Last Week’s report

Economic Reports

Housing Market

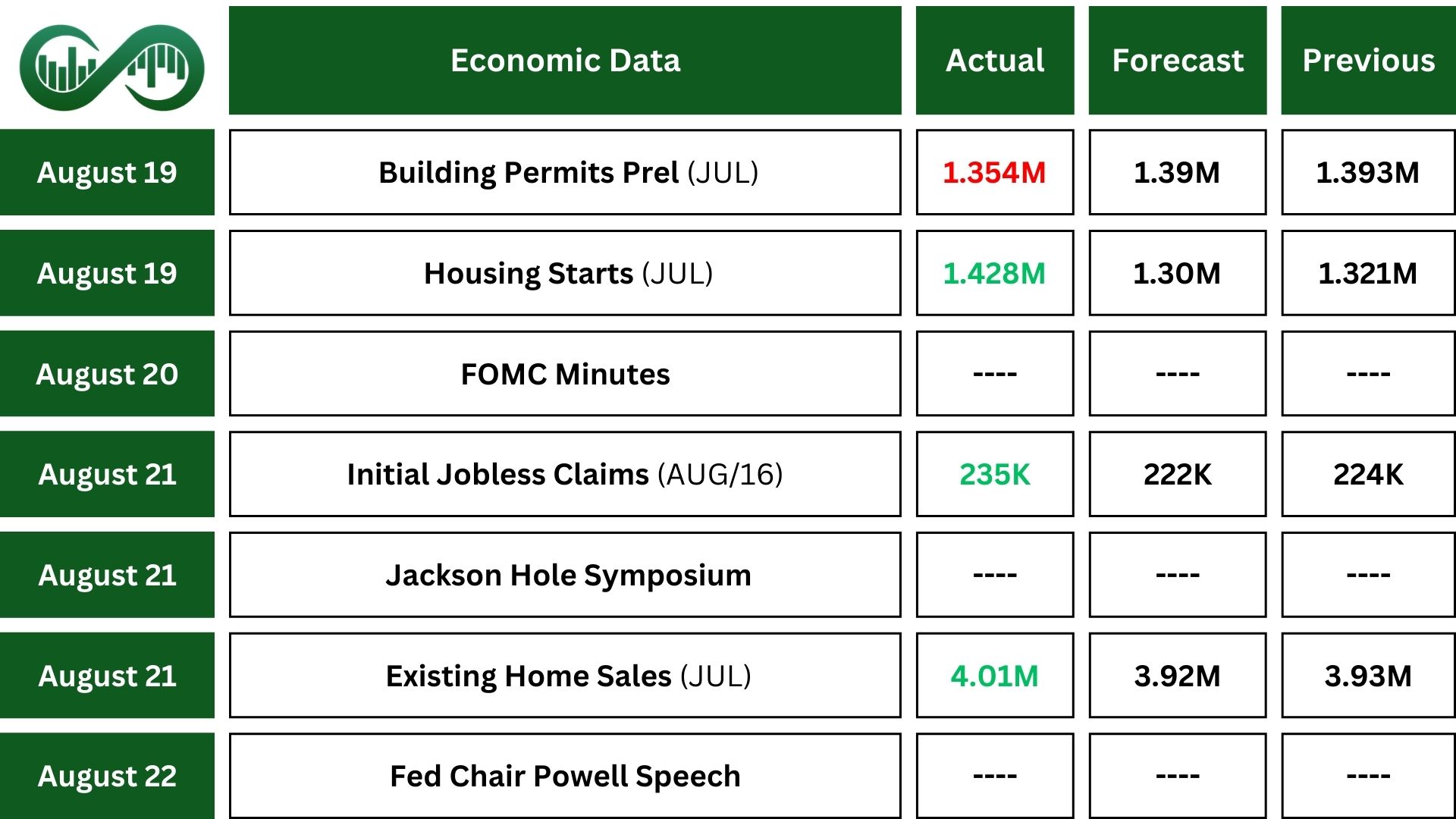

In July, U.S. building permits fell 2.8% to 1.354 million, the lowest since mid-2020 and below expectations. The decline was driven by a sharp drop in multi-unit permits, while single-family permits saw a slight increase.

Despite weaker permitting activity, housing starts rose 5.2% to 1.428 million, defying forecasts and marking a five-month high. This suggests continued strength in actual construction, even as future building intentions show signs of softening.

Sectors tied to active construction (homebuilders, materials, and equipment) may benefit from the rise in housing starts. Also, drop in building permits signals potential slowdown in future construction, which could weigh on forward-looking earnings and sentiment.

Job Report

This week, U.S. Initial jobless claims rose by 11,000 to 235,000, marking the highest level in about two months. The four-week average also edged up to 226,500, suggesting a gradual increase in layoffs.

Continuing claims, those who remain on unemployment benefits, climbed by 30,000 to nearly 2 million, the most since late 2021.

While the labor market isn’t showing signs of mass layoffs, the rise in claims points to a cooling trend. Hiring has slowed, and more people are staying on benefits longer, which could signal that finding new jobs is getting tougher.

Jackson Hole

At the 2025 Jackson Hole Economic Symposium, Federal Reserve Chair Jerome Powell delivered his final address, signaling a cautious shift in monetary policy amid rising inflation and a cooling labor market.

He acknowledged that risks to inflation remain elevated due to factors like U.S. tariffs and tighter immigration policies, while employment growth has slowed significantly.

Powell hinted that interest rate cuts may be considered soon, though any decision will depend on incoming data. The speech also emphasized the Fed’s commitment to balancing its dual mandate of price stability and maximum employment, while defending central bank independence amid political pressure.

Earnings Reports

Target (TGT) Q2 2025 earnings showed mixed results, with some signs of recovery but ongoing challenges.

The company reported adjusted earnings per share of $2.05, slightly above expectations, though down from $2.57 a year earlier.

Revenue came in at $25.2 billion, a 0.9% decline year-over-year, but still beat analyst forecasts.

Comparable sales fell 1.9%, with store traffic and discretionary spending remaining weak. However, digital sales rose 4.3%, driven by strong growth in same-day delivery services.

Non-merchandise sales, including advertising and memberships, jumped 14.2%, helping offset some of the pressure from markdowns and inventory costs.

The company maintained its full-year guidance, expecting a low-single-digit decline in sales.

Despite the earnings beat, Target’s stock dropped, reflecting investor concerns about shrinking margins and soft consumer demand.

Walmart

Walmart (WMT) second-quarter earnings showed strong sales growth but mixed profitability.

Total revenue rose 4.8% year-over-year to $177.4 billion, beating market expectations. U.S. comparable sales increased by 4.6%, with e-commerce jumping 25%, reflecting strong consumer demand.

Sam’s Club also performed well, with a 5.9% gain, while international sales grew 5.5%, driven by food and general merchandise.

Despite the solid revenue performance, earnings per share came in at $0.68, missing the expectations.

Operating income fell 8.2%, largely due to $450 million in legal and liability-related costs.

Walmart’s higher-margin businesses showed promising growth. Advertising revenue surged 46%. The company continues to invest in digital tools, artificial intelligence, and faster delivery services, aiming to reach 95% of the U.S. population with three-hour delivery options.

Despite the strong sales figures, Walmart’s stock dropped following the earnings miss. Investors remain focused on how the company balances growth with profitability amid rising costs and competitive pressures.

Indices

Indices’ Weekly Performance:

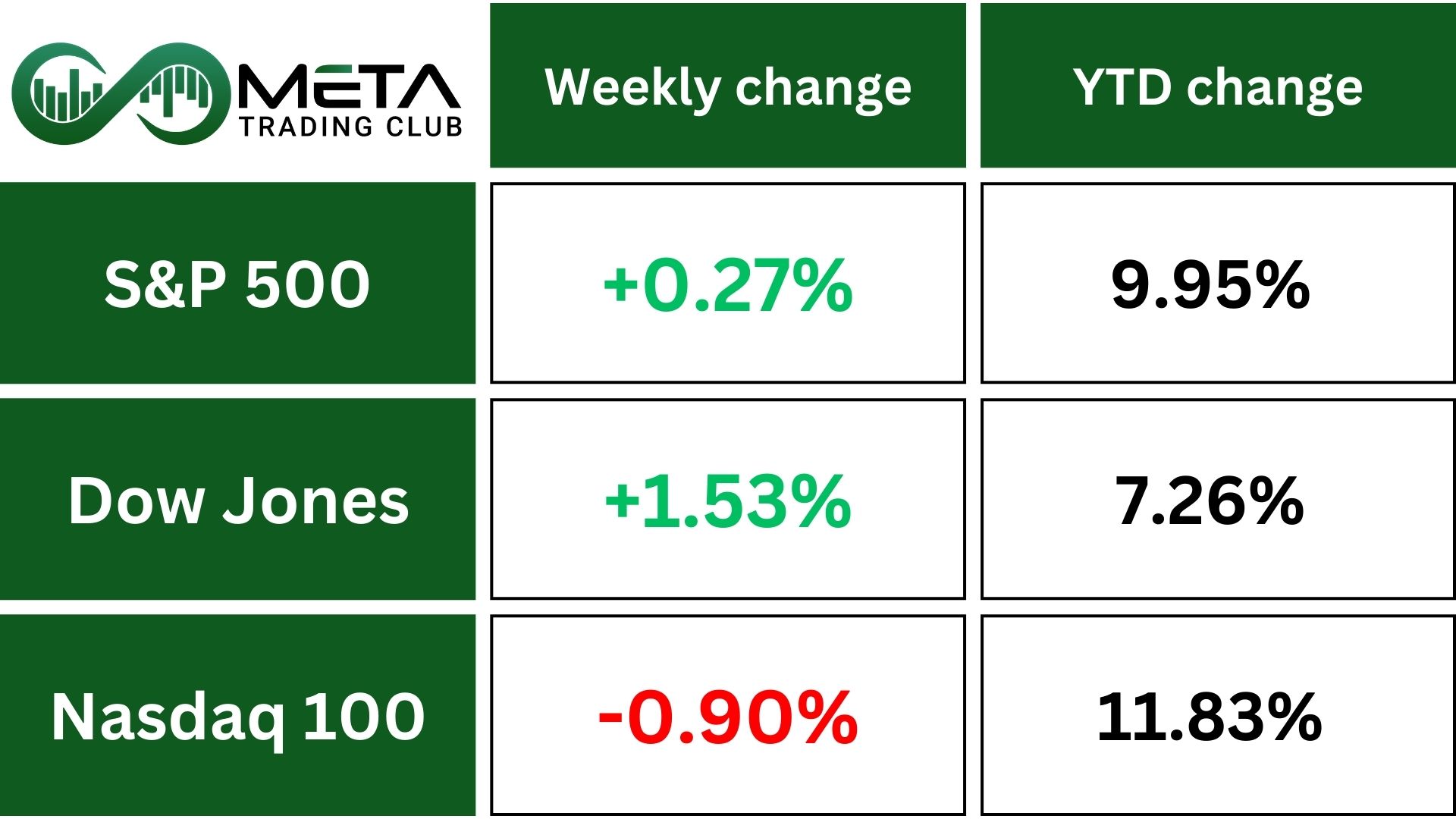

US stocks soared after Fed Chair Powell signaled the possibility of a September rate cut during his Jackson Hole speech, sparking the strongest cross-asset rally since April.

The Dow scored its first record closing high since Dec. 04, 2024.

Speaking at the Fed’s annual Jackson Hole Symposium, Powell noted that the shifting balance of risks in the economy “may warrant adjusting our policy stance,” while cautioning that inflation pressures remain.

Traders quickly ramped up bets on a 25 bps rate cut in September to roughly 91%. Tech the strength, with Tesla jumping.

The rally allowed markets to recover from earlier weakness tied to megacap tech, leaving the Dow and S&P 500 with weekly gains and trimming the Nasdaq’s losses.

Technically, SPX is approaching the 6500 Fibonacci resistance zone, if passes this zone could soar. However, if rejected then further decline anticipated.

Stocks

Sector’s Weekly Performance:

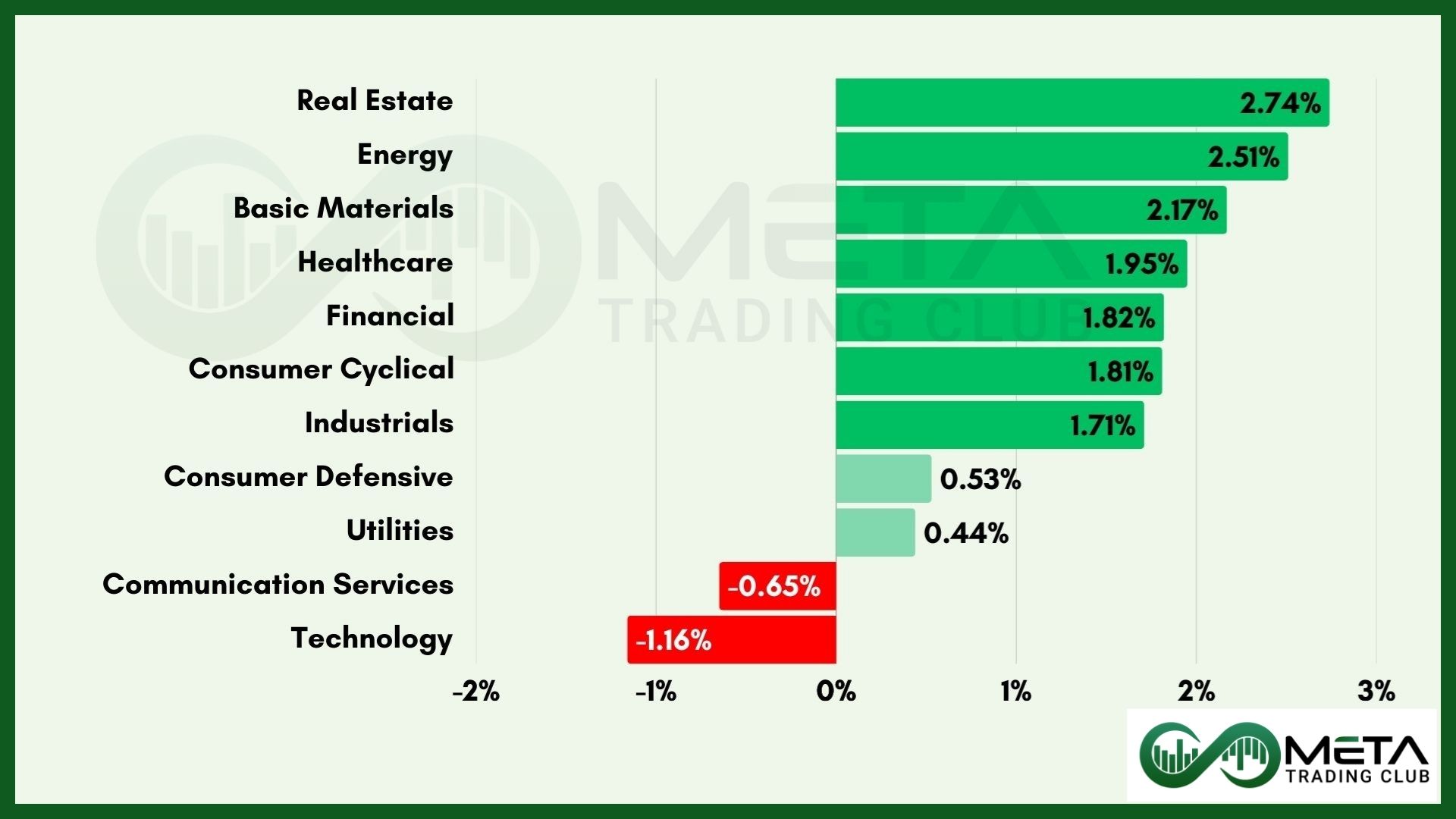

Most sectors moved higher this week, especially those tied to the economy. Only Communication Services and Technology lagged behind. Growth stocks took a breather compared to Value stocks, with Growth having its worst week relative to Value since late March.

- Real estate also climbed 2.7%, with REITs like Alexandria Real Estate and Prologis gaining from rate cut optimism.

- Energy stocks jumped 2.5%, boosted by hopes of a rate cut after Fed Chair Powell’s speech at the Jackson Hole Symposium.

- Financials rose 1.8% as banks rallied on Powell’s comments. The S&P 500 bank index gained 3% for the week, and regional banks surged over 5%, led by the KBW index.

- Consumer Discretionary stocks rose 1.8%, with Home Depot climbing after sticking to its yearly forecast and noting small price increases due to tariffs. Homebuilders like D.R. Horton, Lennar, and Pultegroup also rallied on rising rate cut expectations.

- Industrials were up 1.7%, helped by a big move in Dayforce, which soared 31% after a $12 billion buyout deal by Thoma Bravo.

- Consumer Staples edged up 0.5%. Walmart slipped after missing profit estimates for the first time in three years, even though it raised its annual forecast. Target also fell after naming a new CEO, despite beating Q2 expectations.

- Communication Services dropped 0.6%, although Alphabet rose Friday following news that Meta signed a $10 billion cloud deal.

- Technology was the weakest sector, falling 1.2%. Palantir was the worst performer in the S&P 500, sliding 10% as AI stocks showed signs of cooling off and short sellers profited. Intel rose earlier in the week after Japan’s SoftBank invested $2 billion. The semiconductor index ended the week mostly flat.

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- DayForce (DAY): Surged 31% after a $12 billion buyout deal by Thoma Bravo.

- Paramount Skydance (PSKY): Jumped 16% on news of a strategic partnership in the clean energy sector.

- LyondellBasell (LYB): Rose 10% due to better-than-expected quarterly results and cost-cutting measures.

- Packaging (PKG): Gained 10% on rising demand for sustainable packaging solutions.

- Royal Caribbean Cruise (RCL): Benefited 9% from record cruise bookings and strong summer travel demand. Positive guidance and reduced fuel costs added to the rally.

- Analog Devices (ADI): Advanced 9% on growing demand for industrial and automotive chips.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold (XAU/USD) prices climbed after Federal Reserve Chair Jerome Powell hinted at a possible interest rate cut in September.

Gold rose 1%, putting them on track for a weekly gain of the same amount after weeks of flat trading at the Jackson Hole Symposium. Powell suggested that a weakening job market could ease worries about inflation caused by tariffs. This shift in outlook may support the case for cutting rates again.

As a result, markets are now expecting a 0.25% rate cut in September. That’s boosting demand for gold, which doesn’t pay interest but tends to shine when rates fall.

Technically, Gold has been consolidating in a range between $3,240 and $3,440 for some time. It bounced off its 100-day moving average, showing renewed buying interest. For the next clear trend to emerge, gold needs to either break above $3,440 resistance or below $3,240 support. Until then, price action may remain sideways.

WTI Crude Oil prices rose this week, reaching multi-week highs thanks to a weaker U.S. dollar and stronger stock markets, which boosted confidence in energy demand.

However, gains may be short-lived as Morgan Stanley predicts a global oil surplus, which could push prices down. OPEC+ is gradually increasing production, and non-OPEC supply is also expected to grow.

Meanwhile, tensions around the Russia-Ukraine war and lower oil storage on tankers are helping support prices.

In the U.S., oil inventories remain below average, and the number of active drilling rigs has slightly declined.

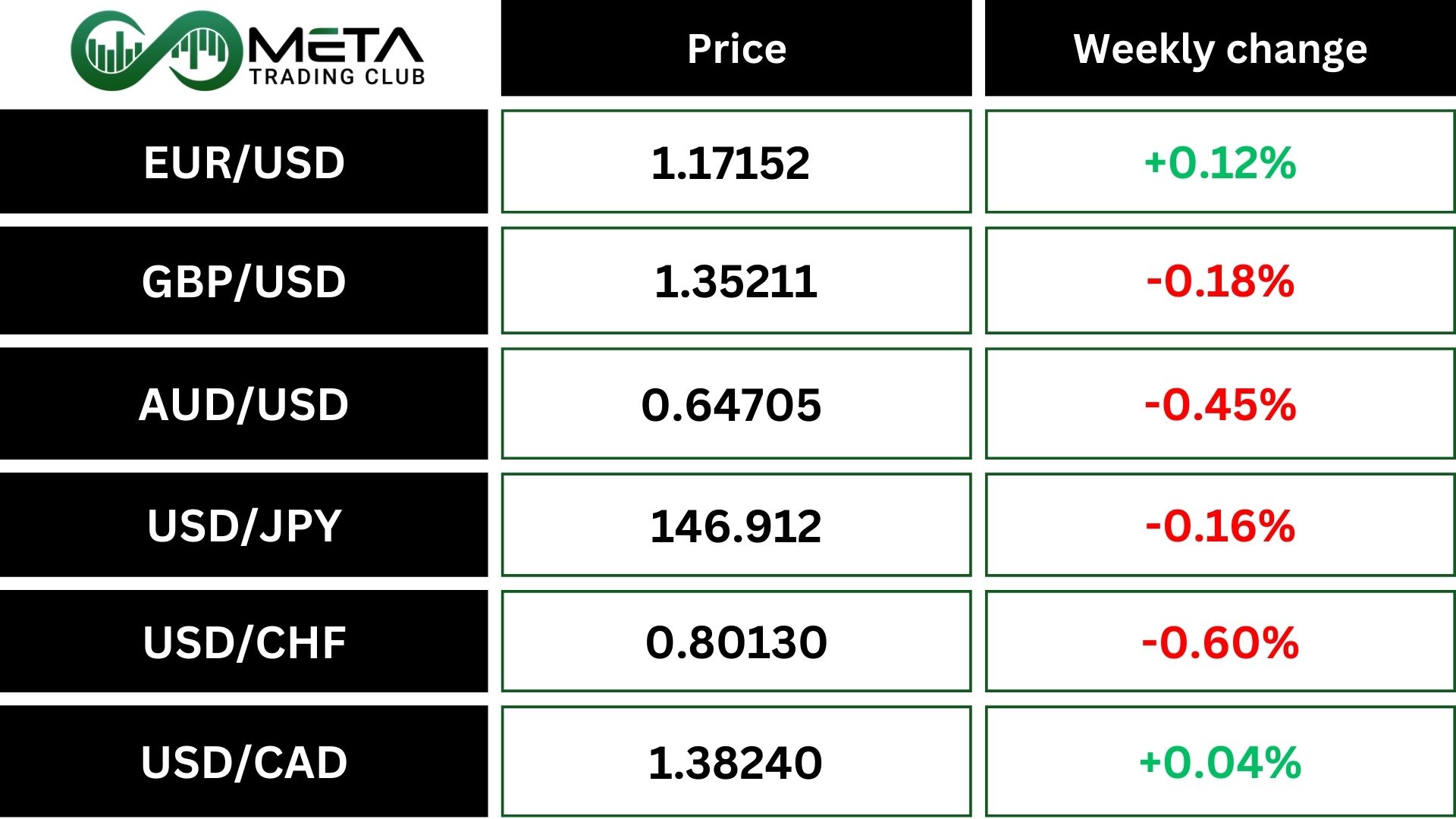

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The U.S. dollar fell after Federal Reserve Chair Jerome Powell hinted at a possible interest rate cut in September, though he didn’t confirm it.

The dollar index dropped nearly 1%, while the euro and yen gained strength against the dollar. Powell noted that the job market is slowing down, which could lead to rising risks for employment. His comments came during a major economic conference in Jackson Hole.

Crypto

The crypto market cooled after a record-breaking rally. Bitcoin’s Fear & Greed Index dropped from 70 to 53, signaling a shift from “Greed” to “Neutral.” The total market cap fell below $4 trillion, with Bitcoin sliding 2.2% to around $115,000 and Ethereum dropping 4% to just under $4,300, reflecting cautious sentiment and macro-driven profit-taking.

Ethereum surged to a record high of $4,878 on strong ETF inflows and speculative optimism ahead of the Jackson Hole Symposium, but quickly reversed course after Fed Chair Powell delivered a cautious speech, warning of persistent inflation risks. The shift in tone triggered profit-taking and $134 million in ETH liquidations, dragging the price down to around $4,236 by week’s end. Despite the pullback, ETH remained up nearly 18% for the month, reflecting underlying strength amid macro-driven volatility.

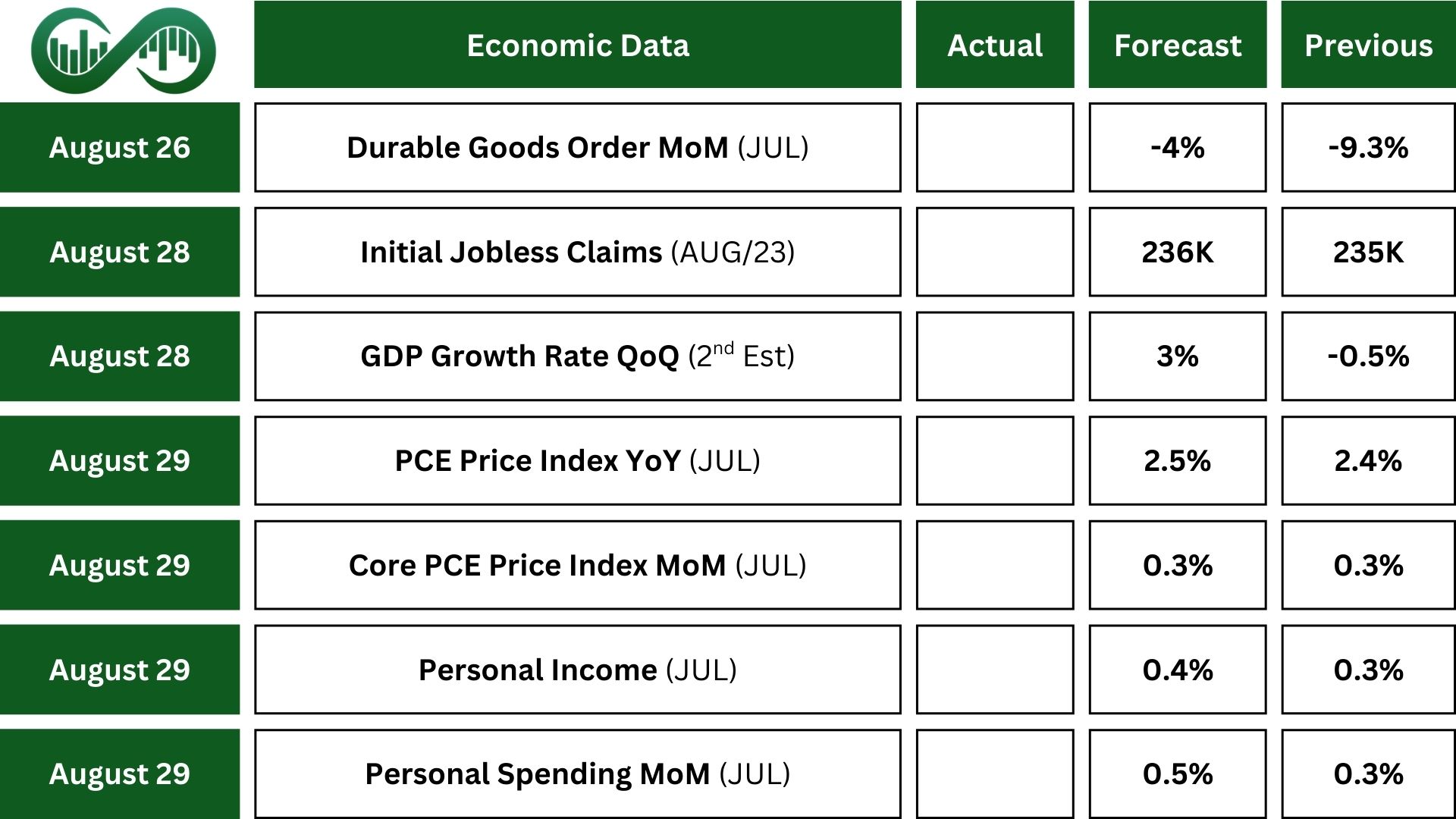

Next Week’s Outlook

Economic Events

The key economic report in the U.S. this week is the July Personal Income and Spending release. The market expects personal income to rise by 0.4%, while personal spending is forecast to grow by 0.5%.

Inflation indicators, both the headline and core Personal Consumption Expenditures (PCE) price indexes, are projected to increase by 0.3%, offering insight into consumer behavior and price trends.

Before that, the second estimate of second-quarter GDP will be released.

Also, the initial estimate showed a strong 3% annualized rebound, suggesting solid economic momentum.

Meanwhile, durable goods orders are expected to decline by 4%, though figures excluding transportation are likely to remain stable, pointing to mixed signals in manufacturing demand.

Consumer sentiment will be tracked through the Conference Board’s Consumer Confidence Index and the final reading of the University of Michigan’s Consumer Sentiment Index.

Regional economic activity will be measured by the Chicago Fed National Activity Index, the Chicago PMI, and the Dallas Fed Manufacturing Survey.

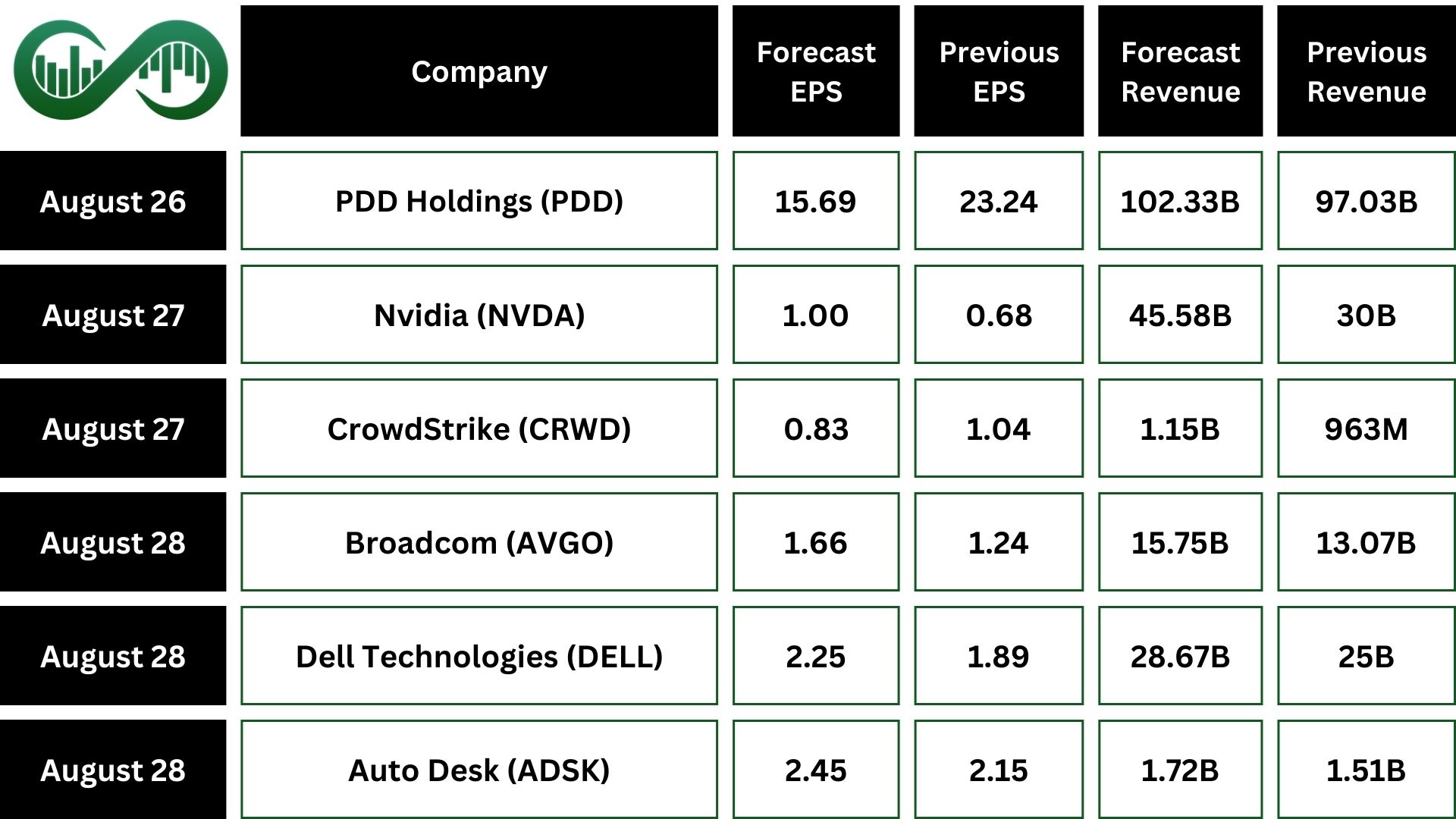

Earnings Events

In the U.S., Nvidia (NVDA) earnings report is drawing major attention as a key indicator of global interest in artificial intelligence. The chipmaker, now the world’s most valuable company after a 31% rise this year, is expected to show a 47% jump in profits. Investors are also watching for updates on chip demand, data center growth, and how U.S.-China trade restrictions are affecting business