Last Week’s report

Economic Reports

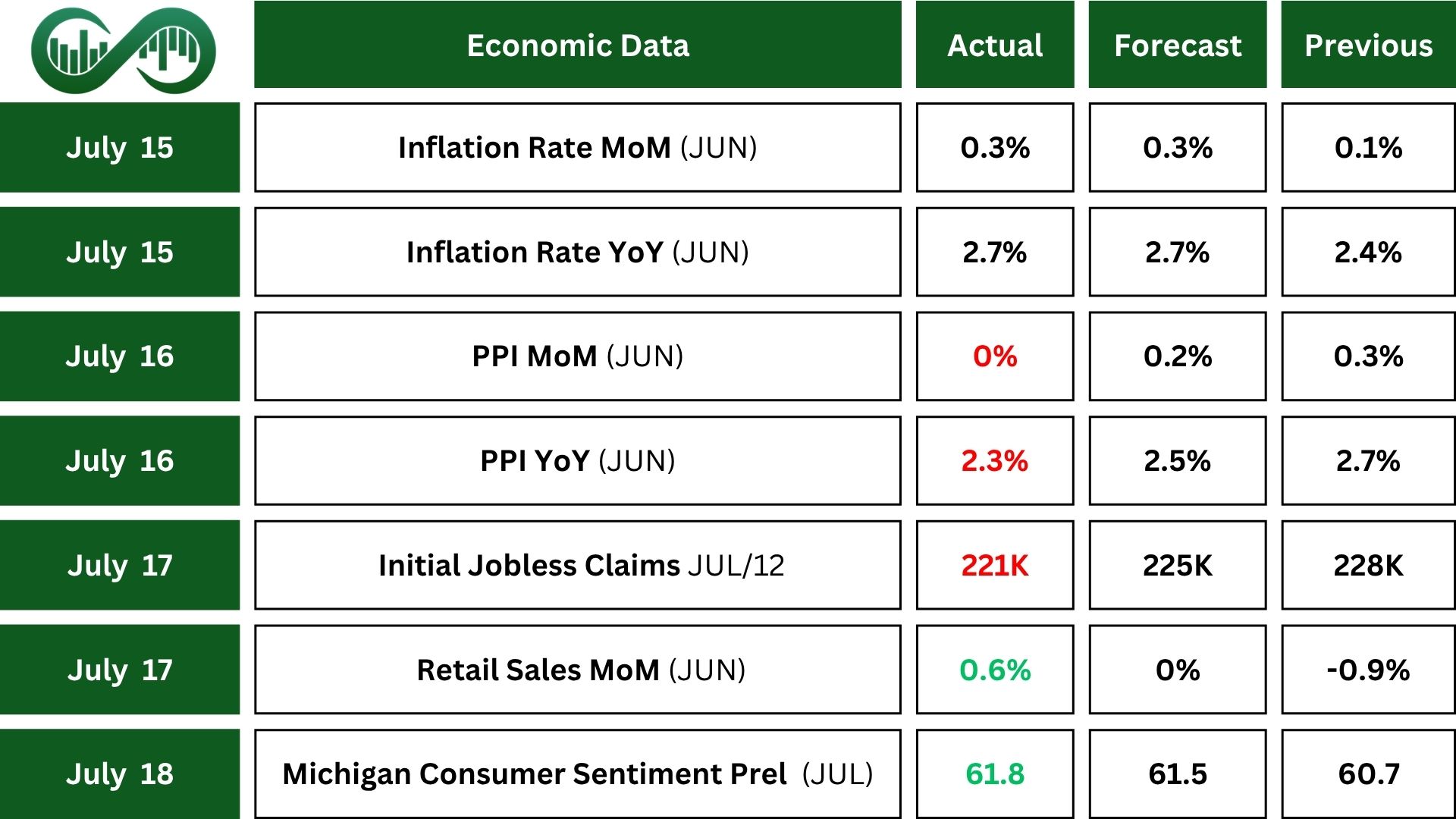

U.S. Consumer Inflation edged up 0.3% in June, marking the fastest monthly rise since February and bringing the annual rate to 2.7%. Also, Core Inflation, which excludes food and energy, rose 0.2% for the month and 2.9% year-over-year, slightly below expectations. This signaled that broader inflation pressures remain manageable, easing market fears.

Producer Prices held steady in June, signaling a potential cooling in inflation pressures. While overall prices remained unchanged month-over-month, they rose 2.3% annually. Goods saw modest increases, while service prices dipped slightly. Core producer prices were flat in June and up 2.5% year-over-year. The stability in price growth is seen as a positive development, possibly paving the way for future interest rate cuts.

U.S. retail sales showed a solid rebound in June, rising 0.6% month-over-month and 3.9% year-over-year, signaling renewed consumer strength. Sales from April to June climbed 4.1% versus the same period last year. The shows easing fears of a slowdown and suggesting that inflation pressures may be stabilizing. This resilience could factor into the Federal Reserve’s future rate decisions.

In July, the Michigan Consumer Sentiment Index edged up slightly to 61.8, its best reading in five months. While consumers showed more optimism about short-term business conditions, personal finance expectations dipped, suggesting ongoing household concerns.

Inflation expectations declined for a second month, marking the lowest levels since February.

Earnings Reports

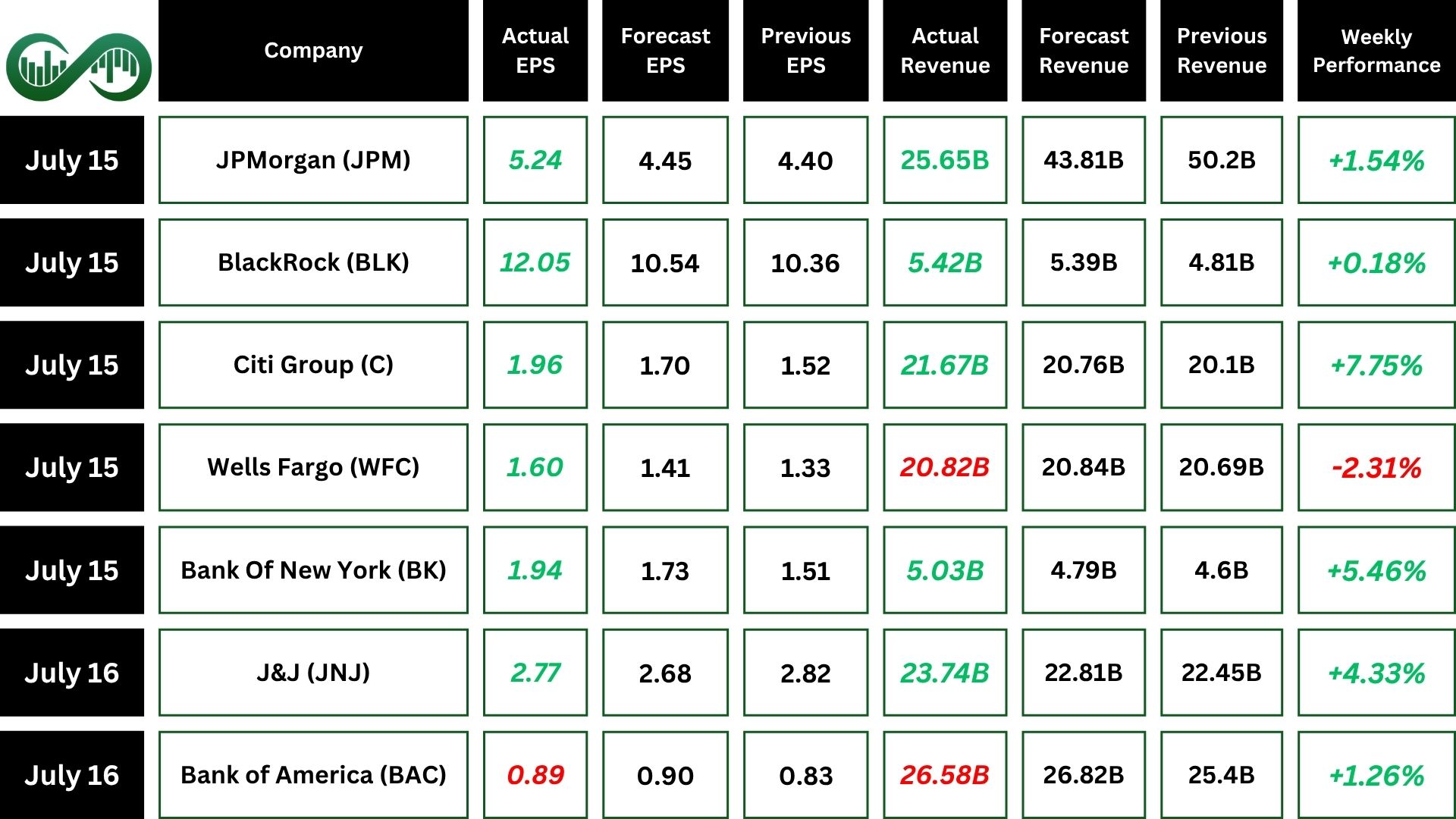

JPMorgan

JPMorgan (JPM) posted strong Q2 results with $15 billion in net income and $44.9 billion in revenue, driven by solid gains across all major segments.

Consumer banking saw a surge in card usage and mobile app engagement, while investment banking benefited from a jump in trading and fees.

Asset management also performed well, with AUM rising to $4.3 trillion. The bank repurchased $7 billion in shares and announced a second dividend hike.

Despite outperforming expectations, stock flat last week due to elevated credit costs and a cautious outlook. JPMorgan emphasized economic resilience but flagged risks such as trade tensions and fiscal challenges.

BlackRock

BlackRock (BLK) reported solid Q2 results, beating forecasts on both revenue and earnings.

Total net inflows reached $152 billion year-to-date, driven by record iShares ETF performance and steady growth in private markets.

The acquisition of HPS Investment Partners added $165 billion in AUM, bolstering its private investment footprint.

Despite these gains, stocks were flat as investors reacted to a $52 billion client redemption, a drop in performance fees, and noncash acquisition costs that lowered GAAP income.

Still, assets under management hit a record $12.5 trillion, and the firm remains optimistic about continued growth through personalized strategies and global expansion.

JNJ

Johnson & Johnson (JNJ) delivered a strong Q2, with sales rising 5.8% to $23.7 billion and adjusted earnings per share reaching $2.77, beating expectations.

Growth came from both its Innovative Medicine and MedTech segments, supported by product approvals and promising drug trials.

The company raised its full-year forecast, anticipating $2 billion more in sales and stronger earnings, reflecting confidence in its pipeline and clinical momentum.

JNJ stock jumped over 4%, as investors welcomed the upbeat performance and strategic focus on cancer therapies, surgical tech, and future product rollouts.

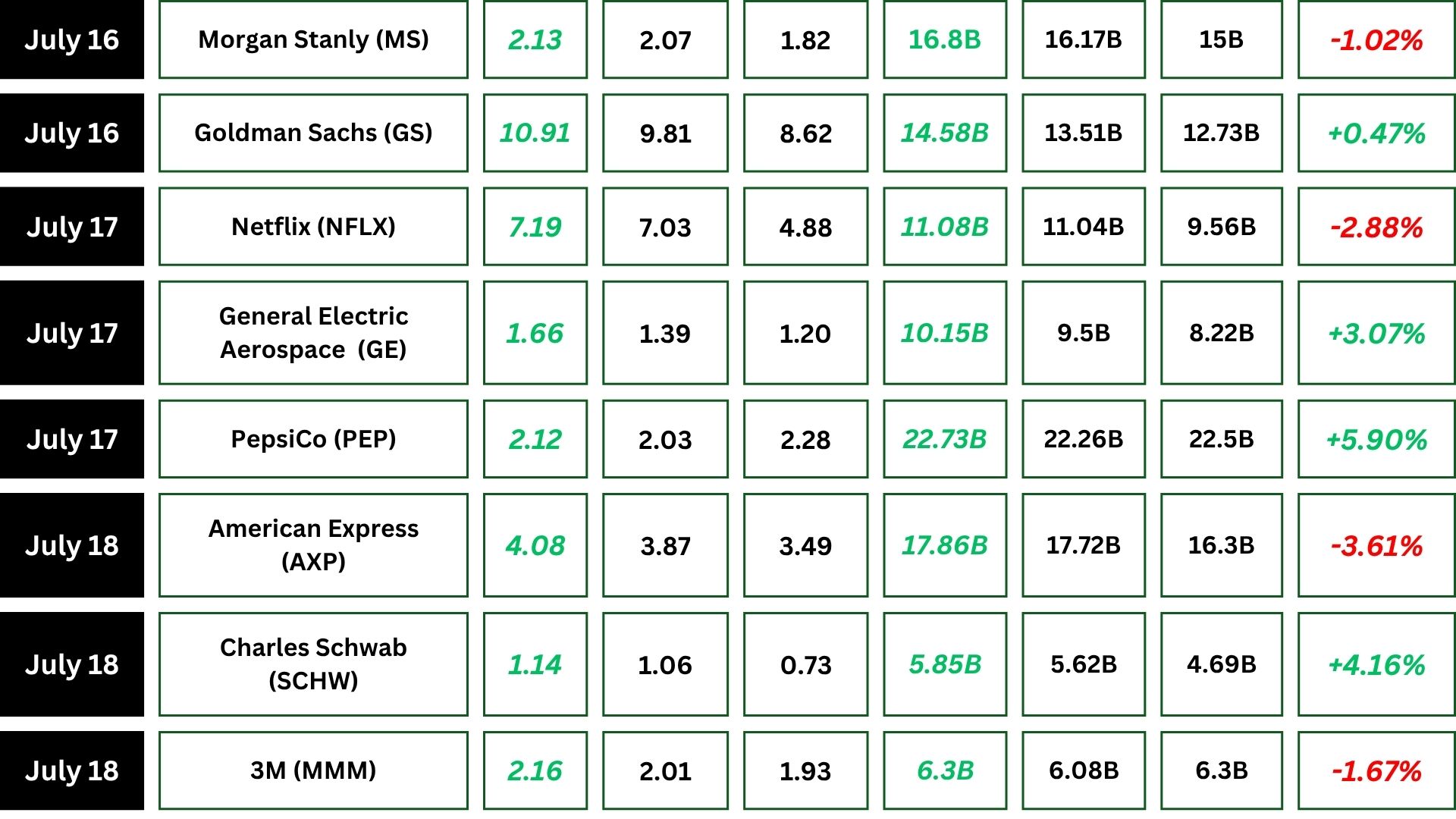

Netflix

Netflix (NFLX) posted a strong second quarter with revenue growing 16% and operating margin expanding to 34%, thanks to subscription increases, pricing adjustments, and ad revenue across all regions.

The company raised its full-year guidance, citing momentum from a weaker U.S. dollar and successful global content releases.

Strategic moves included launching the Netflix Ads Suite and redesigning the TV homepage.

Despite the upbeat results, shares dipped about 2%, reflecting investor caution over conservative forecasts and elevated market expectations following a sharp rally.

GE Aerospace

GE Aerospace (GE) posted strong second-quarter results, with revenue up 21% to $11 billion and adjusted EPS at $1.66, beating expectations.

Free cash flow nearly doubled to $2.1 billion, driven by operational improvements and key deals, including over 400 engines for Qatar Airways.

The FLIGHT DECK system boosted service revenue and engine output, while testing milestones in the CFM RISE program and upgrades to U.S. hypersonic sites showed innovation.

GE raised its financial targets through 2028 and pledged substantial shareholder returns.

Its stock reached a 25-year high, reflecting investor confidence in the company’s future growth.

Pepsi

PepsiCo (PEP) reported strong Q2 results, with revenue exceeding expectations and adjusted EPS rising to $2.12.

Growth was driven by solid demand for snacks and beverages across global markets, especially in Asia Pacific and Europe. Health-conscious offerings like Poppi also supported performance.

Quaker Foods North America saw a sharp drop due to product recalls. While, international sales remained resilient, contributing nearly 40% of net revenue.

The company expects modest full-year growth and plans to return $8.6 billion to shareholders. Despite facing foreign exchange headwinds.

PepsiCo improved its profit outlook, and shares surged, reflecting investor confidence.

Indices

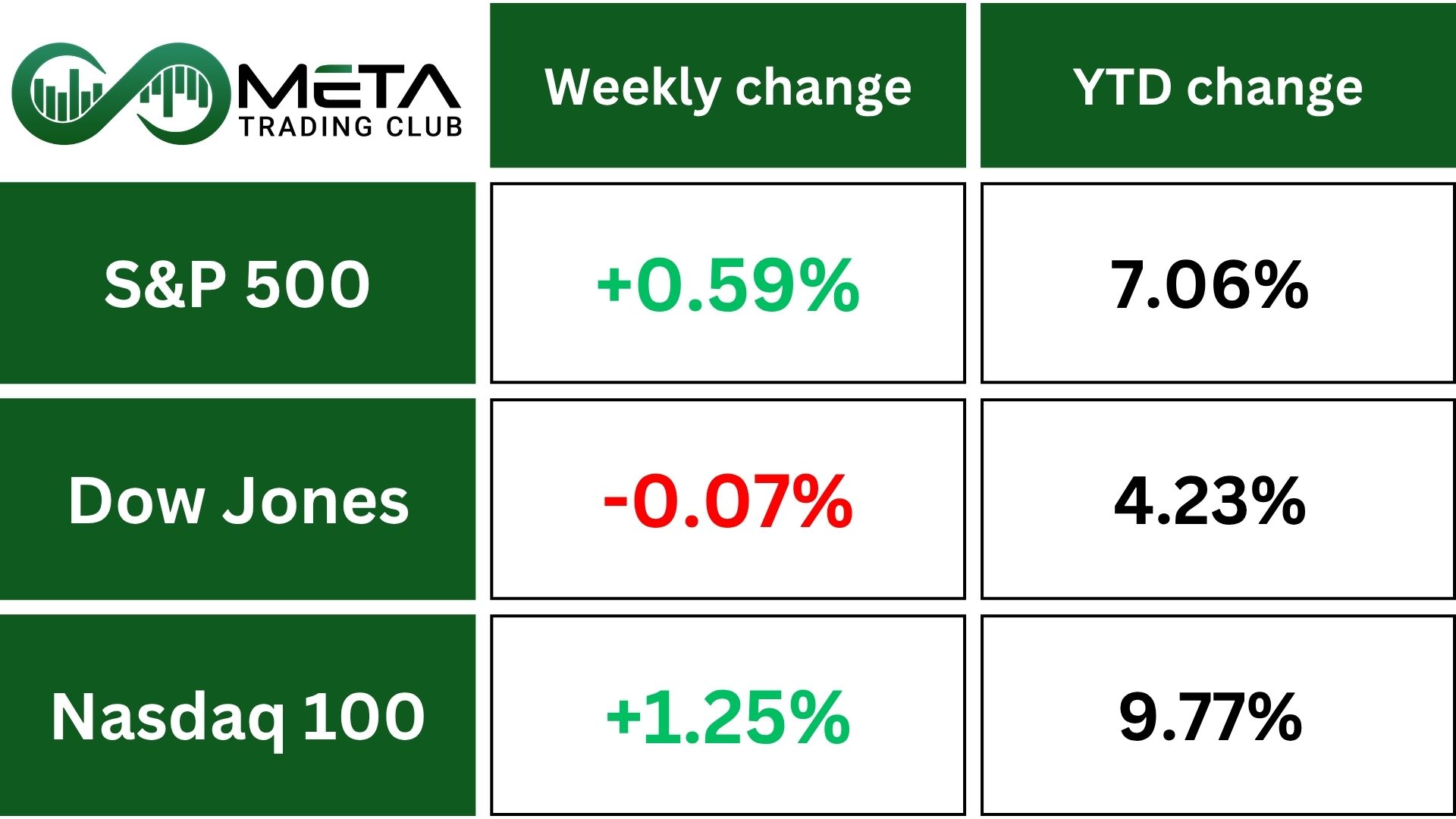

Indices’ Weekly Performance:

U.S. stock indexes ended the week with mixed results as investors weighed corporate earnings, inflation data for June, and comments from President Donald Trump about Fed Chair Jerome Powell.

Despite concerns, earnings from big companies boosted market sentiment and helped push the S&P 500 and Nasdaq to new record highs.

Inflation picked up slightly in June and annual inflation reached 2.7%. However, core inflation stayed mostly in line with expectations. Producer prices remained unchanged from May, signaling steady price trends.

Trump denied reports that he plans to remove Powell as Fed Chair, calling it “highly unlikely” after earlier rumors caused market jitters.

Meanwhile, Fed Governor Waller supported a rate cut and Powell maintained a cautious approach due to ongoing trade and inflation uncertainties.

Technically, SPX is currently testing the psychological barrier around the 6300 level, with momentum showing signs of slowing as it approaches the RSI uptrend line. If the RSI bounces back from the trend line and regains strength, the index could break above 6300, potentially triggering a further rally, provided it holds above that level.

However, if the RSI trend line fails and breaks down, it could signal weakening momentum, putting 6300 at risk and potentially dragging the index down to its key support near 6150.

Stocks

Sector’s Weekly Performance:

Most sectors advanced last week, with technology leading the way, while healthcare and energy struggled to keep pace.

- Technology rose 2.2%, driven by strength in semiconductor stocks like Nvidia and AMD, which gained after news that China chip exports would resume. The semiconductor index also edged up 0.6%, reflecting sector-wide momentum.

- Financials posted a 0.9% gain. JPMorgan eased slightly despite strong investment banking results, while Citigroup surged to its highest level since 2008 on upbeat earnings and share buyback plans. Wells Fargo fell after trimming its interest income outlook, but Bank of America and Goldman Sachs benefited from trading strength. Morgan Stanley slipped amid shrinking investment banking revenue. Overall, big banks edged higher, with the S&P 500 bank index up about 1%, and regional lenders added 0.6%. Coinbase rallied to a record high amid renewed enthusiasm in the crypto space.

- Communication Services saw a modest 0.6% gain. Netflix stumbled after its Q2 revenue met expectations but failed to excite with its updated outlook.

- Healthcare dropped 2.4%, weighed down by Waters Corp, which fell sharply following its $17.5 billion acquisition of a biosciences and diagnostics unit from Becton Dickinson. However, Johnson & Johnson jumped after raising its 2025 forecast and cutting its tariff cost outlook.

- Energy plunged 2.6% as an increase in U.S. fuel inventories overshadowed signs of rising demand. Chevron slipped after finalizing its acquisition of Hess, and SLB sank due to disappointing quarterly profit.

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- Shopify (SHOP): Soared 13.3%, as U.S. shoppers spent more than expected, showing strong consumer demand that’s helping support the economy.

- Applovin (APP): Jumped 8.8% boosted by a fresh “Buy” rating reaffirmed by a leading Wall Street bank and strong interest from institutional investors.

- Warner Bros. Discovery (WBD): Climbed 8.7% thanks to The Man of Steel, scored a strong box office debut, boosting confidence in the studio’s outlook.

- Coinbase (COIN): Rose 8.5%, riding the wave of crypto sector momentum and favorable regulatory signals that helped boost trading volumes and investor appetite.

- First Solar (FSLR): Advanced 8.3% after U.S. solar panel manufacturers pushed for new tariffs on foreign imports, raising hopes for stronger domestic industry protection.

- Palantir (PLTR): Gained 8%, following a strategic partnership with Knightscope and an analyst upgrade, which highlighted growing federal market potential.

- Citigroup (C): Increased 7.8% on better-than-expected earnings, robust buyback plans, and optimism around its streamlined capital strategy.

- Arm Holdings (ARM): Rose 7.4% as stock upgraded driven by optimism around ARM’s potential in the ASIC chip market

- Advanced Micro Devices (AMD): Added 7.2% on news of China export license approval for its MI308 chips and sustained demand for AI processors.

- GE Vernova (GEV): Gained 6.6% thanks to strong earnings of GE Aerospace.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold (XAU/USD) ended its two-week winning streak with a modest pullback, reflecting a pause after its recent run of record highs.

While central bank demand and geopolitical tensions continue to support the precious metal long-term. In short-term traders focus especially toward alternative metals like silver and platinum have capped momentum for now.

A mix of profit-taking and mild risk-on sentiment may also be weighing on gold’s near-term appeal.

Technically, Gold has been moving sideways in recent weeks, stuck within a narrow trading band. For the bullish trend to pick up again, prices need to break past the all-time high. A potential early signal could come from the RSI breaking its downward trend line, possibly pushing gold toward that ATH resistance.

On the flip side, a break below the short-term uptrend line might indicate weakening momentum and open the door to further downside.

WTI Crude Oil ended the week lower, breaking a two-week winning streak. The early boost came from the EU tightening sanctions on Russia, but concerns over how well those sanctions would be enforced pulled prices down.

Also, oil prices faced pressure as an increase in U.S. fuel inventories outweighed signals of growing demand. Despite early optimism, the unexpected stockpile buildup suggested supply may be outpacing consumption for now, cooling momentum in energy markets.

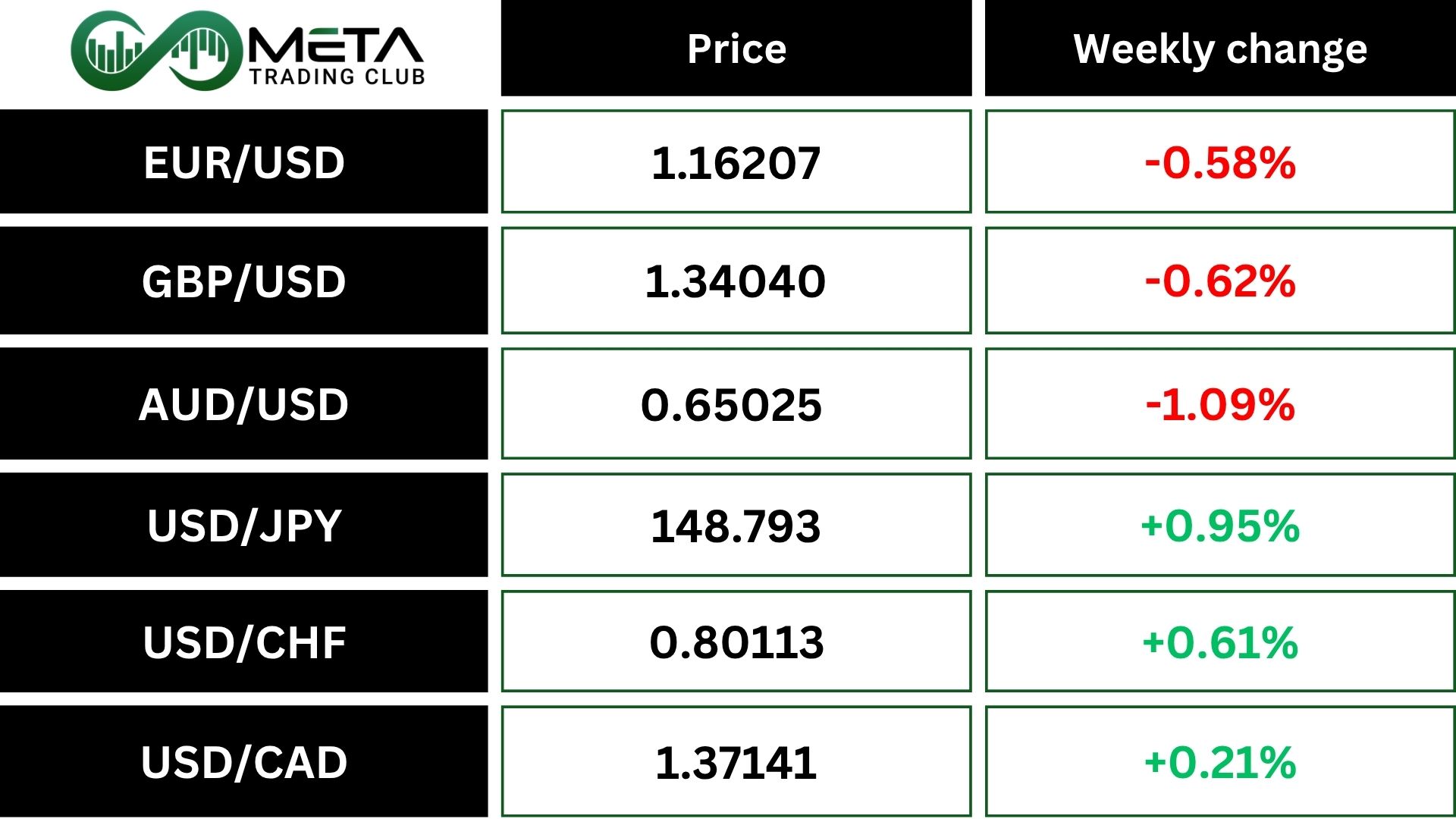

Forex

Weekly Performance of Major Foreign Exchange Pairs:

USD/JPY: The Japanese yen fell as concerns raised about the country’s economic outlook, especially with a new 25% U.S. tariff on Japanese goods looming and national elections approaching.

AUD/USD: The Australian dollar was headed for its first weekly decline in a month amid growing expectations that the Reserve Bank of Australia may cut interest rates in August following soft labor data.

USD/CAD: The Canadian dollar slipped past 1.37 per U.S. dollar, marking its weakest level since early June. The drop came from uncertainty over a potential 35% U.S. tariff on Canadian non-USMCA exports dampened demand from exporters for Canadian dollars. Meanwhile, Canada’s core inflation stayed steady at 3% in June, reinforcing expectations that the Bank of Canada will keep its policy rate unchanged at 2.75% for now.

EUR/USD: The euro was pressured by a stronger U.S. dollar, which gained on upbeat inflation data and reduced expectations for Fed rate cuts. Meanwhile, the European Central Bank is expected to hold rates steady next week. Eurozone inflation held at 2%, reinforcing cautious outlooks on monetary policy.

GBP/USD: The British pound remained weak around $1.34, weighed down by a stronger U.S. dollar. Rising unemployment in the UK and softer wage growth point to a slowing labor market, yet inflation jumped unexpectedly to 3.6% in June. This contrast has made the outlook for Bank of England rate decisions less clear.

Crypto

President Trump’s “Crypto Week” brought the House approval of three major bills aimed at regulating digital assets. One, the Genius Act, lays out rules for stablecoins, but won’t take full effect for up to three years. The other two bills, which cover crypto platform oversight and ban a government-issued digital currency, still need Senate approval.

Bitcoin and other cryptocurrencies rose on the news, along with shares of Coinbase and Robinhood.

Charles Schwab is gearing up to launch spot trading for Bitcoin and Ethereum, marking a major step into the crypto space for one of the largest U.S. brokerage firms.

Bitcoin has cooled off after its record-setting surge to $122,800 on July 14. Following a week of intense trading and strong inflows, BTC broke past key resistance levels but quickly ran into volatility. Then price dropped to $116,000 and has since been moving within a narrower range, fluctuating between $117,000 and $118,500, signaling a temporary pause in upward momentum.

Technically, if BTC breaks above its short-term downtrend line and gains confirmation on lower timeframes, it could rally toward its all-time high. But if it slips below the $155K level, that may signal further downside, with the next support zone likely coming into play.

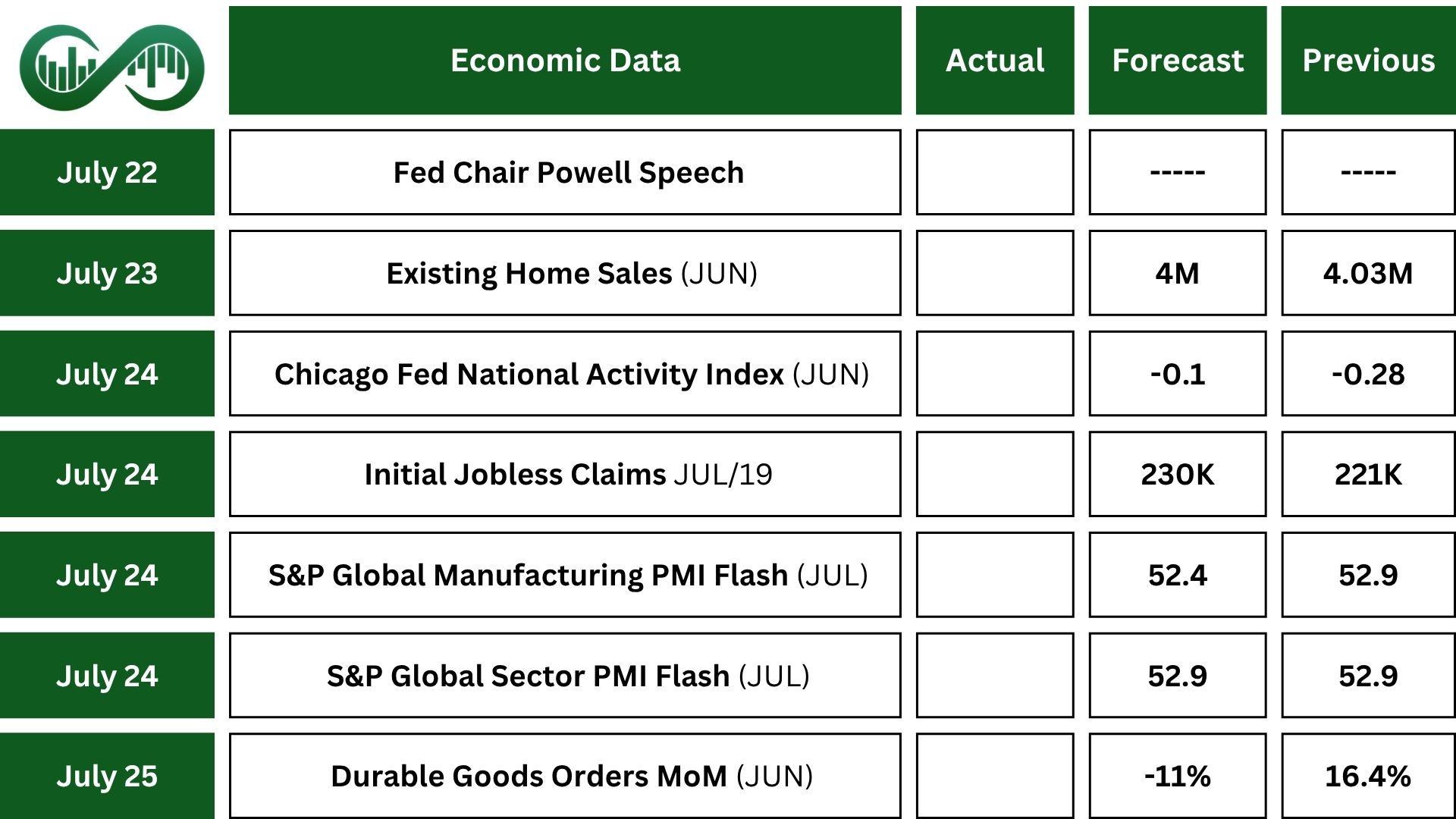

Next Week’s Outlook

Economic Events

This week’s economic lineup is relatively light, with durable goods orders taking center stage, expected to ease after last month’s sharp rise.

S&P Global PMIs should point to steady growth in private sector activity, and both new and existing home sales are projected to inch upward.

Regional Fed reports are also on tap, while investors will closely monitor Fed Chair Jerome Powell’s remarks at an upcoming banking event.

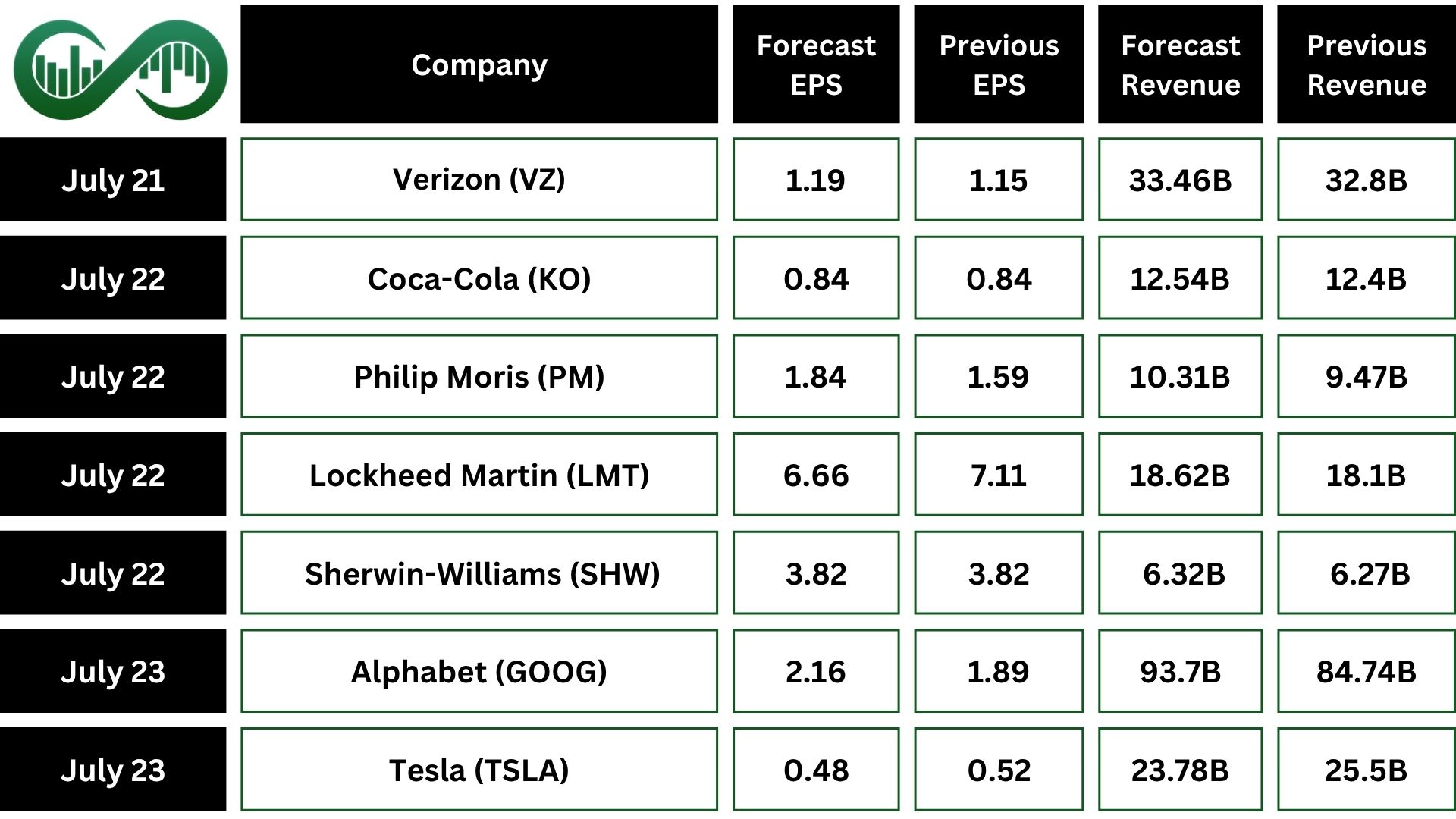

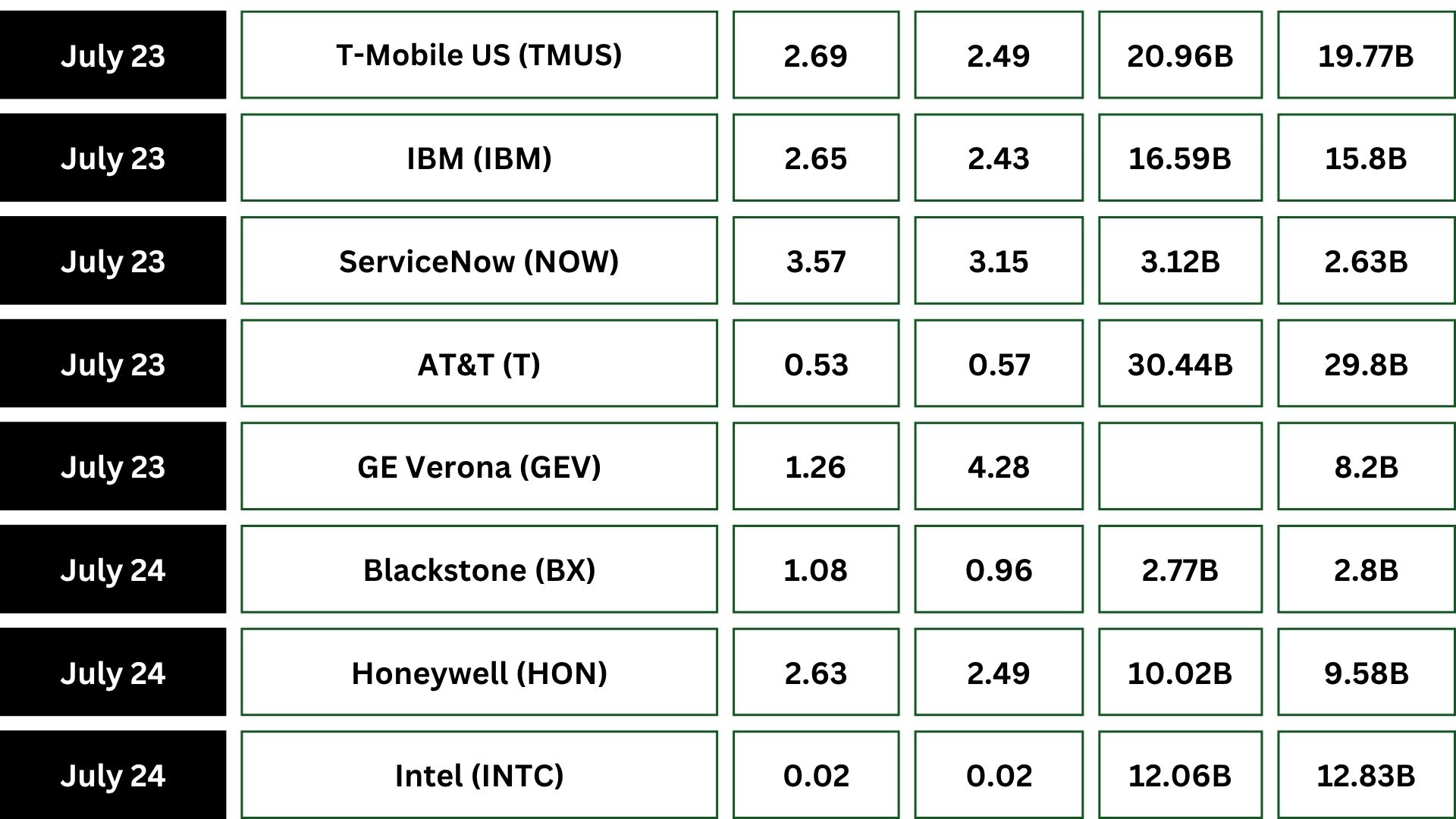

Earnings Events

A packed week of corporate earnings is ahead, spotlighting major players across industries.

Big tech firms like Alphabet (GOOG), Tesla (TSLA), IBM (IBM) , and Intel (INTC) will headline the action.

Key updates are also expected from defense companies such as Raytheon, Texas Instruments, and Lockheed Martin.

In the telecom space, Verizon (VZ), AT&T (T), and T-Mobile (TMUS) will be closely watched.

Additional results from household names including Coca-Cola (KO), Philip Morris (PM), ServiceNow (NOW), and Blackstone (BX) will round out the lineup.