Last Week’s report

Economic Reports

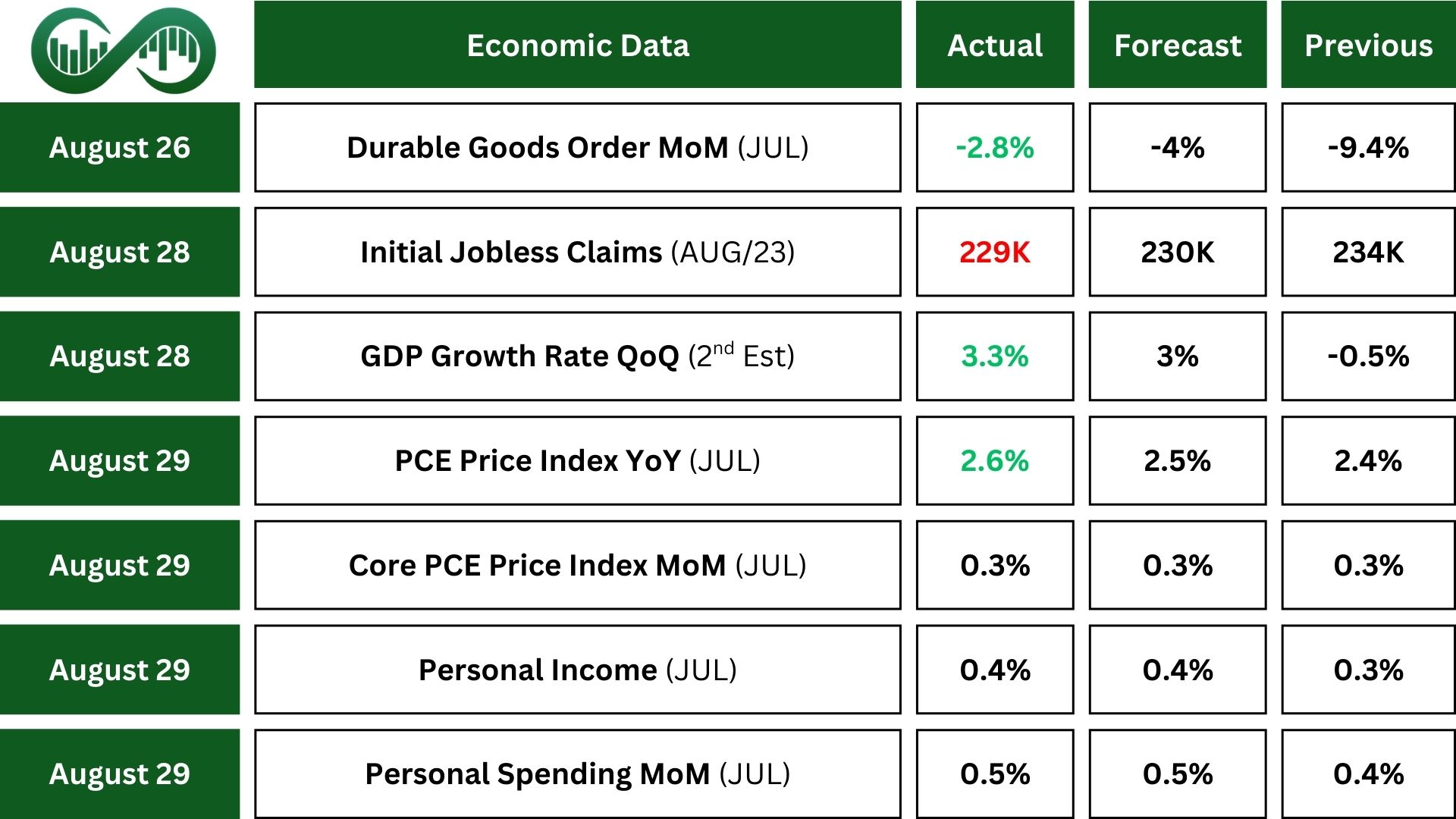

In July, U.S. Durable Goods Orders fell 2.8%, continuing a sharp decline from June, as companies slowed purchases after front-loading imports to avoid new tariffs. Manufacturing orders were especially weak.

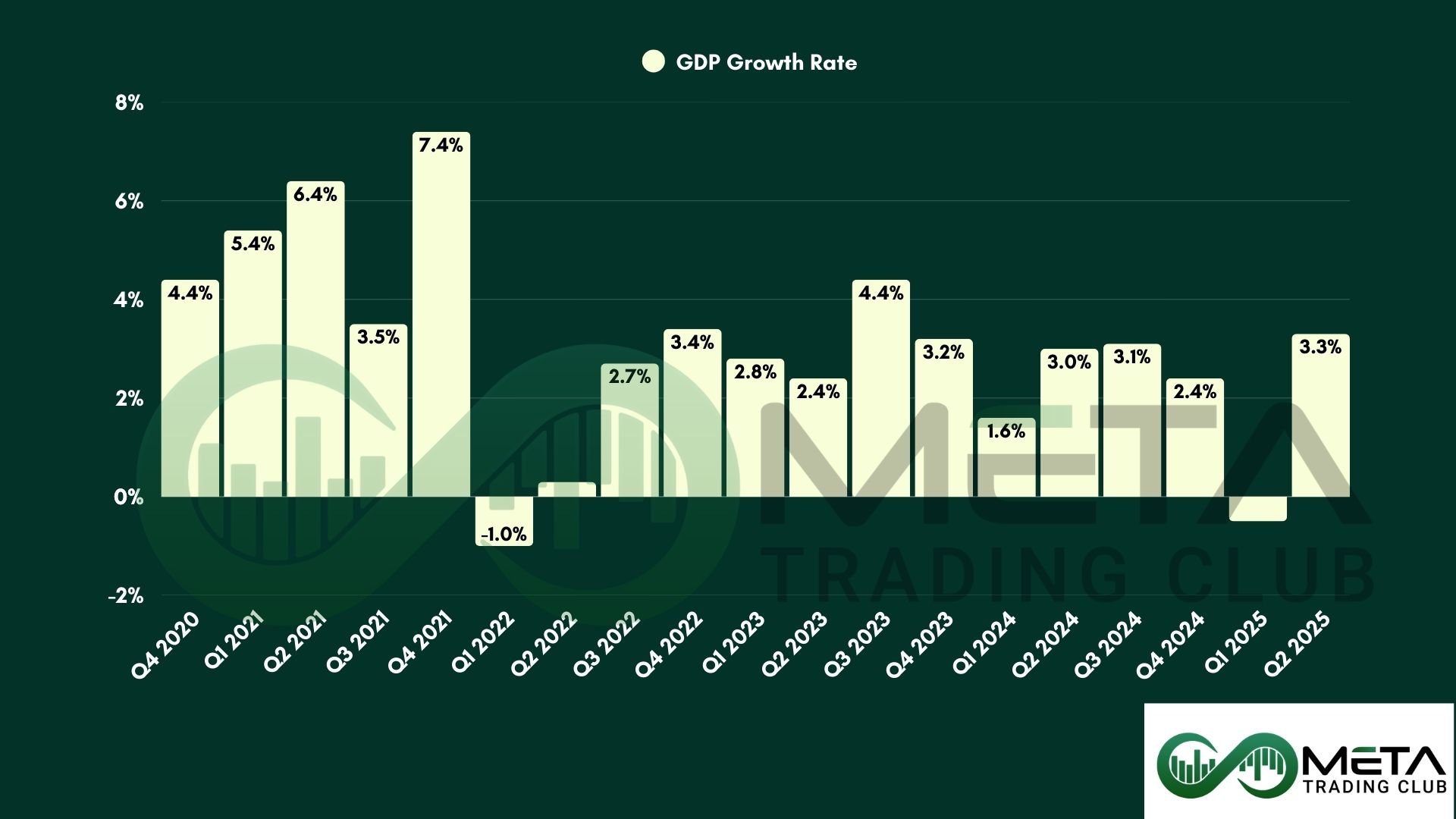

The economy showed strength in Q2, growing at an annual GDP Growth rate of 3.3%, rebounding from a 0.5% contraction in Q1. The growth was driven by higher consumer spending and reduced imports, though investment and exports declined.

Jobless claims showed slight improvement, with initial claims falling to 229K and continuing claims dropping to 1.954 million. While not signaling a major downturn, the data suggests a softening labor market. Claims from federal employees also declined, following recent government layoffs.

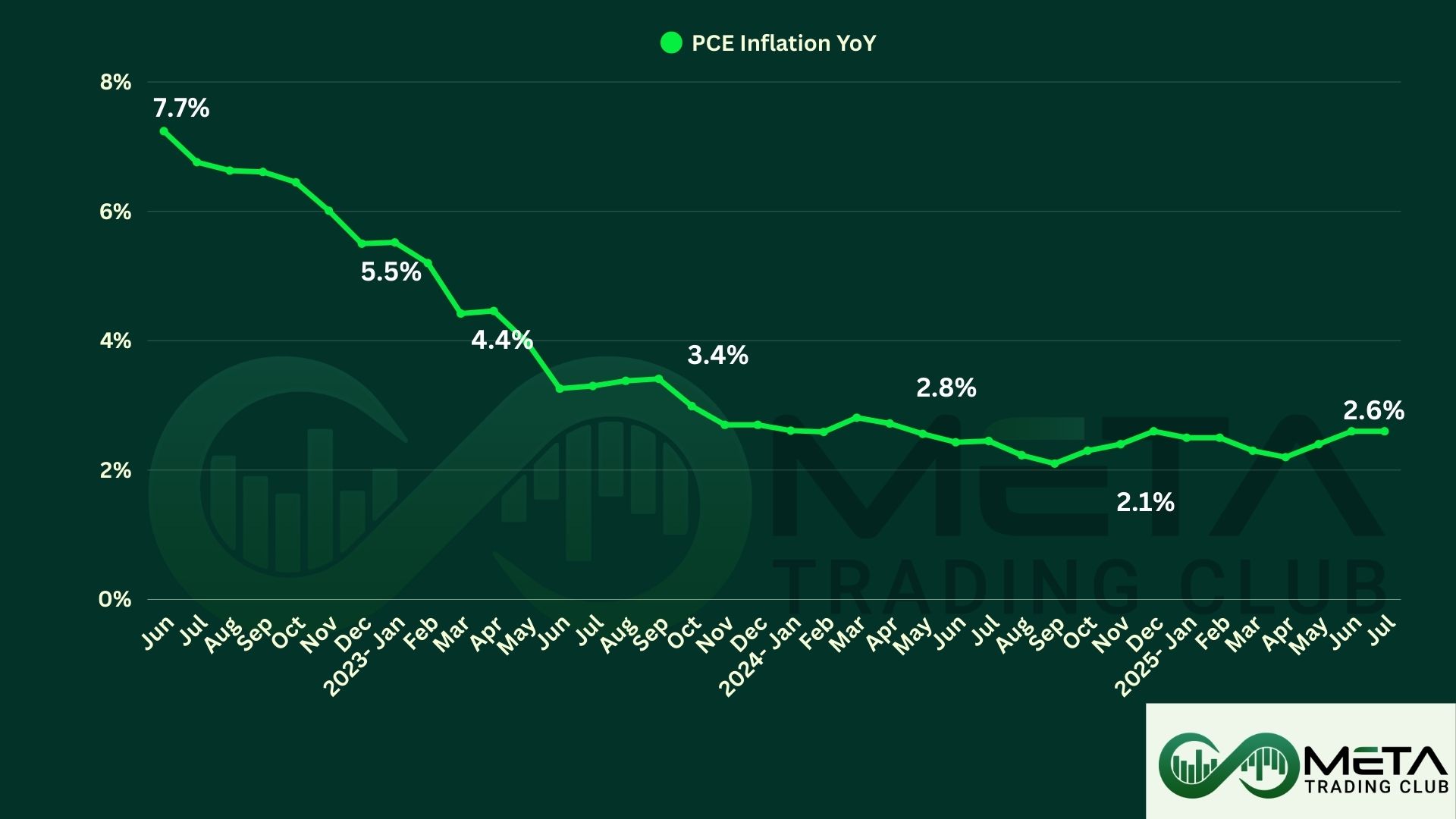

Inflation remained steady, with the Core PCE Price Index rising 0.3% month-over-month and 2.9% year-over-year, the highest in five months. Headline PCE inflation held at 2.6%, matching expectations. Goods prices dipped slightly, while service costs rose. Food and energy prices both declined. These figures support the Federal Reserve’s cautious approach to interest rates.

Personal income increased by 0.4% in July, mainly due to higher wages and business income. Disposable income also rose, with real disposable income edging up 0.2%. Consumer spending grew 0.5%, the strongest in four months.

However, consumer sentiment dropped to 58.2 in August, down from 61.7, as inflation worries and poor buying conditions for durable goods weighed on confidence. Expectations for business conditions and the labor market also declined, while inflation expectations rose to 4.8%, reflecting concerns over tariffs.

Overall, the U.S. economy is showing mixed signals, growth and spending remain solid, but inflation and labor concerns continue to weigh on sentiment.

Earnings Reports

Nvidia

NVIDIA (NVDA) reported strong Q2 results. Revenue reached $46.74 billion, up 56% from last year and above expectations. Adjusted earnings per share came in at $1.05, also beating estimates.

NVIDIA didn’t sell any H20 chips to China this quarter but did sell $180 million worth to another customer. Revenue from its Blackwell Data Center rose 17% from the previous quarter.

CEO Jensen Huang highlighted the strong demand for NVIDIA’s Blackwell AI platform and NVLink computing technology, calling them key to the future of AI. The company also announced a new $60 billion stock buyback plan, with $14.7 billion still available from a previous program.

Looking ahead, NVIDIA expects third-quarter revenue, slightly above analyst forecasts. After the report, NVIDIA’s stock fell 3.4%.

Technically, NVDA is losing momentum after failing to break the $184 resistance three times. If it drops below $169 support, the stock may fall further. But if it breaks the RSI downtrend and clears $184, it could rally strongly.

CrowdStrike

CrowdStrike (CRWD) reported strong growth in Q2 FY2026, with revenue rising 21% to $1.17 billion and subscription revenue up 20% to $1.10 billion.

While the company posted a GAAP net loss of $77.7 million, it achieved a record non-GAAP profit of $237.4 million. Annual Recurring Revenue reached $4.66 billion, and cash flow from operations hit $333 million.

CrowdStrike expanded its customer base, acquired Onum Technology, and was recognized as a leader in cybersecurity. It launched new AI-powered tools and partnered with AWS and NVIDIA to enhance its offerings.

Looking ahead, CrowdStrike expects Q3 revenue between $1.208 and $1.218 billion, below expectations, with strong earnings guidance. The stock fell after the report due to disappointing guidance for Q3.

Technically, CRWD could move higher if it breaks its short-term downtrend line, potentially reaching the next resistance level. But if it falls below the key $408 support, which aligns with a Fibonacci level, the stock may decline further.

Autodesk

Autodesk (ADSK) posted strong results for Q2 fiscal 2026, with non-GAAP earnings of $2.62 per share, up nearly 22% year-over-year and beating estimates.

Revenue grew 17.1% to $1.76 billion, driven by solid performance in its AECO segment, increased enterprise agreements, and momentum in the Autodesk Store.

Subscription revenue made up 94% of total sales, rising 17.8%, while billings jumped 36% to $1.68 billion. R

The company also repurchased 1.2 million shares for $356 million. The company lifted its full-year revenue and EPS guidance, now projecting up to $7.08 billion in revenue and $9.98 EPS, signaling confidence in sustained growth. The stock surged 9% after earnings were released.

Technically, if ADSK breaks above $327 with strength, it could rally toward its previous all-time high.

Indices

Indices’ Weekly Performance:

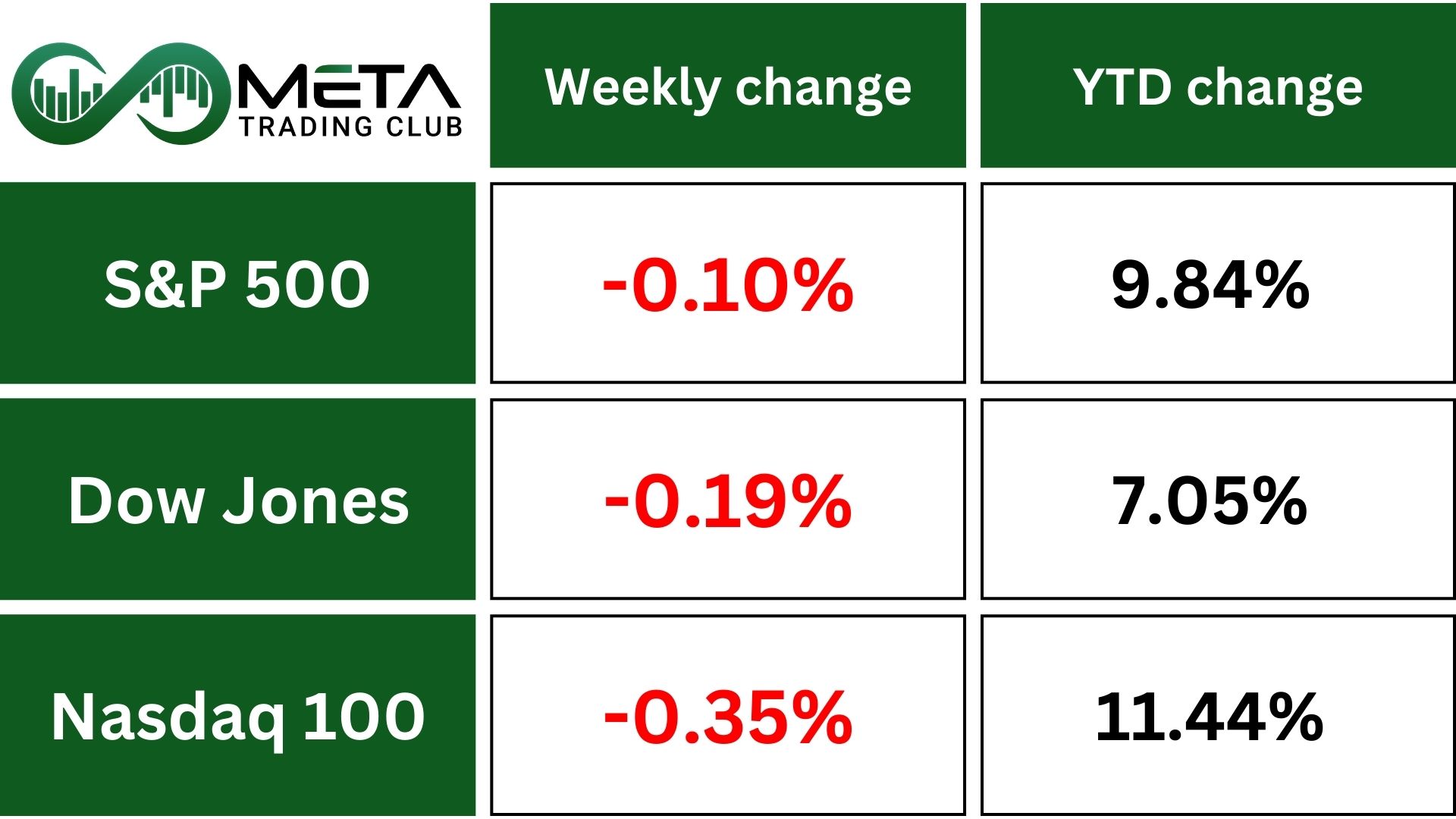

Last week, the S&P 500 slipped 0.1%, while the Nasdaq dropped 35% and Dow dipped 0.19%. The S&P 500 broke its three-week winning streak, weighed down by cautious sentiment around Nvidia’s earnings. Both the Dow and Nasdaq edged lower as traders braced for volatility in the tech sector. Last week’s dip-buying lacked momentum, and investors remained watchful of chipmaker developments.

For the month, all three indexes posted gains, with the S&P up 1.91%, the Nasdaq rising 1.58%, and the Dow climbing 3.21%. That marked four straight monthly gains for the S&P and Dow, and five for the Nasdaq. However, trading volume was lighter than usual ahead of the holiday.

Technically, if SPX keeps losing RSI momentum and breaks its short-term uptrend line, it could drop further. But if the RSI downtrend breaks and the index clears the strong resistance near 6500, a sharp rally may follow.

Stocks

Most sectors retreat, but Energy bucks the trend with solid gains

- Consumer Staples fall 1.45%. Keurig Dr Pepper dropped 17% after announcing an $18 billion acquisition of Dutch coffee company JDE Peet’s. Hormel Foods suffers its worst trading day ever after forecasting lower profits due to rising commodity costs

- Industrials decline 0.68%. Caterpillar slips after warning of a larger tariff impact expected in 2025

- Technology edges down 0.1%. Nvidia dips after a cautious sales forecast and news that Alibaba developed a new AI chip. Dell falls despite strong demand for AI servers. Semiconductor Index loses 1.5%

- Energy climbs 2.5%. Gains driven by falling U.S. crude inventories and potential effects of new U.S. tariffs on India.

Investor sentiment shifts. Retail traders grow more cautious, with some turning bearish. Technical trendlines gain attention, especially in China’s Large-Cap ETF.

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- Autodesk (ADSK): Surged +9.09% after strong quarterly earnings and upbeat guidance.

- The Cooper Companies (COO): Rose +4.36% on solid margins and analyst upgrades in its medical device segment.

- J.M. Smucker (SJM): Gained +3.55% after announcing divestitures and cost-cutting plans.

- Elevance Health (ELV): Climbed +2.65% on strong Medicare and Medicaid enrollment growth.

- Edison International (EIX): Advanced +2.58% as utilities attracted defensive investors amid volatility.

- UnitedHealth Group (UNH): Rebounded +2.51% on strength in healthcare services and cost control.

- Centene Corporation (CNC): Added +2.39% after contract wins and improved margin outlook.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold (XAU/USD) rose over 2% last week, approaching April’s record high of $3,500, as investors turned to safe assets amid uncertainty over U.S. monetary policy.

Expectations of a September rate cut, fueled by political pressure on the Federal Reserve and supportive comments from Fed Governor Christopher Waller, helped lift prices. Strong consumer spending in July and a 0.3% rise in the core PCE price index showed demand remains firm despite inflation. Year-over-year, core PCE rose to 2.9%, the highest since February. Overall, gold is up about 4% in August, marking its strongest monthly gain since April.

Technically, Gold is back at a key resistance, matching its June 16 high. A recent dip hints at a possible double top, which could trigger a fall toward $3,380–$3,400. But if prices break out, especially with dovish Fed signals, gold could climb to $3,500. For now, it’s holding strong above major moving averages.

WTI Crude Oil ended the week slightly higher, despite a drop ahead of the U.S. Labor Day weekend.

Prices were held back by expectations of weaker demand after summer and increased output from OPEC+. Geopolitical tensions, including the Russia-Ukraine war and potential U.S. sanctions, added some support but weren’t enough to drive prices higher.

Analysts expect refinery activity to slow and crude imports to rise, which could narrow the supply gap and push prices lower next month.

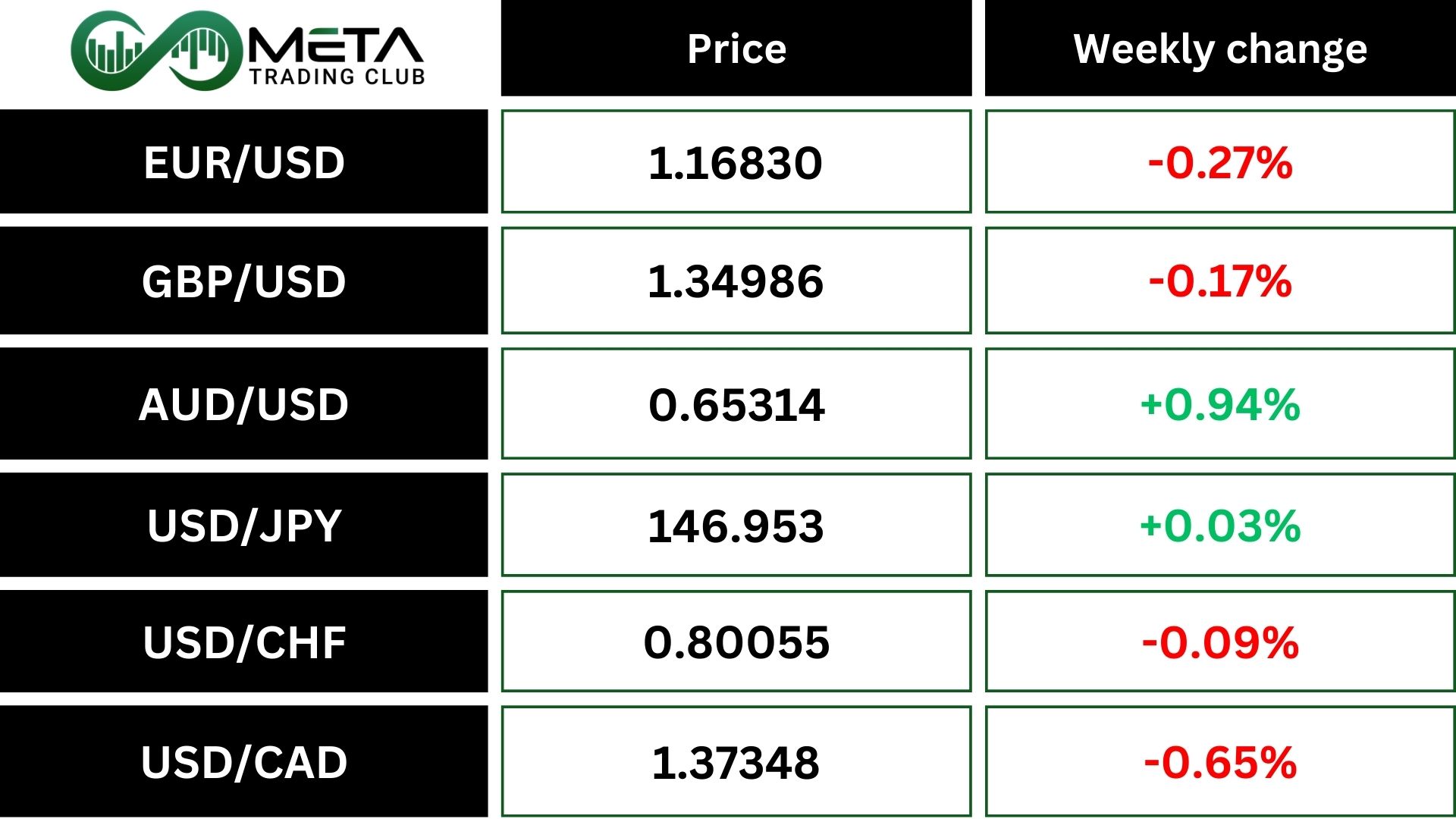

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The week began with attention on the market’s reaction to Fed Chair Powell’s dovish tone from Jackson Hole, but momentum faded quickly.

The dollar (DXY) initially weakened, then recovered as traders priced in two rate cuts by year-end. However, renewed selling later in the week reset sentiment. With month-end approaching, markets are quiet, and major currencies are barely moving, changes are limited to around 0.1% or 15 pips.

The U.S. dollar strengthened against the euro and pound last week, heading for a 2% monthly decline as traders anticipated a Federal Reserve rate cut in September. Although inflation data met expectations, the dollar failed to recover from a three-day losing streak. The PCE Price Index rose, keeping rate cut expectations high, with markets pricing in an 87% chance of easing.

Political pressure on the Fed, including efforts to dismiss Governor Lisa Cook, added to market uncertainty. Meanwhile, Fed Governor Christopher Waller voiced support for starting rate cuts next month.

In Europe, inflation expectations remained steady, with French and Spanish data showing mild price increases. The euro and pound both gained over 2% in August, while the dollar fell 2.5% against the yen and 1.3% against the Swiss franc.

Crypto

Ethereum is showing strong momentum, hitting a yearly high of 1.8 million transactions this month, with more Ether being staked following new U.S. regulatory guidance.

In contrast, Bitcoin has dropped over 5% in the past 30 days, partly due to a $2.7 billion whale trade that triggered a flash crash on August 24.

Despite the downturn, countries holding Bitcoin continue to invest heavily, with Strategy and Metaplanet buying 5,370 BTC in August.

Meanwhile, U.S. state regulators are teaming up with senior advocacy groups to limit crypto ATM usage, aiming to reduce fraud, with two states proposing new laws recently.

Technically, BTC has slipped below the key $111K resistance and is now hovering near $108K. If the $107K–$108K support zone fails to hold, a deeper drop toward $103K is likely.

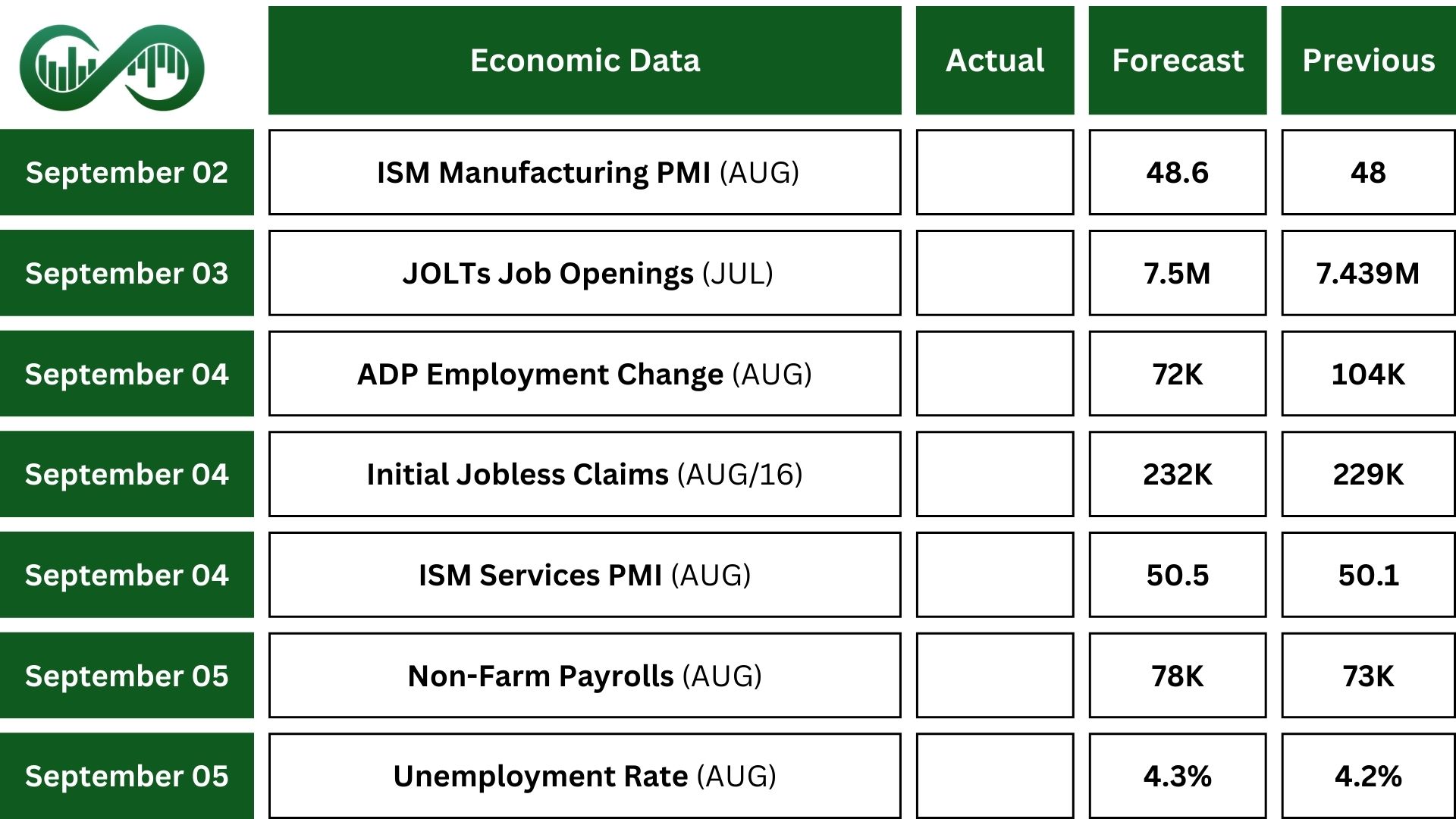

Next Week’s Outlook

Economic Events

In the U.S., attention is on the August jobs report, the last major labor update before the Fed’s September rate decision.

After last month’s downward revisions, officials are watching for signs of a slowing job market. Forecasts expect just 78K new NFP added and unemployment rising to 4.3%, the highest in nearly four years. Also, wage growth is likely to stay at 0.3%.

Investors will also focus on the ADP private-sector jobs report and JOLTS data.

Other key indicators include ISM surveys, showing weak factory activity but steady growth in services. The trade balance will be watched too, as tariffs continue to affect goods movement.

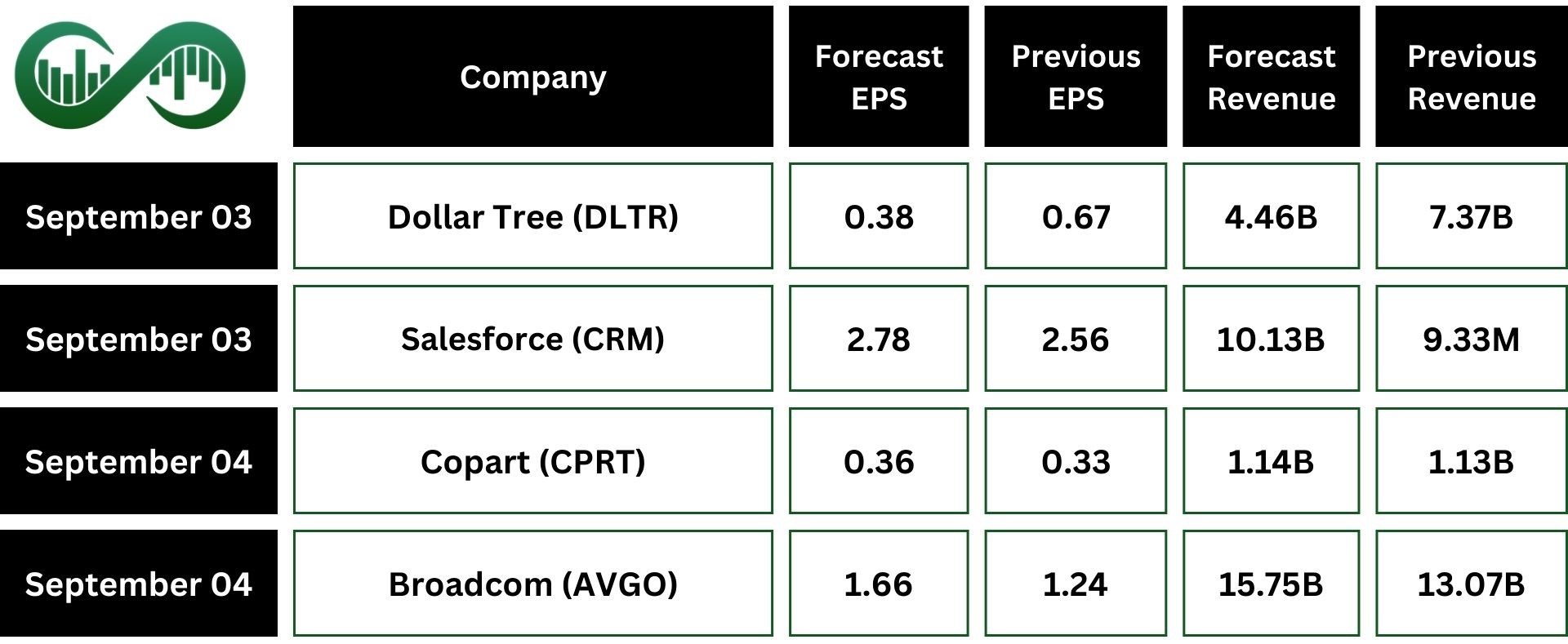

Earnings Events

Broadcom (AVGO) and Salesforce (CRM) are set to report earnings this week, and their results will play a key role in shaping investor sentiment toward the broader tech sector.