What You Gained by Reading Last Week’s Market Mornings and What You Missed If You Didn’t!

Last Week’s report

Economic Reports

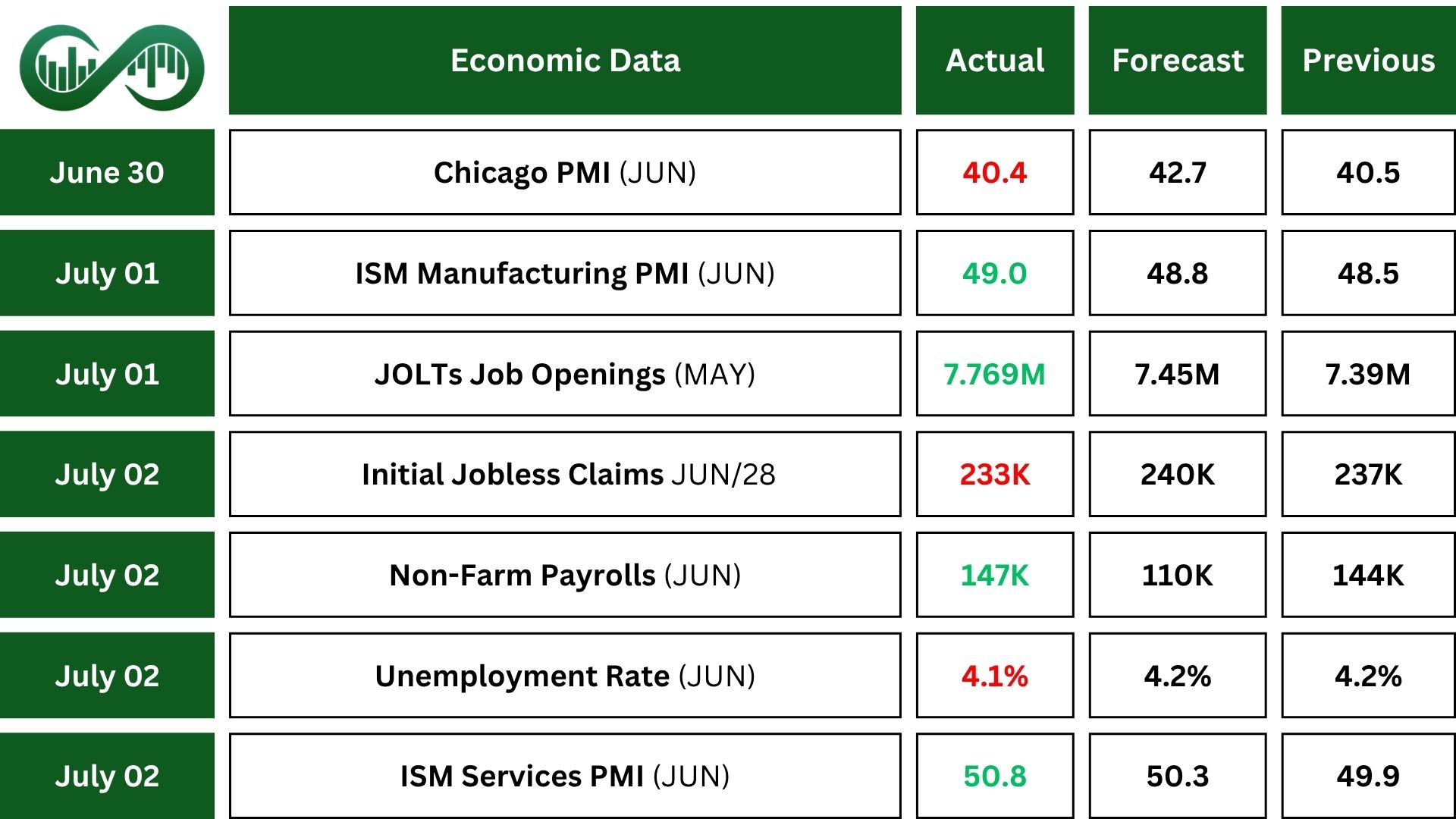

Chicago’s manufacturing sector continued to shrink in June, with the PMI falling slightly to 40.4 from May’s 40.5. This marks 19 straight months of contraction, driven by ongoing declines in new orders, backlogs, and production. Also, this shows that demand remains weak, and businesses are facing operational challenges.

Still, a few signs of stability are emerging. Some parts of the supply chain and labor market seem to be steadying, hinting that conditions could slowly begin to improve, even though overall activity is still subdued.

Business confidence in the U.S. improved in June, rising to 49 from 48.5 in May and beating forecasts. This uptick shows businesses are feeling more optimistic, even though the score is still just shy of the expansion line.

Manufacturing data added to the positive mood. The S&P Global Manufacturing PMI showed healthy growth, while the ISM Manufacturing PMI, although still below 50, came in stronger than expected. Signs like higher production and smoother supply chains helped boost market sentiment.

Altogether, the data suggests businesses are more confident, with many increasing outputs, rebuilding inventories, and feeling hopeful about the months ahead.

The U.S. services sector is showing mixed signals. The ISM Services PMI rose to 50.8 in June from 49.9 in May, pointing to a return to growth after a brief slowdown. This increase is a positive sign, especially since it came in stronger than expected.

Meanwhile, the S&P Global Services PMI slipped slightly to 52.9 in June, down from 53.7 in May. While that means growth slowed a bit but still above 50, showing the sector is expanding.

Jobs Report

Job openings climbed to 7.77 million in May, beating expectations and showing that employers are still actively looking to hire, signaling solid demand for workers.

Meanwhile, job cuts dropped sharply in June, with about 48,000 layoffs announced, half as many as in May, making it the lowest monthly total this year.

Despite June’s decline, Challenger job cuts showed layoffs for the second quarter totaled 247,000, the most for any Q2 since 2020. Overall, nearly 744,000 jobs have been cut so far this year, pointing to underlying stress in parts of the job market.

In June, the U.S. job market showed strength, with 147,000 new Non-Farm Payrolls added, well above the forecast of 110,000 and in line with the past year’s monthly average. Hiring was strongest in state government and health care, while federal job numbers fell.

The unemployment rate dipped slightly to 4.1%, signaling a stable labor market. However, wage growth slowed to just 0.2%, which could mean less upward pressure on inflation.

Initial Jobless claims in the U.S. dropped slightly to 233,000 for the week ending June 28, which was a bit better than expected. However, the number is still higher than it was earlier this year, pointing to a slow cooling in the job market.

Continuing claims stayed unchanged at 1.96 million, the highest level since late 2021, indicating more people are struggling to find new employment. Meanwhile, claims from federal workers fell to just 453, marking the lowest level in seven weeks.

Overall, these solid job reports point to a resilient economy. Businesses continue to hire, which supports consumer spending and gives markets a reason to stay upbeat.

Indices

Indices’ Weekly Performance:

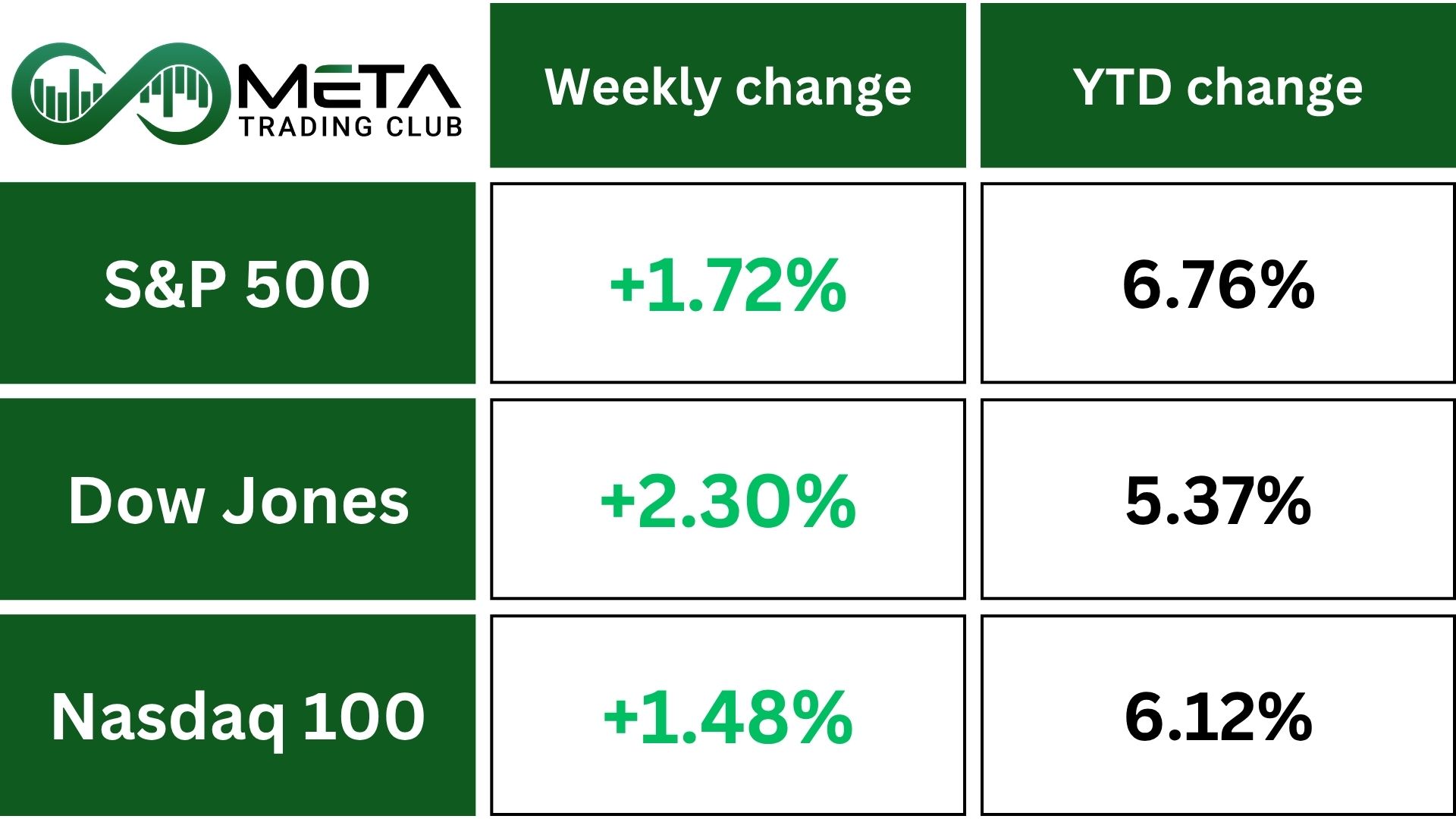

Last week, the stock market kept going up. The S&P 500 rose 1.7% (its second week in a row of gains) thanks to good news on trade and a strong jobs report. The Dow went up even more, climbing 2.3%, and the Nasdaq grew by 1.6%.

Markets have rebounded strongly in recent weeks, with the S&P 500 up 26% since early April, driven mostly by retail investors and company stock buybacks. Institutional investors, however, remain cautious, keeping overall stock holdings below pre-February levels. Some of them call the rally more speculative than solid.

July is historically a strong month for stocks, averaging a 2.5% gain over the past two decades. Despite ongoing concerns like high valuations and slow economic growth, clearing the tariff deadline could remove a key short-term worry. Still, investors know trade tensions aren’t going away entirely.

Traders are watching closely as a temporary suspension on U.S. import tariffs is set to expire next Wednesday. If tensions don’t rise, markets could react positively. Trade negotiators from key U.S. partners are working fast to avoid new tariffs, but progress is mixed, Vietnam struck a partial deal, while talks with Japan are struggling.

Technically, on the weekly chart, SPX is showing a clear upward trend with solid momentum. If this strength continues, especially with help from improving trade conditions, the index could rally further, potentially reaching the 6,500 Fibonacci resistance zone.

Stocks

Sector’s Weekly Performance:

This week, nearly all sectors of the market saw solid gains. Materials, Technology, and Financials led the way..

- Materials: Surged 3.1%, driven by Packaging Corp of America’s climb following its deal to acquire Greif’s containerboard business.

- Technology: Gained 2.7%. First Solar surged on trade optimism and tax credit support. HPE and Juniper rose after resolving an antitrust case. Nvidia hit a new high, briefly nearing a $4 trillion market value. The semiconductor index added nearly 2%.

- Financials: Increased 2.6%, as major banks rallied after clearing the Fed’s stress tests, clearing the way for dividends and buybacks. The S&P 500 bank index rose 4%, with regional banks jumping over 6%.

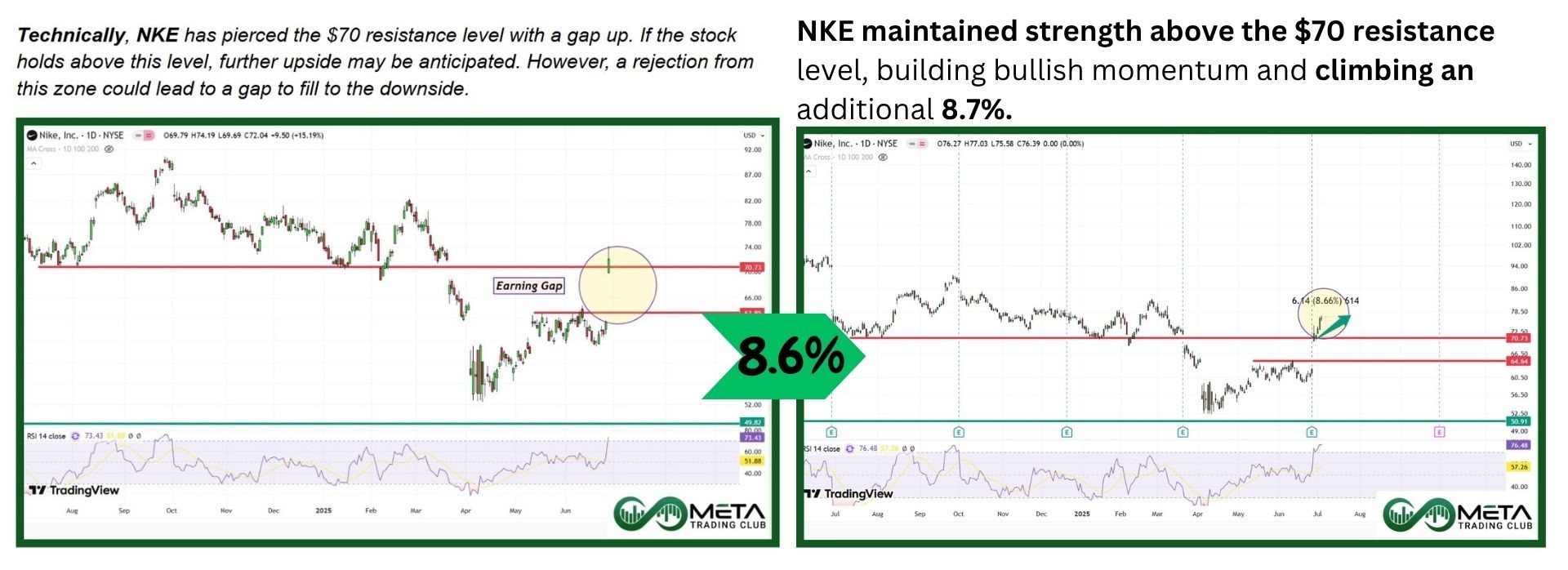

- Consumer Discretionary: Advanced 2.4%. Casino stocks climbed on strong Macau gaming revenues. Nike gained after news of a Vietnam trade deal. Tesla had a volatile week sliding after comments from Trump, then recovering on better Q2 deliveries, but still ending down about 3%.

- Communication Services: Rose 1.4%. Meta’s stock dropped over 2% despite a price target increase, as concerns lingered over its investment in Scale AI.

- Healthcare: Up 0.9%. Moderna advanced on promising flu vaccine trial results. Centene, however, tumbled 38% after withdrawing its 2025 forecast.

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- Datadog (DDOG): Soared 17% after it was announced that the software maker would replace Juniper Networks in the S&P 500 index beginning July 9.

- Oracle (ORCL): Jumped 13% as OpenAI plans to rent 4.5 gigawatts more of data center power from Oracle to support its growing AI operations.

- Synopsys (SNPS): Rose 9% after the company said the U.S. had eased restrictions on exports of semiconductor design software to China.

- Royal Caribbean (RCL): Climbed 8% thanks to cruising demand staying strong into 2025, the company is using loyalty data, exclusive experiences and digital integration to convert demand into higher guest spend and repeat bookings

- Amgen (AMGN): Lifted 7% by positive trial results for one of its key obesity drug, MariTide. In a mid-stage trial, the drug helped patients lose an average of 20% of their body weight over a year

- NXP Semiconductors (NXPI): Gained 7% on strong results driven by high demand in auto and industrial semiconductor markets.

- Apple (AAPL): Rose 6% after sales of iPhones in China grew for the first time in two years.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold (XAU/USD) prices have stayed steady since hitting a record high on June 13.

The metal is getting support from the weaker U.S. dollar, which just hit its lowest level since early 2022 as the economy slows. Many expect the Federal Reserve to cut interest rates again this year, which could also support gold.

Meanwhile, President Trump is set to sign the “Big Beautiful Bill,” which includes tax cuts for the wealthy, reduced spending on social programs, and adds over $3 trillion to the national debt.

Rising debt, falling dollar, and trade tensions might push the Fed to adopt a more supportive policy. With inflation risks and central banks continuing to buy gold, there’s a growing belief that gold could rise further within the next year.

Technically, Gold has been trading in a tight range over the past few weeks. To resume a bullish trend, it needs to break above its all-time high. On the downside, a drop below the $3,150 support zone could signal further declines

WTI Crude Oil set a weekly gain of 1.4%, bouncing back from its biggest drop in over two years, supported by fresh U.S. sanctions targeting Iranian oil exports. These sanctions aim to disrupt a network of companies and ships helping Iran trade crude, increasing pressure on Tehran.

The recent trade deal between the U.S. and Vietnam gave a slight boost to oil markets, but broader uncertainty remains. Key trading partners like the EU and Japan still haven’t finalized deals ahead of the July 9 tariff deadline.

OPEC announced a bigger oil production increase for August, 548,000 barrels a day instead of the 411,000 that was expected. Oil may see downward pressure after this report was released on Sunday.

The group, including major players like Saudi Arabia and Russia, is shifting its strategy. Rather than trying to keep prices high, they’re focusing on boosting their share of the market while demand is strong and supplies are tight.

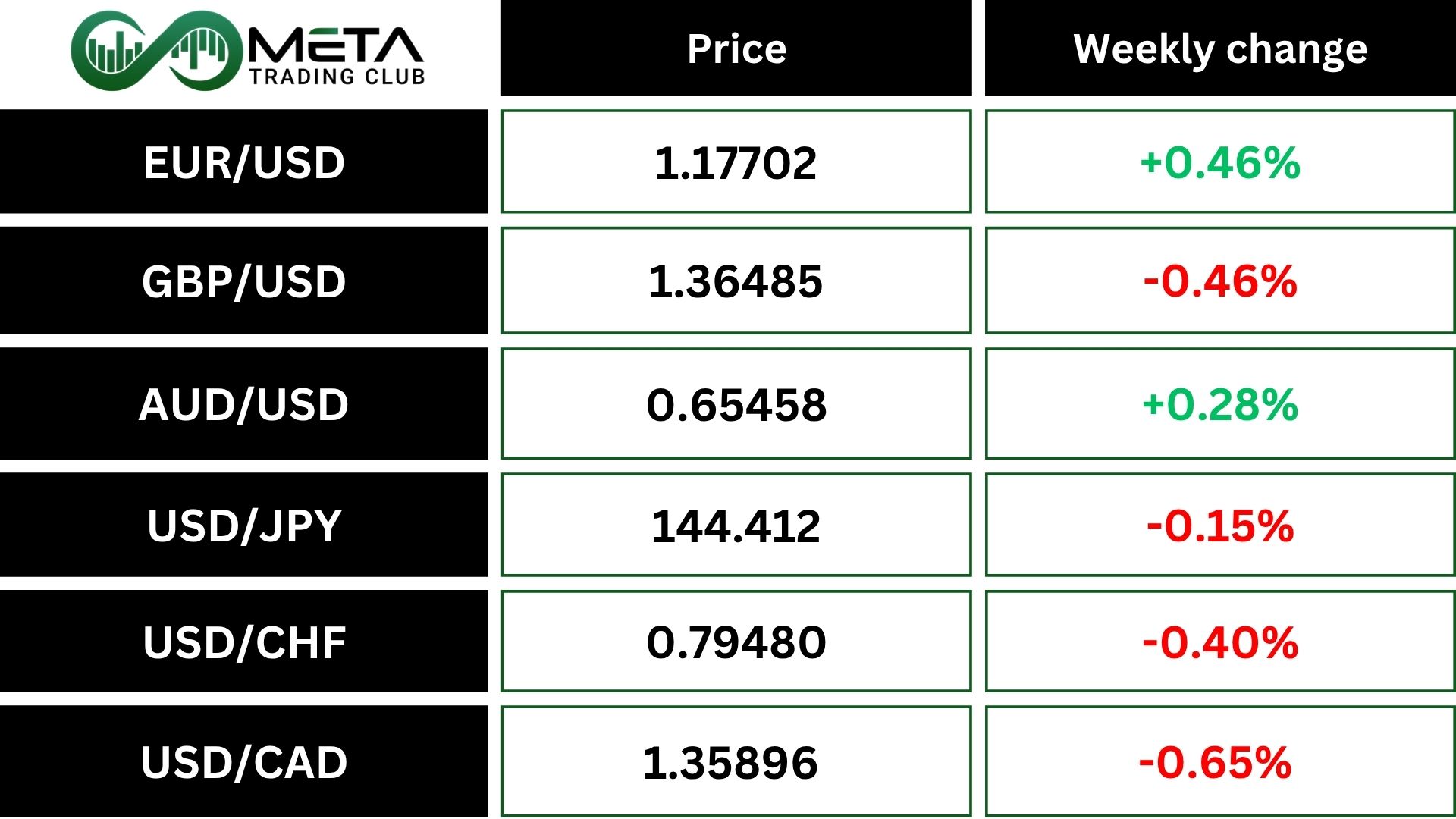

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The U.S. dollar had a rough first half of the year, its worst since 1973, largely due to uncertainty surrounding new trade tariffs introduced by President Trump. Since the announcement on April 2, the dollar has dropped more than 6%, hitting a three-year low against both the euro and the British pound.

Adding to the pressure, Trump announced that many countries will receive official notices detailing the tariff rates they’ll face, signaling a shift away from one-on-one trade negotiations. These developments have raised worries about the U.S. economy and the reliability of its government bonds.

Last week the dollar index dipped slightly to 96.92, even after gaining some ground the previous day. Meanwhile, the euro edged up to $1.178, and the yen and Swiss franc both strengthened against the dollar.

Technically, DXY has reached oversold territory on the weekly RSI as it tests the $97 support zone. Given the oversold conditions, a potential rebound from this level is possible. However, if the index breaks below last week’s low, further downside toward lower support levels could follow.

Crypto

Bitcoin is staying just above the $108,000 mark as buyers continue to push forward despite a shaky start to July. But behind the scenes, the outlook isn’t entirely solid.

Two key support zones ($106,738 and $98,566) where a large number of holders are concentrated. These price levels are crucial for bulls to protect. If Bitcoin drops below them, it could trigger stronger selling pressure and lead to a bigger pullback.

Technically, To stay on a bullish track, Bitcoin needs to close the week above $108,890, which is acting as a key resistance level. This price point is currently blocking its upward move, and breaking through it could open the door for a push toward new all-time highs.

However, if Bitcoin fails to close above this level, its price could remain unstable and potentially fall back toward the $106,000 support zone. That makes this week’s closing level especially important for Bitcoin’s short-term direction.

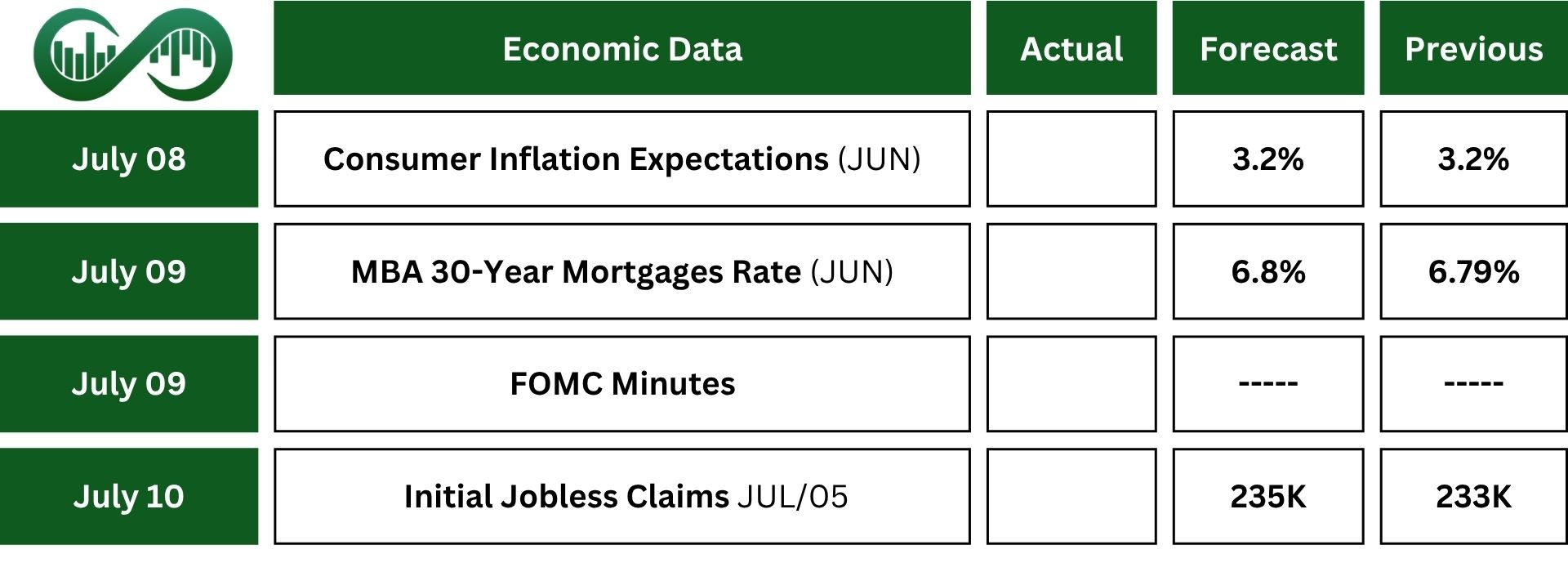

Next Week’s Outlook

Economic Events

The pause on higher tariffs from April is about to expire. If no new trade deals are made, the U.S. could start charging much higher import taxes, which might shake up markets.

The Federal Reserve is in the spotlight too. Several officials will be giving speeches, and minutes from their last meeting will be released, giving clues about future interest rate moves.

As for economic reports, it’s a quieter week, but important updates include jobless claims, consumer credit, small business confidence, and the government’s monthly budget numbers.

Earnings Events

Second quarter earnings season is starting soon. Big companies like Delta Air Lines (DAL) and Conagra (CAG) Brands will report their results on Thursday, and investors will be watching closely.