Last Week’s report

Economic Reports

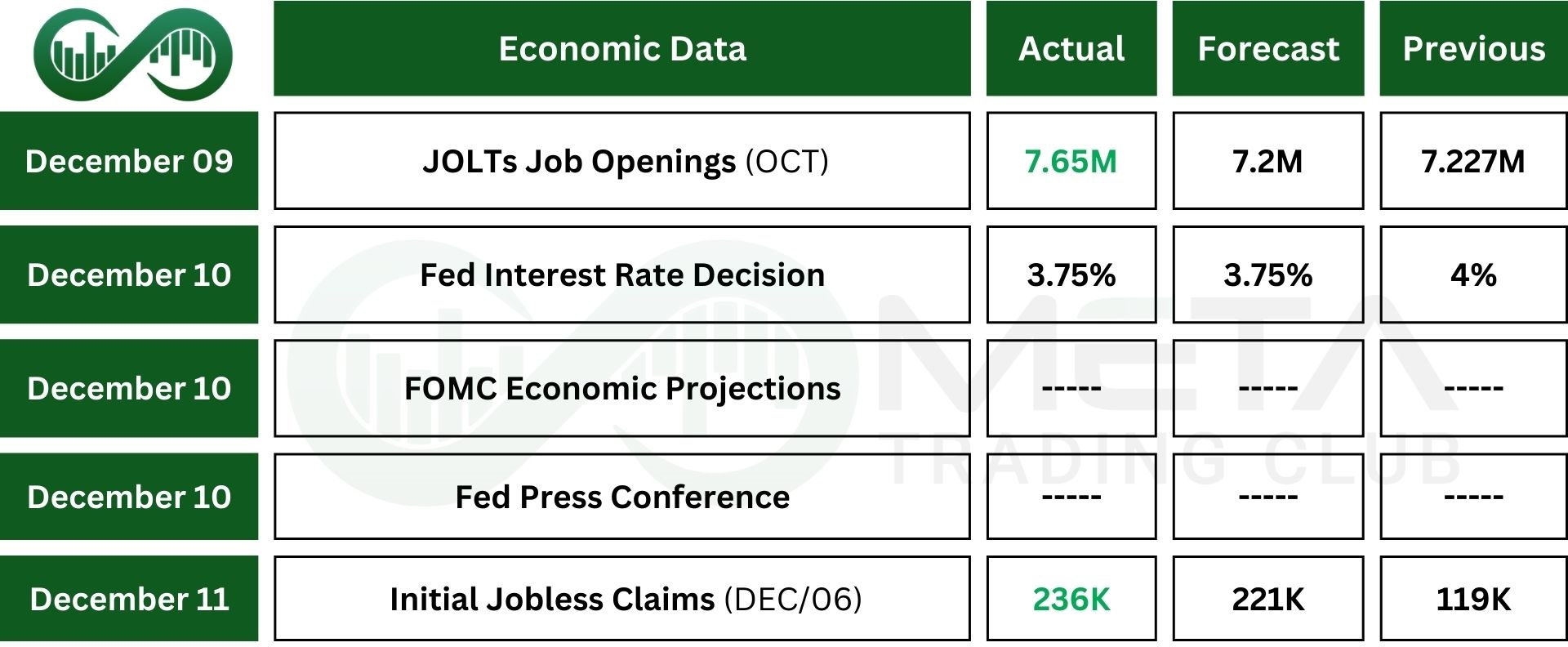

U.S. job openings edged up to 7.67 million in October, slightly above September’s 7.66 million. September had already shown a sharp 431,000 jump from August, with both months beating expectations.

Most of the gains came from trade, transportation, and utilities, along with health care, while openings fell in professional and business services, the federal government, and leisure and hospitality. The September and October reports were released together because of the 43‑day government shutdown, with September data partly self‑reported and later updated.

The Federal Reserve lowered the federal funds rate by 25 bps to 3.5%–3.75% at its December 2025 meeting, its third straight cut and the lowest level since 2022. The decision was split, with three officials dissenting, an unusually high number not seen since 2019. Stephen Miran argued for a larger 50 bps cut, while Austan Goolsbee and Jeffrey Schmid preferred to keep rates unchanged.

The Fed left its longer‑term rate outlook the same, signaling just one more cut in 2026. Growth forecasts were revised slightly higher for 2025 and 2026, while PCE inflation projections were nudged lower. Unemployment estimates remained steady at 4.5% for 2025 and 4.4% for 2026.

U.S. initial jobless claims jumped by 44,000 to 236,000 for the week ending December 6, 2025, the biggest weekly increase since March 2020 and well above expectations.

The rise followed the Thanksgiving week, when claims had dropped to a three‑year low, and reflects the typical holiday‑related volatility that often continues through year‑end. Meanwhile, continuing claims fell to 1.838 million in late November, the lowest since April and well below forecasts, after a downward revision to the prior week’s figure.

Earnings Reports

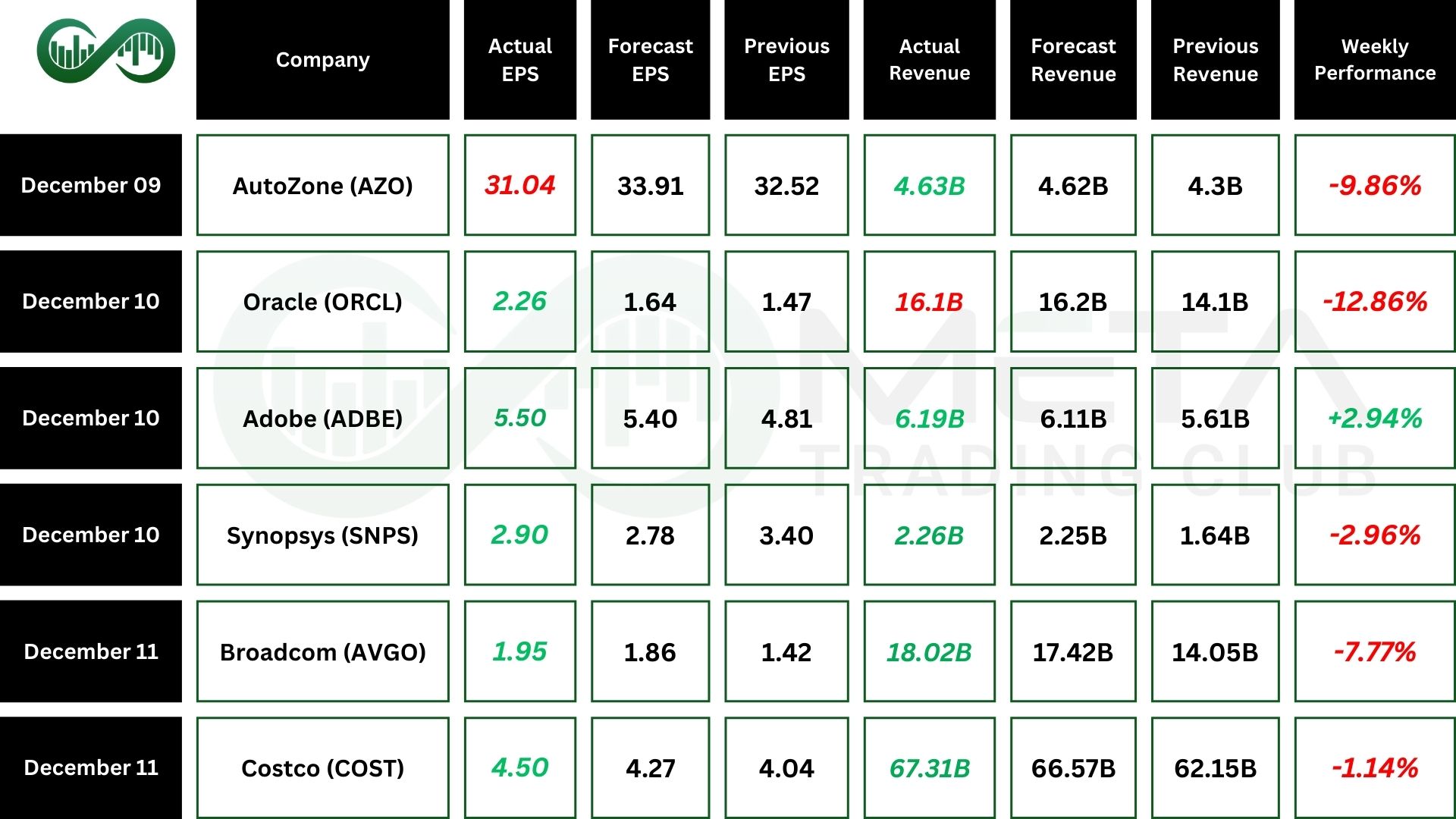

Oracle

Oracle (ORCL) reported strong cloud growth and rising financial strain. Revenue missed expectations despite a big earnings beat boosted by a one‑off Ampere stake sale, while cloud and AI‑infrastructure demand continued to surge.

Heavy spending on data centers has pushed Oracle into deep free‑cash‑flow losses and rising debt, raising concerns about profitability and leverage as margins slip and borrowing needs grow.

A massive $523 billion cloud backlog, including its large OpenAI contract, underscores long‑term opportunity but also execution risk.

With Project Stargate accelerating and debt costs climbing, investors are increasingly questioning whether Oracle can sustain its rapid cloud expansion without compromising financial stability.

Adobe

Adobe (ADBE) reported solid Q4 results with revenue up 10% to $6.19 billion and non‑GAAP EPS rising 14% to $5.50.

Digital Media and Digital Experience units both posted steady growth, and the company generated more than $10 billion in operating cash flow. Management said AI‑driven recurring revenue now accounts for over one‑third of total ARR, reflecting rising use of AI features across its products.

Also, Adobe expects fiscal 2026 revenue of about $26 billion and strong ARR growth, and it confirmed plans to acquire Semrush to expand its marketing data capabilities, a move investors are watching closely as AI adoption accelerates.

Costco

Costco (COST) reported beating revenue and profit estimates as shoppers stocked up on essentials and affordable extras ahead of the holiday season.

Even with inflation and a soft labor market making consumers cautious, Costco continued to attract buyers with strong value offerings and its popular Kirkland Signature brand.

Same‑store sales rose 6.4%, topping expectations. Costco’s appeal to higher‑income households and its focus on deep value are helping it gain market share.

Broadcom

Broadcom (AVGO) reported strong Q4 results, with earnings up 37% and revenue rising 28% to $18 billion, driven by a 74% surge in AI‑related semiconductor sales and solid growth in infrastructure software.

Margins improved across the board, cash flow strengthened, and the company raised its dividend by 10%.

Despite the strong numbers, the stock fell more than 7% last week as investors reacted to its sharp 12‑month run‑up. Broadcom ended the quarter with higher cash reserves, slightly higher debt, and expects Q1 fiscal 2026 revenue to reach $19.1 billion, with AI sales projected to double thanks to strong demand for custom accelerators and Ethernet AI switches.

The chip maker’s earnings sparked questions about its sales forecasts, contract backlog, and anticipated future margins.

Indices

Indices’ Weekly Performance:

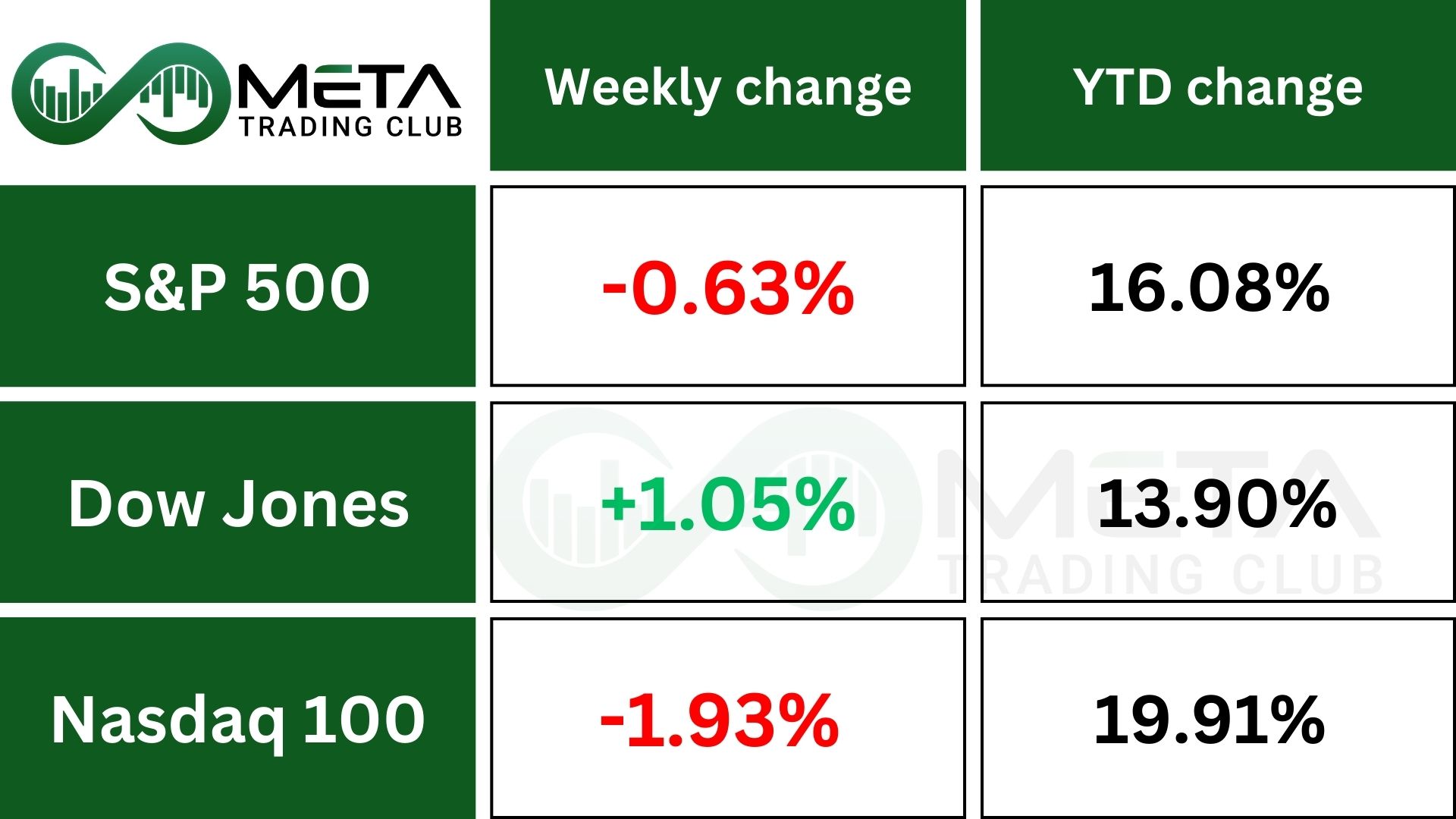

The major indexes moved in different directions this week, reflecting a clear rotation in the market. The S&P 500 slipped 0.6% as tech weakness weighed on the broader index, while the Nasdaq fell 1.9% amid sharp declines in AI‑linked and semiconductor stocks. In contrast, the Dow rose 1%, supported by strength in financials, industrials, and other value‑oriented sectors. Overall, the divergence shows investors pulling back from high‑valuation tech and shifting toward more defensive, stable areas of the market.

If the S&P 500 breaks above 6,900, it would be a bullish sign that could lead to more gains if the index stays above that level. The market had been stuck in a narrow range. SPX is now sitting at the top of the wider 6,500–6,900 band that has shaped trading since October.

Stocks

Sector’s Weekly Performance:

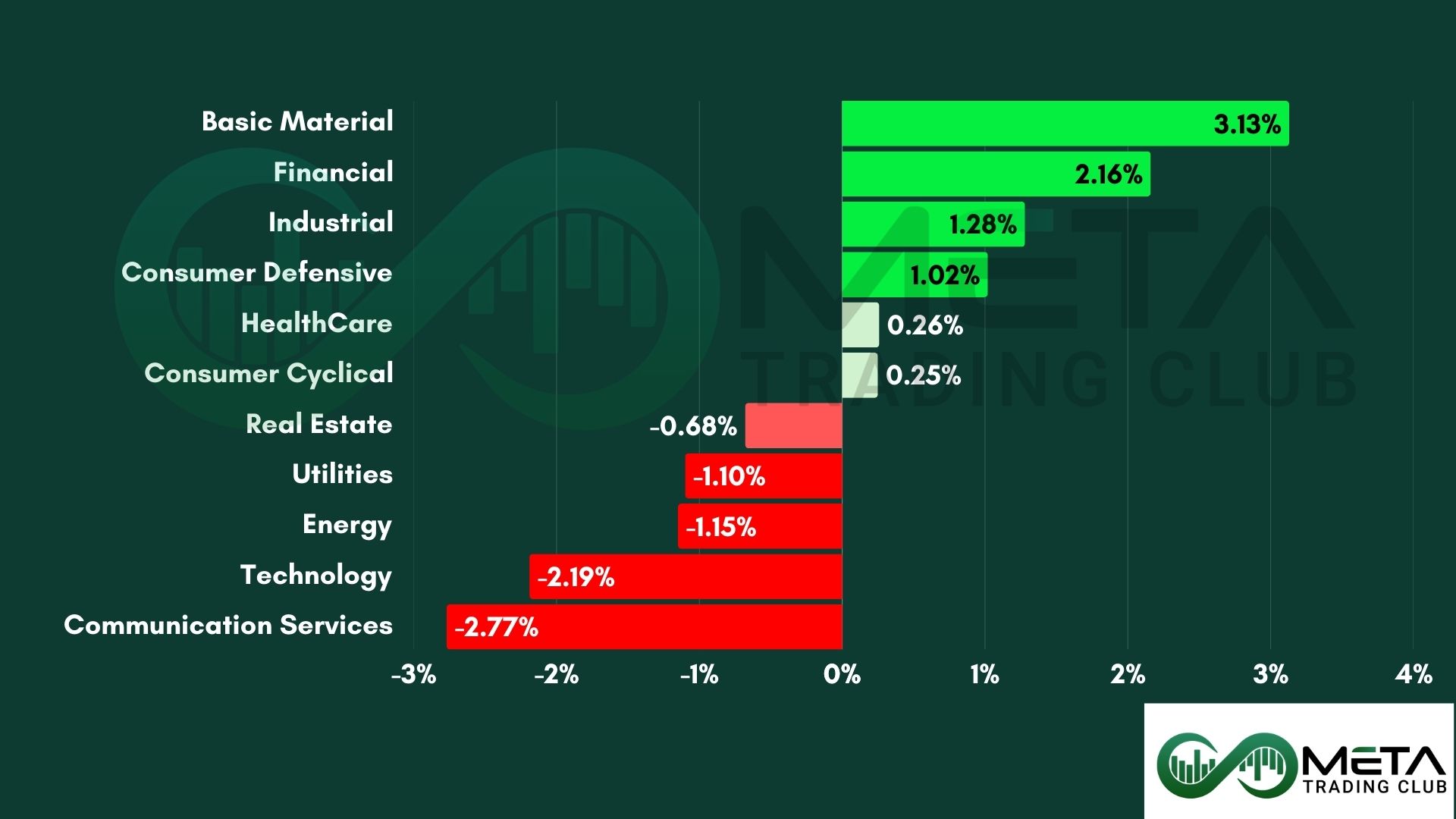

Tech is under pressure, especially AI-linked names; however, Defensive sectors and financials are gaining, supported by rising yields and cautious sentiment.

- Basic Materials surged 3.13%, the strongest sector; gold and silver pushed higher; miners and metals names broadly bid. Freeport‑McMoRan (FCX) and Newmont (NEM) caught flows as precious metals rallied.

- Financials climbed 2.16%, benefited from rotation out of tech; banks and insurers saw steady inflows.

- Industrials rose 1.28%, stable demand and defensive rotation supported the group; machinery and transport names firmed.

- Consumer Defensive gained 1.02% as investors moved into staples amid macro caution; household and food names outperformed.

- Consumer cyclical slid as Lululemon (LULU) jumped on a profit forecast boost and CEO transition. However, Costco (COST) finished flat despite beating revenue and profit expectations.

- Real Estate down 0.68% due to higher yields continued to pressure REITs.

- Utilities fell 1.10% after the rate‑sensitive sector lagged as Treasury yields climbed.

- Energy dropped 1.15% after softer demand expectations and rate pressure weighed on oil‑linked names.

- Technology plunged 2.19% as margin worries and AI fatigue weighed on the group. Oracle (ORCL) plunged after weak guidance; denial of OpenAI data‑center delays didn’t help sentiment. Broadcom (AVGO) sank on slimmer‑margin warnings, raising doubts about AI profitability. Nvidia (NVDA) slid, adding to tech pressure. The Philadelphia Semiconductor Index (SOX) dropped, its worst session since October.

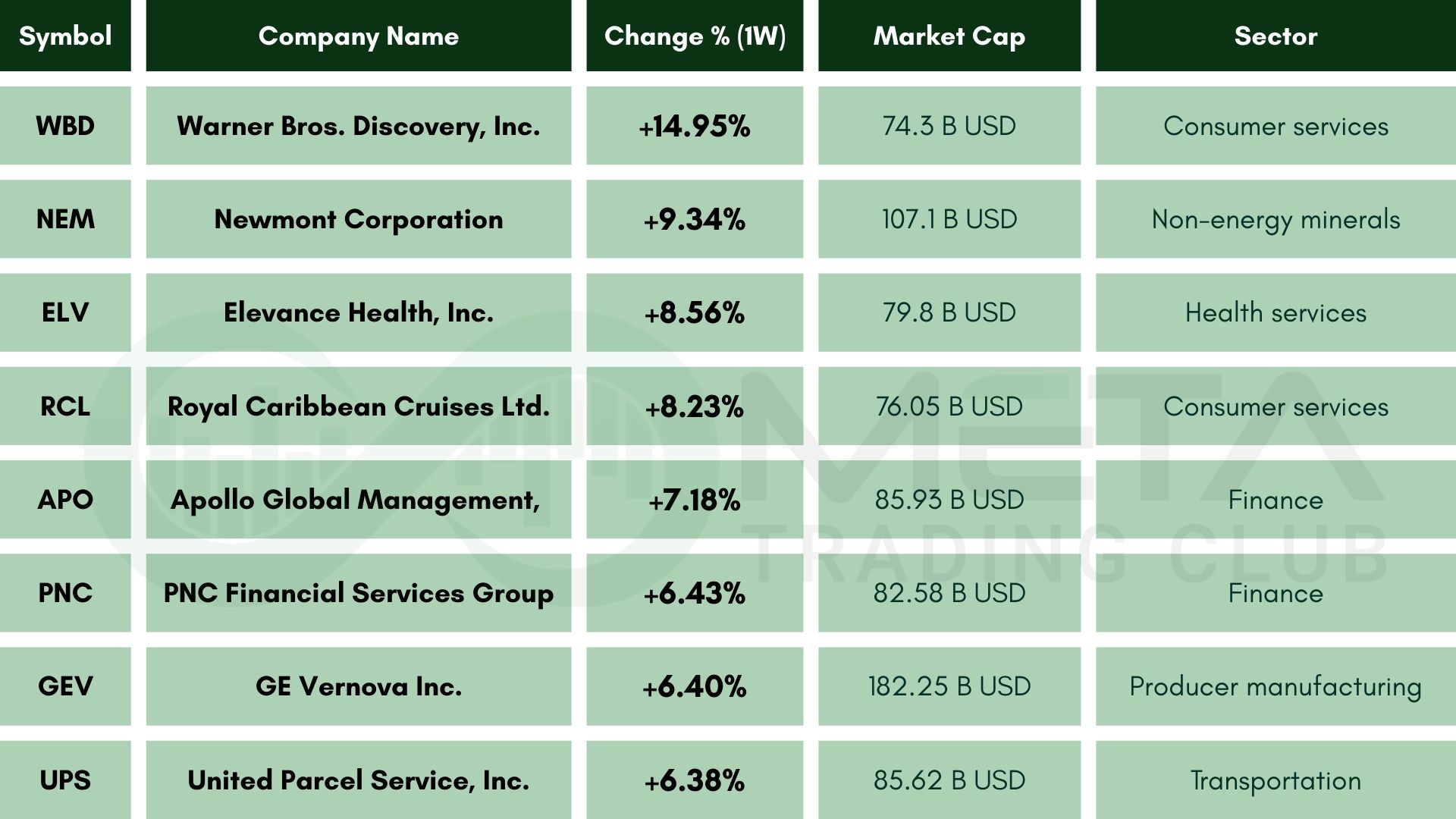

Top Performers

Last week saw a remarkable stock market performance, with several companies standing out as top gainers:

- Warner Bros. Discovery (WBD): Surged 14.9% due to a $30/share all‑cash hostile takeover bid from Paramount Skydance, which topped Netflix’s earlier offer and fueled expectations of a bidding war.

- Newmont Corporation (NEM): Gained 9.3% as gold prices rallied following the Fed’s rate cut, boosting miner margins and driving renewed investor interest in precious‑metal producers.

- Elevance Health (ELV): Rose 8.6% after strong insurer sentiment and investors rotating into defensive healthcare names.

- Royal Caribbean (RCL): Jumped 8.2% as travel demand remained resilient and lower interest‑rate expectations improved the outlook for cruise operators.

- Apollo Global Management (APO): Climbed 7.2% on continued inflows into private credit and alternative assets, alongside optimism around the firm’s expanding infrastructure and energy‑transition investments.

- PNC Financial (PNC): Increased 6.4% as bank stocks benefited from easing rate‑cut expectations and improving net‑interest‑income outlooks.

- GE Vernova (GEV): Advanced 6.4% on strong momentum in energy‑transition spending, with investors pricing in rising demand for grid upgrades and renewable‑power infrastructure.

- United Parcel Service (UPS): Gained 6.4% as cost‑cutting progress and improving delivery‑volume trends boosted confidence in the company’s margin recovery heading into year‑end.

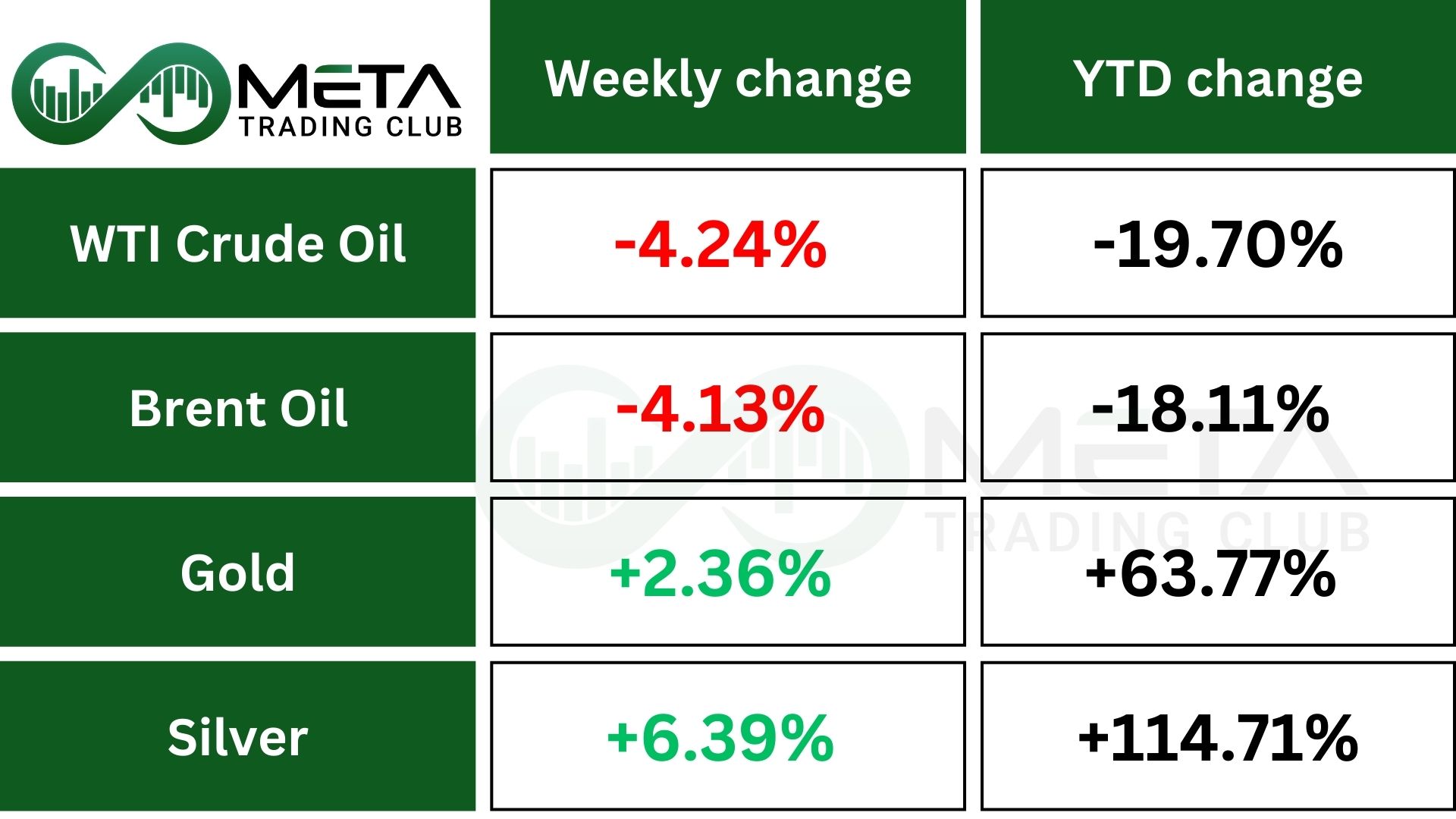

Commodity

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Metals

Gold climbed to around $4,290, its highest level in nearly two months, after the Fed’s latest rate cut weakened the dollar and boosted demand for non‑yielding assets.

Lower interest rates reduce the “opportunity cost” of holding gold, making it more appealing compared with bonds or cash.

With the dollar at an eight‑week low and silver also rallying, traders are now watching the $4,300 level and looking ahead to the December 16 jobs report for clues on the Fed’s next move.

For now, softer rates and a weaker dollar are keeping gold’s outlook strong, though volatility remains a risk.

Silver dipped below $62 per ounce after hitting record highs earlier in the week, as traders took profits and the market paused heading into the weekend.

Despite the pullback, the overall bullish trend remains intact. The recent Fed rate cut and a softer policy outlook continue to support prices, with Powell signaling no more hikes and only gradual cuts ahead. S

trong ETF inflows and solid retail buying point to a potential supply deficit next year, while industrial demand from solar, EVs, and data‑center growth is keeping fundamentals tight. At the same time, rising lease rates and higher borrowing costs for physical silver in London highlight ongoing delivery stress in the market.

Energy

Crude oil held near $58 a barrel but remained headed for a weekly loss of more than 4% as expectations of a global supply surplus weighed on prices.

The IEA reaffirmed its outlook for a record glut and noted inventories are now at a four‑year high, while OPEC kept its 2026 supply‑and‑demand forecast unchanged, suggesting a more balanced market ahead.

Geopolitical tensions added volatility earlier in the week, including the U.S. interception of a sanctioned Venezuelan tanker and Ukraine’s strike on another Russia‑linked “shadow fleet” vessel, its fifth since late November.

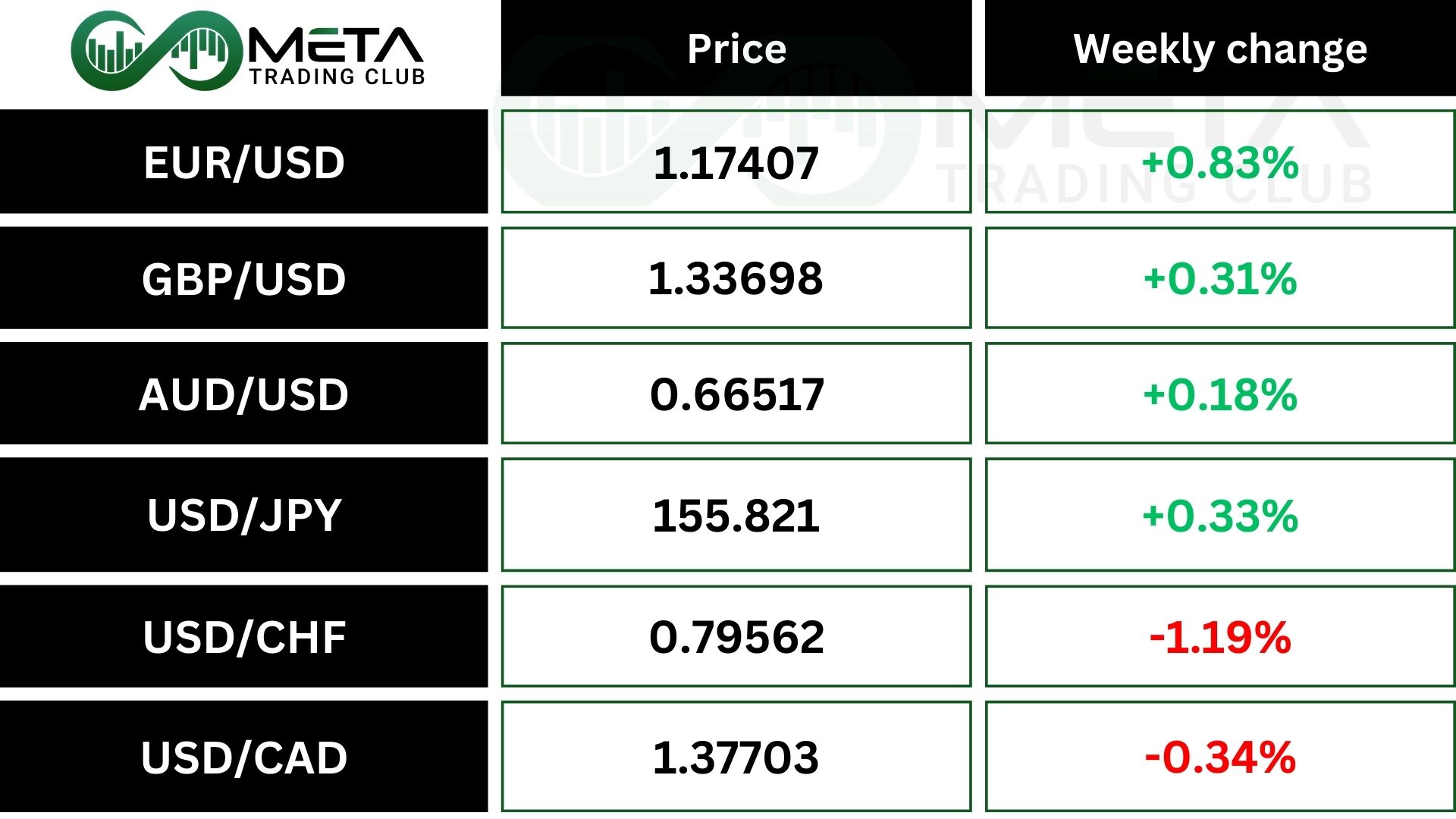

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The dollar index held near a two‑month low around 98.3, marking its third straight weekly decline, as investors absorbed recent Federal Reserve comments and reassessed the outlook for 2026 rate cuts.

The Fed lowered rates, its third consecutive cut, while signaling only one more reduction next year.

Fed officials were split: Kansas City’s Jeffrey Schmid warned inflation is still “too hot” and argued for tighter policy, while Chicago’s Austan Goolsbee opposed the cut but expects more easing in 2026.

Philadelphia’s Anna Paulson struck a more dovish tone, pointing to labor‑market softness as the bigger risk. Meanwhile, hawkish moves by central banks in Australia, Canada, and Europe added further pressure on the greenback, contributing to a broader weakening trend.

The Swiss franc strengthened to about 0.79 per USD, close to its highest level since 2011, helped by a weaker dollar and the Swiss National Bank’s decision to keep interest rates at 0% for a second meeting.

The SNB signaled a cautious stance, noting a slightly better economic outlook supported in part by a recent US tariff deal. SNB President Martin Schegel said he still expects inflation to rise gradually in the coming months, suggesting rates are likely to stay on hold for now.

Crypto

The crypto market has bounced modestly over the past three weeks, lifting total market value back to $3.07 trillion.

Bitcoin is up 11% from its recent low, and Ethereum has gained 18%, but there is still a possibility that a bear market is underway.

Bitcoin fell about 36% earlier in Q4 and is still trading below all major moving averages, from short‑term to long‑term. These averages are also sloping downward, which suggests sellers remain in control and the recent rebound may not signal a full recovery.

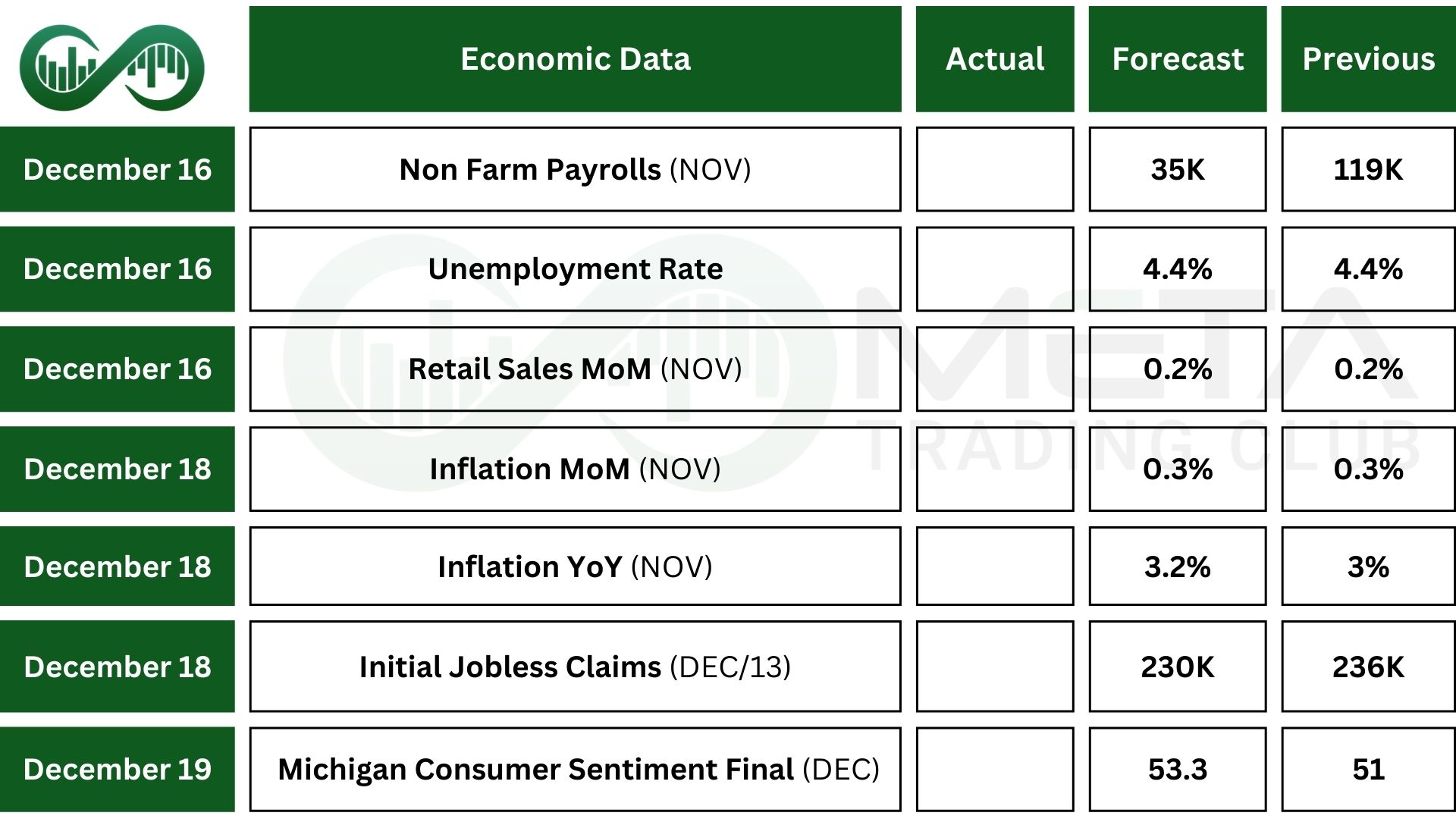

Next Week’s Outlook

Economic Events

A busy week of U.S. data is coming up, with markets focused on the delayed jobs report, November CPI, and retail sales.

The nonfarm payrolls for both October and November will be released, but only November’s unemployment rate will be available because October data were not collected during the government shutdown.

Wall Street expects 35,000 new jobs in November, including 40,000 in the private sector, with the jobless rate holding at 4.4%.

November CPI is projected to show headline and core inflation at 3.2%, still above the Fed’s 2% target.

October retail sales are expected to rise 0.2%, matching September’s slowest pace since May.

Additional releases include December flash PMIs, the NY Empire State and Philadelphia Fed manufacturing surveys, the NAHB housing index, November existing home sales, October capital flows, and the delayed September business‑inventories report.

Investors will also be watching comments from Federal Reserve officials for clues on policy direction heading into 2026.

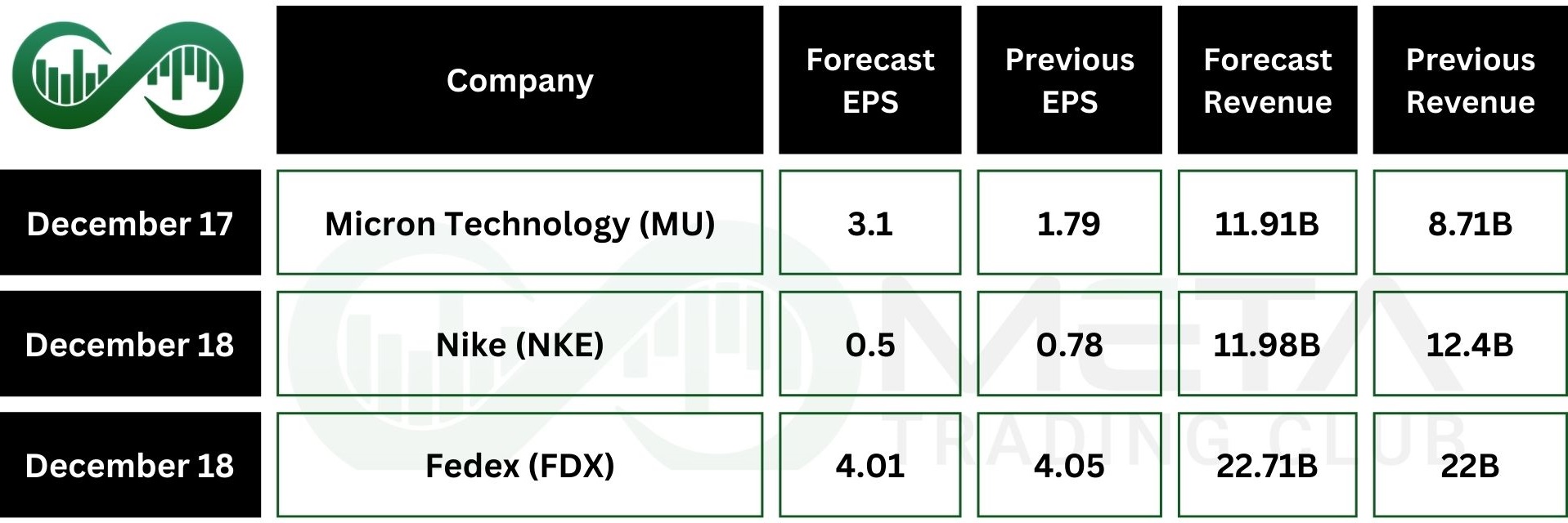

Earnings Events

Earnings season continues this week with results from Micron Technology (MU), FedEx (FDX), and Nike (NKE), giving investors a fresh look at trends across the market.