Last Week’s report

Economic Reports

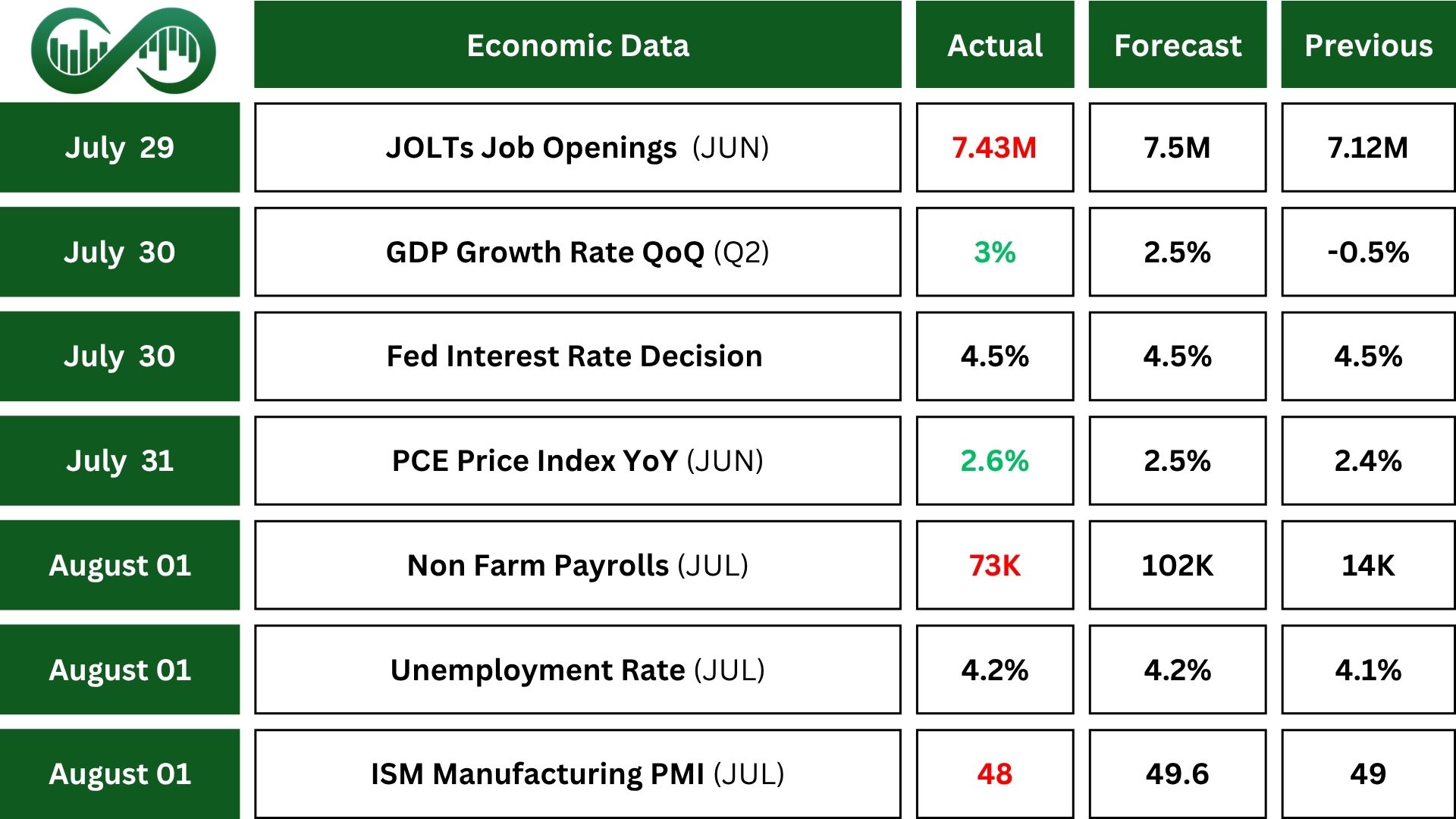

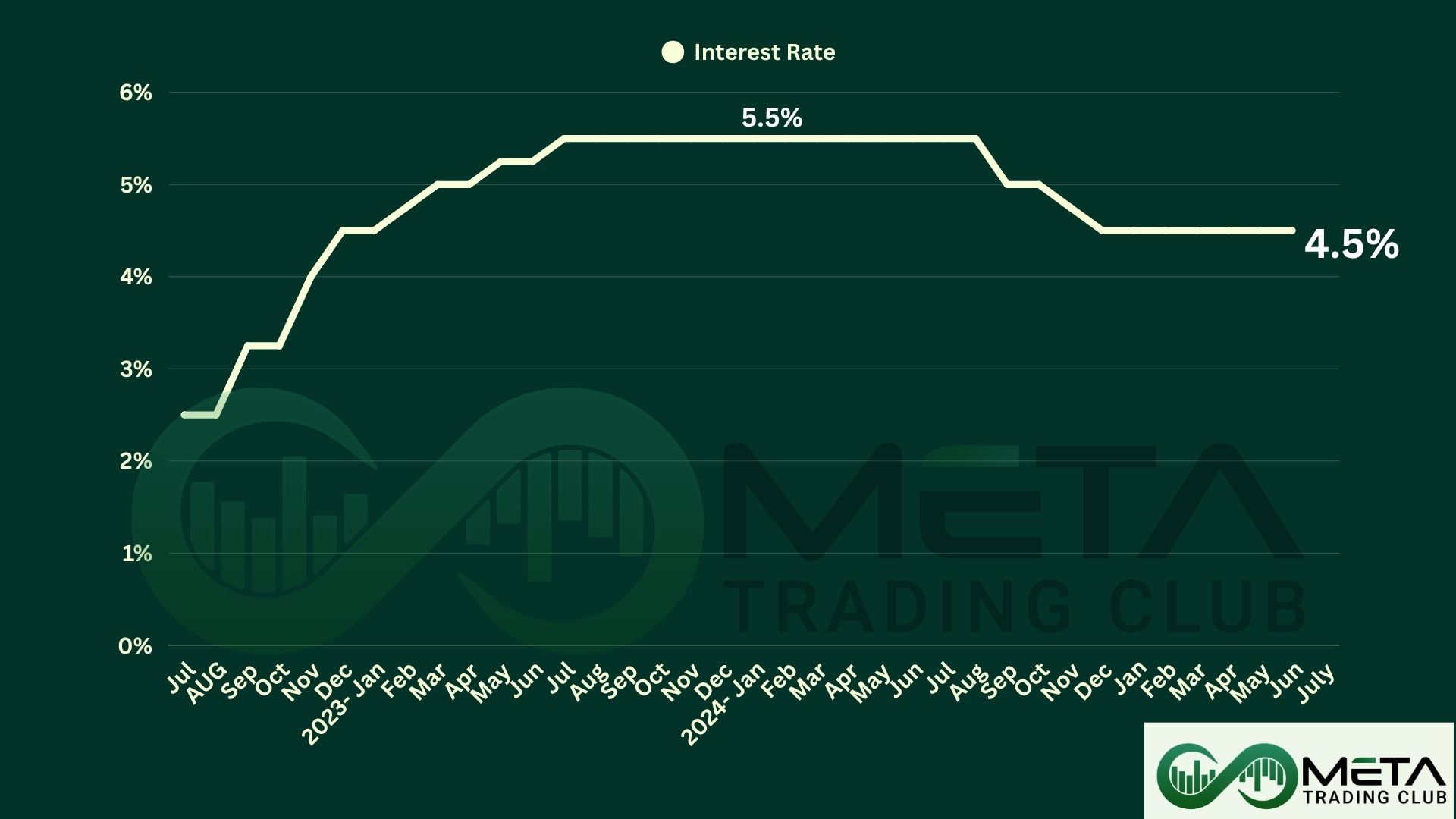

In July, the Federal Reserve held interest rates steady at 4.25%–4.50% for the fifth straight meeting, sticking to a cautious stance amid rising inflation and trade war uncertainties. Despite political pressure from President Trump to slash rates to 1%, the Fed maintained its position, prompting investors to anticipate a possible rate cut in September.

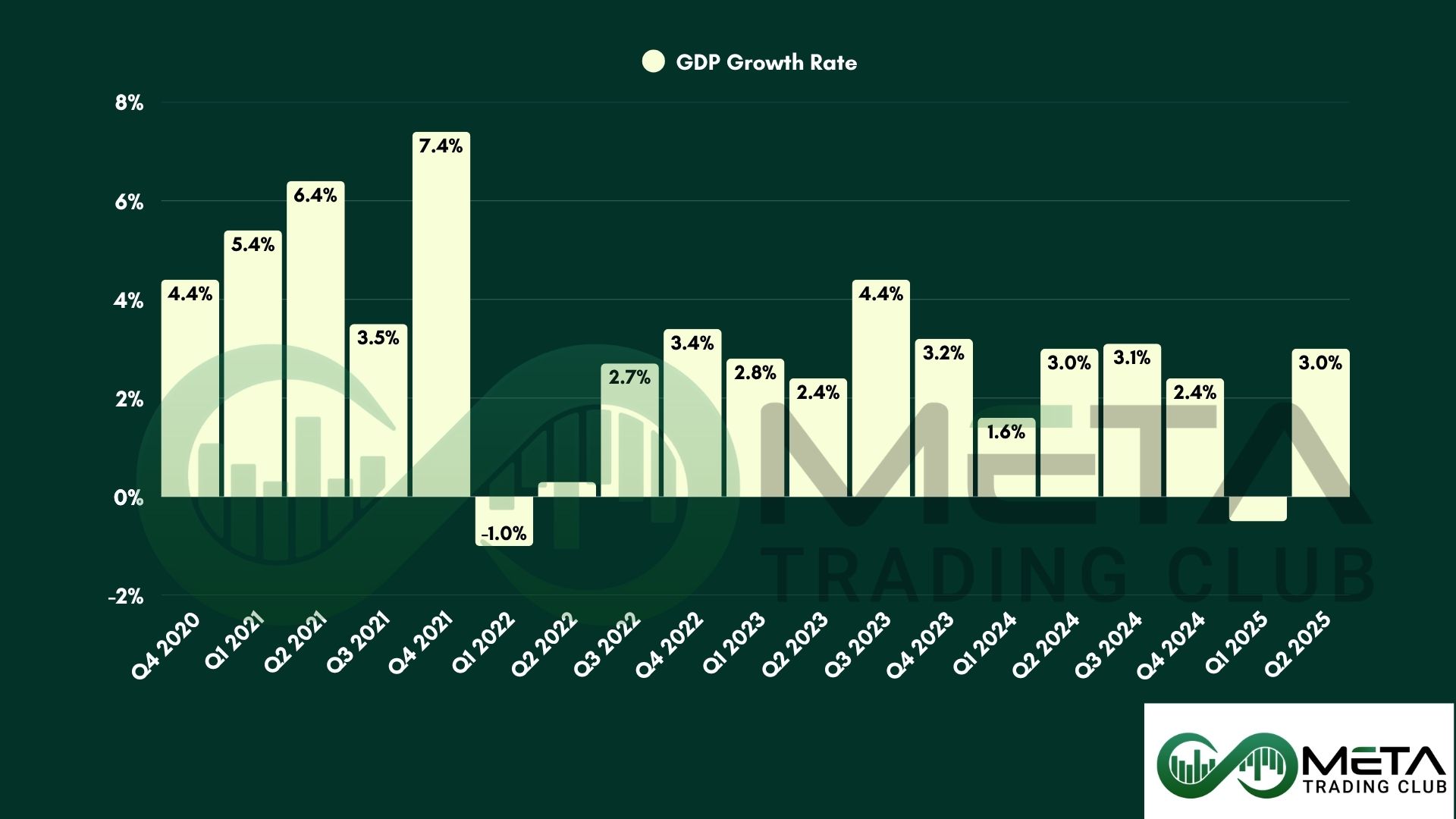

In Q2 2025, the US economy grew at an annualized rate of 3%, rebounding from a contraction in the previous quarter and surpassing expectations. This growth was largely driven by a sharp drop in imports, which boosted the GDP, along with modest increases in consumer and government spending. However, business investment and exports weakened, and inventory reductions dragged on growth.

The GDP figure looks strong, but underlying demand remains soft, suggesting the recovery is more statistical than structural, and economic momentum may be fragile going forward.

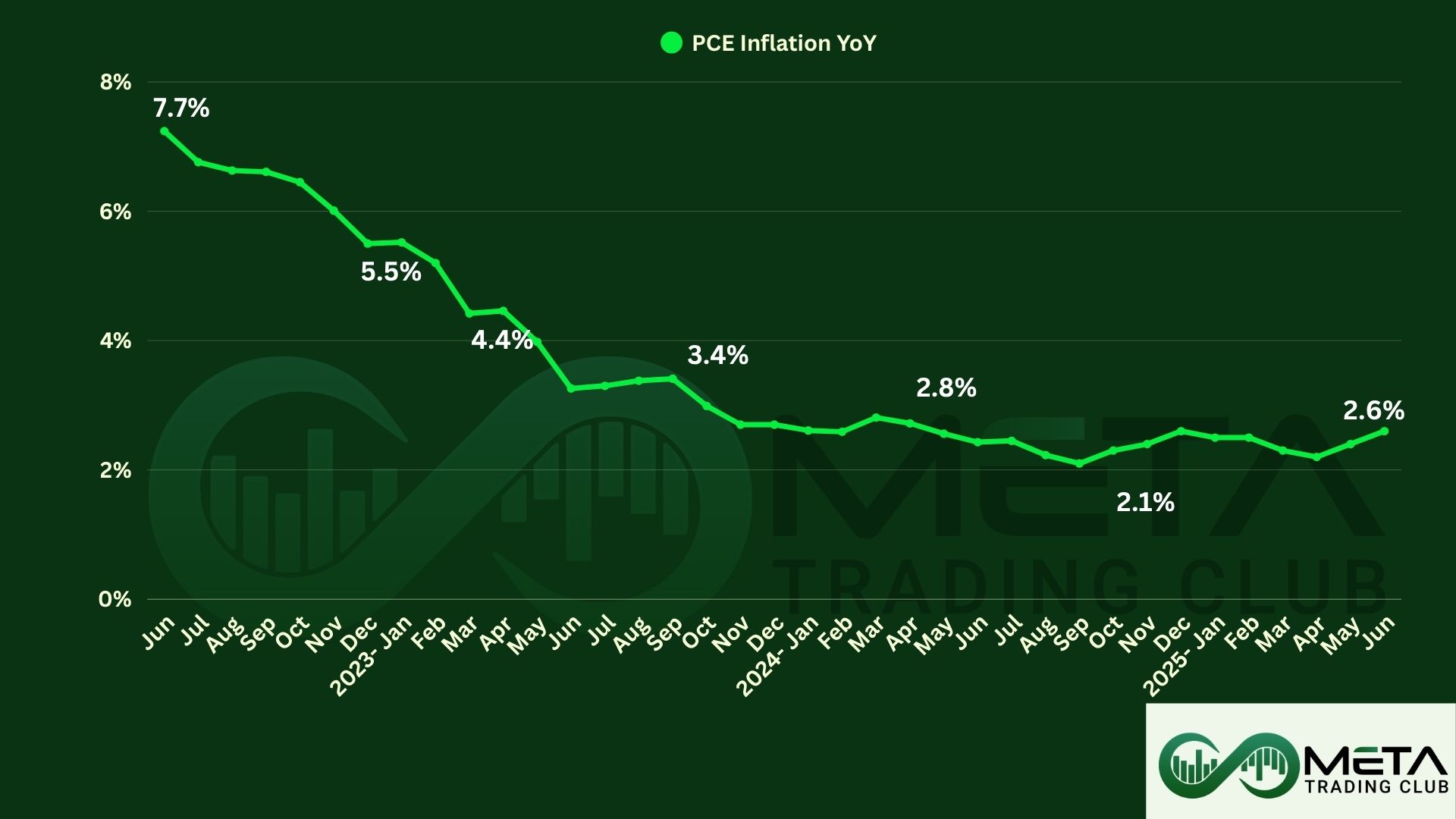

The US PCE price index climbed 0.3% in June, its strongest monthly rise in four months. Annual PCE inflation rose to 2.6%, continuing its climb. However, Core PCE inflation held steady at 2.8%, with May revised upward.

This increase and steady core inflation above target means the Fed’s job is far from done.

The US manufacturing sector shrank for the fifth straight month in July, with the ISM PMI index falling to 48, signaling continued weakness. Supplier deliveries and employment declined further, as companies focused on managing staff rather than hiring. While production picked up slightly and order declines eased, overall momentum remains sluggish.

Michigan Consumer Sentiment in the US hit a five-month high in July, rising to 61.7. People felt better about current conditions, especially investors, while expectations for the future dipped slightly. Inflation worries continued to ease, which likely helped boost overall mood. However, general confidence is still lower than ideal.

Job report

In June, US job openings fell by 275,000 to 7.437 million, missing forecasts. Declines were most notable in accommodation and food services, healthcare, and finance, while gains appeared in retail, information, and education. Despite fewer openings, hiring and separations remained stable, with quits and layoffs holding steady.

This signals a cooling in labor demand but not a collapse, suggesting that employers may be growing cautious without yet reducing staff aggressively.

In July, US private businesses added 104,000 jobs, marking the strongest monthly gain since March and beating expectations. Most of the growth came from service industries like leisure, hospitality, and finance, while education and health services saw notable job losses. Goods-producing sectors also contributed, with solid hiring in construction and manufacturing. Pay growth held steady, with job-stayers earning 4.4% more and job-changers seeing a 7% increase year-over-year.

In July, US companies announced over 62,000 job cuts, a sharp rise from both the previous month and the same time last year. The increase was driven mainly by federal budget reductions from DOGE, along with layoffs linked to artificial intelligence and tariff concerns. So far this year, total job cuts have already surpassed all of 2024, with government, tech, and retail sectors hit hardest.

This signals that the labor market is under growing pressure from policy shifts and automation, raising concerns about economic stability.

US initial jobless claims rose slightly to 218,000 in late July but stayed near a three-month low, beating expectations. Ongoing claims were steady, and filings by federal workers dipped, despite recent government job cuts.

These suggest the job market remains fairly stable, showing resilience despite signs of a cooling trend.

The US added just 73,000 new non-farm payrolls in July, far below the expectations. While previous months were revised sharply downward, revealing a much weaker labor market than initially thought.

On the plus side, the unemployment rate remained steady at 4.2% and wages rose 0.3%, matching forecasts, and wage growth reached its strongest in four months.

Those shows the labor market is losing momentum, but wage growth shows some resilience.

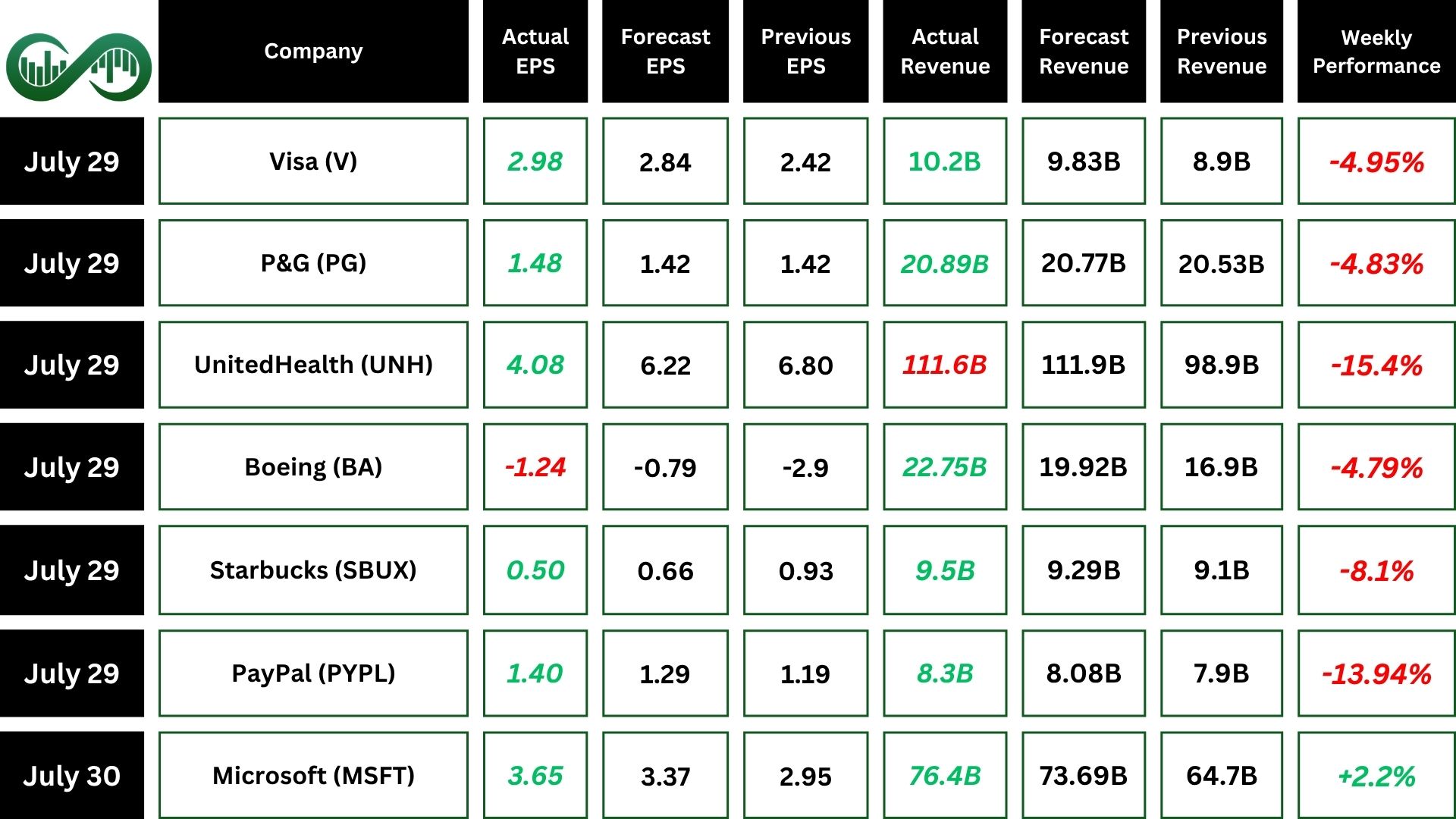

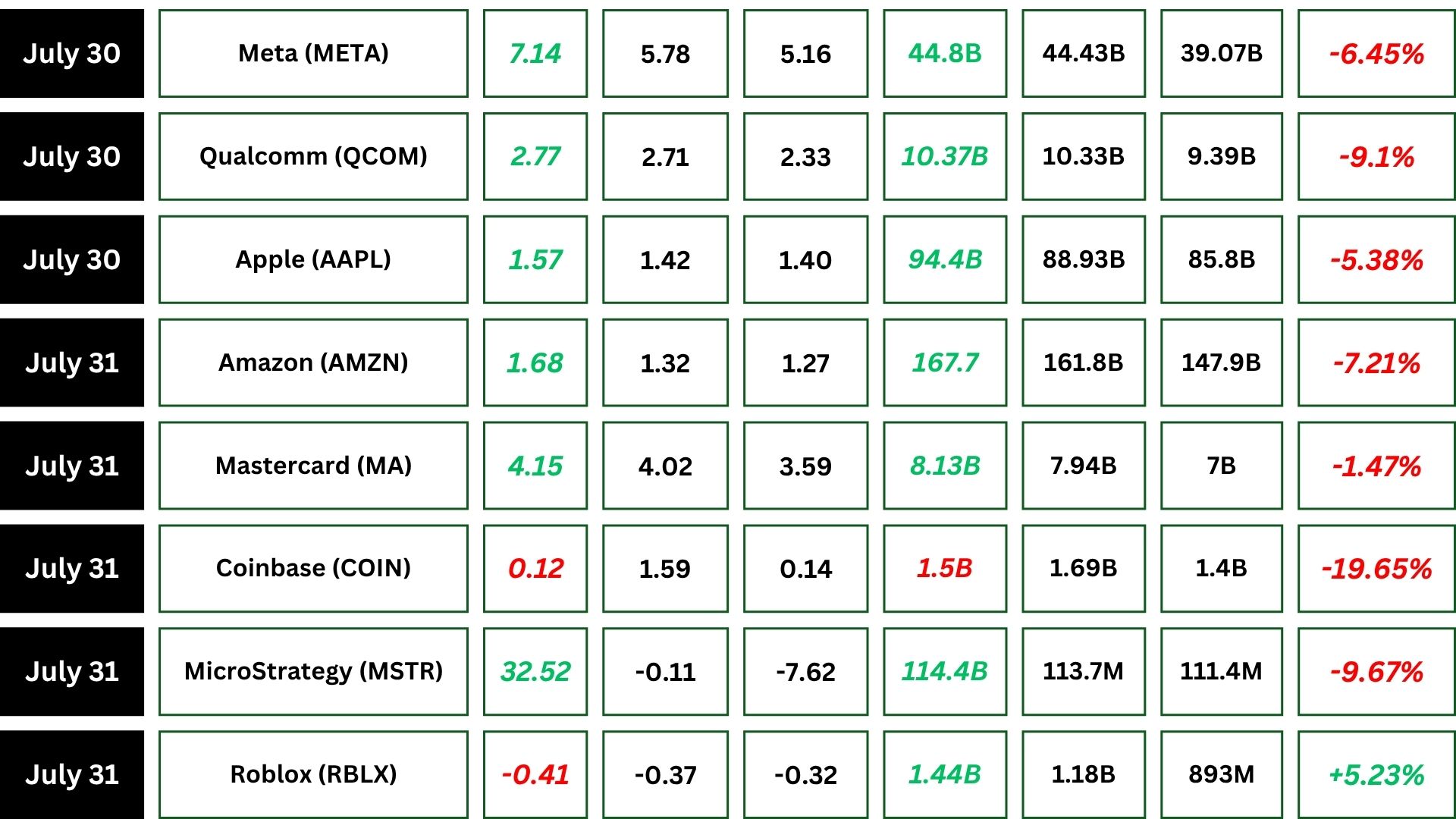

Earnings Reports

Amazon

Amazon (AMZN) posted strong Q2 results with net sales jumping 13% to $167.7 billion and operating income climbing to $19.2 billion, led by AWS profitability.

However, a cautious AWS income forecast below market expectations triggered a stock dip, as investors worried about Amazon’s pace versus rivals like Microsoft and Google.

Looking ahead, Q3 projections remain optimistic amid global economic uncertainty.

Technically, AMZN has Fibonacci and static support at $208. If it holds, a rebound is possible with confirmation but if it breaks, price may drop to the next support level.

Apple

Apple (AAPL) posted strong Q3 results with revenue up 10% to $94 billion and EPS rising 12% to $1.57, both topping estimates.

A 13.5% surge in iPhone sales, driven by U.S. buyers anticipating tariff hikes, fueled growth. Despite the $800 million tariff impact, set to rise to $1.1 billion, Apple’s demand in Greater China softened the blow.

Strategic production shifts to India and Vietnam are helping reduce long-term trade exposure.

Apple remains optimistic for mid to high single-digit growth next quarter amid trade uncertainties.

Technically, AAPL is near a short-term uptrend line. If it breaks, it might drop to $192. But if it rebounds, it could climb to $216.

Microsoft

Microsoft (MSFT) posted strong Q4 earnings, revenue rose 18%, reaching $76.4 billion. Also, net income jumped 24%, hitting $27.2 billion. Growth was fueled by strong performance across all segments.

Microsoft 365 and Dynamics 365 saw double-digit growth and intelligent Cloud surged 26%, reaching $29.9 billion. Also, Azure and related services jumped 39%.

Shares rose after earnings, boosting Microsoft’s valuation past $4.14 trillion.

Meta

Meta (META) beat expectations in Q2 earnings with $47.5B in revenue and $7.14 earnings per share.

Daily active users hit 3.48 billion, up 6% from last year. Ad impressions rose 11%, and ad prices climbed 9% year-over-year.

Operating costs grew 12%, totaling $27.07 billion this quarter. Employee headcount grew 7%, reaching 75,945 people.

Q3 revenue is expected between $47.5 and $50.5 billion. Fourth quarter growth may slow compared to last year. 2026 costs will rise due to infrastructure and hiring plans.

Meta faces legal challenges from European regulators. The stock jumped after strong earnings and Q3 forecasts. Market cap is nearing $2 trillion, driven by ads and AI.

Technically, META has dropped from its all-time high and is nearing strong support at $740. If bullish momentum returns, a rebound is possible but if that support breaks, further decline could follow.

eBay

eBay (EBAY) had a strong Q2, with revenue rising 6% to $2.7 billion and earnings beating expectations.

It introduced new features like eBay Live, an AI shopping assistant, and a video tool for sellers. The positive results pushed its stock surged to a new record.

For Q3, eBay expects steady revenue and sales growth, helped slightly by currency exchange, while staying focused on long-term goals despite possible trade challenges.

Strategy

MicroStrategy (MSTR) had a remarkable second quarter in 2025, reporting $114.49 million in revenue, slightly exceeding expectations and demonstrating stability amid broader market turbulence.

Its financial performance was supercharged by Bitcoin-related gains and a transition to fair-value accounting, driving a record-breaking net income of $10 billion and earnings per share of $32.60, vastly outperforming projections.

Despite the cloud of a class action lawsuit, MicroStrategy’s stock rose 8% in July, outpacing broader market trends that were weighed down by trade concerns and employment data.

Over the last five years, its shares have skyrocketed over 3,100%, consistently beating returns from both the US market and software industry.

Technically, MSTR has strong Fibonacci and static support near $359. If this level breaks, the price could drop further. However, entering oversold territory may trigger a rebound.

Roblox

Roblox (RBLX) reported a Q2 loss of $278.4 million, but revenue of $1.08 billion and bookings of $1.44 billion beat expectations.

User growth was strong, with 111.8 million daily users and 27.4 billion hours engaged. Free cash flow rose 58% year-over-year.

Despite losses, the company expects continued growth and increased revenue in Q3 and full year.

Following the report, shares Surged to new record, driven by confidence in Roblox’s expanding user base and solid guidance.

Technically, RBLX is approaching its uptrend amid falling momentum. If the trend breaks, it may drop to lower zones. But if it bounces, the stock could resume growth, especially with its solid guidance for next quarter.

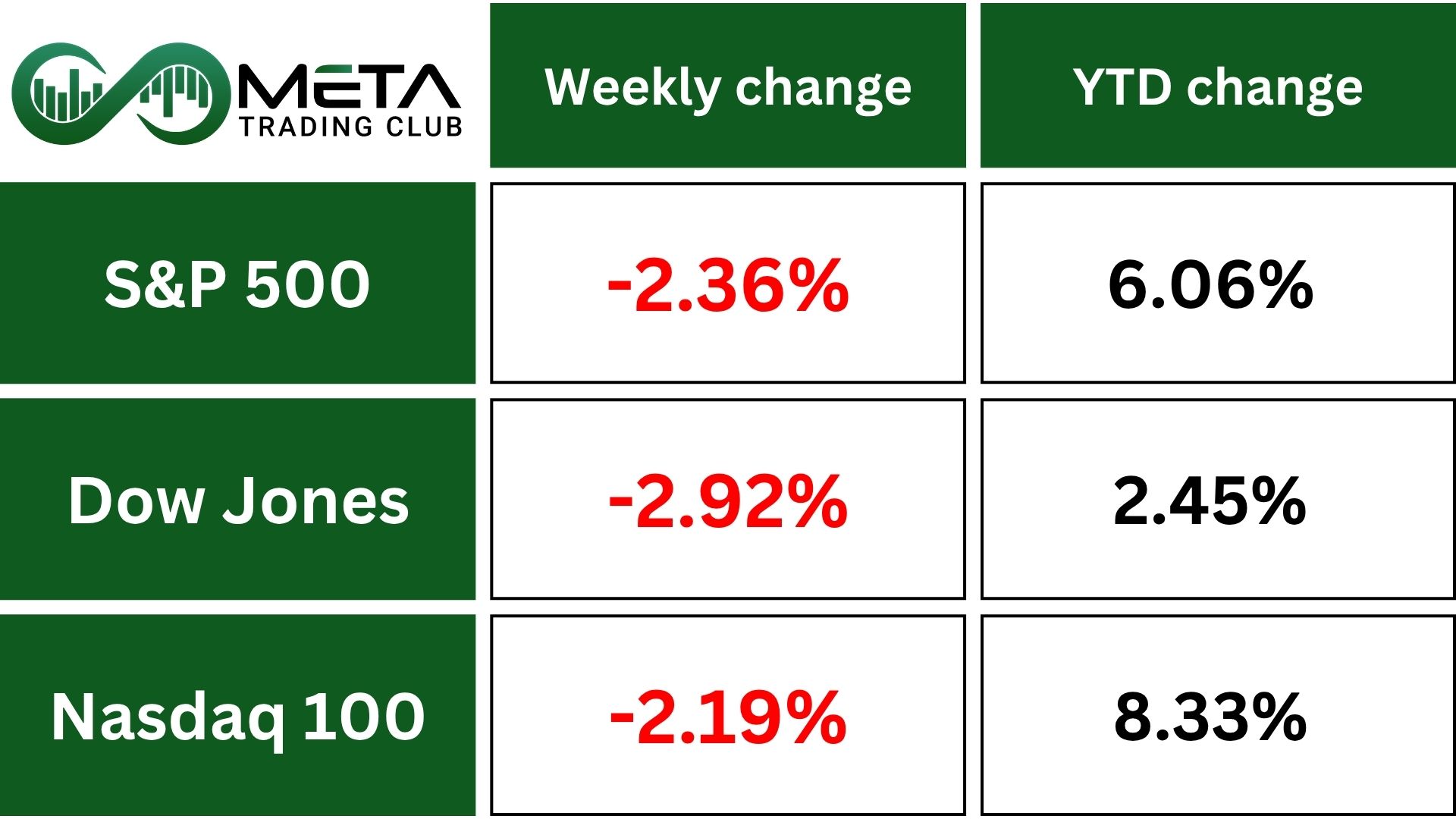

Indices

Indices’ Weekly Performance:

Last week, Wall Street hit a speed bump after a strong run, with major indexes reversing course amid a wave of unsettling news.

The S&P 500 fell 2.4%, snapping its two-week winning streak as concerns mounted over weak payroll data, lackluster earnings results, and heightened trade tensions driven by President Trump’s latest tariff rhetoric.

After a six-day run of record closing highs, the index began the week on a high note, only to slide steadily with four consecutive days of declines that reflected rising investor caution.

Meanwhile, the Dow retreated around 3%, marking one of its steepest weekly drops in recent months. It flirted with fresh all-time highs early in the week but failed to hold momentum, facing yet another technical rejection that underscored resistance at the top.

The Nasdaq also dropped, losing about 2%, as growth-sensitive sectors like semiconductors and internet platforms came under pressure.

Technically, SPX is dropping from 6400 and nearing strong support at its previous high of 6133. If bullish sentiment spreads, it may rebound—but if this support fails, further downside could follow.

Stocks

Sector’s Weekly Performance:

Broad market pullback, with Materials and Consumer Discretionary hit hard but Utilities remained stable.

- Consumer Discretionary slid 4.6%. Amazon declined due to slow cloud growth.

- Basic Materials dropped 4.6%. Freeport-McMoRan sank after copper tariffs and weaker demand.

- Healthcare fell 4.5%. Align crashed 33% on weak earnings and forecast; UnitedHealth cut 2025 outlook.

- Financials dropped 3.7%. Bank stocks slipped as labor data signaled a cooling economy. S&P bank index lost 4.7%; KBW regional banks slid 5%.

- Industrials down 3.2%. UPS dropped over new China import tariffs.

- Tech declined 2.14%. Palo Alto slipped on a costly CyberArk deal; Apple rose, then ended about 5% down. Micrsoft gained on strong Azure growth, hitting $4 trillion market value. Semiconductor stocks lost 2%.

- Energy dipped 1.3%. Chevron and Exxon beat earnings but fell Friday.

- Communication Services held flat. Meta surged on strong revenue forecasts and AI ad growth.

Overall, investors voiced concerns over stock valuations.

Top Performers

Last week saw remarkable stock market performance, with several companies standing out as top gainers:

- eBay (EBAY): Surged 12.66% after beating Q2 earnings estimates. Growth was driven by strong e-commerce demand, advertising revenue up 21%

- Corning (GLW): Advanced 12.08% following record Q2 results. Revenue rose 19%, fueled by booming demand for optical communications products tied to AI infrastructure and next-gen glass technologies.

- Western Digital (WDC): Gained 11.23% amid investor optimism over its planned spin-off of SanDisk and strong Q2 results. Revenue jumped 41% YoY.

- Monolithic Power Systems (MPWR): Up 9.93% after reporting 31% revenue growth, and EPS beat expectations.

- Vistra (VST): Climbed 8.25% as investors priced in higher electricity prices and strong summer demand.

- Cadence Design Systems (CDNS): Up 7.46% after posting revenue growth was led by AI-driven design tools like Cerebrus and the Millennium M2000 supercomputer.

- HCA Healthcare (HCA): Gained 6.77% after reporting Q2 EPS up 24%, driven by higher patient volumes and improved payer mix.

- Meta Platforms (META): Rose 5.24% after reporting Q2 revenue, up 22%. Ad impressions rose 11%, and average price per ad increased 9%.

Commodity

Weekly Performance of Gold, Silver, WTI and Brent Oil:

Gold (XAU/USD) rose nearly 1%, topping $3,400 per ounce, after weak U.S. job data signaled a cooling labor market.

Markets now see a 75% chance of a Fed rate cut in September, up from 45%. This followed hotter-than-expected inflation data, complicating the Fed’s next move.

Separately, President Trump reaffirmed a 10% global base tariff plan. He added new duties (up to 41%) on nations without U.S. trade deals. A 40% tariff was also announced on rerouted goods meant to avoid current trade rules.

Technically, Gold has been consolidating in a range between $3,240 and $3,440 for some time. Last week, it bounced off its 100-day moving average, showing renewed buying interest. For the next clear trend to emerge, gold needs to either break above $3,440 resistance or below $3,240 support. Until then, price action may remain sideways.

WTI Crude Oil fell to $69 per barrel after a three-day rally, as traders weighed geopolitical risks and rising U.S. inventories.

Markets remained cautious amid President Trump’s threats of 100% tariffs on Russian trading partners and possible duties on China. Uncertainty over policy direction led to hesitancy in pricing.

Also, a surprise build of 7.7 million barrels in U.S. crude stocks added pressure, though gasoline inventory drops signaled strong summer demand, softening the impact.

Forex

Weekly Performance of Major Foreign Exchange Pairs:

Dollar slumps after weak U.S. jobs report and downward revisions, retreating from a two-month high after disappointing July economic data raised expectations for a Federal Reserve rate cut in September. These reports pushed the probability of a September rate cut to 84%, up from 40% earlier.

Initially, the dollar had rallied on safe haven demand due to global equity market turmoil sparked by President Trump’s new tariffs, including a 35% hike on Canadian goods and a global minimum of 10%. However, the weak data reversed that momentum.

Crypto

Bitcoin spent most of the week trading steadily between $117K–$119K before dropping sharply to $114K due to new tariffs from President Trump. Despite the volatility, it recovered slightly and ended the month at $115K, down 2.5% for the week.

Altcoins saw steeper losses, with Ethereum and XRP falling about 10%, and others like SOL, DOGE, and ADA dropping above 10%.

On the news front, the White House released a crypto report but didn’t mention a Bitcoin reserve plan. Ethereum marked its 10th anniversary and saw record ETF inflows.

Also, Strategy Corp raised $2.52 billion in its IPO and bought over 21,000 BTC. Meanwhile, whales now control 68% of all Bitcoin after a major buying spree.

Next Week’s Outlook

Economic Events

Markets are keeping a close eye on upcoming Fed commentary for clues about the interest rate outlook, especially after the latest US jobs data pointed to a slowdown in hiring.

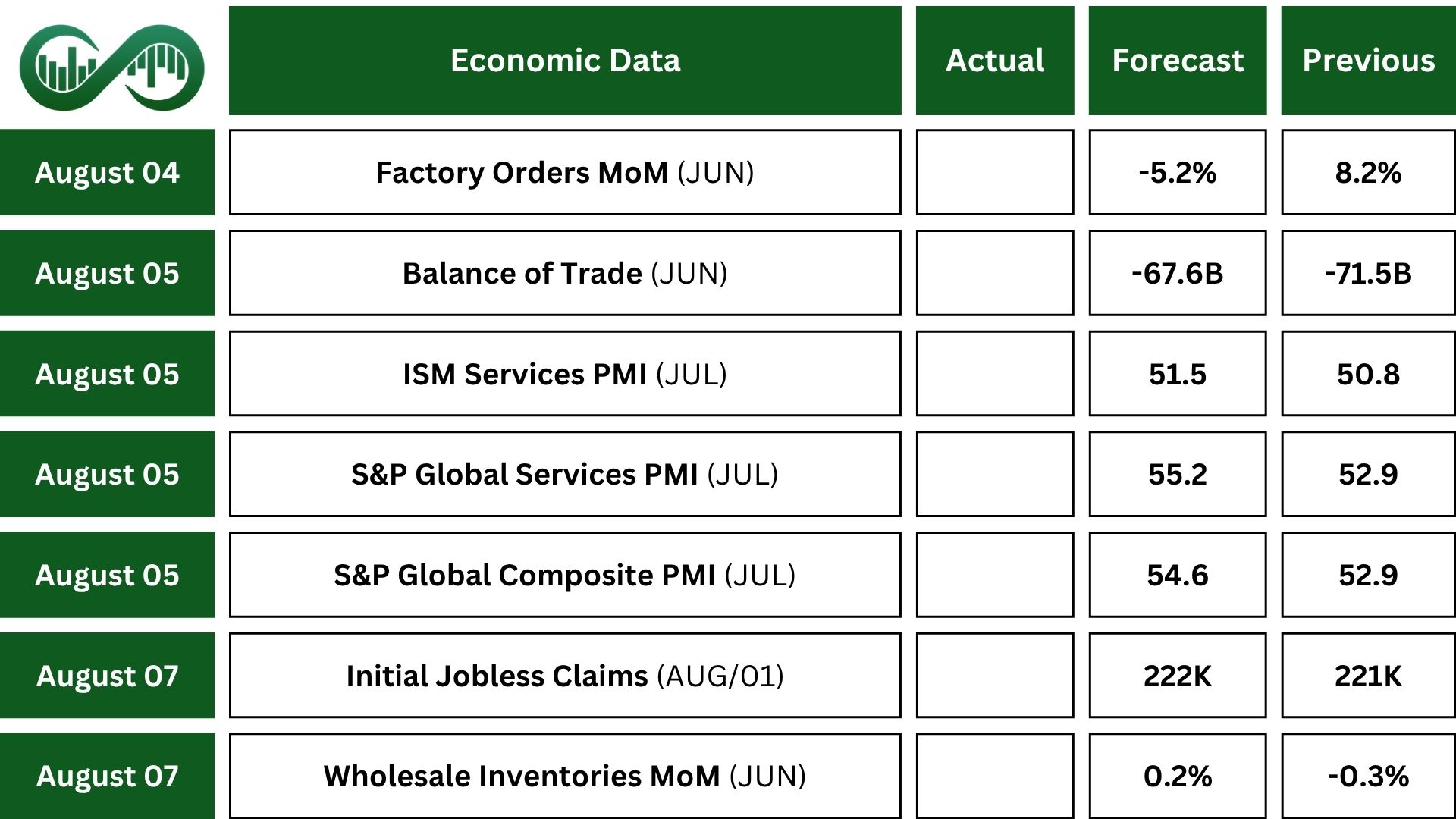

Key economic indicators this week include the ISM Services PMI expected to reflect the fastest growth in three months.

Factory orders are predicted to decline by 5.2% in June, undoing May’s sharp 8.2% jump, while the trade deficit is set to shrink significantly due to falling imports.

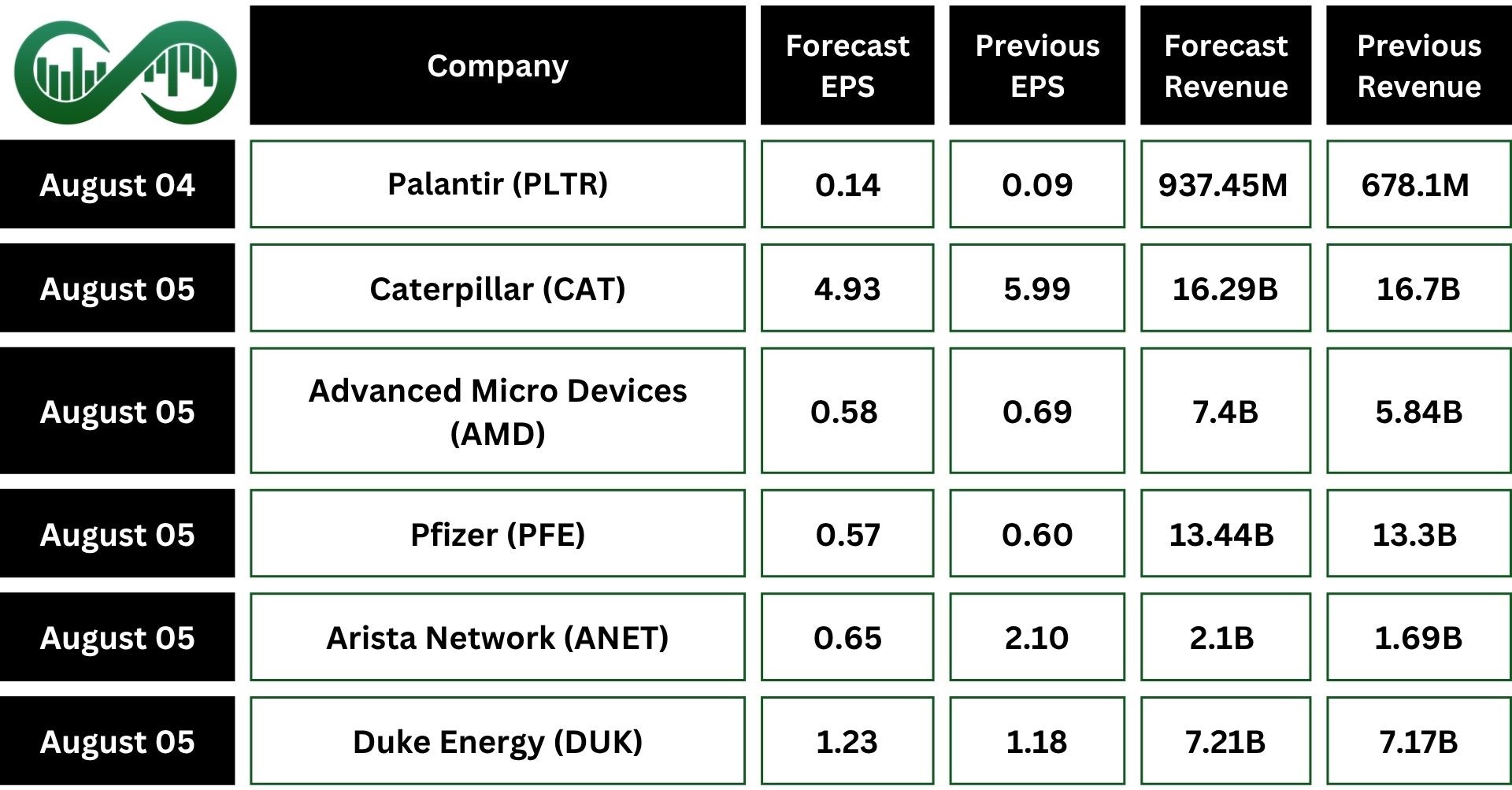

Earnings Events

Earnings season rolls on, with major companies like Palantir (PLTR), Disney (DIS), Uber (UBER), Caterpillar (CAT), Pfizer (PFE), Advanced Micro Devices (AMD), Amgen (AMGN), McDonald’s (MCD), Eli Lilly (LLY), Arista Network (ANET), Gilead (GILD), and Vistra (VST) set to report their results.