Last Week’s report

Economic Reports

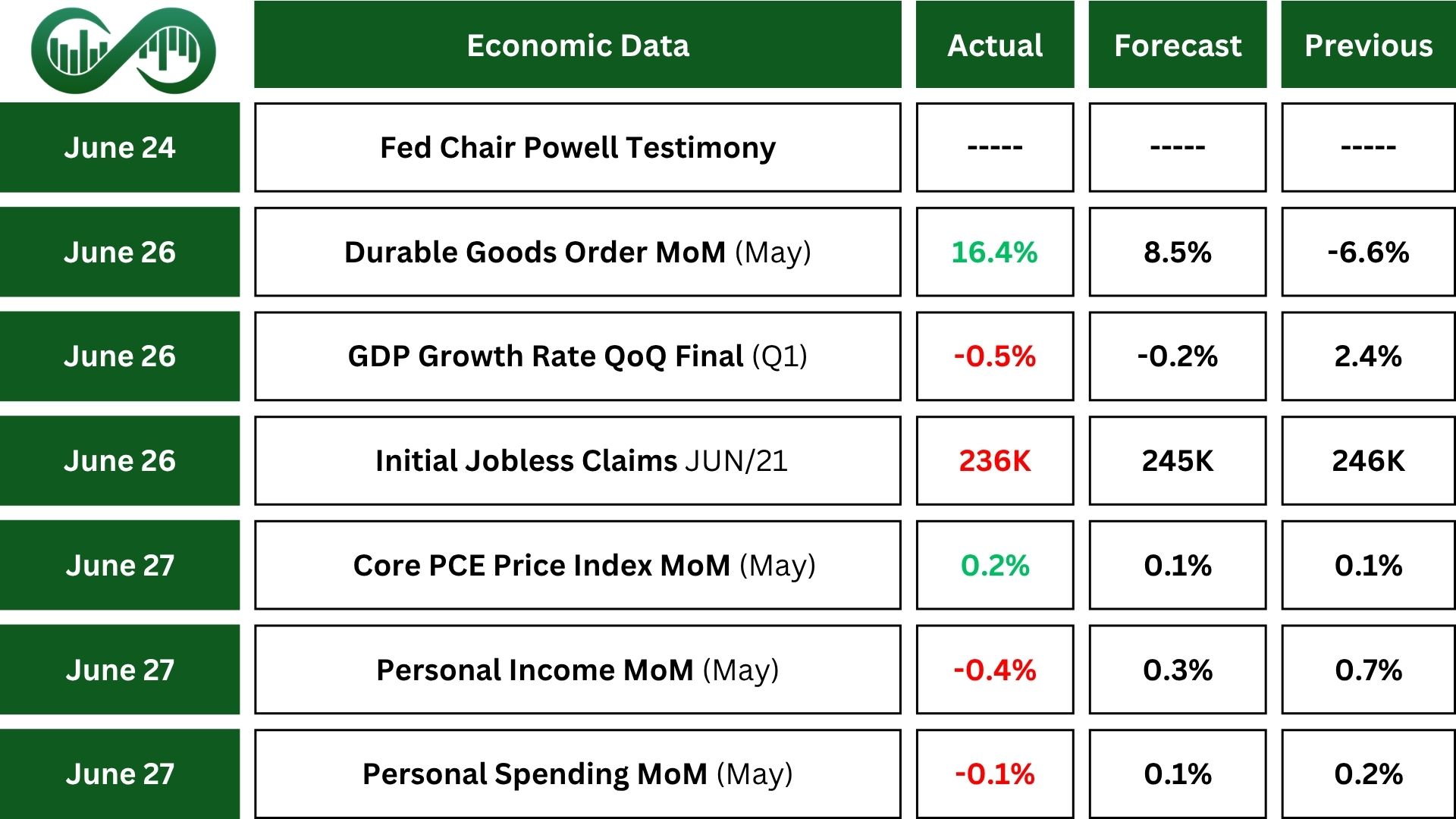

Fed Chair Powell signaled a cautious stance on interest rates, stating the Fed is in no hurry to adjust policy as it monitors the inflation impact of recent tariffs. While he left the door open to future rate cuts if inflation cools but avoided setting a timeline.

U.S. Durable Goods Orders jumped 16.4% in May, the biggest monthly gain since 2014. This followed a steep drop in April and was much higher than expected. The surge might signal a rebound in manufacturing that could help the economy grow.

The U.S. GDP growth shrank by 0.5% in the first quarter of 2025, down from 2.4% in the previous quarter. That drop was worse than expected. More imports and lower government spending were the main reasons for the decline.

Initial Jobless Claims in the U.S. dropped to 236K last week, better than expected. However, this is still above this year’s average, suggesting the job market is cooling off. Meanwhile, Continuing Jobless claims rose to nearly 2 million, the highest since 2021, indicating more people are having a tough time finding new jobs.

In May, Personal income in the U.S. fell 0.4%. This was the first drop since 2021, mainly due to lower business earnings and reduced government payments like Social Security. This was a notable shift from April’s gain and hints at weaker consumer spending ahead.

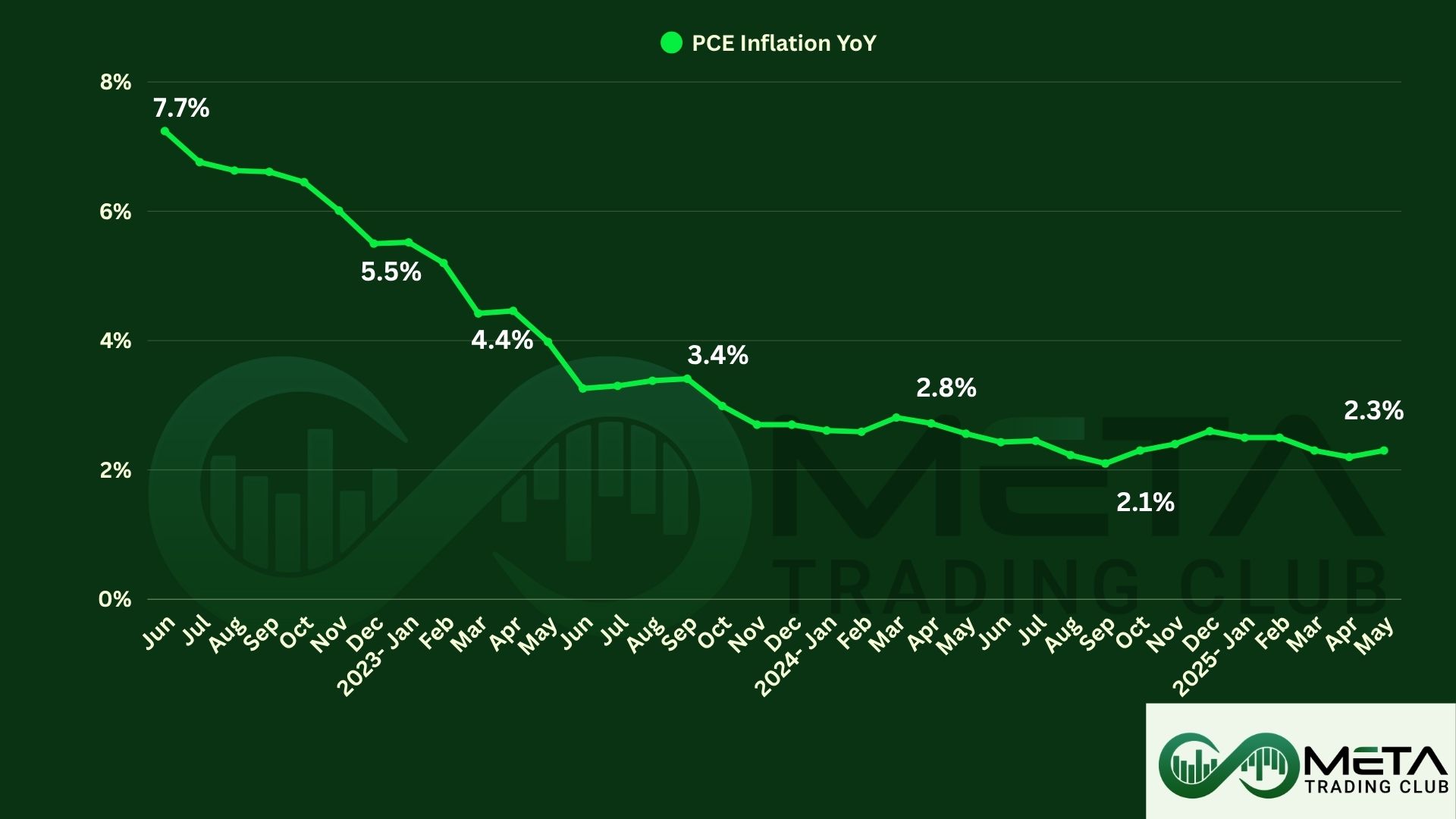

Meanwhile, PCE inflation stayed modest. Prices rose slightly, with the overall PCE index up 0.1%, and the core PCE rose 0.2%. Over the year, headline inflation was at 2.3%, and core inflation at 2.7%, both close to expectations.

In June, U.S. Michigan Consumer Sentiment improved 16%, marking the first increase in six months. People felt more positive about the future, although optimism hasn’t returned to late 2024 levels.

Also, Inflation expectations dropped. Short-term inflation expectation fell from 6.6% to 5%, and long-term to 4%. Still, many are worried about inflation and the impact of tariffs seem to be playing a big role.

Earnings Reports

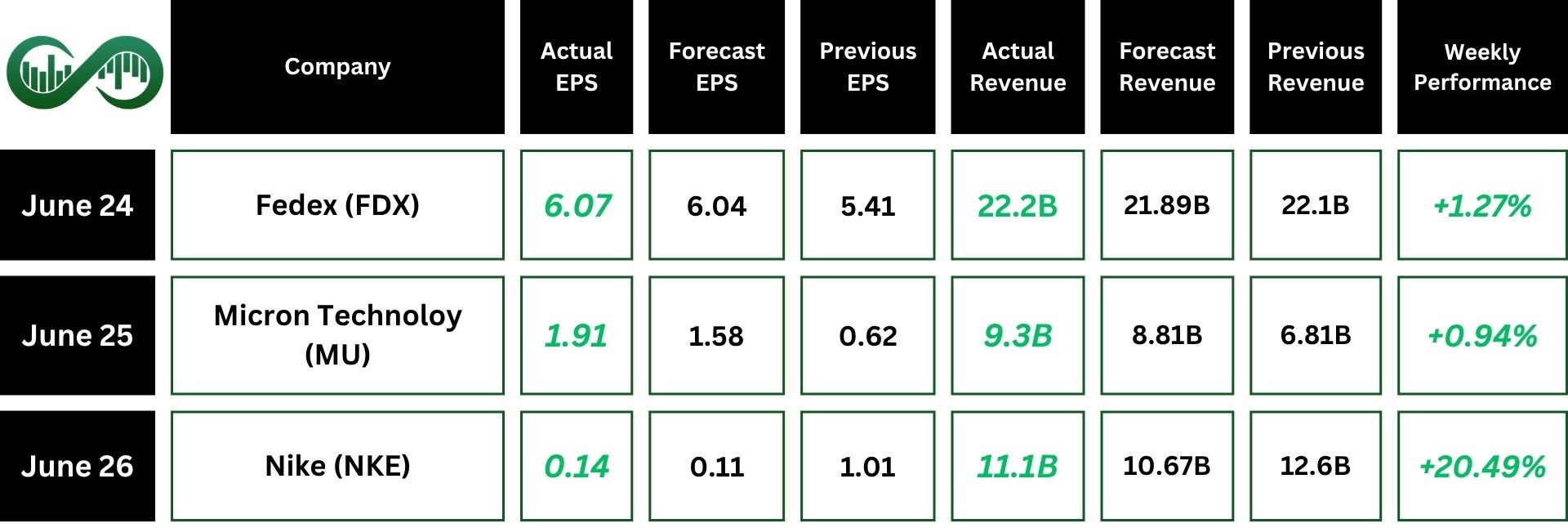

FedEx

FedEx (FDX) delivered a solid Q4, with earnings per share of $6.07 and $22.2 billion in revenue, both above forecasts.

The company also cut $2.2 billion in costs and kept capital spending at a record low.

FedEx returned $4.3 billion to shareholders and plans to boost its annual dividend by 5%.

However, its outlook for next quarter came in soft, with projected earnings below expectations. That, along with concerns about tariffs and trade tensions, pushed the stock down slightly after earning release.

Technically, FDX is experiencing a sharp pullback from its 100-day moving average, despite strong cost management and consistent earnings beats. A breakout above the $238 Fibonacci resistance could spark further upside, while a drop below the $214 support level might trigger deeper losses.

Micron

Micron (MU) posted strong Q3 results, beating expectations with $9.3 billion in revenue, boosted by demand for AI memory chips and growth in data centers. Earnings reached $1.91 per share, well above forecasts, and cash flow also improved.

The company declared a $0.115 dividend and expressed optimism about future growth.

Investors were encouraged, with the stock rising a bit after earnings were released. Despite some economic challenges, Micron’s position in the AI tech space looks solid.

Technically, MU has approached a strong resistance zone between $130 and $137. A breakout above $137 could signal continued upside. However, with weakening momentum, a break below the RSI uptrend line could lead to a further decline, potentially pulling the stock back from this zone.

Nike

Nike (NKE) beat expectations in Q4 with $11.1 billion in revenue and earnings per share of $0.14, despite sales dropping across all regions.

Gross margin declined to 40.3% as consumer demand softened.

Still, the strong earnings boost sent its stock up over 15% after the report. The company is now focusing on a comeback strategy, cutting reliance on China, boosting distribution (including a new Amazon partnership), and shifting back to its sports roots in hopes of driving a turnaround.

Technically, NKE has pierced the $70 resistance level with a gap up. If the stock holds above this level, further upside may be anticipated. However, a rejection from this zone could lead to a gap to fill to the downside.

Indices

Indices’ Weekly Performance:

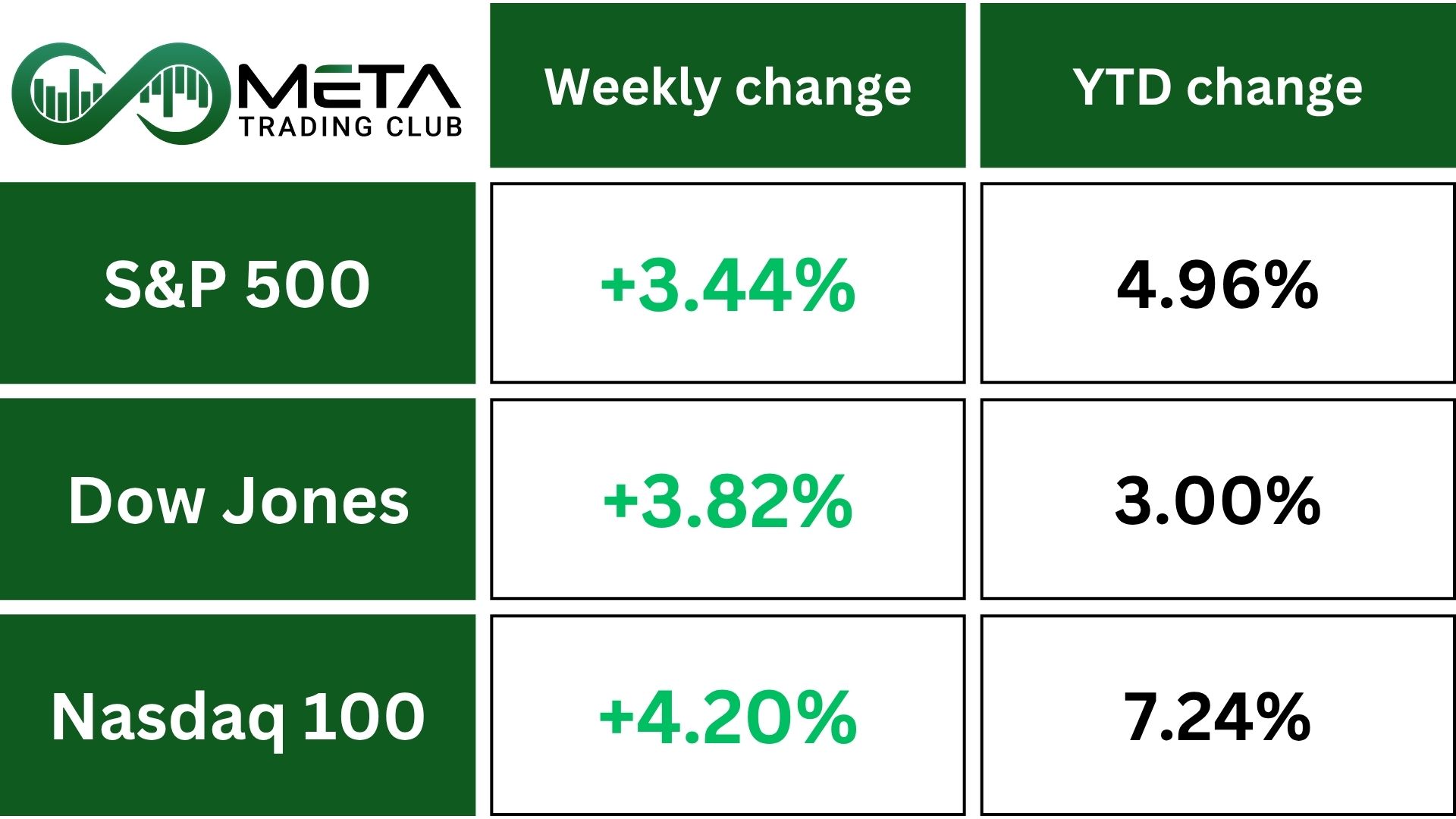

The S&P 500 ended its two-week losing streak with a strong 3.4% gain, driven by growing investor optimism over potential trade deals and anticipated interest rate cuts. On Friday, the index closed at a record high, surpassing its previous peak set back in February.

Meanwhile, the Nasdaq jumped 4.2%, marking its first record closing high since December. The Dow also showed impressive momentum, climbing 3.8% over the week. This broad rally signals renewed market confidence amid hopes for favorable economic developments.

Technically, SPX has reached and pierced its previous all-time high. If the index gains momentum reflected in the RSI, further upside could follow. However, if momentum fades, a pullback from this level may occur.

Stocks

Sector’s Weekly Performance:

Most parts of the stock market rose, with technology and communication companies seeing the biggest gains. Only real estate and energy stocks moved lower.

- Communication services led the market last week with a 5.7% gain. Meta (META) climbed 7.5%, lifting the communication services group after reports of advanced talks to acquire AI voice startup PlayAI and the hiring of AI researchers from OpenAI.

- Technology surged 4.8% as Nvidia (NVDA) hit a record high with its market cap surpassing $3.8 trillion, fueled by an analyst’s bullish AI outlook. Micron (MU) also rallied on upbeat revenue guidance tied to AI chip demand. The Semiconductor Index jumped 6.4%.

- Consumer Discretionary climbed 4%, with Nike (NKE) soaring 20.5% for the week after announcing plans to shift production out of China to reduce tariff exposure. Carnival (CCL) gained after raising its profit forecast on booming cruise demand.

- Financials advanced 3.4%. Northern Trust (NTRS) rose on news of a potential merger approach by Bank of New York Mellon (BK). S&P 500 Banks Index and KBW Regional Banking Index both ended the week up around 5%.

- Industrials gained 3.4%. Although FedEx (FDX) slipped midweek on a cautious profit outlook, it still managed to close the week up 1%.

- Real Estate edged down 0.45%. New York-focused REITs like Vornado (VNO) declined amid political uncertainty as Mamdani emerged as the frontrunner in the city’s Democratic mayoral race. Equinix (EQIX) plunged 11%, the S&P 500’s biggest loser, after issuing a weak revenue forecast.

- Energy dropped 3%, pressured by easing geopolitical tensions after an Israel-Iran ceasefire reduced the risk to Middle East oil supplies.

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- Nike (NKE): Surged 20% due to better-than-expected earnings and a bold restructuring plan. The company is cutting reliance on Chinese manufacturing to reduce tariff risks and is doubling down on sports-focused branding.

- Arista Networks (ANET): Jumped 15% after stocks has been rated higher to mean price target of 109$.

- Carnival (CCL): Rose nearly 15% after raising its annual profit forecast, boosted by record-breaking cruise demand and strong summer bookings.

- Coinbase (COIN): Climbed 14.6% as crypto markets rebounded with higher trading volumes.

- Arm Holdings (ARM): Gained 14.1% thanks to its perceived position at the heart of the AI revolution, given that its architecture underpins a vast number.

- Royal Caribbean (RCL): Advanced 13.6% amid the booming cruise industry. Strong pricing power and a healthy booking pipeline lifted investor sentiment.

- Advanced Micro Devices (AMD): Rose 12.1% after CFRA Research upgraded its rating to “strong buy” and raised its price target significantly.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold (XAU/USD capping a 3% weekly loss, its second in a weekly loss in row, as easing geopolitical tensions and progress on global trade reduced safe-haven demand.

A truce between Israel and Iran held, and U.S. officials hinted at nearing trade deals with major partners. Meanwhile, U.S. inflation data remained modest, and consumer confidence improved, fueling hopes for Fed rate cuts.

Still, gold remains up more than 25% this year, supported by central bank buying and expectations of monetary easing.

Technically, Gold has broken below its upward trendline. If it remains under this level at the weekly open, further downside toward Fibonacci support zones may be expected.

WTI Crude Oil saw sharp weekly losses as easing tensions between Israel and Iran and the absence of supply disruptions stripped away much of the geopolitical risk premium.

There is a sign that oil futures are now entering a consolidation phase, supported by tighter U.S. inventories, a weaker dollar, and increased seasonal demand from the driving season.

However, rising output from OPEC is acting as a headwind. The market appears to be stabilizing near levels seen before the Iran-related conflict began. By week’s end, WTI dropped 11% on the week, marking a 12% weekly loss.

Forex

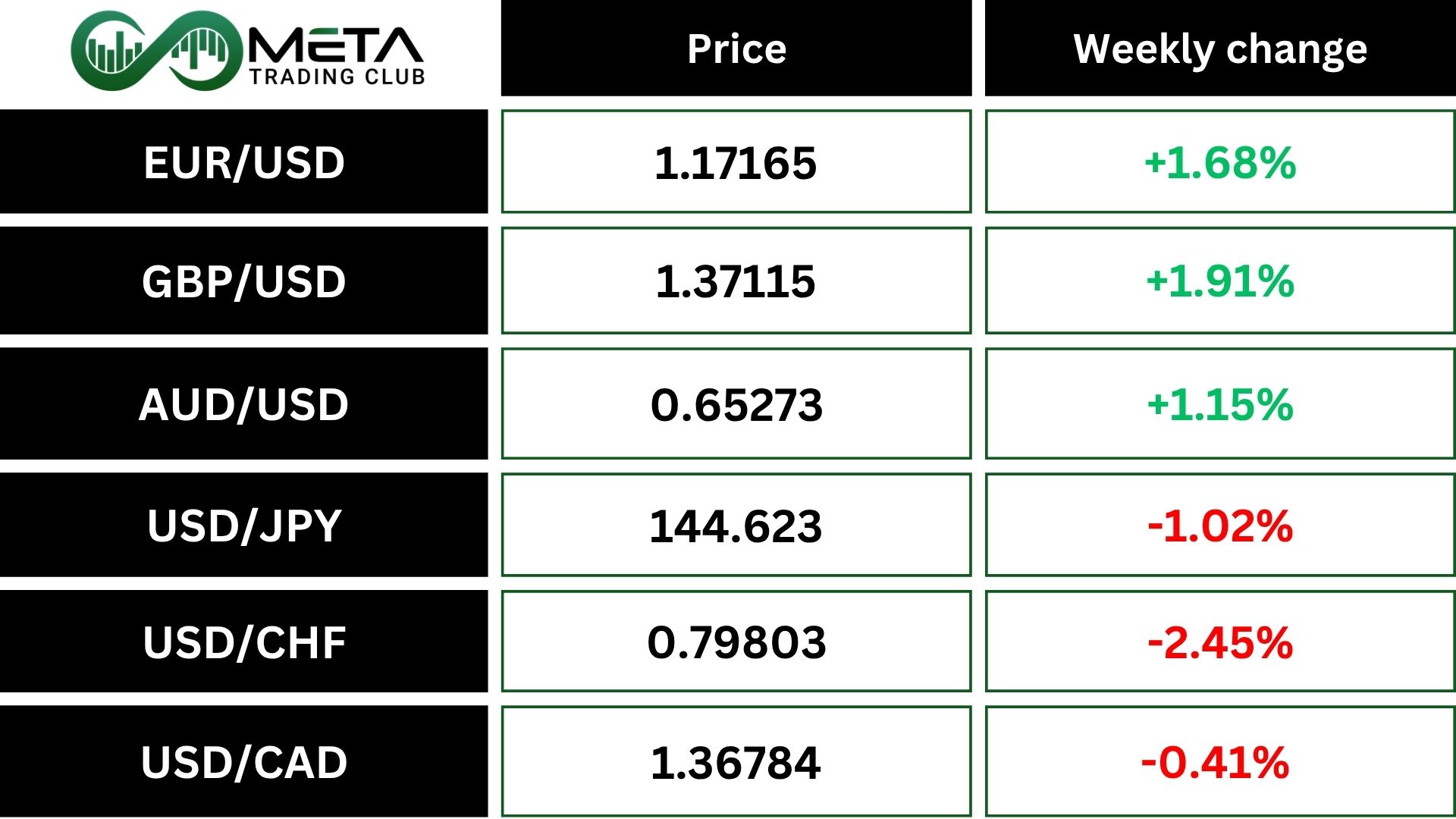

Weekly Performance of Major Foreign Exchange Pairs:

The EUR/USD has climbed to its highest level since 2021. It rose after the U.S. released May’s inflation data, which showed slightly higher core inflation and weaker-than-expected consumer spending and income.

The GBP/USD climbed 2% this week to $1.373, its biggest gain in nearly four months and close to a four-year high. The rally was driven by a weaker U.S. dollar, softened by fading geopolitical tensions and speculation over Federal Reserve leadership changes. The pound was also buoyed by the Bank of England’s cautious stance on rate cuts amid stubborn UK inflation, though domestic politics grew tense as Prime Minister Starmer faced pushback on welfare reforms.

The U.S. Dollar Index (DXY) hovered near its lowest level since March 2022, marking a 2.3% drop for June and its sixth consecutive monthly decline. The index is down over 10% this year, as concerns grow that Trump’s tariffs could hurt U.S. economic growth. Traders are also closely watching for breakthroughs on new trade deals before the July 9 deadline for implementing the administration’s “reciprocal” tariffs.

Technically, DXY has reached oversold territory on the weekly RSI as it tests the $97 support zone. Given the oversold conditions, a potential rebound from this level is possible. However, if the index breaks below this support and confirms the breakdown, further downside toward lower support levels could follow.

Crypto

Crypto Market Weekly Performance:

Previous week, Bitcoin (BTC) and Ethereum (ETH) bounced back after a dip caused by global tensions. Bitcoin recovered more strongly than Ether and even climbed back from $98,000 to $108,000. ETH also rebounded but didn’t fully recover, ending the week lower than it started.

Despite Bitcoin’s strength, its overall dominance dropped slightly. That doesn’t necessarily mean a new “alt season” is around the corner. ETH showed more volatility and less stability as a safe haven compared to BTC.

The recent moves show that investors might be leaning toward riskier assets again. However, optimism about a big altcoin rally is fading, as traders wait to see if Bitcoin will settle down and spark interest in smaller coins like it has in past market cycles.

Technically, if BTC breaks down the uptrend line, it could trigger a drop. However, a break above $111,000 may lead to further gains.

Next Week’s Outlook

Economic Events

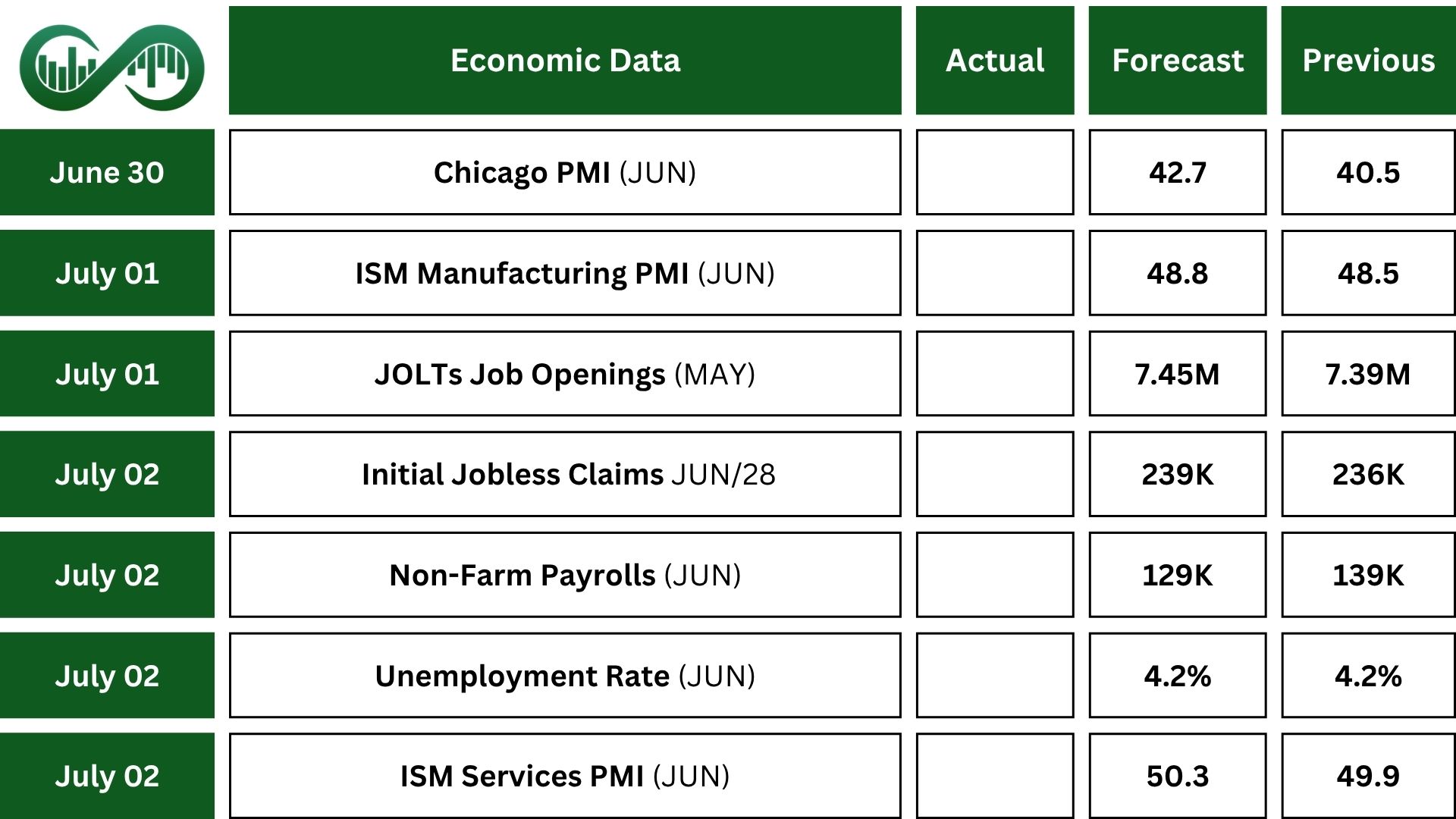

With the U.S. observing a shortened trading week due to the Independence Day holiday, investor attention will center on the June employment data, which is anticipated to signal further easing in the labor market.

Nonfarm Payrolls are projected to rise by 129,000 (down from May’s 139,000) while the Unemployment Rate is expected to remain unchanged at 4.2%. Wage growth may decelerate slightly, edging down to 0.3% from 0.4%.

Additional labor market insights will come from the JOLTS report, with job openings forecast to increase to 7.45 million, and the ADP employment report, which is expected to show private sector job gains of 80,000, up from 37,000.

Among key indicators, the ISM Manufacturing PMI is likely to reflect continued contraction, whereas the ISM Services PMI could suggest a mild recovery.

The trade deficit is anticipated to widen. Also on the data docket are final S&P Global PMIs, the Chicago PMI, the Dallas Fed’s manufacturing and services surveys, construction spending figures, Challenger job cut announcements, and factory orders.

Earnings Events

The earnings season has wrapped up, with no significant reports expected in the week ahead.