What You Gained by Reading Last Week’s Market Mornings and What You Missed If You Didn’t!

Last Week’s report

Economic Reports

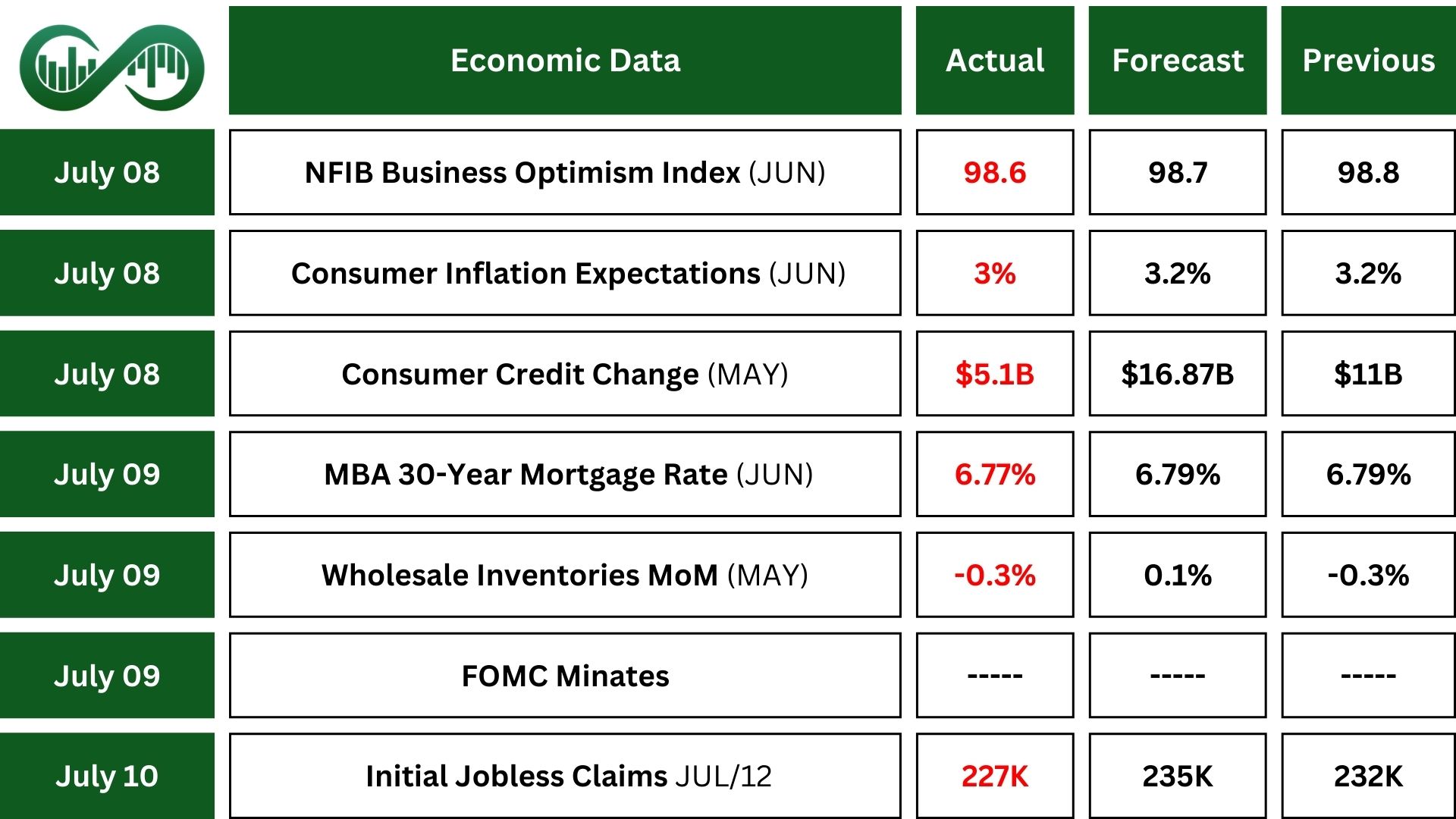

Small Business Optimism in the U.S. dipped slightly in June to 98.6. Most small business owners reported taxes as their single most important problem, ranking as the top problem. Challenges around labor quality and costs persist, while expectations for better business conditions, sales growth, and investment have all slipped.

U.S. Consumer Inflation Expectations eased in June, with the one-year outlook falling to 3%, the lowest in five months. However, expectations for key living costs rose noticeably, signaling that while headline inflation might be cooling, people still feel pressure in everyday expenses. Longer-term inflation views remained steady at 3%, showing cautious optimism.

U.S. Consumer Credit Growth slowed in May, rising just $5.1 billion, well below expectations. Credit card borrowing grew moderately at 3.2%, showing steady but cautious consumer spending.

Mortgage Rates dipped to 6.77% in early July, the lowest in three months, reflecting a broader decline in Treasury yields as investors anticipate at least two rate cuts from the Federal Reserve later this year.

U.S. Initial Jobless Claims dropped in early July to 227,000, marking the fourth straight weekly decline and the lowest level in seven weeks, suggesting the labor market is still holding up despite high rates and uncertainty. However, total unemployment claims rose to their highest since 2021, hinting that hiring may be slowing.

The Fed’s June meeting minutes: some members supported rate cuts later this year, while others preferred holding steady due to lingering inflation concerns. This signals a Fed still in wait-and-see mode, balancing inflation risks with signs of labor market strength, while keeping future rate cuts on the table.

Earnings Reports

Delta Air Lines (DAL) posted strong Q2 2025 results, reporting $15.5 billion in revenue, slightly higher than last year. This strong earnings came after steady travel demand and high-margin sources like premium seating and loyalty programs.

Profit margins were solid, with $2 billion in operating income and $2.10 earnings per share, beat expectations.

Looking ahead to Q3, Delta expects flat to slightly higher revenue and anticipates its best cost control performance of the year.

The market responded quickly, with shares jumping 12% last week. The company also announced a 25% dividend hike and reaffirmed confidence in stable travel demand and disciplined spending.

Indices

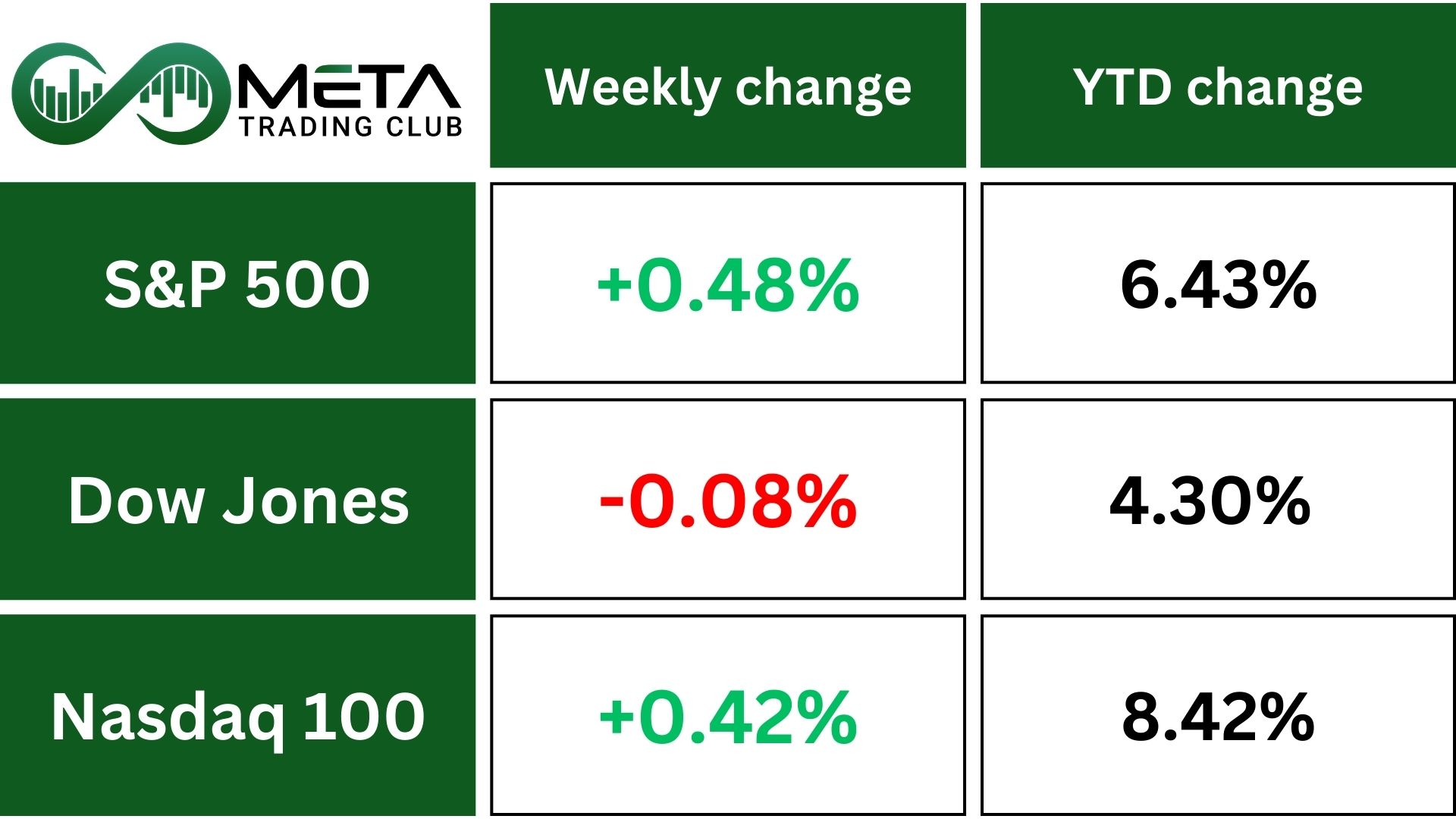

Indices’ Weekly Performance:

U.S. stock indexes retrace from record highs after President Trump announced a wave of new trade tariffs, which shook investor confidence.

Nvidia (NVDA) made history by becoming the first company to reach a market value of $4 trillion.

The U.S. sent tariff letters to more than 20 countries. This includes Canada and Japan, stating that new import duties will begin on August 1. Trump also said he plans to apply a general 15–20% tariff on most trading partners.

Canada was warned it could face a 35% tariff if a new deal isn’t reached by August 1. However, this would likely apply only to goods not covered by the USMCA trade agreement. In addition, the U.S. announced a 50% tariff on copper imports, and Brazil is facing similar penalties.

Technically, SPX is steadily climbing with momentum. The bullish outlook remains intact as long as the index stays above the 6,150 mark. If this trend holds, it could push higher toward the key 6,500 Fibonacci resistance level.

Stocks

Sector’s Weekly Performance:

Markets saw broad losses across sectors, with Financials and Consumer Staples taking the biggest hits, while Energy came out on top.

- Consumer Defensive dipped 1.8% as Conagra (CAG) warned tariffs would hurt profits. Hershey (HSY) shares fell after naming Wendy’s CEO as its new leader.

- Financials fell 1.5%. JPMorgan (JPM) dropped after a downgrade from HSBC, marking a 3% weekly decline. Bank indexes also slid.

- Technology down 0.5%. Even with Nvidia (NVDA) made history, becoming the first public company to reach a $4 trillion market cap. The semiconductor index jumped, but other tech stocks like Fair Isaac (FICO) and First Solar (FSLR) dropped on regulation and policy news.

- Consumer Discretionary was mostly flat. Tesla (TSLA) seesawed after political headlines and bounced updates.

- Materials rose 0.16%, although Freeport-McMoRan (FCX) climbed on news of upcoming copper tariffs.

- Utilities edged up 0.2%, with AES jumping amid takeover buzz.

- Industrials gained 0.5%, led by Delta air lines (DAL) upbeat profit forecast that lifted airline stocks.

- Energy rallied 1.6%, driven by rising oil prices tied to Red Sea conflicts and U.S. supply concerns. Exxon Mobil (XOM) rose despite profit warnings.

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- Delta Air Lines (DAL): Led the pack, soaring over 11% after raising its 2025 profit forecast, sparking a rally in travel stocks.

- Moderna (MRNA): Surged 10% thanks to promising cancer vaccine developments and renewed biotech interest.

- Southwest Airlines (LUV): Climbed 9% on momentum from Delta’s outlook and summer travel optimism.

- Coinbase (COIN): Advanced 8.8% as crypto markets rebounded, with Bitcoin rising and trading volumes improving.

- Halliburton (HAL): Jumped 7%, likely riding higher oil prices and renewed interest in energy services.

- United Airlines (UAL): Rose 6.5%, benefiting from the broader travel sector boost and delta’s outlook.

- Hess (HES): Climbed 6%, supported by crude price increases and geopolitical tensions in the Red Sea.

- Advanced Micro devices (AMD): Added 6%, driven by strong chip demand and AI enthusiasm caused by Nvidia surge.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold (XAU/USD) prices climbed as investors sought safety amid rising trade tensions. President Trump’s threat to raise tariffs on Canadian goods from 25% to 35% intensified fears of a broader trade war.

At the same time, uncertainty around efforts to replace Fed Chair Jerome Powell added to the market. The combination of geopolitical and monetary instability helped gold notch its fourth weekly gain in six, ending the week up 0.6%.

Technically, Gold has been trading in a tight range over the past few weeks. To resume a bullish trend, it needs to break above its all-time high. An early bullish signal may start by breaking RSI down trend momentum line, which could lead gold to ATH resistance. On the downside, a drop below the $3,150 support zone could signal further declines.

WTI Crude Oil moved higher last week, with prices rising 3%. However, the International Energy Agency cut its forecast for global oil demand in 2025 and 2026, while increasing supply estimates. This comes as some speculation that oil-producing countries may be preparing to slow down production growth.

OPEC and its allies are discussing a plan to pause further production increases starting in October.

Forex

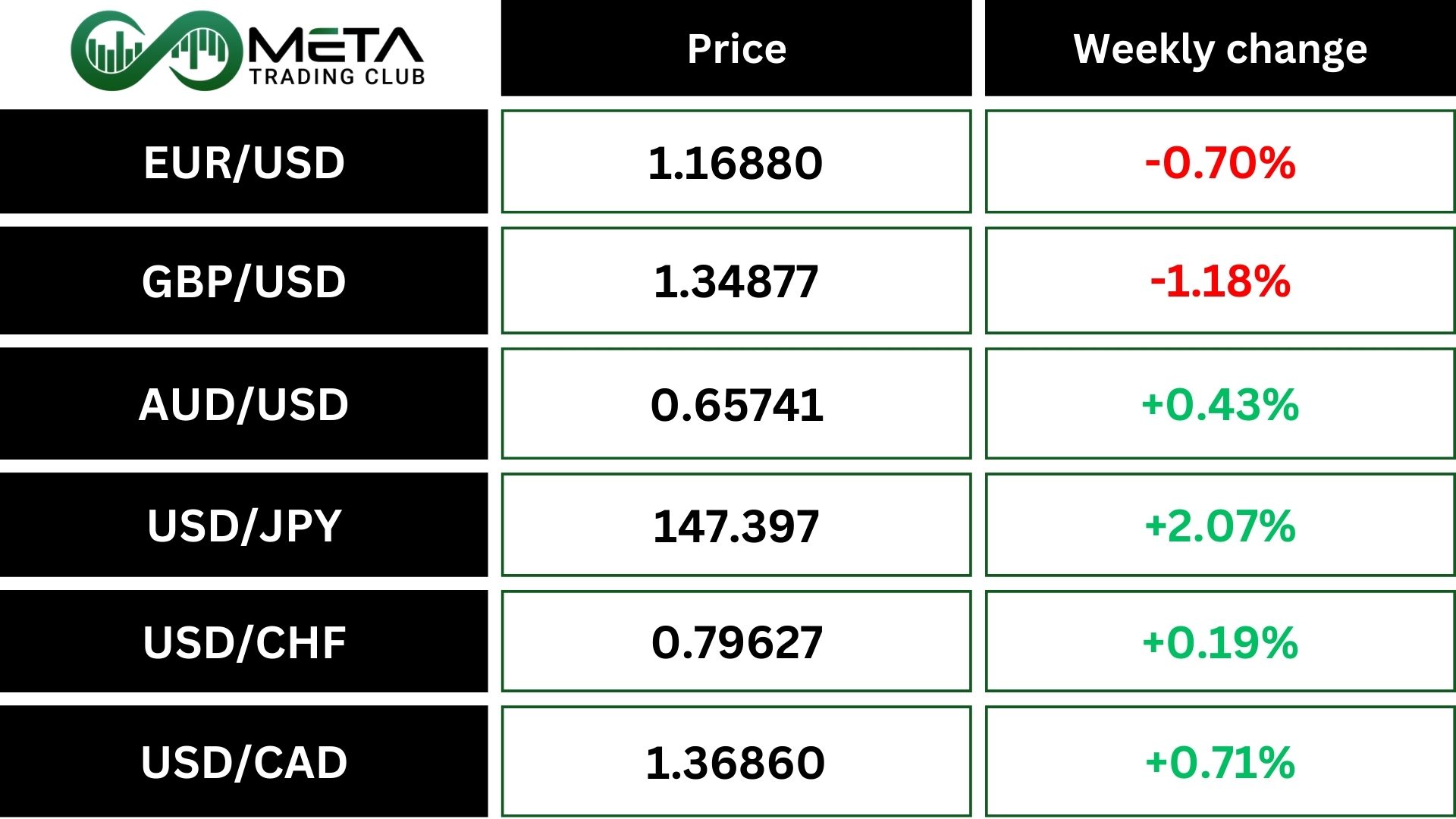

Weekly Performance of Major Foreign Exchange Pairs:

The Japanese yen weakened sharply after President Trump announced a 25% tariff on imports from Japan, starting August 1, due to a failed trade deal. This pushed the USD/JPY currency pair a 2% jump last week.

Trump also sent similar letters to over a dozen countries, warning of tariffs up to 40%, depending on future relations. Forex markets reacted swiftly, expecting Japan’s economy, already struggling with slow growth and inflation, to take a hit.

With just weeks until the tariffs take effect, currency markets are bracing for more volatility, and Japan has limited options to counter the move.

The GBP/USD dropped 1.1% from last week’s high, as renewed tariff concerns strengthened the U.S. dollar. Traders are bracing for volatility ahead of August 1, when the U.S. plans to reinstate tariffs (up to 50%) on imports from many countries.

While the UK has secured a trade deal that offers some protection for sterling, other nations are still negotiating. The uncertainty is shaking up forex markets and putting pressure on global supply chains.

The U.S. dollar index (DXY) has dropped close to 10% this year amid growing concerns that upcoming data may reveal broader economic harm from current U.S. policies. Still, it rose 1% last week, putting it on pace for a weekly gain and ending a two-week losing streak.

Technically, as expected DXY bounced back from oversold territory on the weekly RSI as it tests the $97 support zone. This potential rebound from this level could continue. However, if the index breaks below week’s low, further downside toward lower support levels could follow.

Crypto

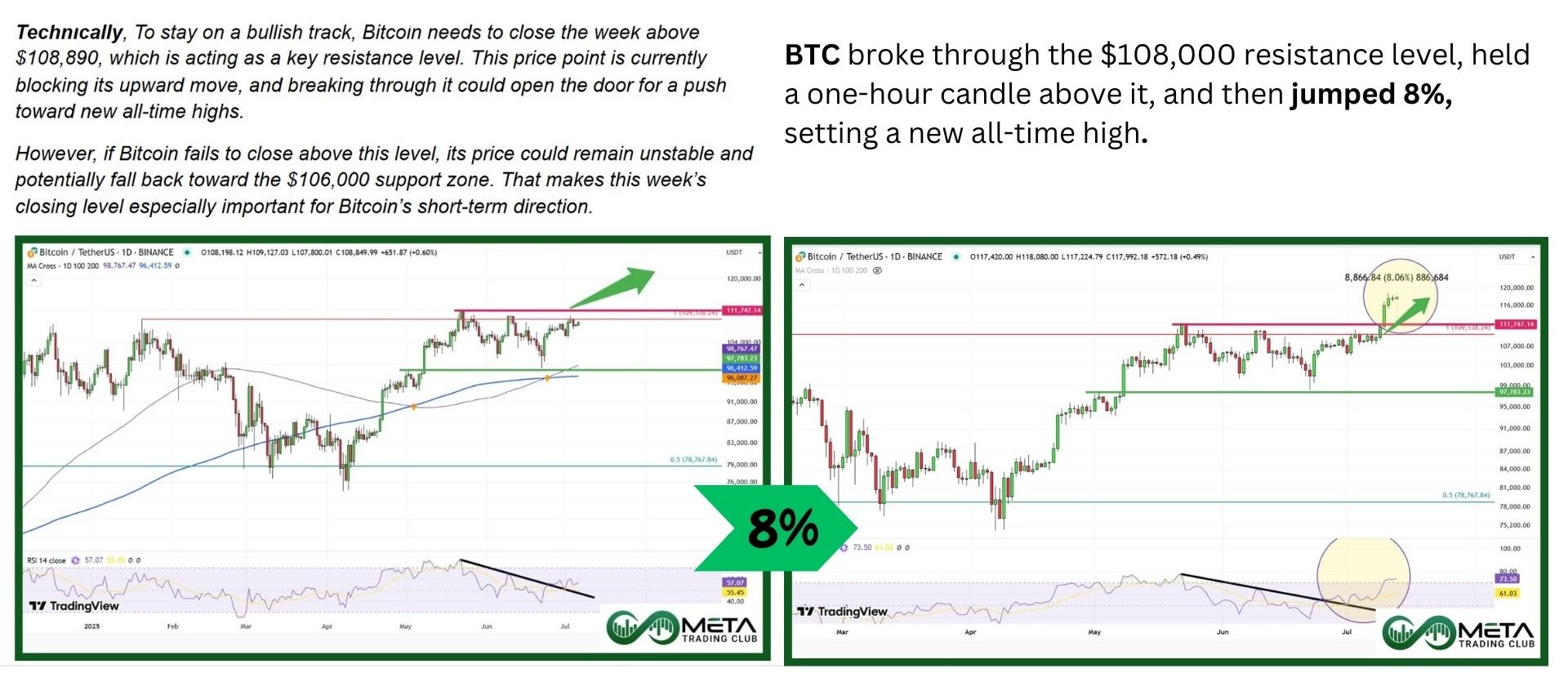

Bitcoin has broken out from a long period of sideways trading under $110,000, after a new bullish wave energizing the crypto market. This breakout is rising market sentiment, with the potential for another strong rally. The surge above prior highs has also sparked renewed excitement throughout the entire crypto space.

Altcoins are gaining momentum too, climbing past key resistance levels as investor confidence grows.

XRP has surged 25.8% over the past week, boosting its market value to over $170 billion and making it the third-biggest cryptocurrency again.

Technically, Bitcoin continues to trade in a bullish zone as long as it stays above $112,000, keeping upward momentum intact. However, if it slips below $109,000, that could signal a breakdown and raise near-term risks for investors. On the flip side, a solid move above $118,000 may trigger another surge toward the key $120,000 psychological level and also a Fibonacci resistance zone.

Next Week’s Outlook

Economic Events

In the U.S., trade news is expected to stay in the spotlight. Investors are watching for new tariffs on the EU, higher taxes on imports from other big trade partners, and possible deals with countries already facing tariffs.

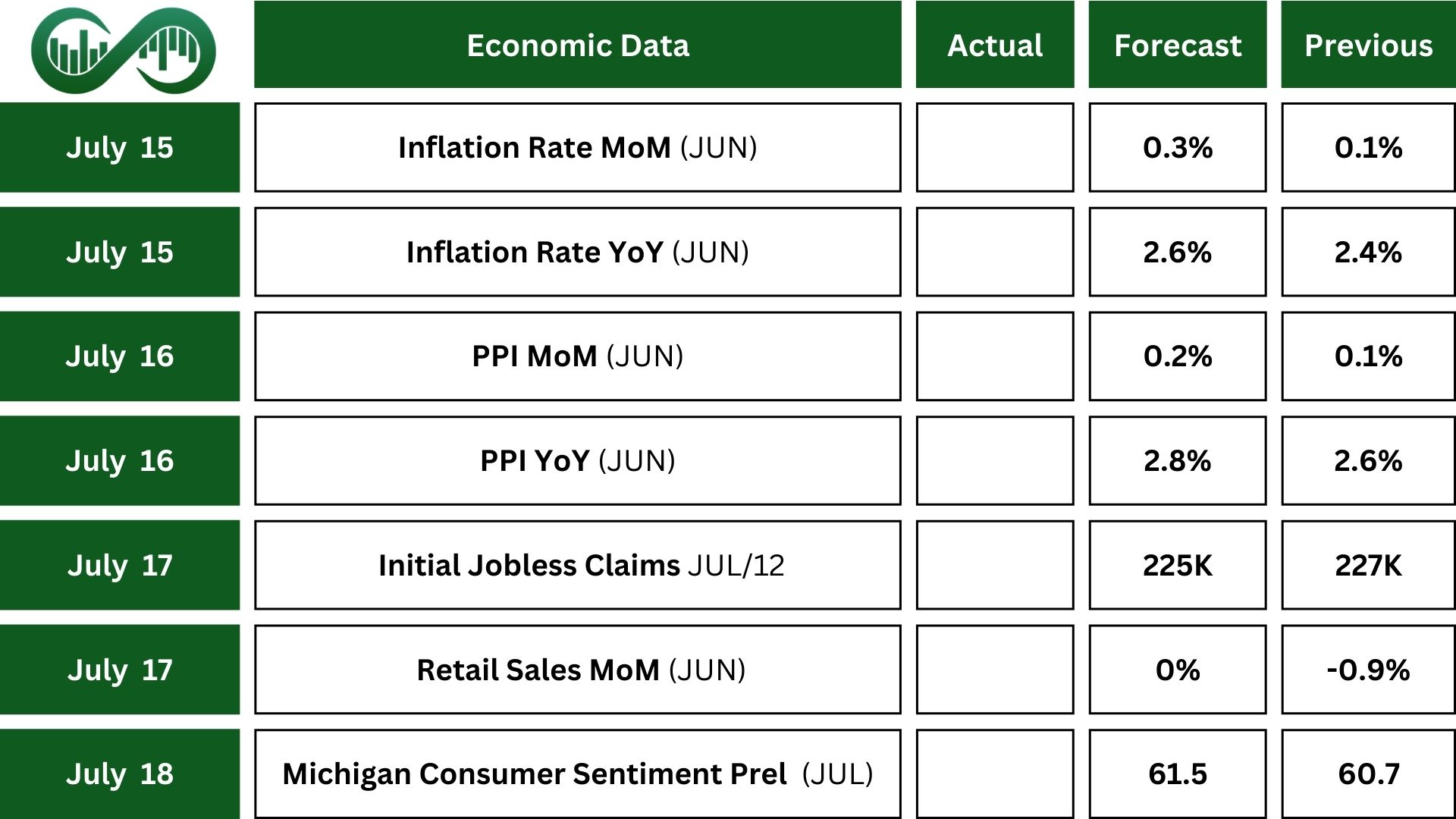

Economic data will be heavy this week. The June CPI report will show how tariffs may affect inflation, with headline inflation expected to rise to 2.6% and core inflation nearing 3%. The PPI report, along with import and export price data, will offer more clues on how businesses are handling costs.

The Michigan consumer survey will check inflation expectations and overall confidence. Retail sales are expected to stay weak.

While building permits should remain flat and housing starts might tick up.

Lastly, speeches from key Federal Reserve members, especially Governor Waller, seen as a possible future Fed Chair, will be closely watched for policy hints.

Earnings Events

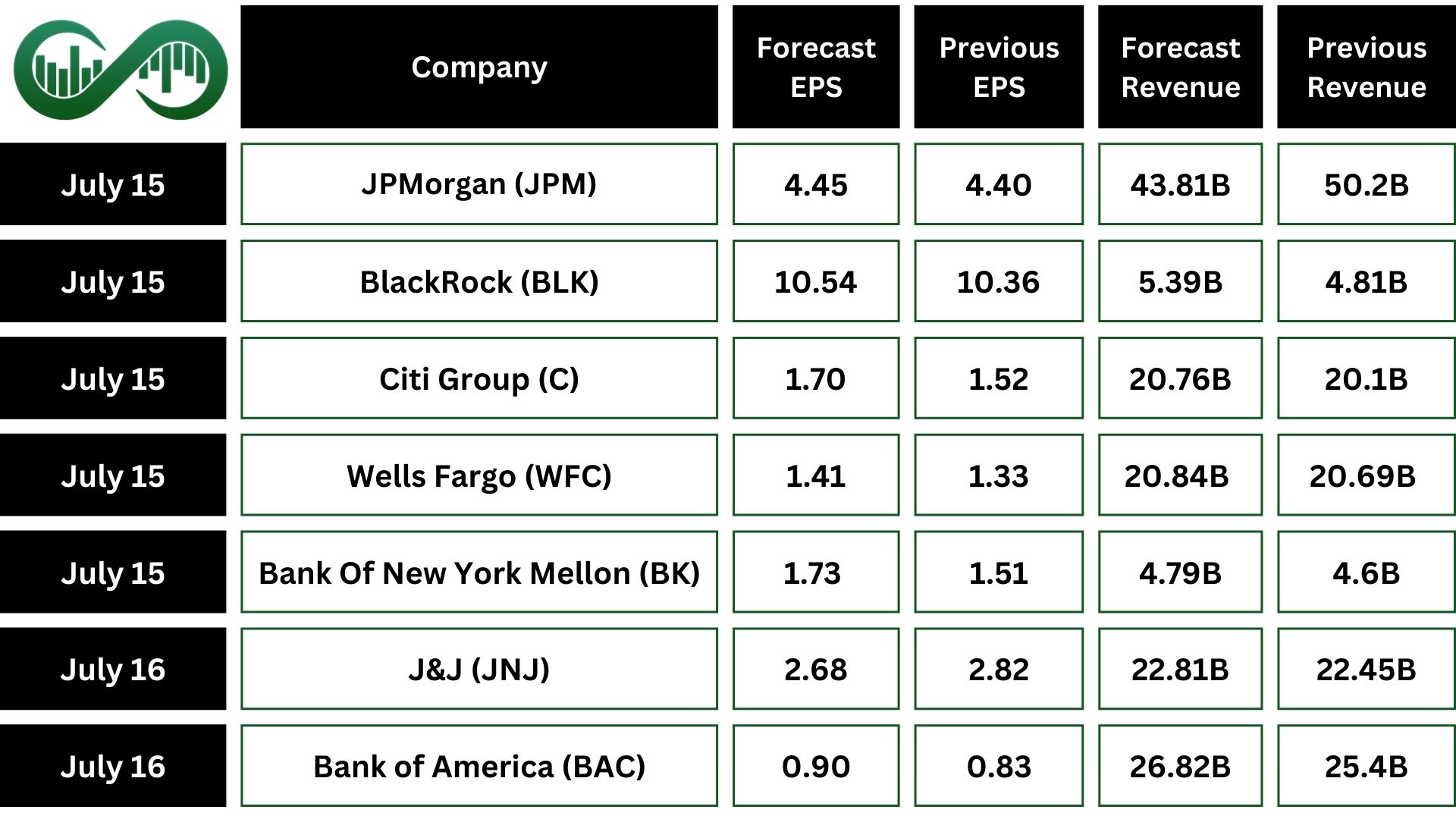

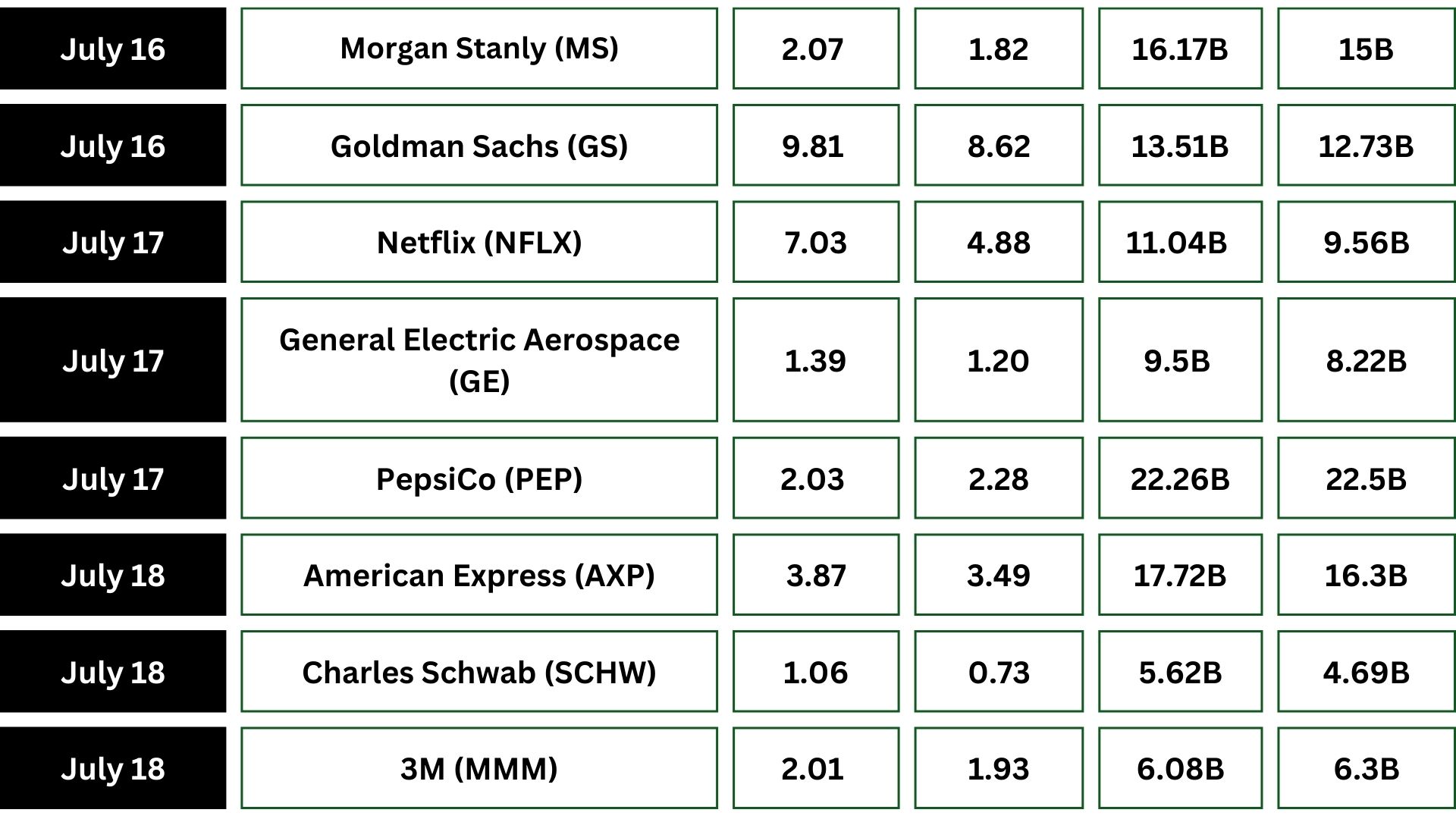

Markets are also focused on the first full week of earnings season, with forecasts pointing to weaker profits. Big names like JPMorgan (JPM), BlackRock (BLK), Goldman Sachs (GS), and Bank of America (BAC) will report results. Tech and consumer trends will be reflected in earnings from TSMC (TSM), Netflix (NFLX), J&J (JNJ), and PepsiCo (PEP).

{kind=link}