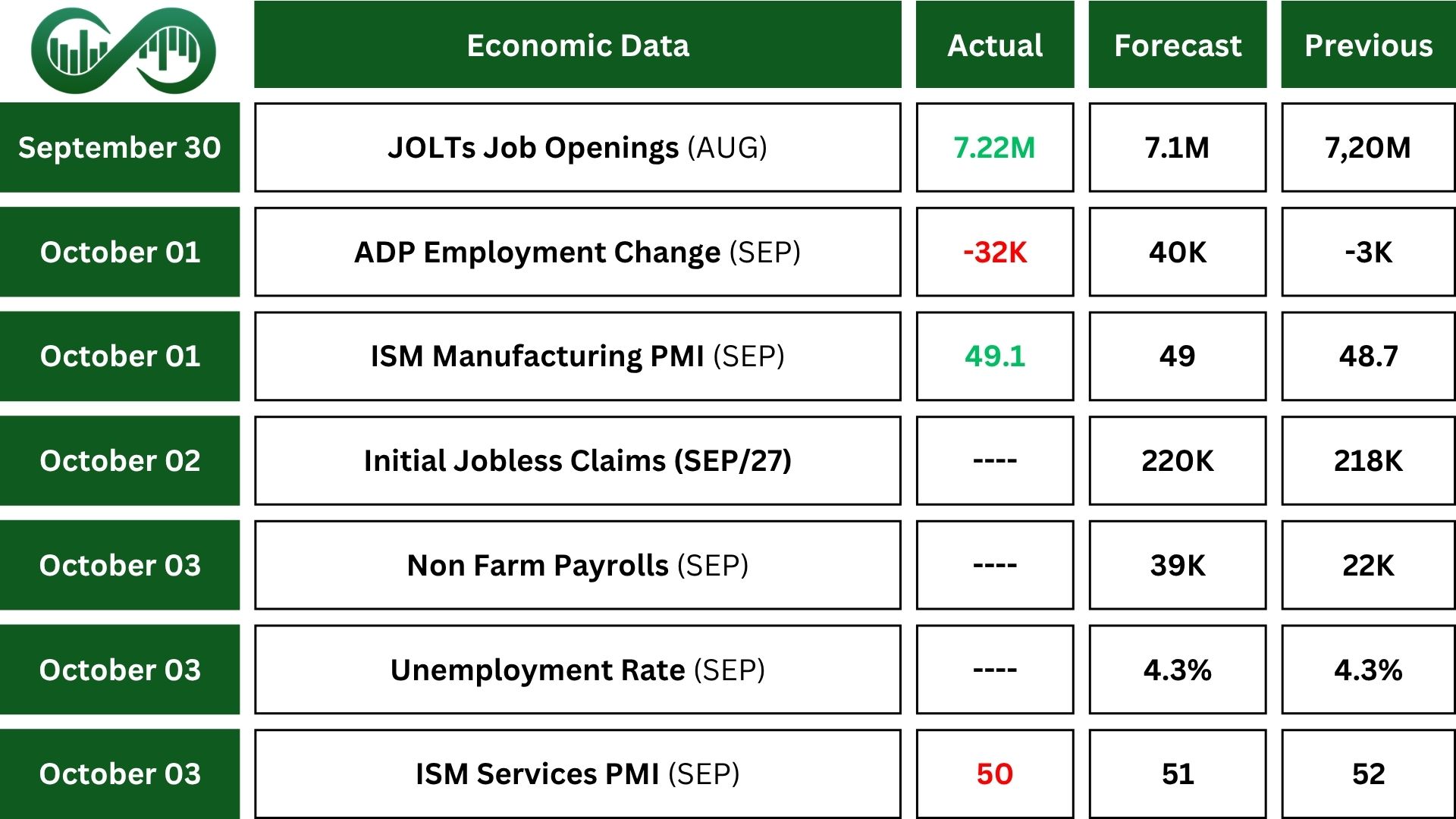

Last week, key economic reports, including jobless claims, nonfarm payrolls, and unemployment rates, were not released due to the ongoing U.S. government shutdown.

In August, U.S. Job Openings rose slightly to 7.227 million, matching market expectations. Job openings grew most in several sectors, including health care and social assistance.

Hiring and separations remained stable at 5.1 million. Within separations, both voluntary quits and layoffs or discharges showed little change, suggesting a steady labor market despite sector-specific shifts.

In September, private businesses in the U.S. unexpectedly cut 32,000 jobs, following a revised loss of 3,000 in August. This defied forecasts of a 50,000 gain and marked the sharpest decline since March 2023. It was also the first time since 2020 that the private sector reported job losses for two straight months.

The overall trend showed weakening job creation across most industries.

The service-producing sector shed 28,000 jobs, and the goods-producing sector lost 3,000 jobs, mainly from construction. Meanwhile, wage growth for employees who stayed in their jobs held steady at 4.5%, while pay increases for job-changers slowed to 6.6% from 7.1%.

PMI

In September, the ISM U.S. Manufacturing PMI rose slightly to 49.1 from 48.7 in August, just above expectations. Although this marked the seventh straight month of contraction, it was the strongest reading during the current downturn.

Production showed improvement, rising to 51, but new orders declined to 48.9, signaling uneven momentum. Employment continued to shrink, though at a slower pace, while customer inventories and order backlogs also fell, reflecting weak demand across the sector.

Input prices eased slightly to 61.9 but remained high, suggesting ongoing cost pressures. Manufacturers cited tariffs, elevated costs, and sluggish demand as major hurdles. Many companies are delaying investments, cutting expenses, and facing slower orders, especially in the machinery, metals, and semiconductor industries.

Also, the September U.S. services sector showed signs of stalling as the ISM Services PMI dropped to 50, down from 52 in August and below expectations. Business activity and new orders both weakened, while inventories slipped into contraction. Employment remained soft due to hiring delays and a shortage of skilled workers.

Price pressures grew stronger, with the prices index climbing to 69.4, its second-highest level since October 2022. Supplier deliveries also slowed, marking the weakest performance since February. A small positive came from a slower decline in backlogged orders. Overall, only 10 industries reported growth, down from 12 last month, while those reporting contraction rose from 4 to 7.

Earnings Reports

Nike

Nike (NKE) posted adjusted EPS of $0.49, beating expectations despite a 30% year-over-year drop. Revenue rose 1% to $11.7B, topping forecasts, though currency-neutral sales declined slightly.

Nike Brand revenue hit $11.4B, with strong growth in North America offset by weakness in Greater China. Nike Direct fell 4% due to a sharp 12% drop in digital sales. Wholesale rose 7%, while Converse plunged 27%.

Also, Nike returned $714M to shareholders, $591M in dividends (up 6%), and $123M in buybacks, reflecting continued capital discipline.

Nike shares rose after these reports, as strong earnings and resilience in key areas boosted investor sentiment despite broader market uncertainty.

Indices

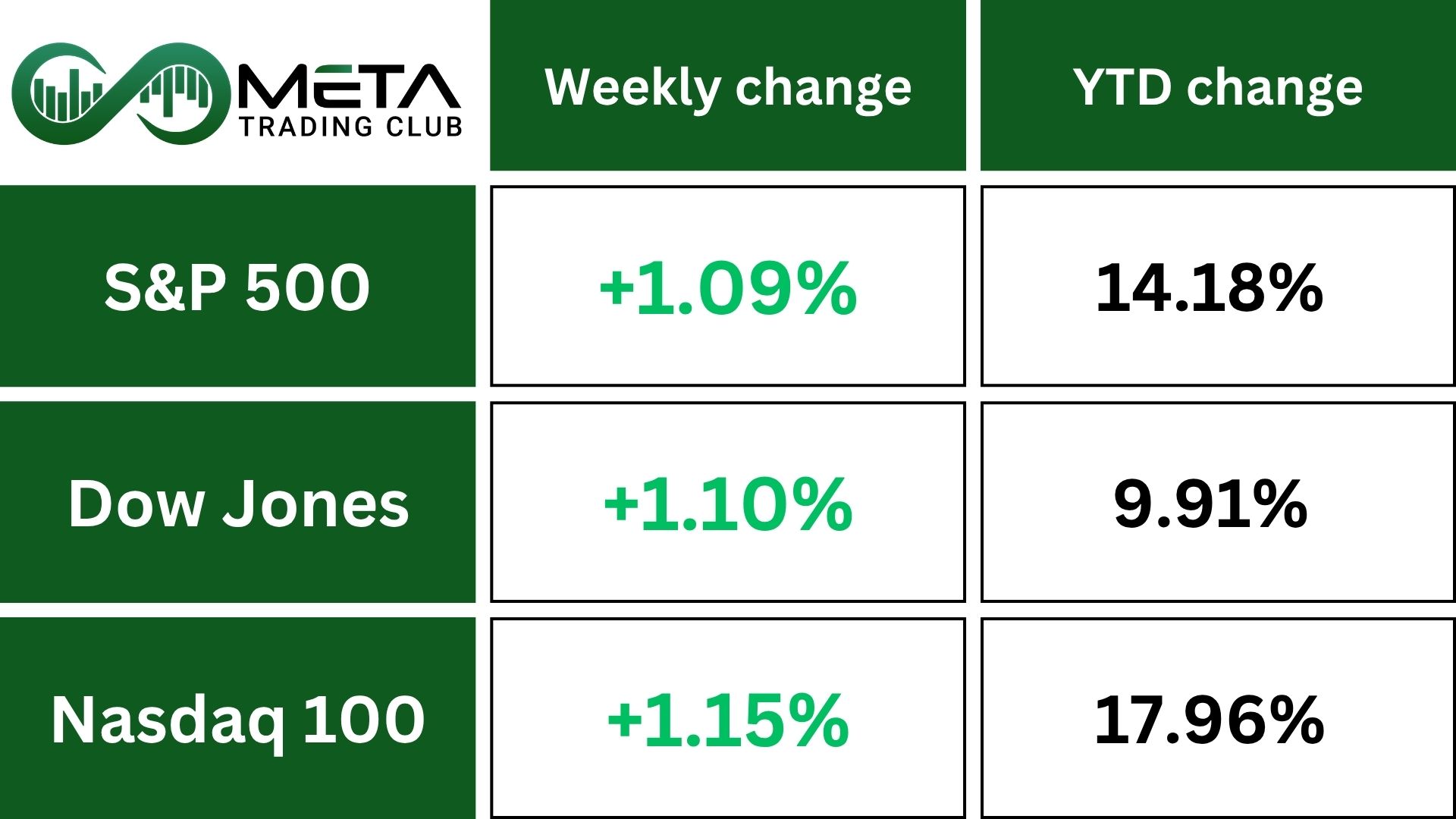

Indices’ Weekly Performance:

Stock markets had a strong week, with tech shares leading the rally and hopes for lower U.S. interest rates helping offset concerns about the ongoing U.S. government shutdown. Despite the lack of key data like the monthly payrolls report, investors remained optimistic, pushing major U.S. indexes to record highs and lifting global benchmarks.

The shutdown, now the 15th since 1981, has delayed important economic reports, and analysts expect more delays ahead, including jobless claims, inflation, and retail sales data.

Markets are nearly fully pricing in a 25-point Fed rate cut this month and several more over the next year.

Technically, SPX has a key Fibonacci extension resistance zone around 6900; the index could continue its rise to this level if bearish confirmations don’t appear.

Stocks

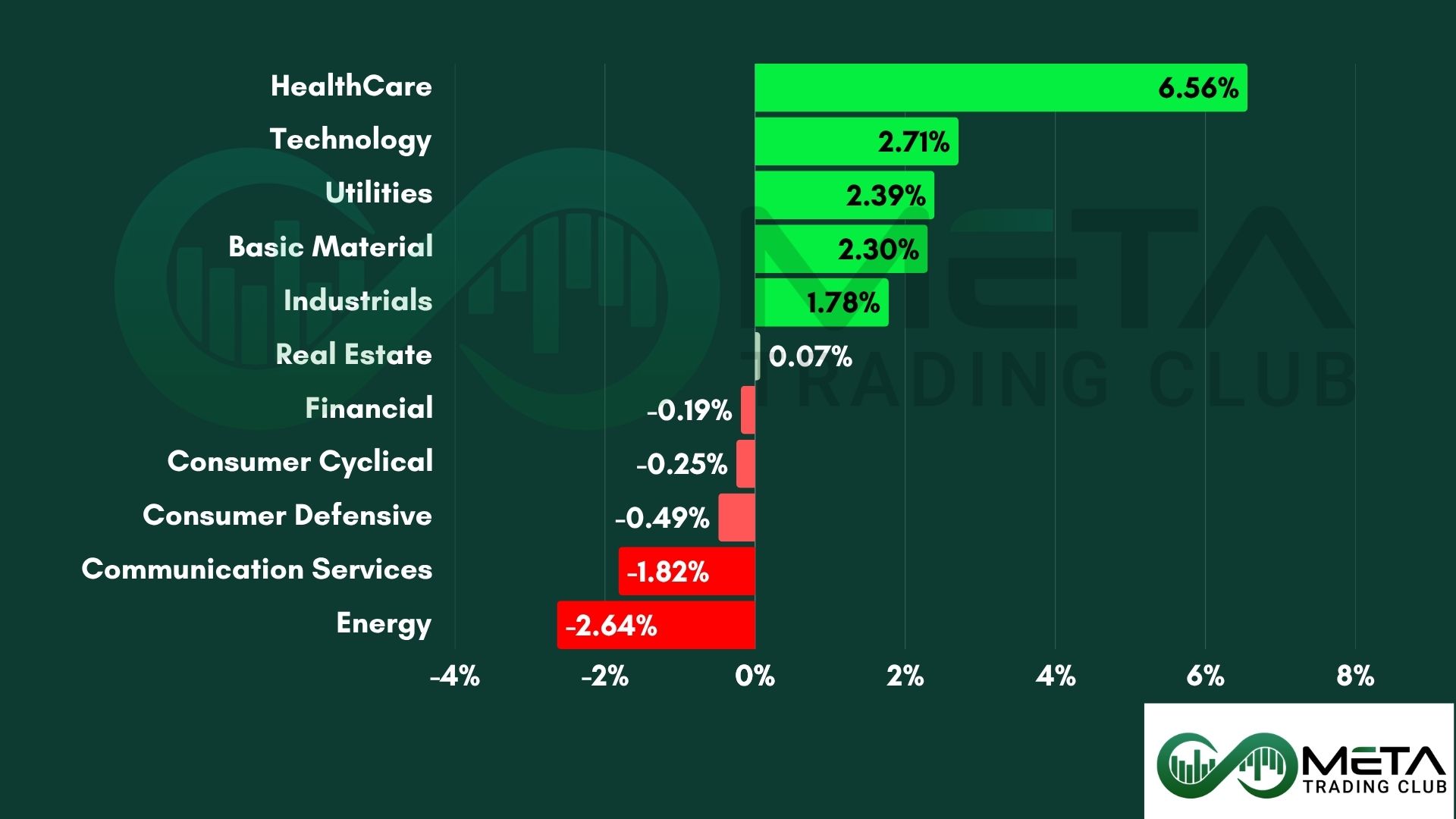

Sector’s Weekly Performance:

Last week, Healthcare leads, while Communication Services and Energy falter.

- Healthcare surged 6.5%, emerging as the strongest performer. Pfizer (PFE) rallied on news of a drug pricing agreement announced by President Trump, boosting sentiment across pharmaceutical and life sciences stocks. The sector posted its best weekly performance in the S&P 500 since June 2022, while the Nasdaq Biotech Index (NBI) jumped over 6%, reaching a four-year high.

- Technology rose 2.7%. Data storage firms Western Digital (WDC) and Seagate (STX) hit record highs, fueled by AI momentum. WDC logged a 23% weekly gain. Chipmakers also rallied, driven by global AI enthusiasm after Samsung and SK Hynix agreed to supply chips for OpenAI’s Stargate project. The Semiconductor Index (SOX) gained 4.4%. Fair Isaac (FICO) soared 22% after launching a direct licensing program for mortgage scores.

- Utilities climbed 2.4%. AES (AES) advanced following reports that BlackRock’s Global Infrastructure Partners (GIP) is nearing a $38 billion acquisition of the power company.

- Financials dipped 0.2%, pressured by concerns over a potential U.S. government shutdown. The S&P 500 Banks Index fell nearly 3%, while the KBW Regional Banking Index (KRX) declined 1%.

- Consumer Discretionary slipped 0.5%. Tesla (TSLA) initially rose on record quarterly deliveries but reversed on demand concerns as the EV tax credit expired. However, Nike (NKE) jumped after a surprise beat on quarterly revenue and profit, signaling progress in its turnaround despite headwinds from China and tariffs.

- Communication Services dropped 1.8%. Netflix (NFLX) fell for five consecutive days following Elon Musk’s call for a boycott over a controversial show. In contrast, Electronic Arts (EA) rose on news of a record-breaking $55 billion leveraged buyout led by Silver Lake, Saudi Arabia’s Public Investment Fund, and Jared Kushner’s Affinity Partners.

- Energy declined 2.6%, dragged down by falling oil prices amid oversupply concerns. Occidental Petroleum (OXY) slid after announcing a $9.7 billion sale of its chemical business to Berkshire Hathaway (BRK.A).

Top Performers

Last week saw a remarkable stock market performance, with several companies standing out as top gainers:

- Western Digital (WDC): Surged +22.86% on strong AI-driven demand for data storage, boosted by involvement in OpenAI’s Stargate chip project.

- Robinhood (HOOD): Jumped +22.08% as crypto trading volumes rose and investor optimism grew around platform monetization.

- Fair Isaac (FICO): Gained +21.85% after launching a direct licensing program for mortgage scores, signaling expansion in credit analytics.

- Coinbase (COIN): Rose +21.57% amid a crypto market rebound, with Bitcoin strength lifting trading activity and investor sentiment.

- Micron Technology (MU): Climbed +19.03% on rising AI chip demand and a supply agreement with OpenAI, fueling semiconductor momentum.

- Thermo Fisher (TMO): Advanced +17.43% following positive reactions to drug pricing reforms, boosting healthcare sector confidence.

- Danaher (DHR): Increased +16.92% on strong life sciences demand and upbeat earnings guidance.

- Seagate Technology (STX): Up +16.22% due to AI infrastructure demand and record highs, riding momentum alongside Western Digital.

- Eli Lilly (LLY): Gained +15.92% on continued strength in obesity and diabetes drug sales, supported by bullish analyst upgrades.

- Pfizer (PFE): Surged +15.19% after President Trump’s drug pricing agreement, which renewed confidence in the pharmaceutical sector.

Commodity

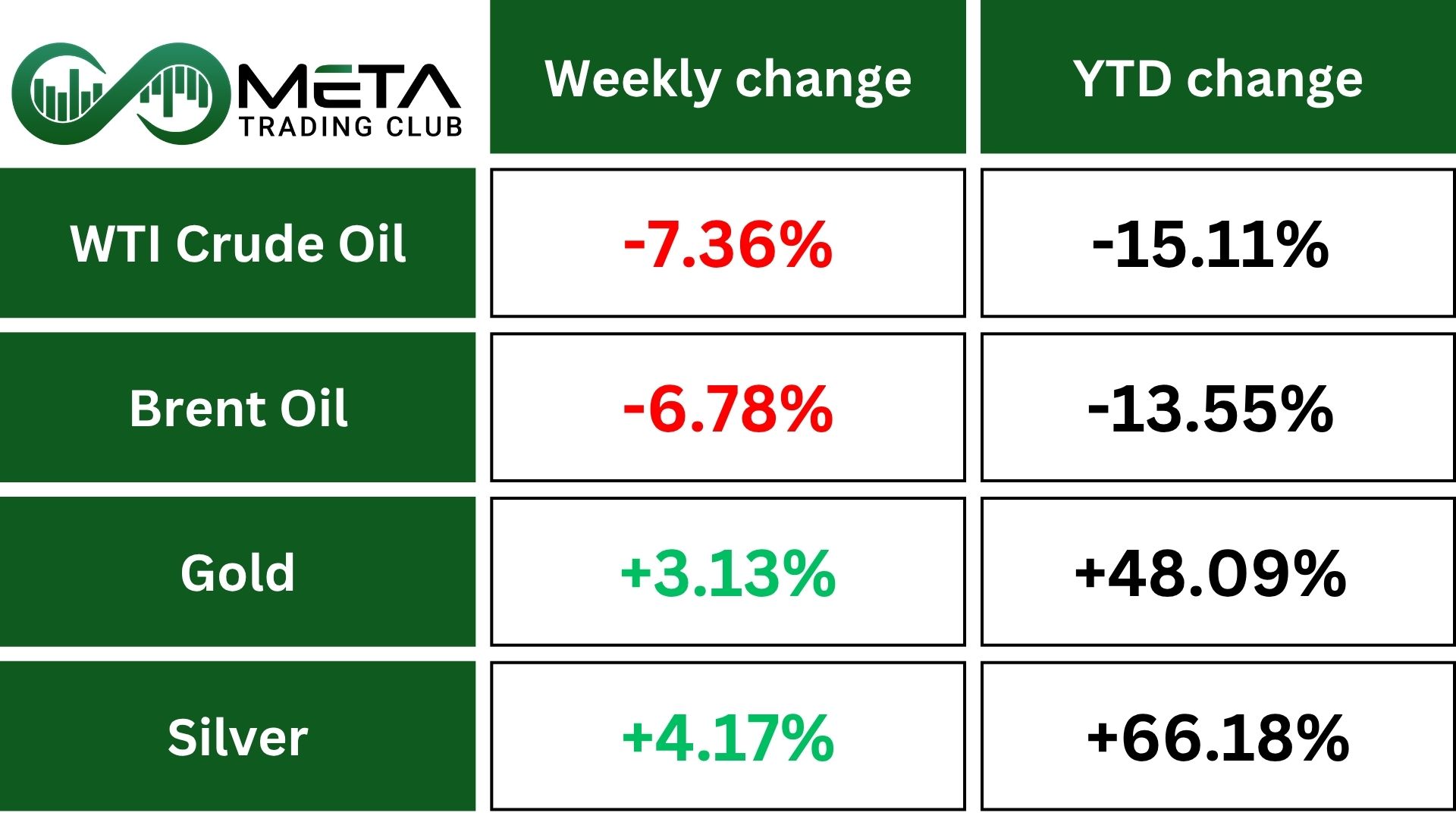

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Gold

Gold rose to a new record high and marking its seventh consecutive weekly gain. The rally continues to be driven by safe-haven demand amid the ongoing U.S. government shutdown and growing expectations of a more dovish Federal Reserve.

With the shutdown likely to delay the release of September’s job data, investors have shifted their focus to alternative indicators that suggest economic momentum is fading. The ADP employment report revealed an unexpected decline in private-sector hiring, while the latest ISM Services PMI pointed to stagnation.

As a result, market participants now anticipate the Fed will implement two 25-basis-point rate cuts at its remaining meetings this year. There is a 97% chance of a 0.25% cut in October and an 85% chance of another in December.

Lower rates make gold more attractive, and its price has already jumped over 48% this year. This is its strongest annual performance since 1979.

UBS predicts gold could reach $4,200 per ounce in the coming months. They say falling real interest rates and a weaker U.S. dollar are helping gold rise, as it becomes cheaper to hold and more appealing during uncertain times.

Technically, Gold has reached a key Fibonacci extension resistance zone. With multiple signs of rejection forming, a pullback from this strong level is possible. However, if the index breaks through and closes above this resistance, it could open the door to further upside momentum.

Oil

Crude oil prices stayed near a four-month low and were heading for their worst week since June.

The drop was mainly due to expectations that OPEC+ might increase oil production by up to 500,000 barrels per day in November, with Saudi Arabia aiming to regain market share.

Oversupply worries grew as U.S. data showed rising inventories of crude, gasoline, and distillates, while demand and refining activity slowed.

Additional pressure came from fears that the U.S. government shutdown could hurt economic activity and news that Kurdish oil exports from Iraq had resumed. Meanwhile, G7 finance ministers pledged to tighten actions against Russia by targeting buyers of its oil.

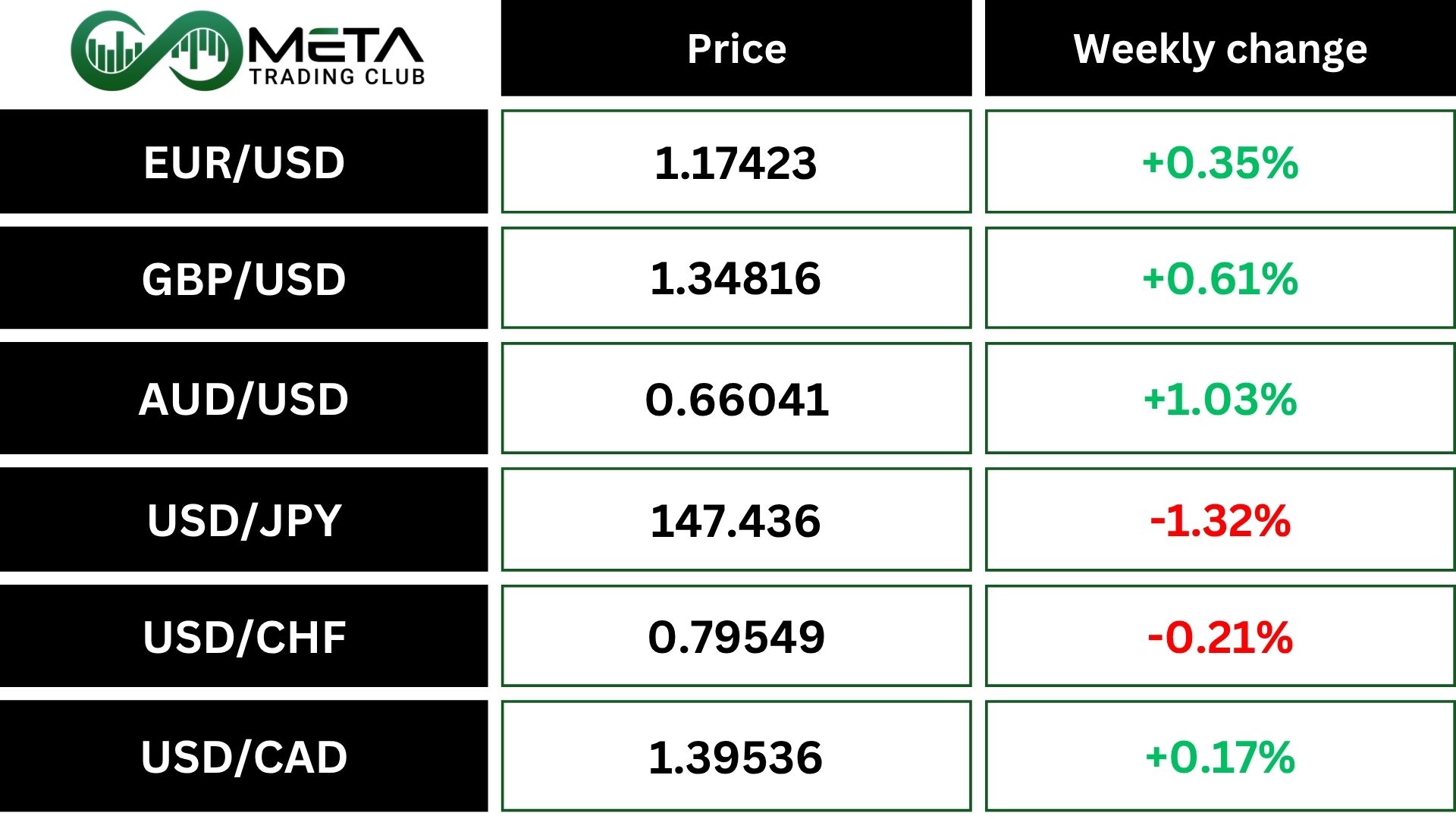

Forex

Weekly Performance of Major Foreign Exchange Pairs:

Dollar Index (DXY): The DXY, which tracks the dollar against a basket of major currencies, slipped to 97.7. It was pressured by shutdown-related uncertainty and weaker-than-expected U.S. services sector data.

EUR/USD: The euro rose 0.35% against the U.S. dollar, marking its best weekly performance in a month. The gain came as traders reacted to the U.S. government shutdown and the delay of key economic data, including the nonfarm payrolls report, which clouded the dollar’s outlook.

USD/JPY: The dollar gained 1.3% against the Yen, its best performance since mid-May. Traders were watching Japan’s political developments and comments from BOJ Governor Kazuo Ueda, which tempered expectations of a near-term rate hike.

Crypto

Bitcoin surged past $125,000 over the weekend, reaching a new all-time high and a market value of $2.5 trillion, surpassing even Amazon.

This rally comes as the U.S. government shutdown continues, creating a brief window where traders have jumped back into riskier assets, such as cryptocurrency. With key economic reports delayed, investors are reacting to uncertainty by seeking alternative places to park their money.

October has historically been a strong month for Bitcoin, earning the nickname “Uptober.” This year, the cryptocurrency is already up 35%, boosted by corporate interest and growing demand for crypto investment products.

Technically, BTC has tested its all-time high resistance and briefly broke above it, but hasn’t yet secured a close beyond that level. If the breakout holds, further upside is likely. However, a rejection from this zone could trigger a pullback toward the 120K support area.

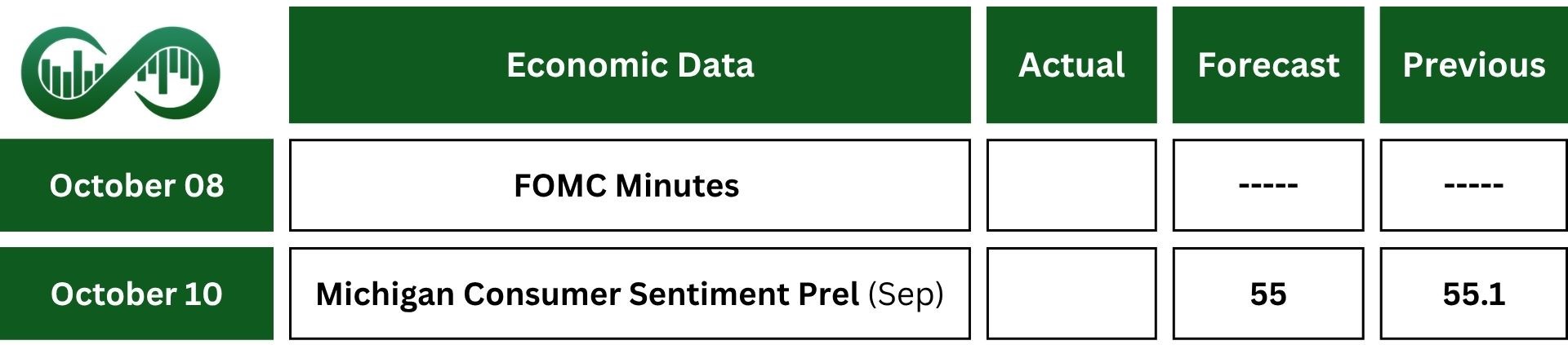

Next Week’s Outlook

Economic Events

This week, the main focus will be on the evolving situation surrounding the federal government shutdown, especially whether Republicans and Democrats can broker a deal to fund operations and resume the release of key economic data.

Uncertainty persists as the Senate prepares to vote on October 3rd on two competing proposals: a GOP-supported seven-week stopgap funding bill and a Democratic measure that includes health care provisions.

With both sides locked in a stalemate, neither bill is expected to pass, heightening the risk of delays to critical reports due this week, including foreign trade figures, weekly jobless claims, and the federal budget statement.

Meanwhile, investors will closely monitor the preliminary Michigan Consumer Sentiment Index, which is projected to show October confidence at its lowest level since May.

On the monetary policy front, market attention will shift to the release of FOMC meeting minutes and public remarks from several Federal Reserve officials, including Chair Jerome Powell, for insights into the Fed’s outlook for the remainder of the year.

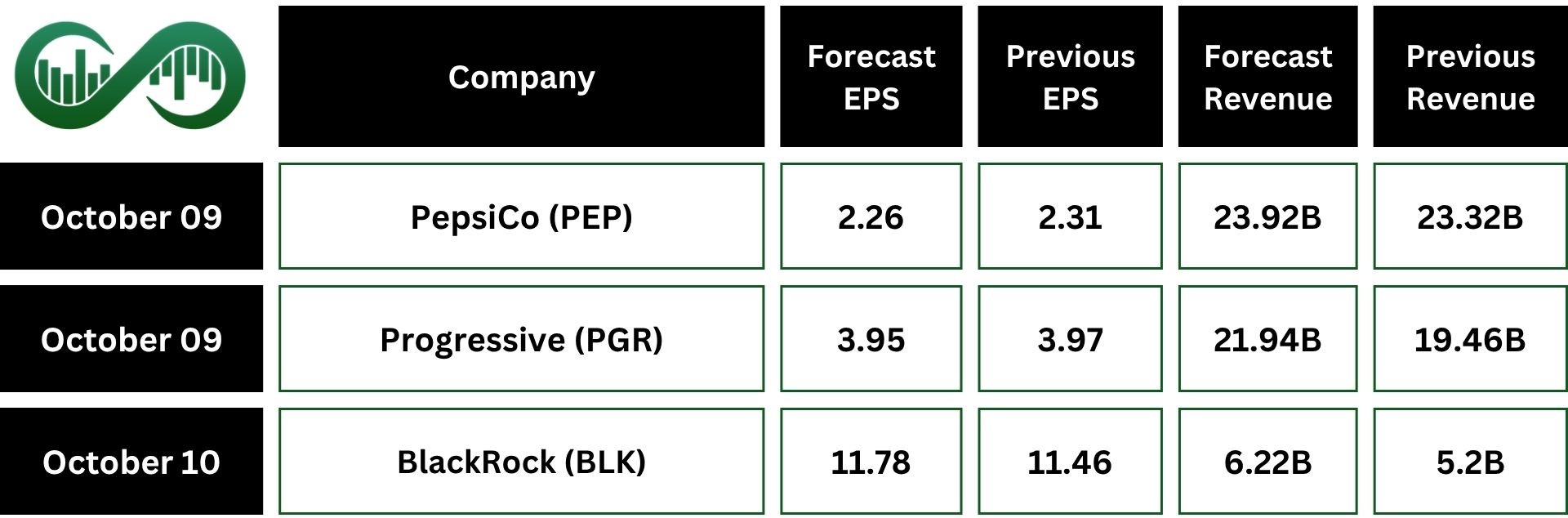

Earnings Events

The earnings season will begin this week with BlackRock (BLK) reporting its third-quarter results.