Last Week’s report

Economic Reports

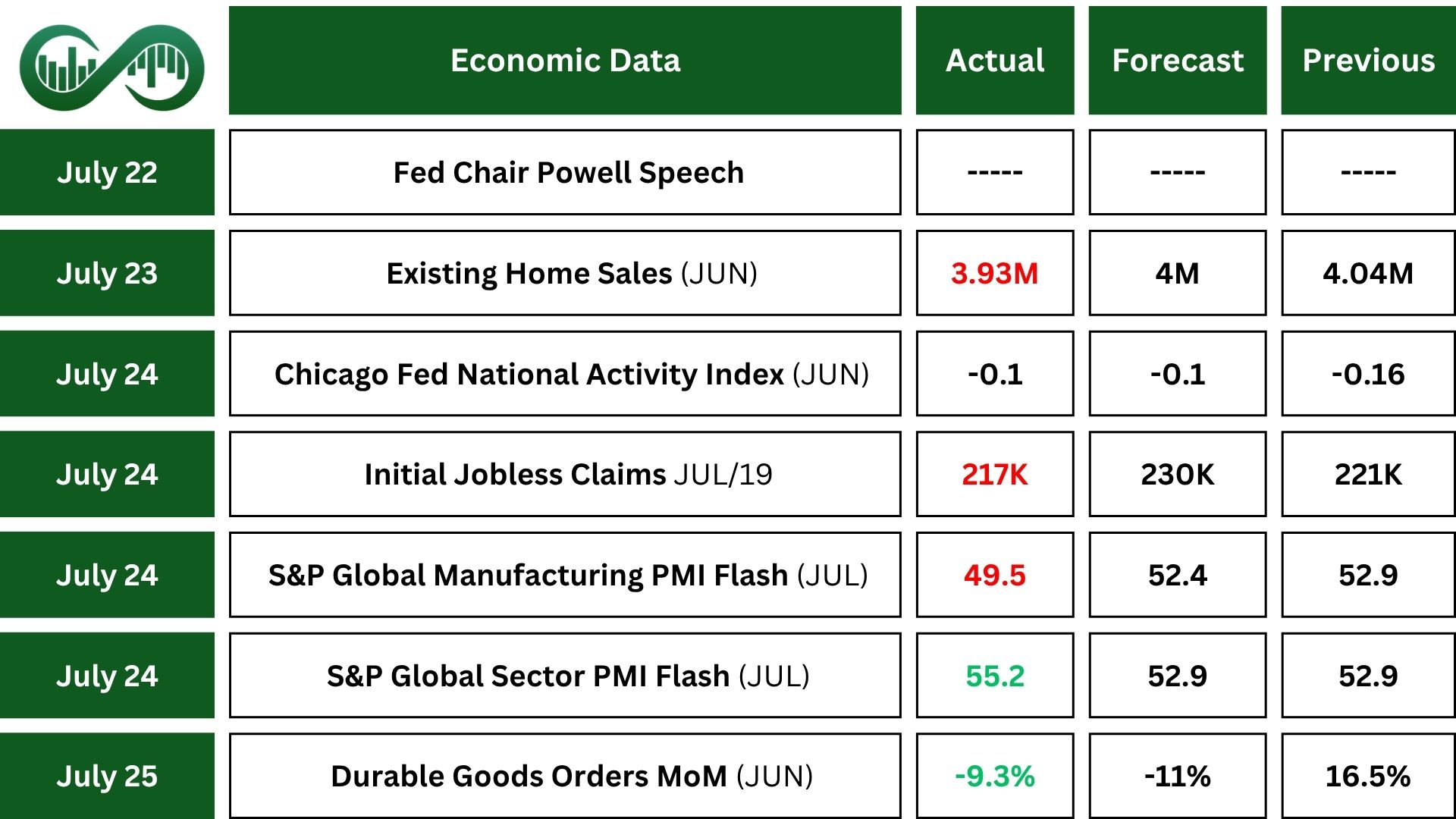

U.S. existing-home sales dropped by 2.7% in June, falling to an annualized rate of 3.93 million units from 4.04 million in May, missing market forecasts of 4.0. This marks the slowest pace of sales since September 2024.

In June, the Chicago Fed National Activity Index (CFNAI) rose modestly to -0.10 from -0.16 in May, marking the third consecutive month below zero. This sustained negative reading suggests that economic activity continues to lag behind its long-term trend. While production and personal consumption indicators showed slight improvement, their contributions remained negative. Overall, the data points to a sluggish economic environment, with softening labor market conditions and waning business momentum potentially raising concerns about the durability of future growth.

In the third week of July, initial jobless claims in the U.S. fell to 217,000, defying market expectations for an increase to 227,000. This marked the sixth consecutive weekly decline and the lowest level since April, underscoring continued strength in the labor market despite prior concerns earlier in the year.

However, continuing claims edged higher to 1.955 millions, slightly below expectations but still the second-highest since November 2021. This suggests that while layoffs remain low, hiring momentum may be slowing.

Durable goods orders in the U.S. fell by 9.3% in June to $311.84 billion, reversing a sharp 16.5% surge in May and coming in slightly better than the expected 10.8% drop. The decline was driven primarily by a steep pullback in transportation equipment, especially nondefense aircraft and related parts, and nondefense capital goods.

This data reflects while underlying industrial demand remains steady, business investment may be facing headwinds.

Earnings Reports

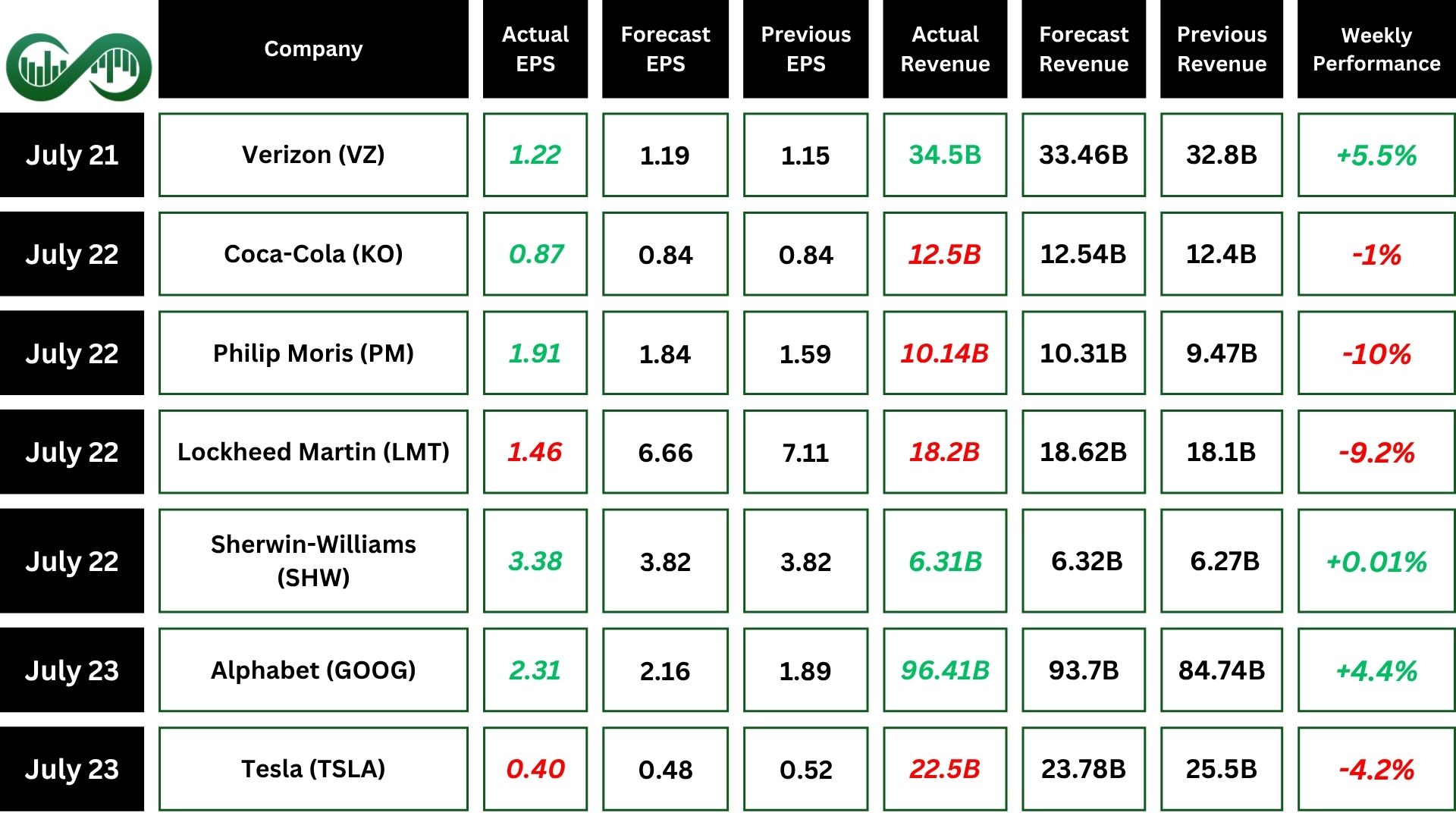

Alphabet

Alphabet (GOOG) delivered a robust Q2, with revenue climbing 14% to $96.4B and EPS jumping 22% to $2.31. All segments posted double-digit growth, with Cloud surging 32% thanks to AI-driven demand.

Strong margins, improved profitability, and a bold $85B capital spending plan reinforced investor optimism.

This earnings report sent stock up over 4% Last week.

Tesla

Tesla (TSLA) Q2 results reflected a transitional phase, as the company leaned deeper into AI, robotics, and autonomous tech amid weakening EV demand and lower vehicle prices.

Revenue fell 12% to $22.5B and EPS missed estimates, while rising R&D costs cut margins to just 4.1%.

Reported modest energy growth and the launch of its Robotaxi service. Hence,shares fell over 4% last week, as concerns mounted over scalability, regulatory hurdles, and declining auto sales.

Tesla remains committed to innovation, supported by $36.8B in cash and the rollout of a new affordable EV later this year.

GE Vernova

GE Vernova (GEV) posted a strong Q2, with $9.1 billion in revenue, up 11% year-over-year. Also, EPS of $1.86 that topped forecasts.

Orders rose to $12.4 billion, driven by robust Power equipment and services, while margin gains came from volume growth, pricing, and productivity.

Although free cash flow dipped due to a prior-year refund, outlook upgrades for revenue. Investors responded positively, sending the stock up 5% on revised full-year guidance and resilient performance across its Power and Electrification segments.

T-Mobile US

T-Mobile US (TMUS) delivered a standout performance in Q2, achieving industry-leading growth in postpaid and 5G broadband customer additions, which fueled record-high earnings and cash flow.

The company reported $17.4 billion in service revenue and $3.2 billion in net income, with EPS reaching $2.84, its highest ever for a second quarter.

Strengthened by robust customer momentum and operational efficiency, T-Mobile raised its full-year outlook and returned $3.5 billion to shareholders, driving a more than 7% surge in its stock price following the report.

Intel

Intel (INTC) Q2 reported revenue slightly beating expectations at $12.9 billion, but deep restructuring and impairment charges drove a net loss of $2.9 billion and EPS of –$0.67.

Despite efforts to streamline operations and reduce costs, including a 15% workforce cut and canceled projects across Europe, investors were rattled by declining margins, negative free cash flow, and cautious guidance.

The stock fell nearly 9% post-earnings and is down 22% year-to-date, reflecting market skepticism around Intel’s turnaround strategy and financial outlook.

Indices

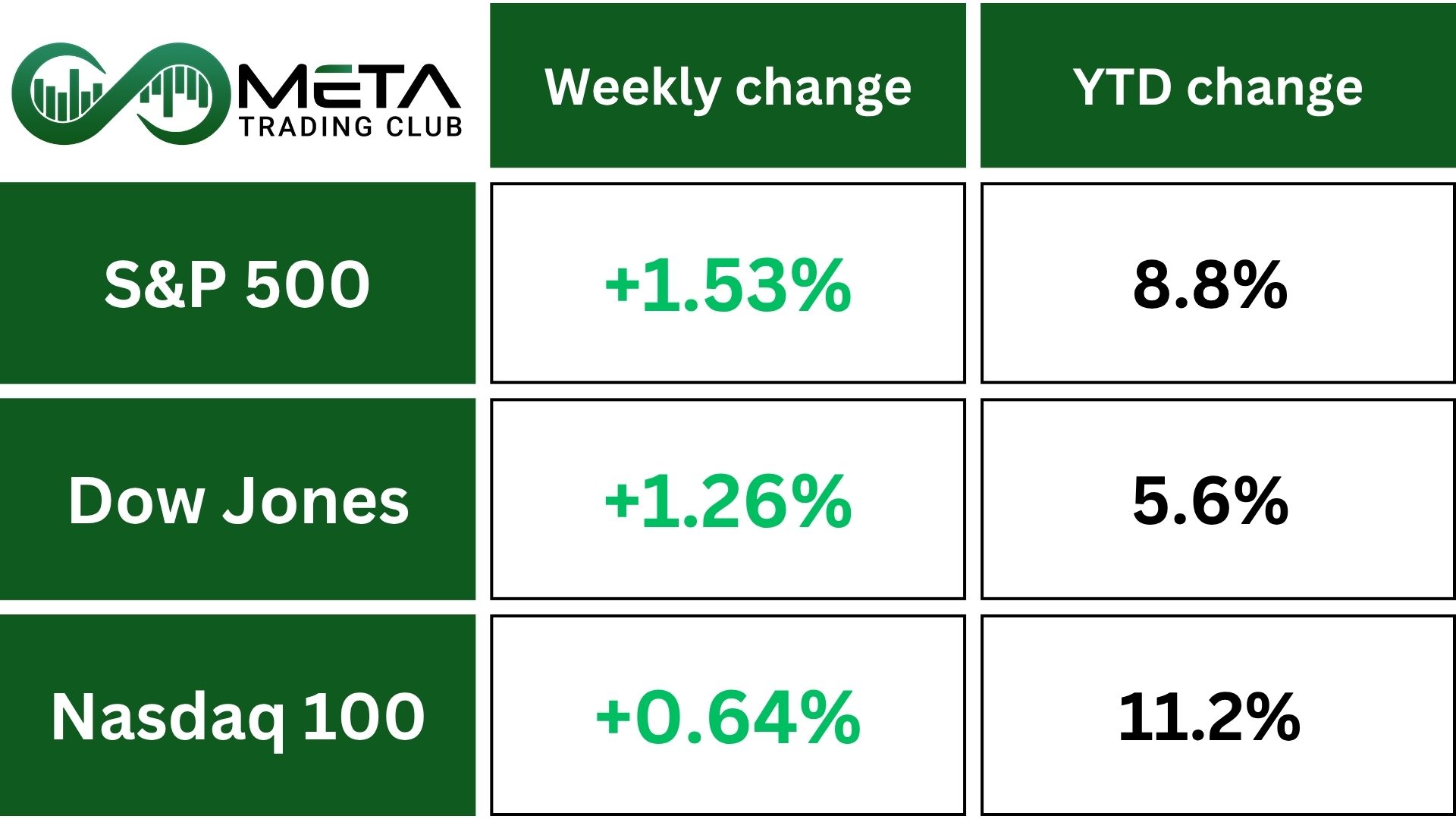

Indices’ Weekly Performance:

Stocks climbed last week, with the S&P 500 and Nasdaq hitting new highs after a week dominated by tariff developments and corporate earnings.

The S&P 500 marked its fifth consecutive record close, its longest streak in over a year.

Optimism around trade negotiations supported market momentum. President Trump is scheduled to meet the European Commission President, as signals point toward a potential breakthrough. On Friday, he described the likelihood of a deal with the EU as “about 50-50.”

Separately, the administration secured trade agreements with Japan and the Philippines, but talks with Canada and Mexico (two key trading partners) remain unresolved ahead of the August 1 deadline. Trump noted that discussions with Canada haven’t made much progress.

Meanwhile, the deadline to raise tariffs is this Friday, August 1, but many countries still haven’t joined the talks.

At the same time, investors are waiting for earnings from four major tech companies: Meta, Microsoft, Amazon, and Apple.

Technically, if SPX keeps upward momentum, the index could potentially trigger a further rally toward 6500. However, if the RSI trend line fails and breaks down RSI trend line, it could signal weakening momentum, putting 6300 at risk and potentially dragging the index down to its key support near 6150.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold

Gold (XAU/USD) dropped to $3,336.5 per troy ounce and are on track to end the week down 0.6%.

Earlier in the week, worries about the U.S.-EU trade conflict pushed prices higher, but hopes for more trade deals (starting with an agreement between the U.S. and Japan) brought gold back to a quieter range.

Gold is also under pressure from fading chances of a Federal Reserve rate cut. If prices fall below the 50-day moving average next week, it may signal a deeper price correction rather than just temporary consolidation.

Technically, Gold has been moving sideways in recent weeks, stuck within a narrow trading band. For the bullish trend to pick up again, prices need to break past the all-time high. A potential early signal could come from the RSI breaking its downward trend line, possibly pushing gold toward that ATH resistance.

On the flip side, a break below the short-term uptrend line might indicate weakening momentum and open the door to further downside.

Crude Oil

WTI Crude Oil pressured by weak economic signals from both the U.S. and China. Over the week, prices dropped as rising global supply and slower business investment weighed on sentiment.

Even so, optimism over possible U.S. trade deals with the EU, Japan, and others helped cushion losses, with hopes these agreements could boost economic activity and drive oil demand.

The U.S. is also preparing to let Chevron and other companies resume limited operations in Venezuela, potentially increasing exports of heavier crude by more than 200,000 barrels a day and relieving supply tightness.

Looking ahead, OPEC+ is expected to raise production at Monday’s meeting as the group aims to reclaim market share during peak summer demand.

Meanwhile, U.S. oil and gas rigs continued to decline for the 12th time in 13 weeks, pointing to possible weakness in future domestic output.

Forex

Weekly Performance of Major Foreign Exchange Pairs:

DXY: The U.S. dollar index dipped 0.8% for the week to 97.45, its weakest weekly performance in a month. However, at the end of week recovered, aided by solid U.S. economic data and clearer trade negotiation signals. Still, political pressure on the Fed and limited rate-cut expectations kept gains in check.

EURUSD: The euro was flat at $1.1741 but poised for a weekly gain of nearly 1%, its best showing in a month. Support came from the ECB’s positive tone on the economic outlook and hopes of a near-term EU-U.S. trade deal. Euro zone bond yields also outpaced British ones, lifting the euro against the pound.

USDJPY: The dollar fell 0.9% against Yen last week, its lowest since June 23. Softer Tokyo inflation data weighed on the yen, although political uncertainty from Japan’s upper house elections may complicate the BOJ’s path forward.

Crypto

Crypto markets are surging, with total market capitalization once again breaching the $4 trillion mark as Bitcoin and Ethereum lead the charge.

Bitcoin extended its weekend rally, climbing to above $119,000, fully bouncing back from Friday’s dip and sitting just 2.8% below its record high.

Ethereum is showing even stronger momentum, rising to surpass $3,900, its highest level in seven months, boosted by ETF flows and increased demand from corporate treasuries. Over the past month, ETH has soared 60%.

Among altcoins, Binance Coin (BNB) hit a new all-time high of $850, while Bitcoin Cash (BCH) and Avalanche (AVAX) also saw notable gains.

Technically, if BTC breaks above 120K and gains confirmation on lower timeframes, it could rally toward its all-time high. But if it slips below the $115K level, that may signal further downside, with the next support zone likely coming into play.

Next Week’s Outlook

Economic Events

This week is packed with a wave of high-impact economic events. The Federal Reserve is expected to keep the federal funds rate unchanged at 4.25% to 4.50%, maintaining a cautious “wait-and-see” approach.

U.S. Q2 GDP is projected to rebound to 2.5%, following a 0.5% contraction in Q1 largely attributed to a spike in imports.

Labor market signals may soften, with July nonfarm payrolls likely increasing by just 102K, the weakest gain since February. The unemployment rate is expected to inch up to 4.2%, while average hourly earnings may rise by 0.3% month-over-month.

Inflation pressures are also in focus, as June’s core PCE price index is seen rising 0.3%, versus 0.1% in May. Personal income and consumer spending are both anticipated to show modest improvements.

Beyond this, an extensive lineup of data releases includes ISM Manufacturing PMI, JOLTs job openings, ADP employment change, advance trade balance and wholesale inventories, Case-Shiller home prices, pending home sales, the employment cost index, and regional indicators like the Dallas Fed Manufacturing Index and Chicago PMI.

Earnings Events

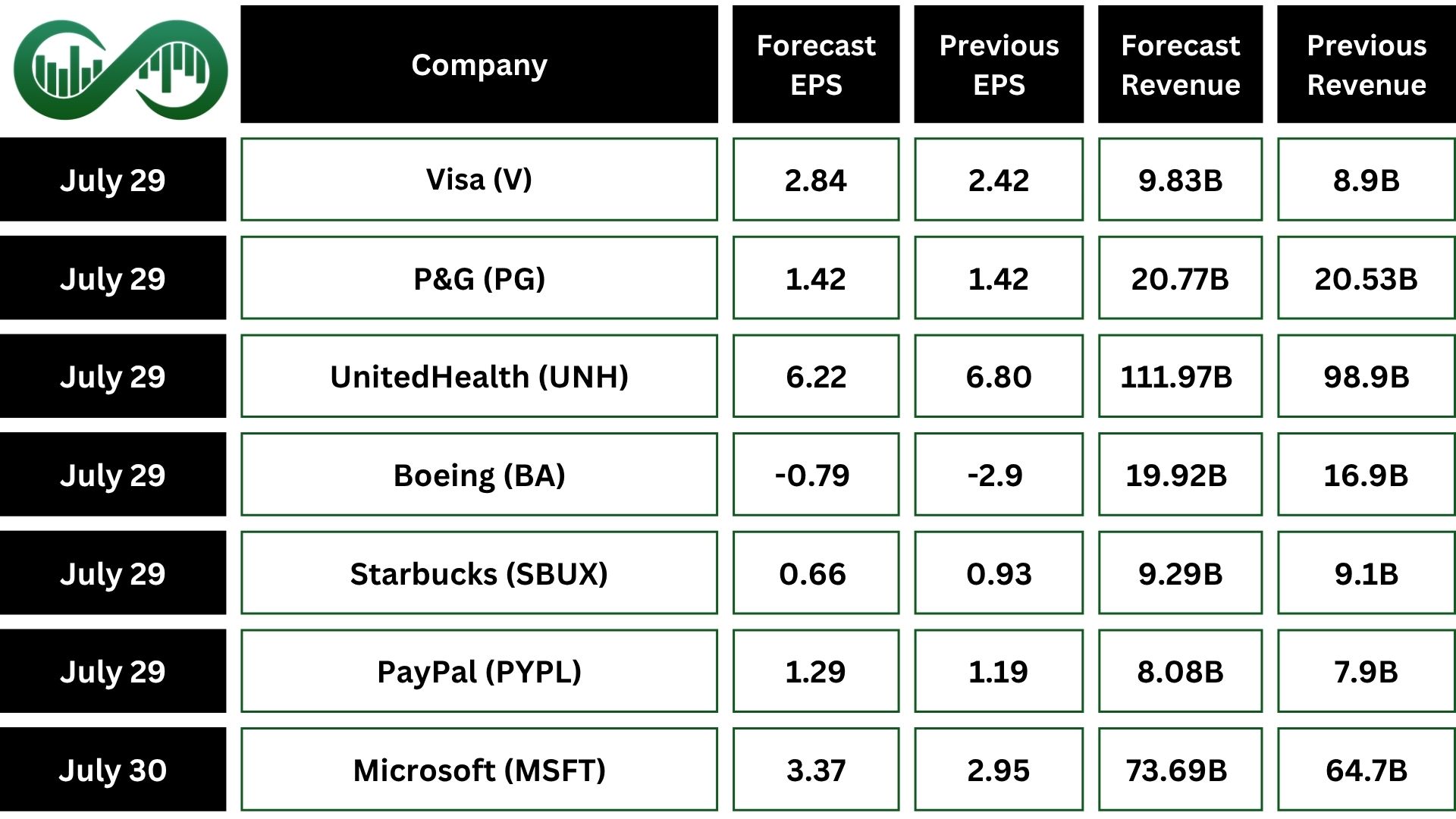

This week marks the peak of the earnings season, with tech giants Microsoft (MSFT), Meta (META), Apple (AAPL), and Amazon (AMZN) in the spotlight.

The calendar is stacked with major reports from companies across sectors, including Boeing (BA), PayPal (PYPL), Procter & Gamble (PG), Spotify (SPOT), UnitedHealth (UNH), Starbucks (SBUX), Visa (V), Mastercard (MA), Merck (MRK), Qualcomm (QCOM), American Tower, ADP, Altria, Etsy, ARM Holdings, Kraft Heinz, Ford, AbbVie, S&P Global, Comcast, Chevron, and Exxon Mobil.