What You Gained by Reading Last Week’s Market Mornings and What You Missed If You Didn’t!

Last Week’s report

Economic Reports

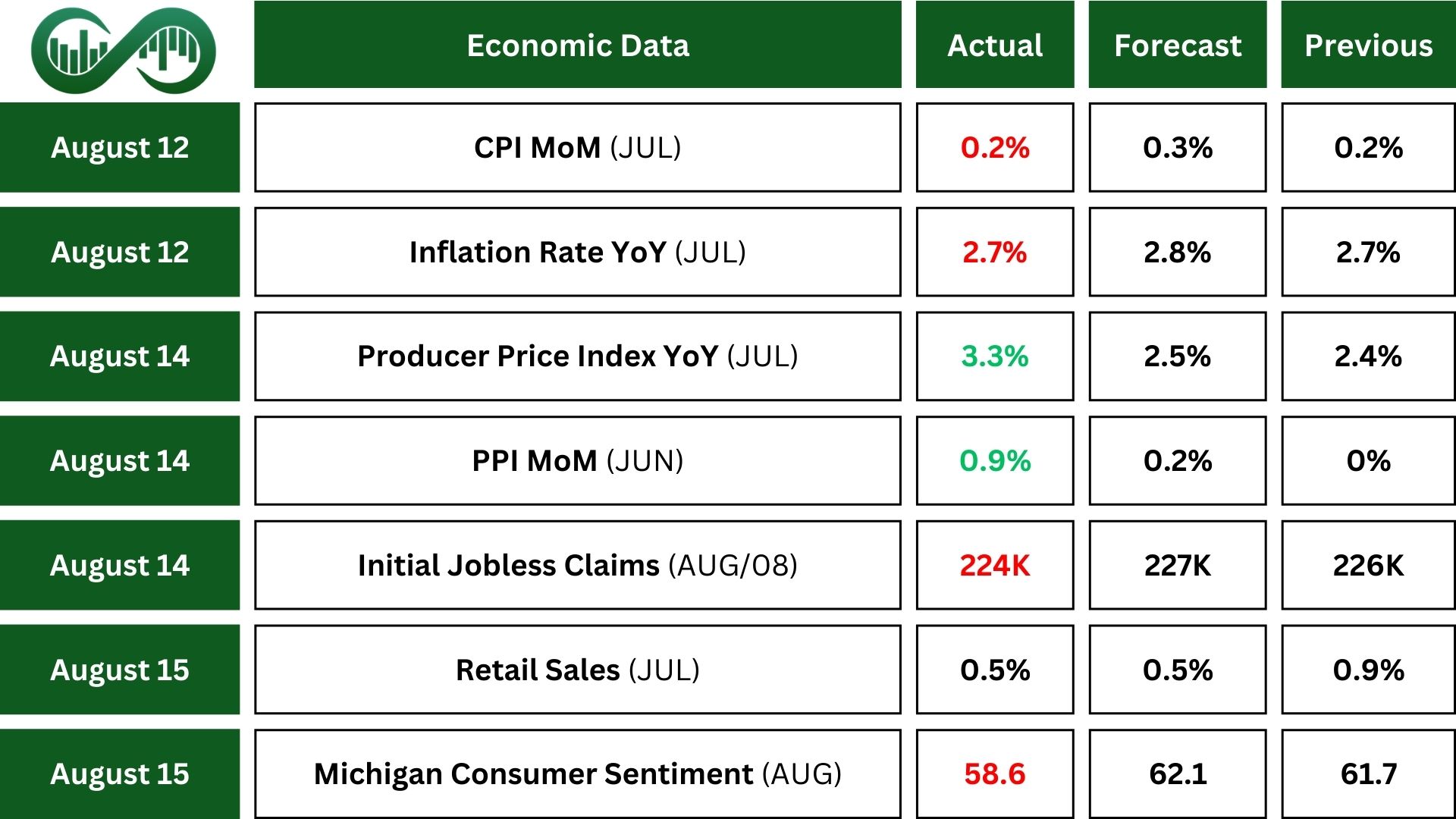

CPI

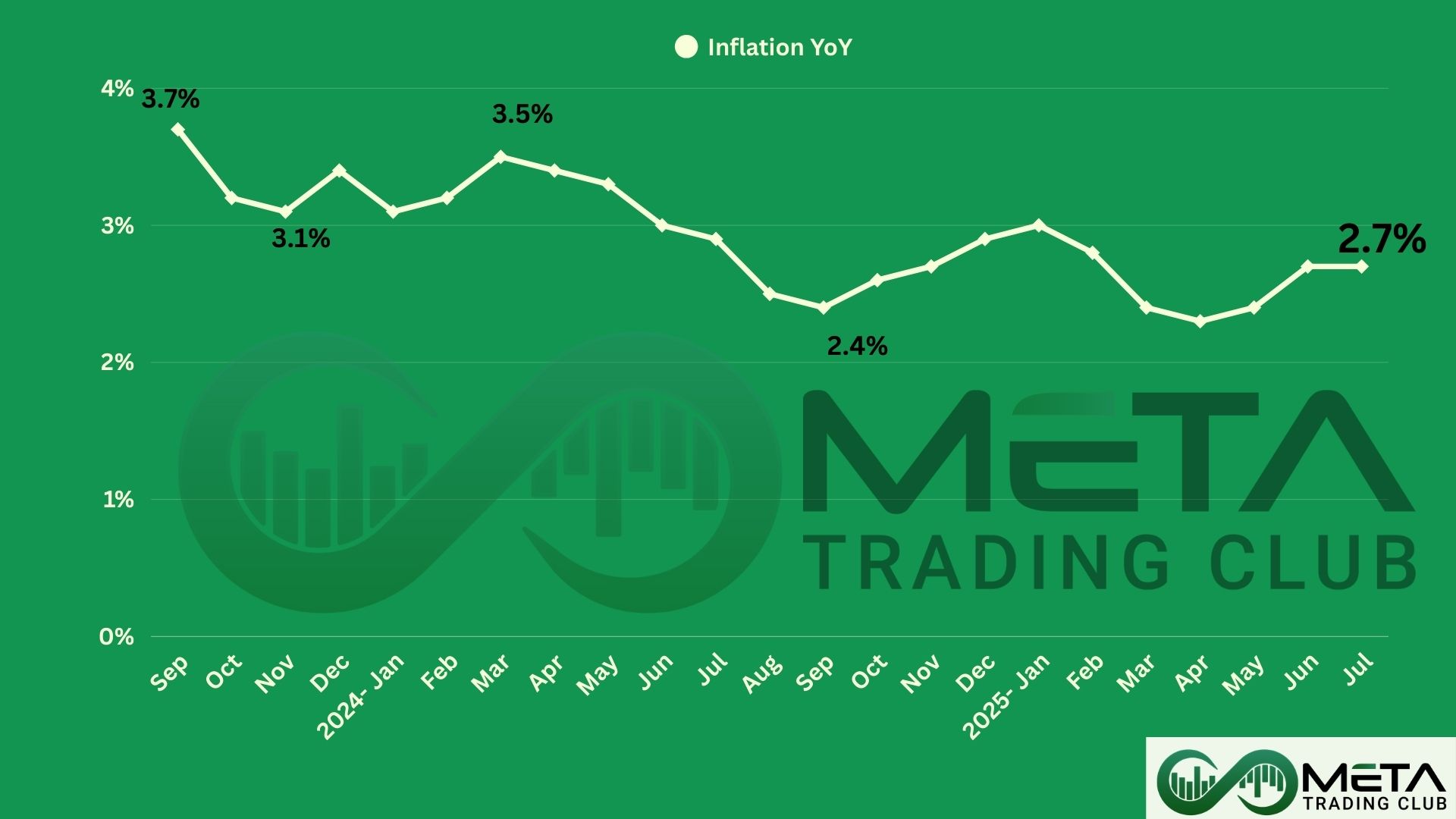

U.S. annual inflation held steady at 2.7% in July, matching June’s rate and coming in slightly below the expected 2.8%. On a monthly basis, the Consumer Price Index (CPI) rose 0.2%, just below June’s 0.3% increase and in line with expectations.

Core inflation, which excludes food and energy, rose to a five-month high of 3.1%, up from 2.9% in June and above forecasts. The monthly core CPI increased by 0.3%, its largest gain in six months.

This signals mixed implications for the stock market. While headline inflation remains stable, the rise in core inflation may pressure the Federal Reserve to stay cautious on rate cuts.

Job Report

Initial jobless claims in the U.S. fell 224,000, defying expectations of a rise to 228,000. Continued claims also declined to 1,953,000, below forecasts, though they remain elevated compared to historical norms.

Notably, federal employee claims dropped to 637 following layoffs at the Department of Government Efficiency (DOGE), easing from a four-month high.

This signals a labor market that is cooling but still resilient, which may temper expectations for aggressive Fed rate cuts.

PPI

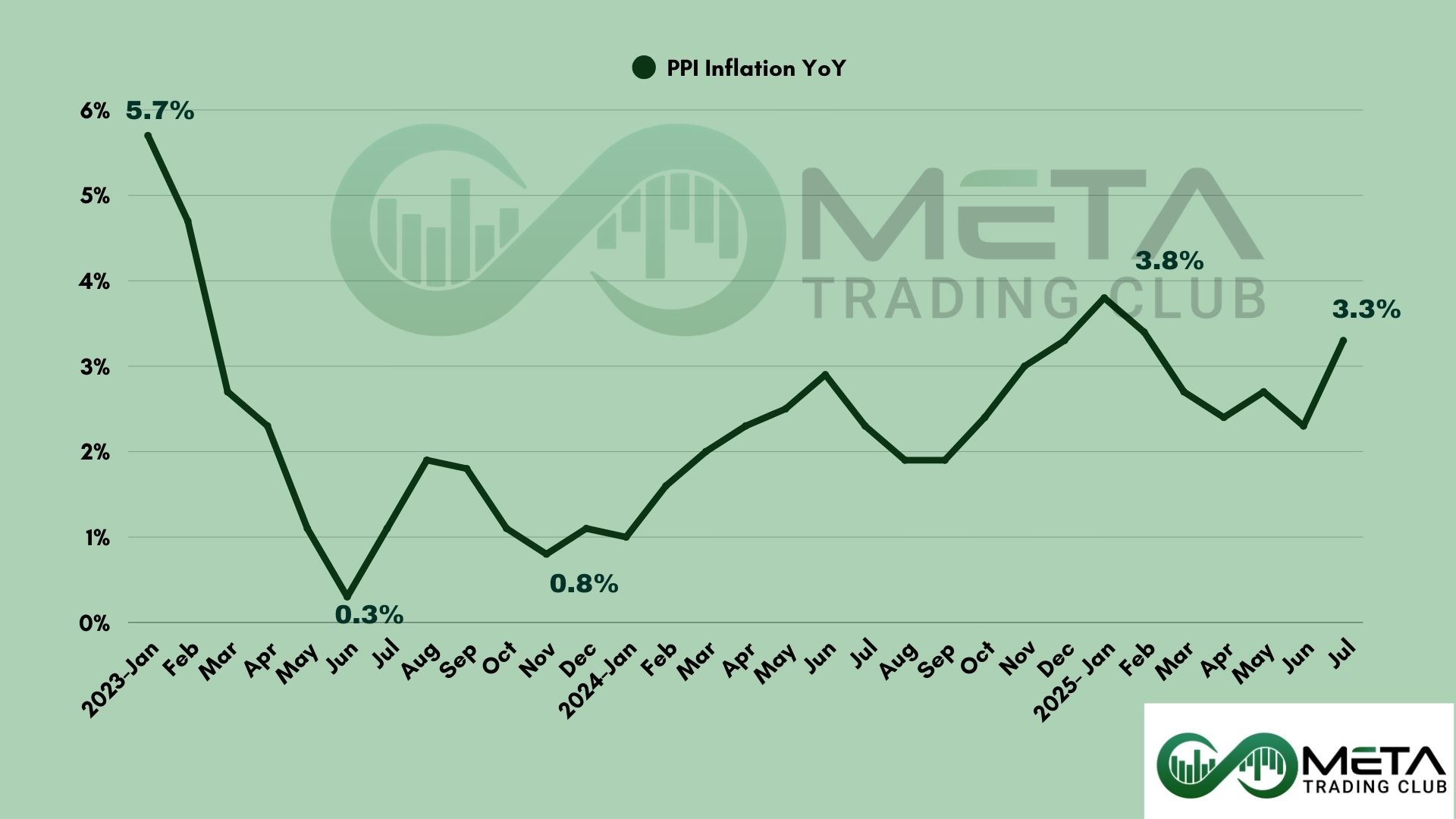

U.S. producer prices surged 0.9% month-over-month in July, the largest gain since June 2022 and far above expectations of 0.2%. Service costs rose 1.1%, Goods prices climbed 0.7%, while gasoline fell 1.8%.

Core PPI also jumped 0.9%, beating forecasts, and annual headline and core producer inflation accelerated to 3.3% and 3.7%, respectively.

This signals rising input cost pressures that could squeeze corporate profit and weigh on equity valuations, especially in rate-sensitive and consumer-facing sectors. So, this report has negative impacts on the market.

Retail Sales

U.S. retail sales rose 0.5% in July, in line with expectations and following a strong upward revision for June (0.9%). Core retail sales, which feed into GDP, also rose 0.5%, beating expectations of 0.4%.

This signals continued consumer strength, which supports corporate revenues and is broadly positive for the stock market.

Consumer Sentiment

U.S. consumer sentiment declined in August, with the University of Michigan index falling to 58.6 from 61.7 in July, missing market expectations of 62. This marks the first drop in four months, driven largely by rising inflation concerns and worsening conditions for purchasing durable goods.

Although inflation expectations also rose, with the one-year outlook climbing to 4.9% and the five-year forecast increasing to 3.9%. These shifts reversed recent declines in inflation expectations, though they remain below the peaks seen earlier in the year.

This signals potential caution for the stock market, as weakening consumer sentiment and rising inflation expectations may dampen consumer spending and increase economic uncertainty.

Earnings Reports

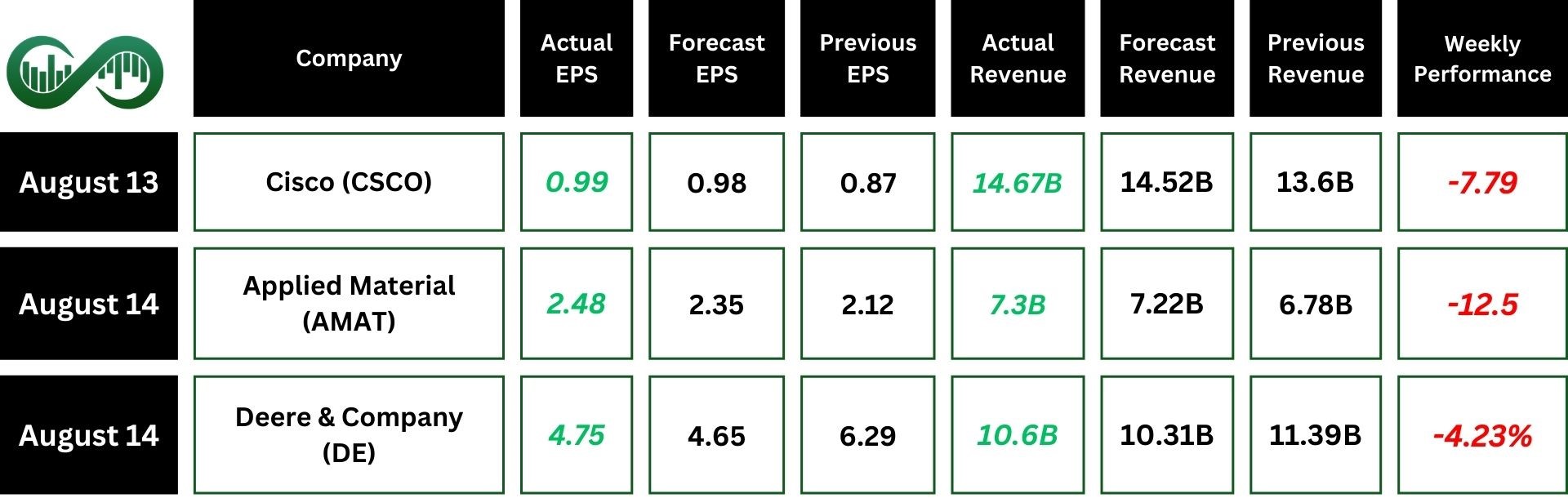

Cisco Systems

Cisco Systems (CSCO) reported a strong close to the fiscal year, with revenue rising 8% year over year to $14.7 billion, surpassing analyst expectations.

Product orders grew 7%, and AI infrastructure orders from webscale customers exceeded $800 million for the quarter. This pushed the full-year total past $2 billion orders which is more than double the company’s original target.

Profitability was solid, with non-GAAP EPS of $0.99, at the high end of guidance. Operating income rose significantly, and cash flow from operations increased 14% to $4.2 billion.

The company’s outlook for Q1 and FY 2026 suggests continued growth, driven by strategic investments in AI and innovation.

Technically, CSCO has approached strong support at $66. A breakdown with confirmation could lead to a move toward lower support levels. However, a rebound from this zone may trigger a potential upside.

Applied Materials

Applied Materials (AMAT) posted adjusted earnings of $2.48 per share for the third quarter, beating expectations.

Revenue came in slightly above forecasts at $7.3 billion, compared to the expected $7.21 billion.

However, its guidance for the fourth quarter disappointed investors.

AMAT stock plunged 12% after the company issued a weaker-than-expected fourth-quarter outlook. Despite beating earnings and revenue estimates, concerns over slowing demand (particularly in China) and broader tariff-related risks weighed heavily on investor sentiment.

Indices

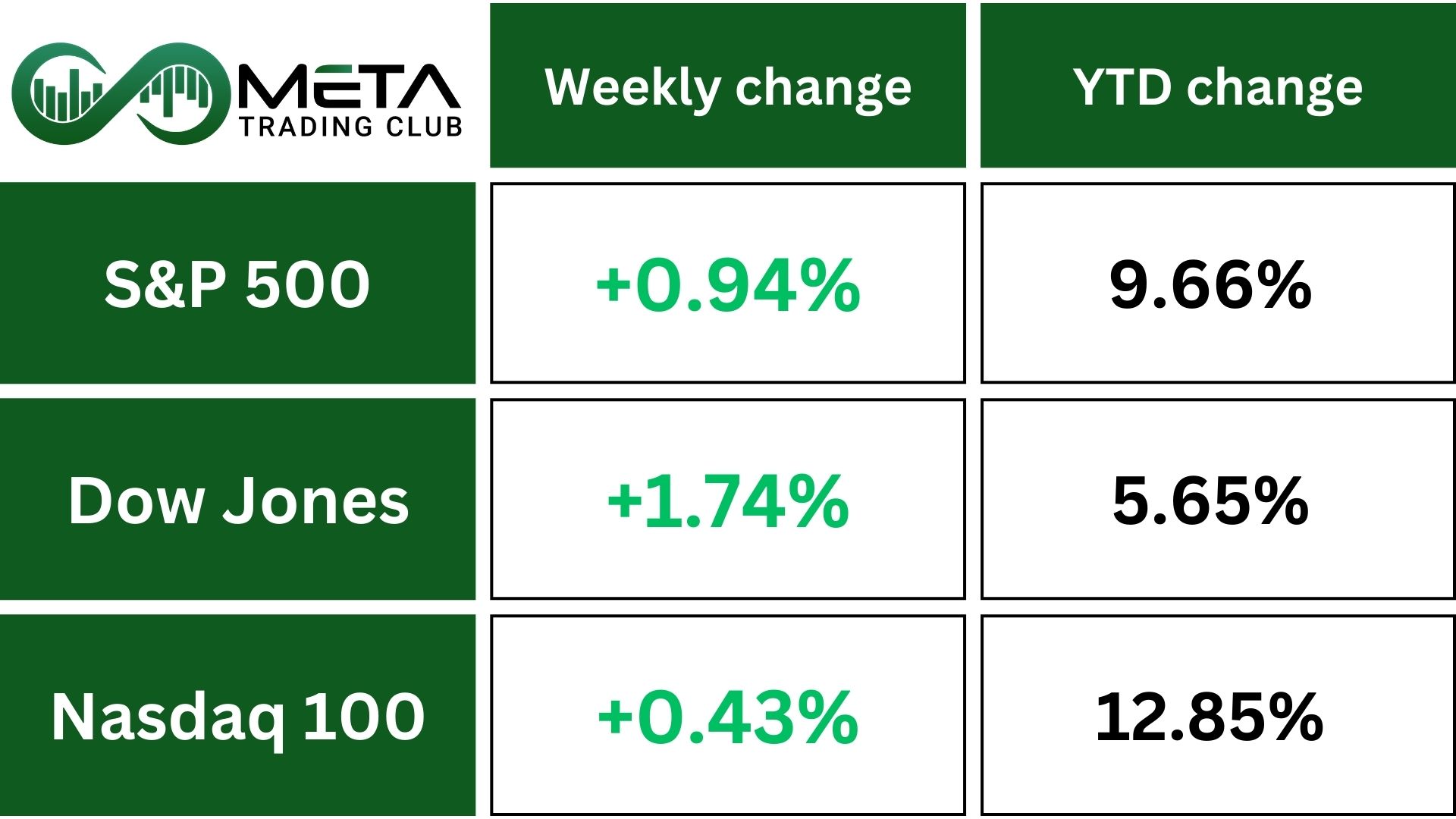

Indices’ Weekly Performance:

S&P 500 (SPX) rose for the second week in a row, gaining 0.9% as investors considered possible Federal Reserve rate cuts and global political developments.

The Dow (DJI) increased by 1.7%, while the Nasdaq (NDX) edged up 0.4%.

Throughout the week, the S&P 500 and Nasdaq continued to reach new highs. On Friday, the Dow tried to join them, hitting a new intraday record, but falling short of a record close.

This week, all eyes turn to Jackson Hole, Wyoming, where the Federal Reserve’s annual Economic Policy Symposium kicks off August 21–23. With the theme “Labor Markets in Transition,” the 2025 gathering comes at a critical moment: inflation remains stubbornly above target, labor market data shows signs of cooling, and investors are betting on a September rate cut.

Fed Chair Jerome Powell’s Friday speech is expected to be a pivotal moment, potentially reshaping expectations for monetary policy amid mounting pressure from the Trump administration and volatile global markets.

Technically, SPX is approaching the 6500 Fibonacci resistance zone amid weakening momentum; caution is warranted for active positions.

Stocks

Most sectors went up this week. Healthcare led the way, while Consumer Staples and Utilities fell the most.

- Healthcare jumped 4.9%, helped by UnitedHealth rising after Warren Buffett made a big investment in the company.

- Consumer Discretionary rose 2.6%. Amazon gained as it expanded same-day grocery delivery to include fresh foods.

- Communication Services climbed 2.1% and hit a record close. Paramount Skydance shares soared 31% after winning exclusive U.S. broadcast rights to UFC in a $7.7 billion deal. TKO Group, which owns UFC, rose 16%.

- Industrials stayed flat. Deere declined after reporting lower profits and warning about bigger tariff impacts.

- Technology slipped 0.1%. Applied Materials dropped after a weak revenue forecast due to low demand from China and tariff issues. Nvidia and AMD fell after agreeing to pay the U.S. government 15% of revenue from advanced chip sales to China. But Intel surged 23% after its CEO met with President Trump and reports suggested the government might invest in the company. The semiconductor index rose over 1%.

- Consumer Staples dropped 0.9%. Walmart and Kroger fell after Amazon’s move into fresh food delivery.

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- Paramount Skydance (PSKY): Surged 30% after securing exclusive UFC broadcast rights.

- Intel (INTC): Jumped 23% after the CEO met with President Trump and reports of potential government investment.

- UnitedHealth (UNH): Gained 21% following Warren Buffett’s major investment in the company.

- TKO Group (TKO): Rose 16% due to the $7.7 billion UFC broadcast deal with Paramount Skydance.

- United Airlines (UAL): Climbed 13% amid strong summer travel demand and upgraded earnings outlook.

- Delta Air Lines (DAL): Increased 12% on robust passenger volumes and favorable fuel cost trends.

- Eli Lilly (LLY): Advanced 12% after positive trial results for its new obesity drug.

- Centene (CNC): Up 11% on strong quarterly earnings and improved Medicaid enrollment figures.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold (XAU/USD) prices fell last week, as stronger-than-expected U.S. economic data dampened hopes for a significant interest rate cut by the Federal Reserve.

U.S. producer prices in July rose at their fastest pace in three years, indicating that companies are passing higher import costs from tariffs onto consumers.

As a result, traders now anticipate a modest 25-basis-point rate cut next month, followed by another in October, aligning with Fed official Mary Daly’s comments against a larger cut in September.

On the geopolitical front, the summit between Donald Trump and Vladimir Putin didn’t lead to a major breakthrough in resolving the war in Ukraine.

Technically, Gold has been consolidating in a range between $3,240 and $3,440 for some time. It bounced off its 100-day moving average, showing renewed buying interest. For the next clear trend to emerge, gold needs to either break above $3,440 resistance or below $3,240 support. Until then, price action may remain sideways.

WTI Crude Oil down about 1% for the week. Oil prices dropped as traders watched U.S.–Russia talks for signs of a Ukraine ceasefire, which could boost Russian output. But any easing of sanctions would need Congress, so quick changes are unlikely.

Weak economic data from China also weighed on prices, with slower factory and retail growth despite higher refinery activity. Rising Chinese fuel exports hint at weaker local demand.

More supply from OPEC+ and possible U.S. rate hikes added to the pressure. Overall, forecasts suggest an oil surplus through mid-2026, keeping prices under pressure.

Forex

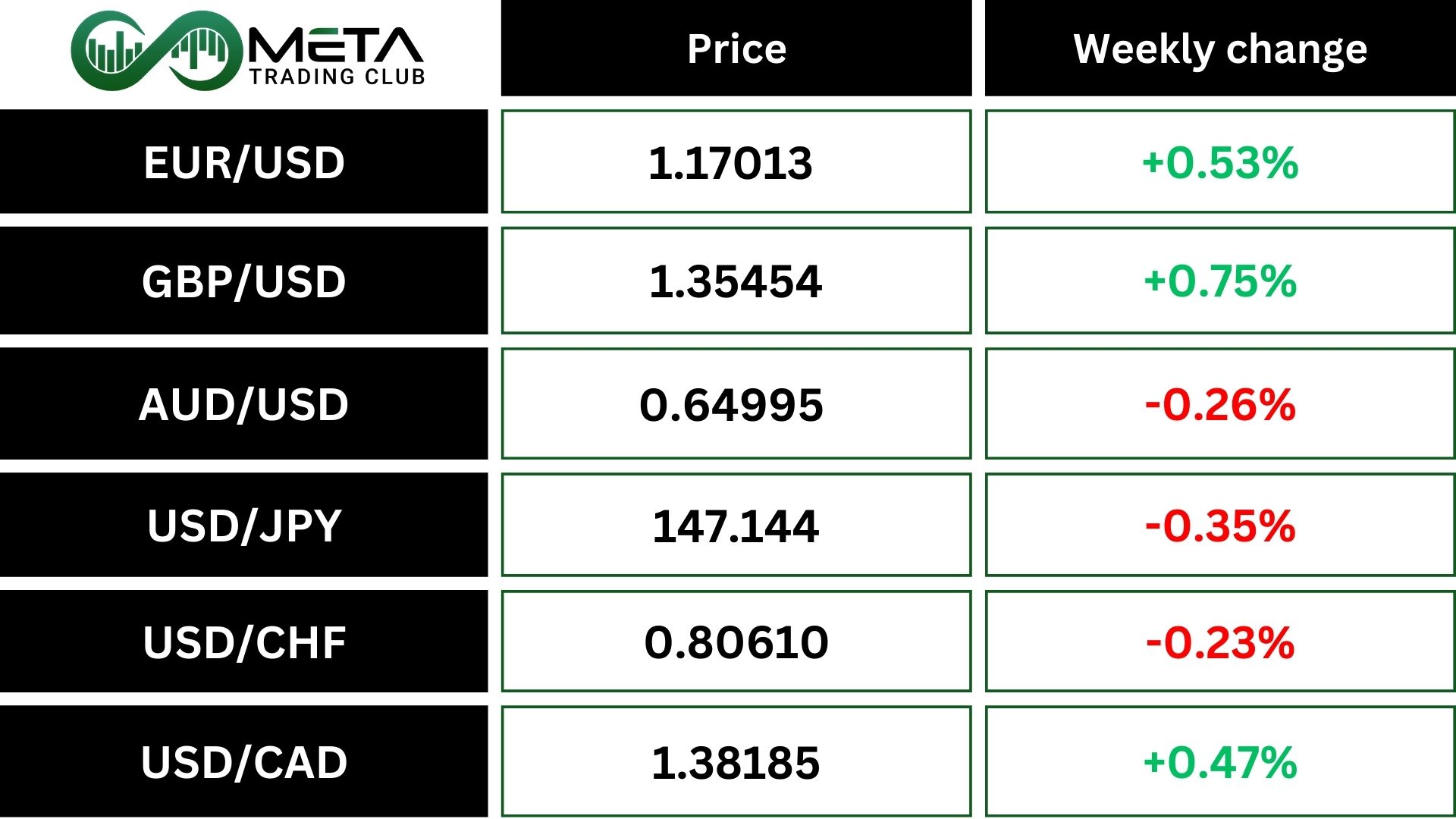

Weekly Performance of Major Foreign Exchange Pairs:

The U.S. dollar, which surged on Thursday after stronger-than-expected producer price data, gave back most of those gains on Friday and was on track to end the week down 0.4% against a basket of major currencies (DXY).

PPI data was surprising, there’s still little solid evidence of inflation being driven by tariffs. With markets still expecting a Fed rate cut in September, currently priced in at 93%, and attention shifting to Alaska, the dollar is losing ground.

The euro gained 0.5%, supported by hopes for a ceasefire in Ukraine.

The dollar also fell 0.4% against the yen, after strong Japanese growth data showed exports holding up despite new U.S. tariffs. Comments from U.S. Treasury Secretary Scott Bessent suggesting the Bank of Japan may be slow to respond to inflation added further support to the yen.

The British pound rose 0.2%, boosted by positive economic data and a hawkish rate cut from the Bank of England, bringing its weekly gain to 0.7%

Crypto

Bitcoin recently hit a new all-time high above $124K but has since pulled back after two bearish daily candles. It’s now retesting a key support zone, and investors are watching closely for signs of a reversal.

Technically, BTC price is approaching its long-term ascending line, which could lead to a downside breakout. If that happens, the $110K level, supported by the 100-day moving average, may act as a strong cushion. However, if the uptrend holds, bullish momentum could resume, potentially pushing Bitcoin toward $130K and beyond.

Next Week’s Outlook

Economic Events

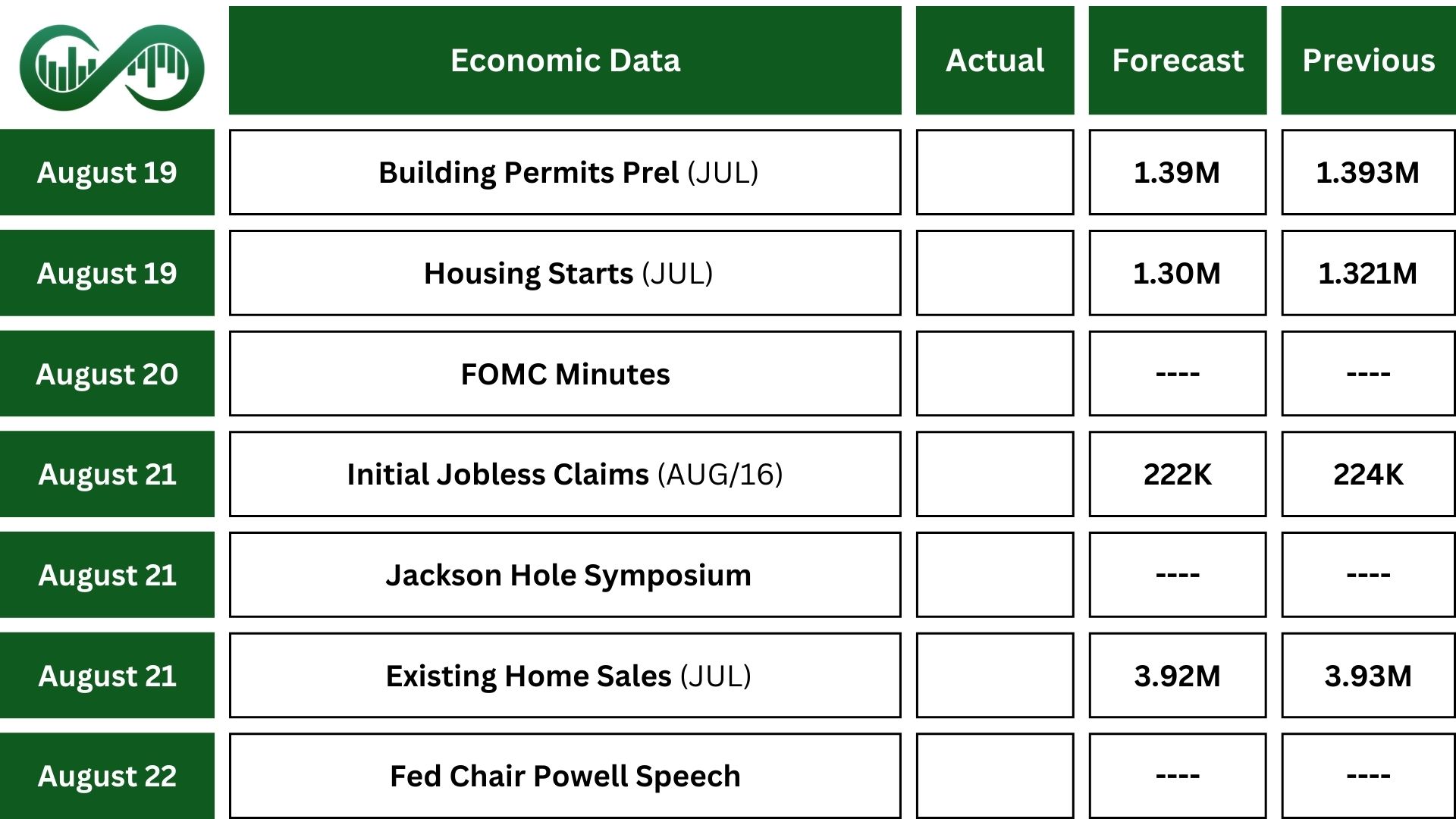

The focus in the U.S. this week will be on monetary policy. The Federal Reserve is set to release minutes from its last meeting, where interest rates stayed the same but two members disagreed.

This comes ahead of the Jackson Hole Economic Policy Symposium, where Fed Chair Jerome Powell will speak. His remarks will be closely watched due to economic uncertainty, global tensions, and pressure from the White House to cut rates.

Speeches from Fed officials Waller and Bowman (who opposed the last decision and may be considered for the top job) could also offer clues.

On the data side, housing reports will lead the week, starting with the NAHB Housing Market Index, followed by building permits, housing starts, and existing home sales, which are expected to stay steady.

Markets will also look at the S&P flash PMIs for August after strong results last month, along with the Philadelphia Fed Manufacturing Index.

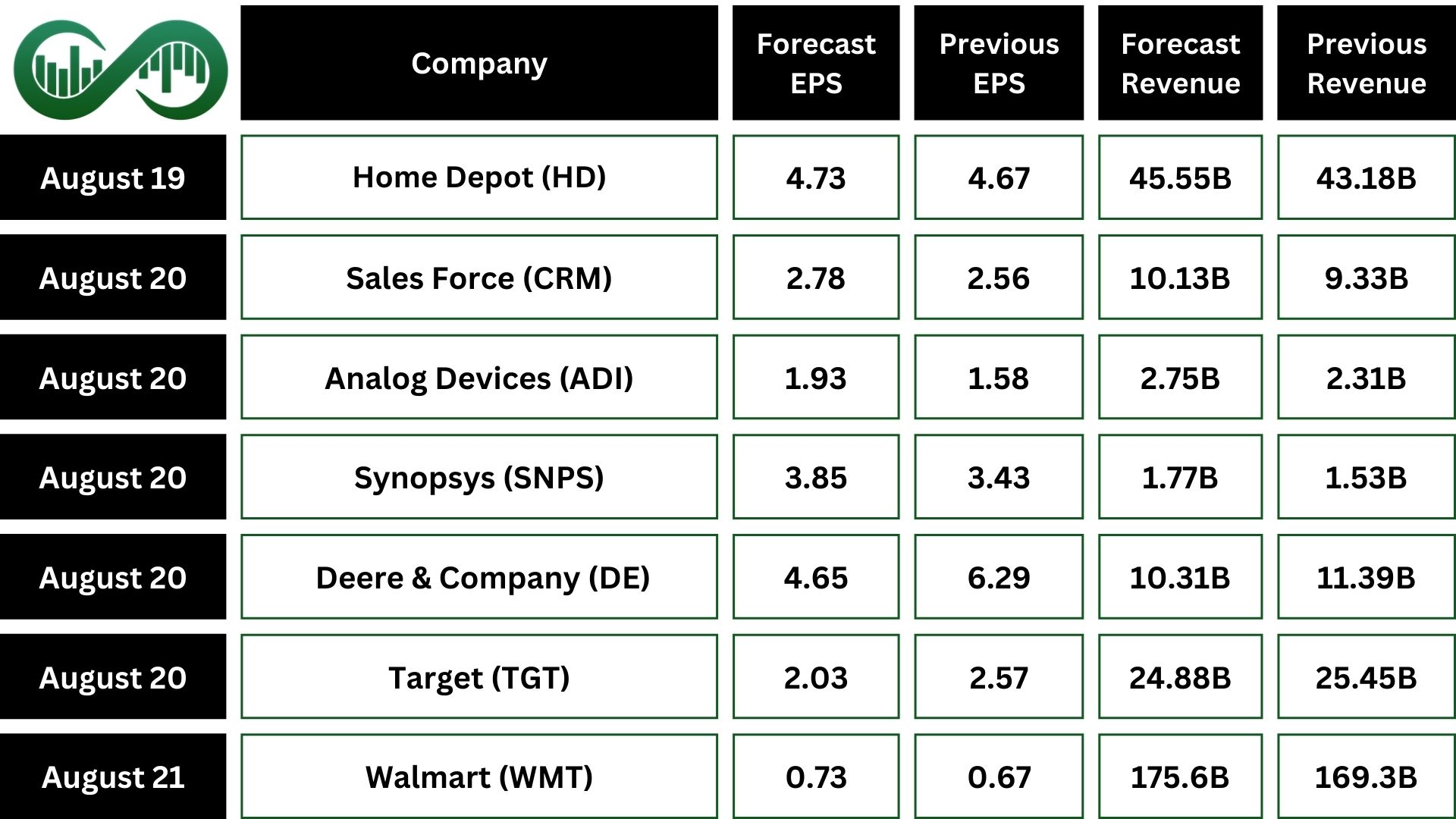

Earnings Events

This week’s earnings reports will include big U.S. retailers like Walmart (WMT), Target (TGT), Home Depot (HD), Lowe’s (LOW), and TJX Companies (TJX).

On the tech side, Salesforce (CRM) and Analog Devices (ADI) are also set to report.