Last Week’s report

Economic Reports

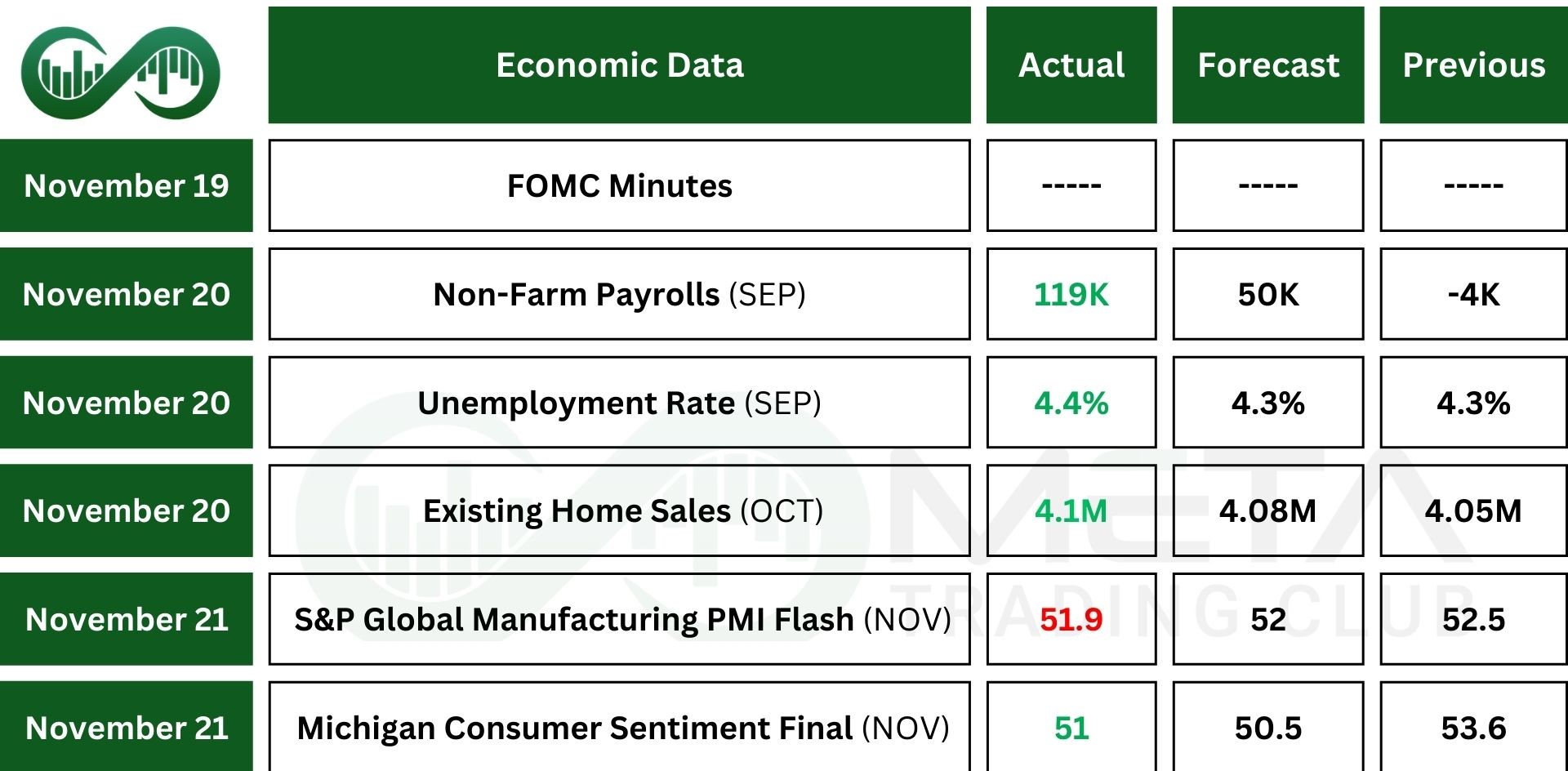

US Nonfarm Payrolls rose by 119K in September, a strong rebound from August’s revised decline of 4K. This beat expectations and marks the biggest monthly job gain in five months. This report was originally set for release on October 3 but was delayed due to the longest government shutdown in US history. The October jobs report has been cancelled.

Michigan Consumer sentiment in the US edged up to 51 in November, following the end of the federal shutdown. Still, the reading remains near historic lows as households continue to struggle with high prices and weaker incomes. The Current Economic Conditions Index dropped sharply to a record low of 51.1, reflecting poorer views on personal finances and durable goods purchases.

Inflation expectations eased modestly, with year-ahead expectations down to 4.5% and long-term expectations falling to 3.4%, though both remain above earlier levels seen in 2022.

Earnings Reports

Nvidia

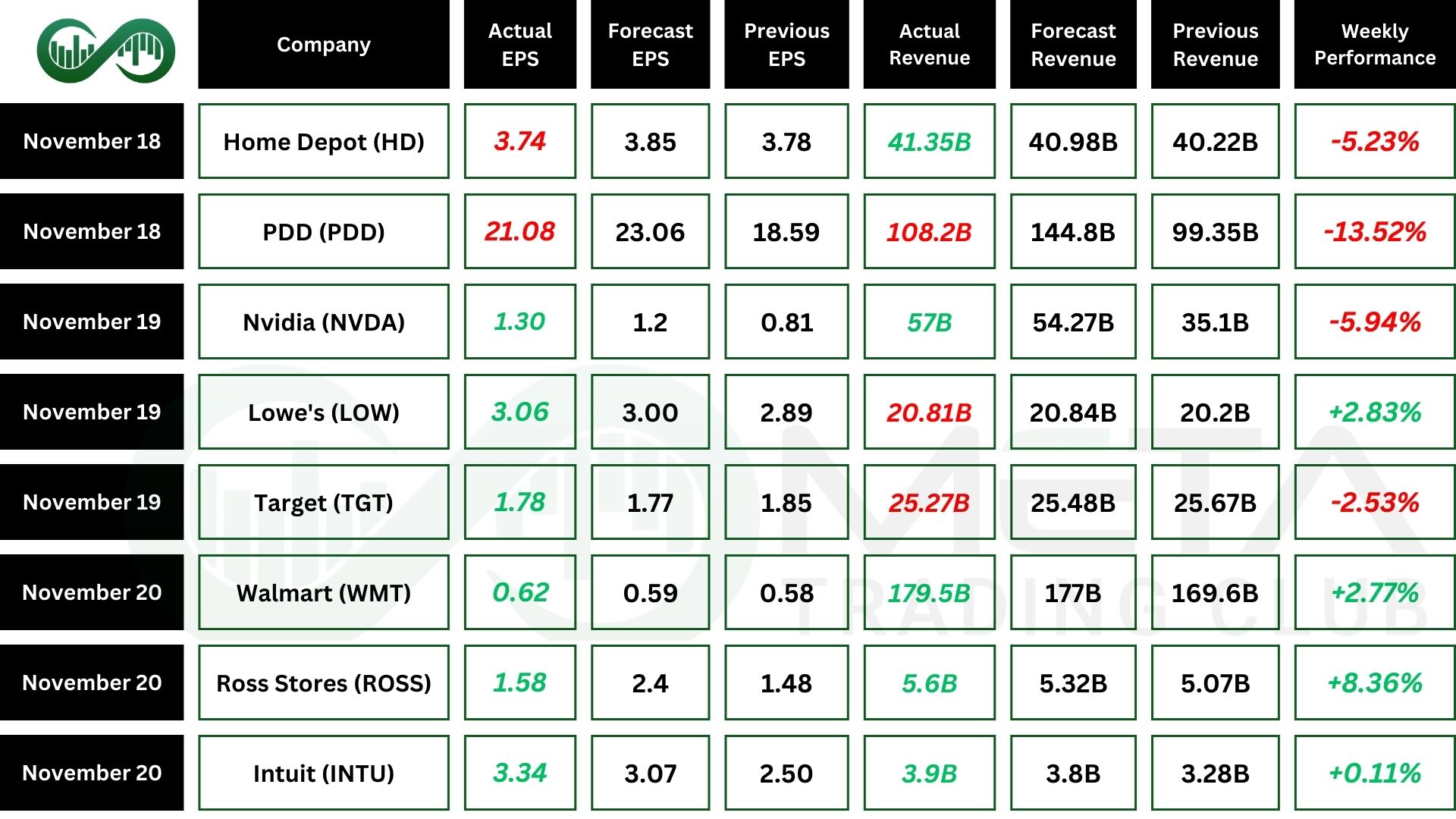

Nvidia (NVDA) reported record fiscal Q3 2026 revenue of $57 billion, up 62% year‑over‑year, with EPS of $1.30 exceeding expectations.

Also, Data Center sales surged 66% to $51.2 billion, driven by strong demand for Blackwell GPUs and strategic partnerships with major AI players, including OpenAI, Google Cloud, and Microsoft.

Gaming revenue reached $4.3 billion, while professional visualization and automotive segments also grew.

Shares initially jumped on the results but later dipped amid AI bubble concerns, though guidance for Q4 revenue of $65 billion reinforced confidence in sustained growth.

Target

Target (TGT) reported adjusted earnings of $1.78 per share, slightly above forecasts but down from $1.85 last year. While revenue fell 1.5% to $25.3 billion, it missed expectations.

Digital sales grew 2.4%, fueled by over 35% growth in same‑day delivery, and non‑merchandise sales jumped nearly 18%, though discretionary categories remained weak.

Also, GAAP EPS was $1.51, and adjusted EPS excluded severance and asset charges. Looking ahead, Target guided for a low single‑digit sales decline in Q4.

Shares initially dropped on soft sales and cautious holiday guidance but rebounded after announcing a new partnership with OpenAI, enabling customers to shop via ChatGPT, a move that could reshape Target’s digital engagement strategy.

Walmart

Walmart (WMT) delivered strong fiscal Q3 2026 results, with revenue rising 5.8% to $179.5 billion and adjusted operating income up 8%, both ahead of expectations.

Also, global eCommerce surged 27%, U.S. comparable sales grew 4.5%, and advertising revenue jumped 53%, while membership income climbed nearly 17%. GAAP EPS came in at $0.77, and adjusted EPS at $0.62.

Looking ahead, Walmart raised its fiscal 2026 outlook, projecting steady net sales and operating income growth. Shares rose as investors welcomed the strong performance and guidance, though broader market sentiment and leadership transitions temper near‑term optimism.

Indices

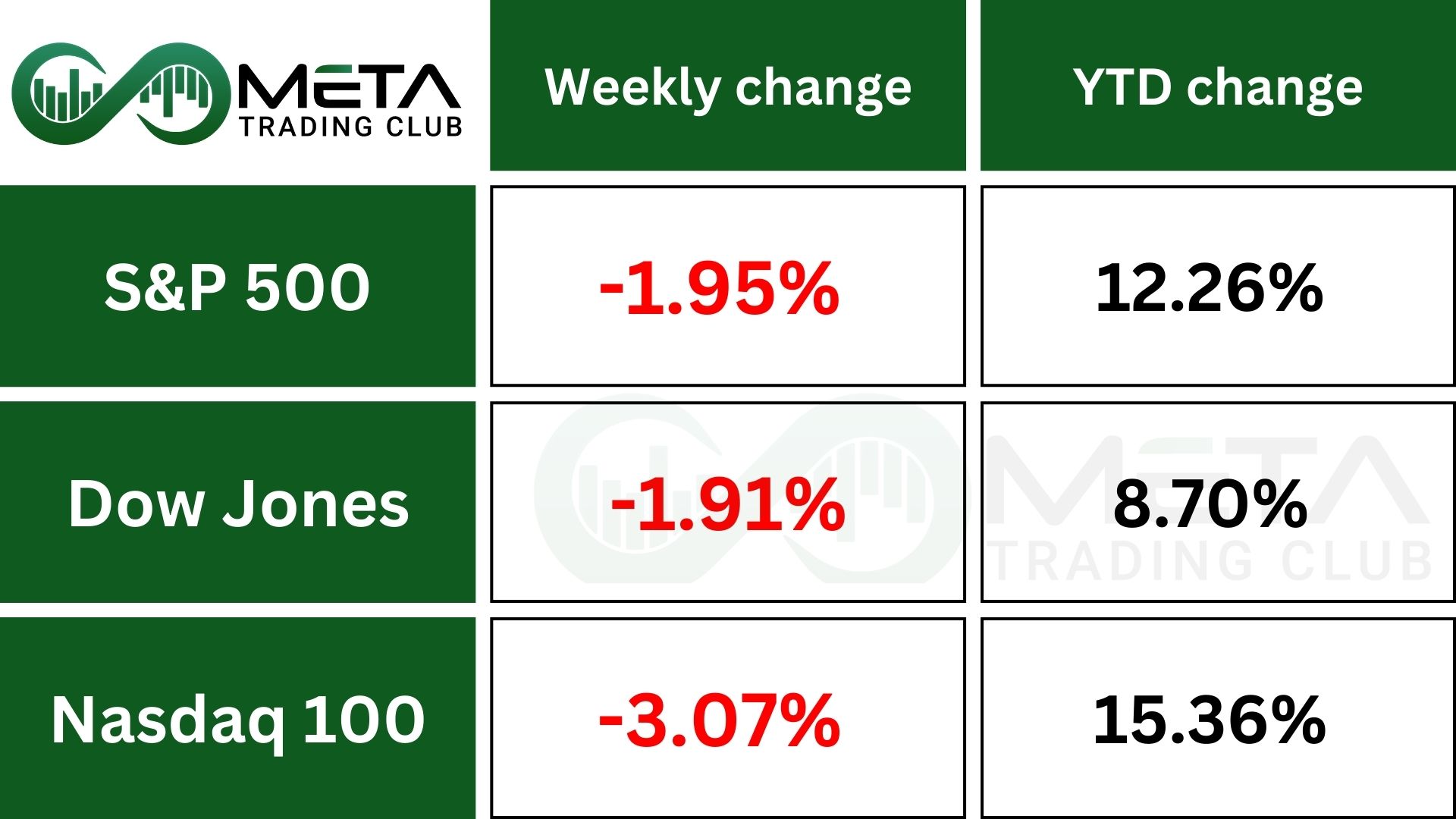

Indices’ Weekly Performance:

U.S. stocks rallied at the end of the week on rising expectations that the Federal Reserve could cut rates at its December 9–10 meeting, after New York Fed President John Williams signaled rates may fall “in the near term.”

Market odds of a cut jumped to 72% from 39% on Friday, sending Treasury yields lower and fueling a 2.8% surge in the Russell 2000, its biggest daily gain since August.

Despite the late rally, equities finished the week lower, with the S&P 500 down 1.95%, Nasdaq off 2.74%, Dow retreating 1.91%, and the Russell slipping 0.78%, its fourth straight weekly decline and longest losing streak since March.

After a strong sell-off last week, the SPX has now reached support at 5440. A hidden divergence is forming on both RSI and MACD, while the 100-day moving average stands as a critical psychological level. This zone carries high potential for a rebound.

Stocks

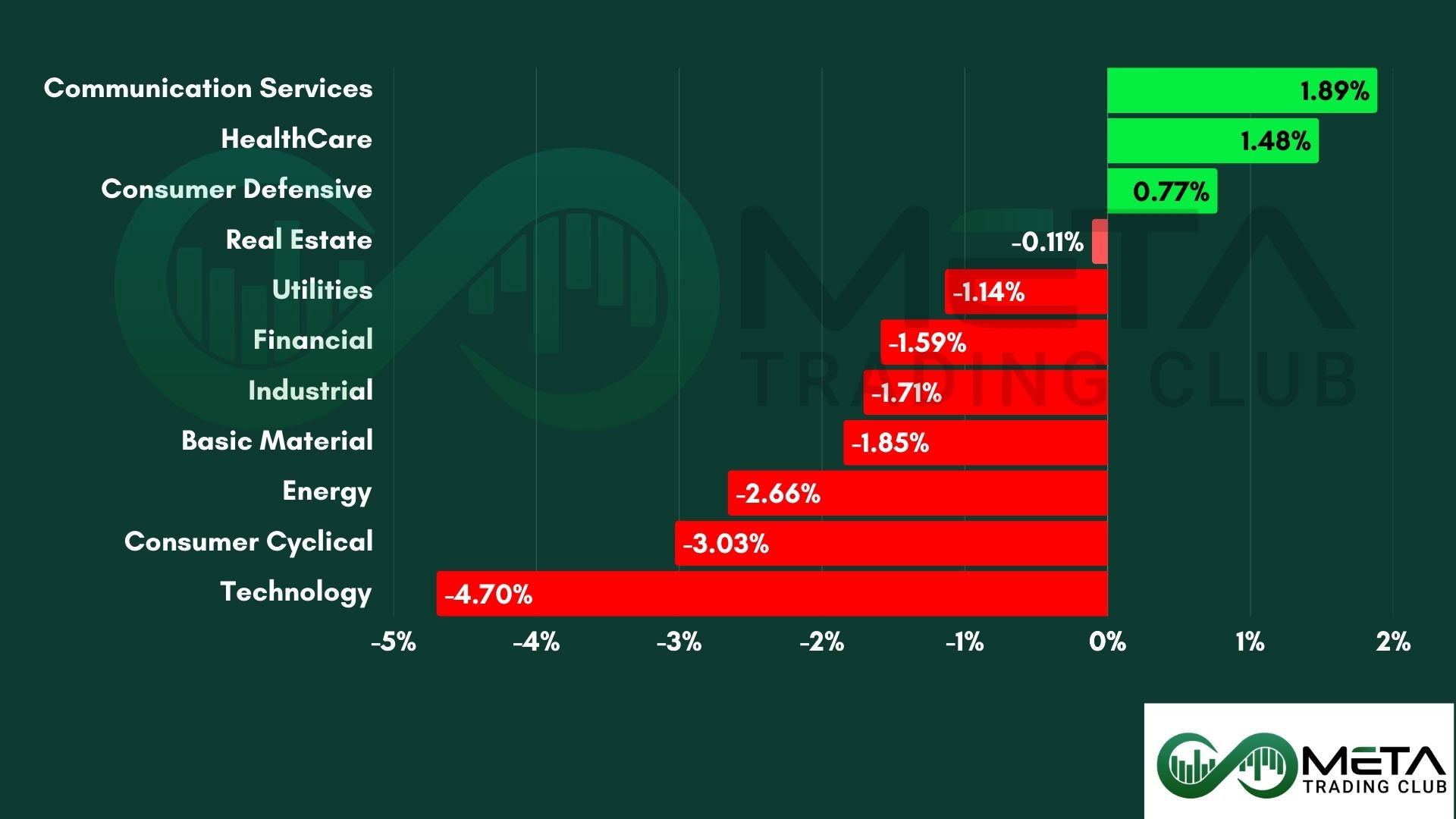

Sector’s Weekly Performance:

- Communication Services soared 1.89%, supported by Alphabet surged after Berkshire Hathaway revealed a $4.3B stake, and gained momentum around its Gemini 3 model and plans for large data centre investments

- HealthCare rose 1.48%, driven by pharma and medical device approvals. Regeneron jumped on the FDA approval of Eylea HD and strong pipeline updates.

- Basic Materials declined 1.85% pressured by weaker global demand and commodity price softness.

- Energy fell 2.6% as crude prices fell on peace talk signals and oversupply concerns.

- Consumer Cyclical dropped 3% as Tesla dropped on delivery concerns and valuation pressure.

- Technology plunged 4.7%, possibly due to AI bubble concerns and rate sensitivity. This was despite Nvidia’s impressive earnings.

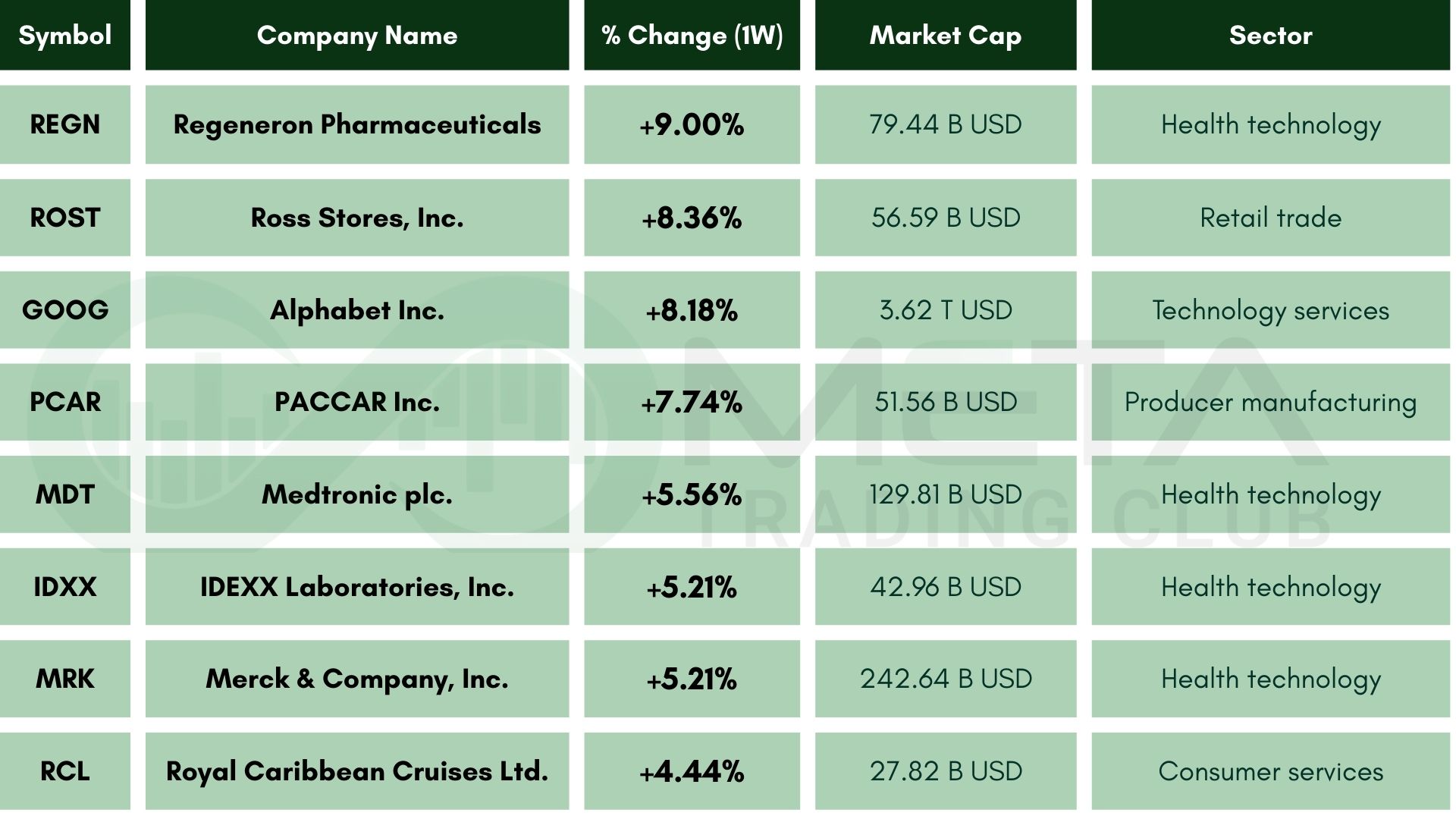

Top Performers

Last week saw a remarkable stock market performance, with several companies standing out as top gainers:

- Regeneron Pharmaceuticals (REGN): Climbed 9% after FDA approval of Eylea HD Injection for macular edema and upbeat pipeline updates.

- Ross Stores (ROST): Surged 8.4% on strong quarterly earnings with EPS and revenue beating forecasts and raised guidance.

- Alphabet (GOOG): Gained 8.2% as Berkshire Hathaway disclosed a $4.3B stake.

- PACCAR (PCAR): Rose 7.7% on analyst upgrades and steady demand in commercial trucking.

- Medtronic (MDT): Advanced 5.6% following approval of a new heart device and strong earnings showing growth in cardiac ablation solutions.

- IDEXX Laboratories (IDXX): Lifted 5.2% by analyst upgrade from Stifel and optimism around pet diagnostics innovation.

- Merck (MRK): Gained 5.2% on positive trial results for KEYTRUDA combinations and European approval for expanded use, strengthening its oncology pipeline outlook.

- Royal Caribbean Cruises (RCL): Up 4.4% after earnings beat expectations, driven by strong bookings and upbeat holiday demand despite rising costs.

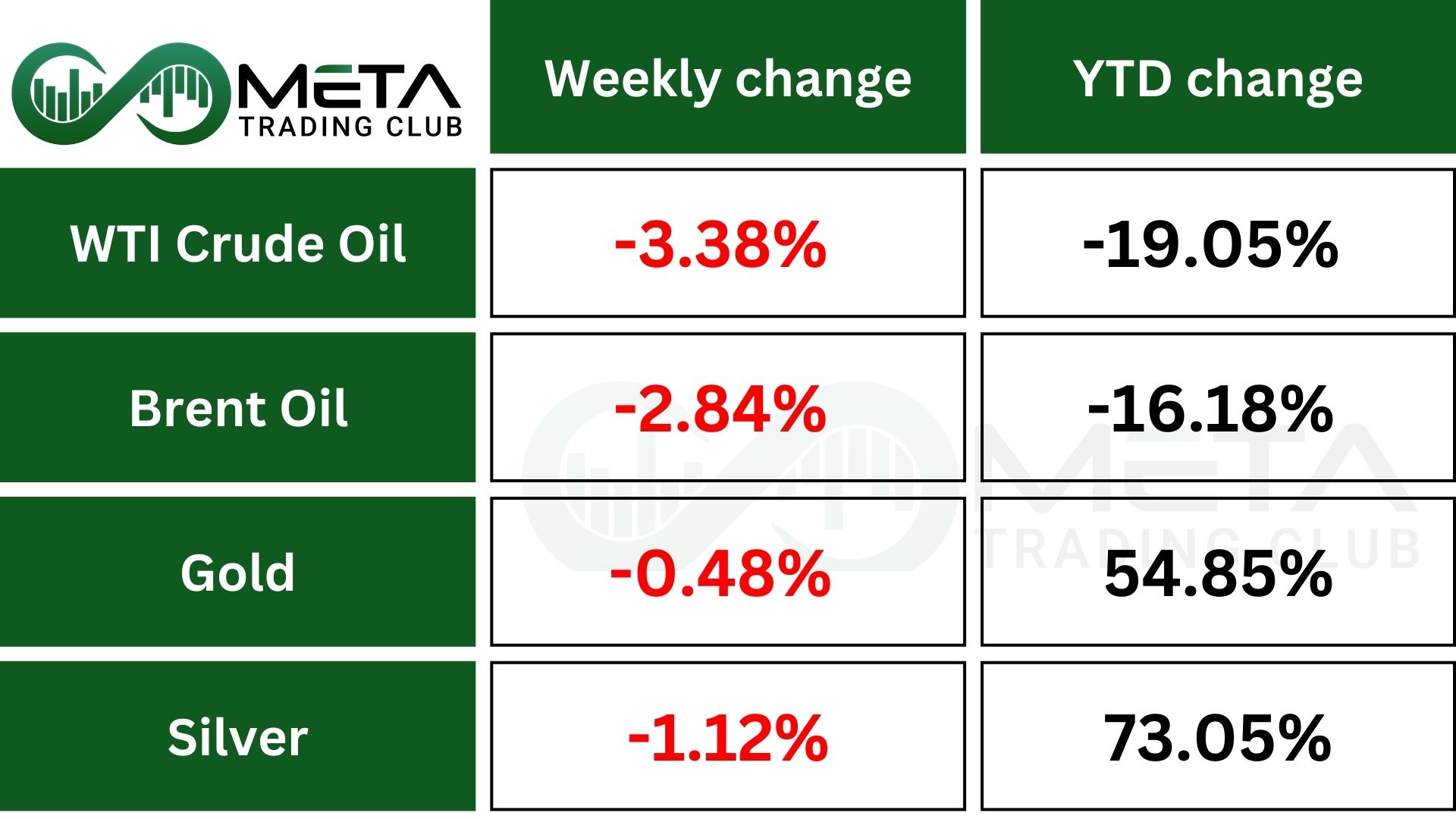

Commodity

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Gold is set for a weekly decline as investors weighed stronger US labor data, central bank signals, and softer bond yields.

Fed minutes showed a divided committee, though comments from the NY Fed president revived hopes of policy adjustment, pushing yields lower and supporting gold.

Crude oil dropped over 3%, hitting a one-month low after Ukrainian President Zelenskiy showed interest in peace talks. A US-Russia proposal, which may include Ukraine making territorial concessions and lifting sanctions, is set to be discussed with President Trump. This could lead to more Russian oil exports, raising concerns about oversupply.

Despite the talks, European diplomats doubt a deal will happen. At the same time, new US sanctions on Rosneft and Lukoil are now in effect, potentially stranding 48 million barrels of Russian crude at sea. Indian refiners, who often buy discounted Russian oil, are now looking for other suppliers. Overall, WTI crude fell more than 4% for the week.

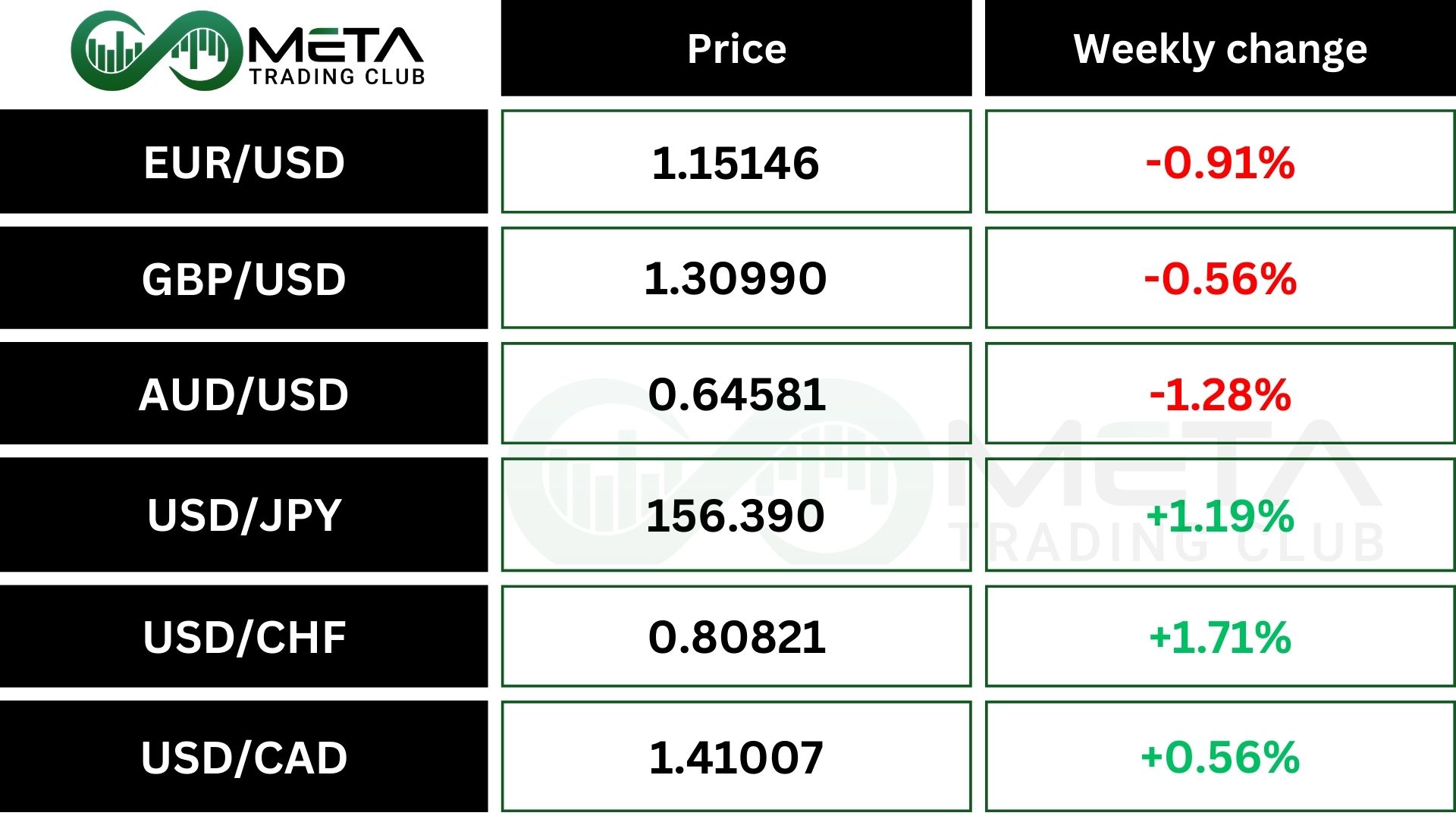

Forex

Weekly Performance of Major Foreign Exchange Pairs:

Dollar Index (DXY) posted its biggest weekly rise in six weeks, supported by strong demand against major currencies and rising expectations of a Federal Reserve rate cut in December, with market odds jumping to 71% after dovish remarks from New York Fed President John Williams.

The yen, despite a late rebound on verbal intervention from Japanese officials, still lost 1.2% for the week, pressured by fiscal concerns and skepticism over intervention credibility.

The euro fell 1% on weak manufacturing data, while sterling slipped 0.5% ahead of Britain’s budget.

Overall, the dollar index touched a 5-month peak, underscoring broad dollar strength despite Friday’s pullback against the yen.

Crypto

Cryptocurrency markets extended their decline for a fourth straight week, raising doubts about the durability of the bull cycle. Bitcoin fell to a six‑month low of $81,000, last seen in April, underscoring mounting pressure across the digital asset space.

Bitcoin fell sharply, reaching the $80K support zone. Hidden divergence is appearing on both RSI and MACD, suggesting potential for a rebound from this level. However, if the $80K zone fails to hold, the $70K area stands out as a strong and solid support where a pullback could occur.

Next Week’s Outlook

Economic Events

This week in the US, markets will be shorter because of Thanksgiving. Stock and bond markets will be closed on Thursday and will shut early on Friday.

Some government data is still being released after delays caused by the recent shutdown. Agencies may update their calendars with new release dates.

One key report is the September Producer Price Index (PPI). It’s expected to show a 0.3% increase in producer prices, after a 0.1% drop in August. The yearly rate may rise slightly to 2.7% from 2.6%.

Retail sales are forecast to grow by 0.4% in September, which is slower than August’s 0.6% gain. Durable goods orders are expected to rise just 0.2%, following a strong 2.9% jump the month before.

Other data to watch includes home price indexes (Case-Shiller and FHFA), business inventories, consumer confidence from the Conference Board, pending home sales, regional Fed reports from Richmond and Dallas, and the Chicago PMI.

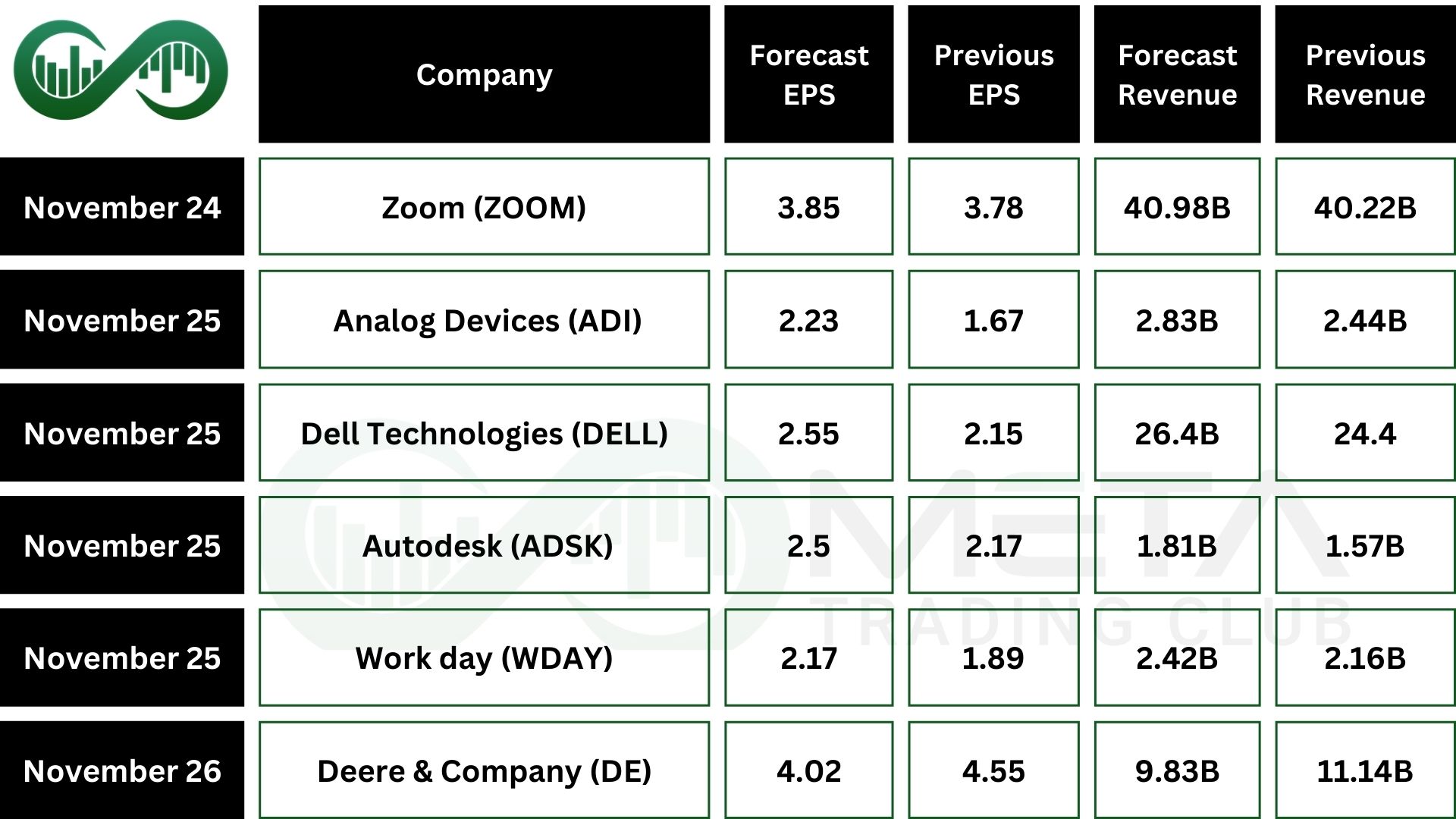

Earnings Events

This week’s earnings calendar is packed with major names across tech, retail, and industrials. Autodesk (ADSK), HP (HPQ), Workday (WDAY), Best Buy (BBY), Analog Devices (ADI), and Deere (DE) are all set to report.