Last Week’s report

Economic Reports

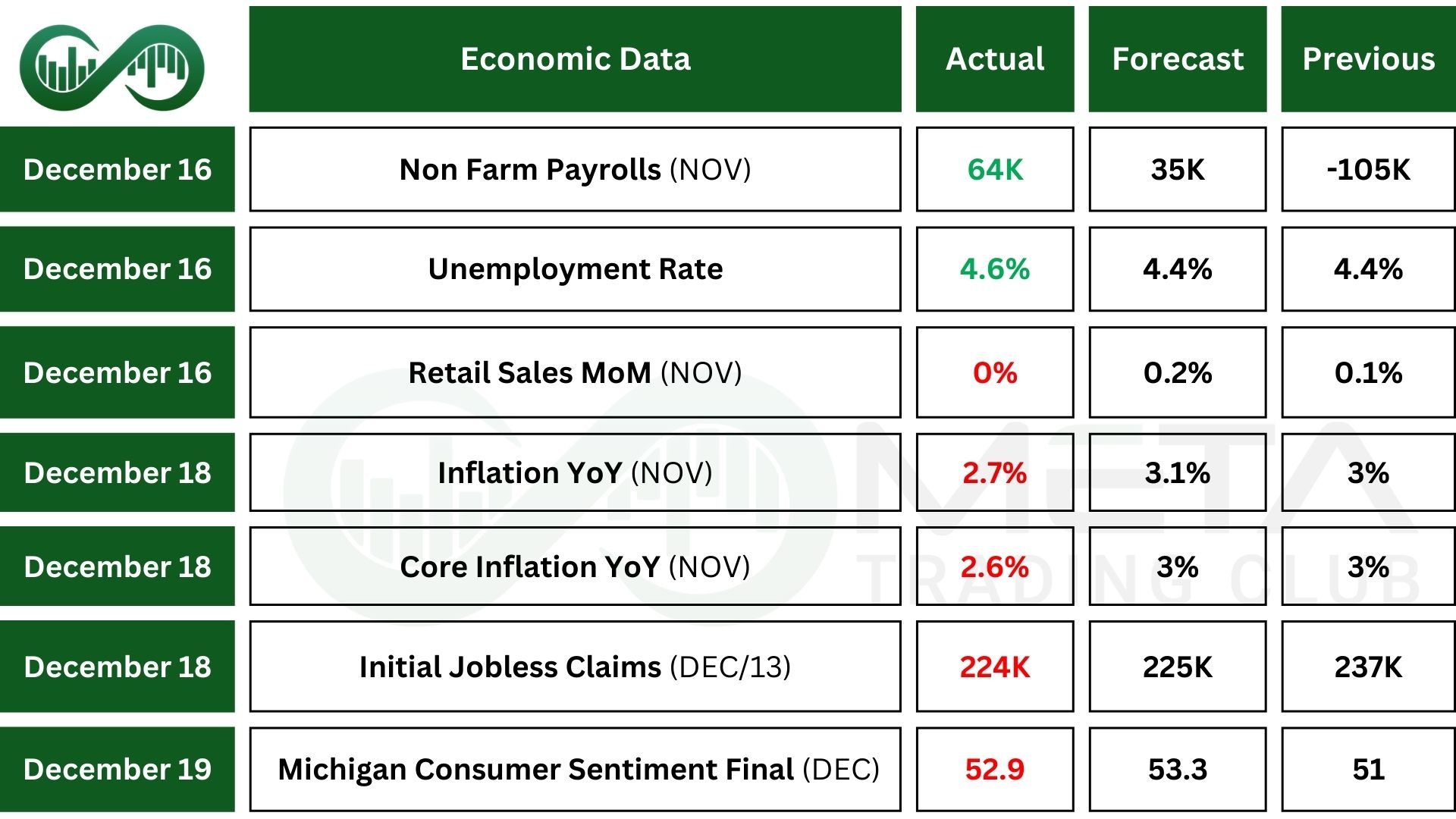

US retail sales were flat in October, showing no growth and coming in weaker than expected. But a key measure that feeds into GDP (sales excluding food services, autos, building materials, and gas) jumped 0.8%, a strong rebound from September. Auto sales fell sharply, and several categories like building materials, gas stations, and restaurants also declined. These drops were partly offset by gains in furniture, sporting goods, online retailers, clothing, electronics, and general merchandise stores.

US inflation slowed to 2.7% in November, the lowest in several months and below expectations. Energy costs rose especially fuel oil and natural gas. While food, shelter, medical care, and used cars also became more expensive. Price increases were smallest for clothing and new vehicles. Core inflation eased to 2.6%, it’s lowest since 2021. Because the government shutdown prevented data collection in October, both October and November reports were missing, though the BLS noted that prices rose 0.2% from September to November.

Job Report

US Non-Farm Payrolls growth improved in November, with payrolls rising 64,000 after a 105,000 loss in October and beating expectations. Most of the gains came from health care and construction. Job losses continued in the federal government, which shed 6K jobs in November and a much larger 162K in October due to workers taking buyouts tied to efforts to reduce the size of government. Earlier months were revised lower as well, with August and September both showing weaker job growth than initially reported.

The US Unemployment Rate rose to 4.6% in November, up from 4.4% in September and higher than expected, reaching its highest level in four years. Even so, the number of unemployed people was 7.8 million and overall employment levels didn’t change much. The labor force participation rate stayed steady at 62.5%, showing little shift in how many people are working or looking for work. A broader measure of unemployment, the U‑6 rate, also increased because more people were forced to work part‑time even though they wanted full‑time jobs.

Fewer people filed for unemployment benefits in mid‑December, with new jobless claims dropping to 224,000, slightly better than expected. This suggests the job market stayed fairly steady, even though recent numbers have been a bit messy because of holiday‑related data issues.

People already receiving unemployment benefits rose to 1.897 million in early December, up from the previous week but still lower than what economists predicted.

Earnings Reports

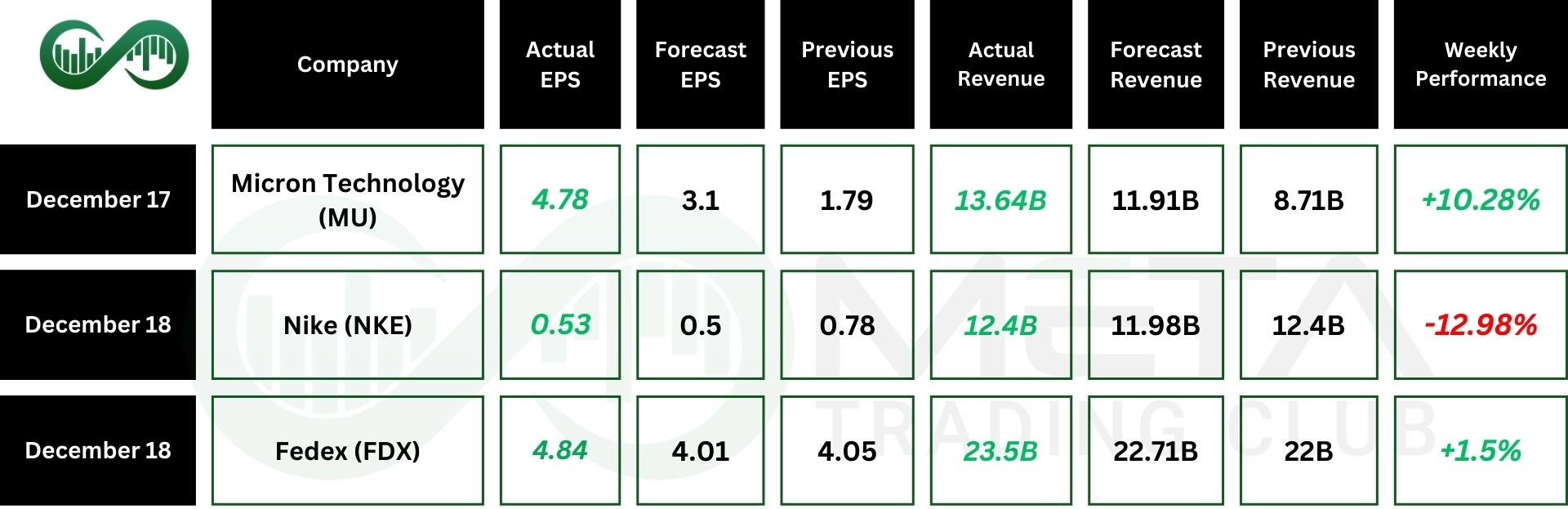

Micron

Micron (MU) posted very strong Q1 results, with revenue jumping 57% year over year to $13.6 billion, beating expectations. The company also delivered adjusted EPS of $4.78, well above forecasts of roughly $3.95.

Micron Technology expects its next‑quarter profit to be almost double what Wall Street predicted, thanks to soaring demand and tight supply for memory chips used in AI data centers. The strong outlook pushed Micron’s shares up 10%.

Micron is one of only three major suppliers of high‑bandwidth memory chips, which are essential for training AI models. Because supply is so tight, the company says it can meet only about half to two‑thirds of customer demand and expects shortages to continue past 2026. Micron is negotiating long‑term contracts and plans to boost its 2026 capital spending to $20 billion to expand capacity.

Nike

Nike (NKE) reported mixed Q2 results for fiscal 2026, with revenue rising 1% to $12.4 billion, slightly above expectations. Strength in North America and an 8% jump in wholesale sales helped offset weakness in Greater China and a sharp 8% drop in Nike Direct.

Profitability slipped, with gross margin down and diluted EPS falling 32% to $0.53, while Converse revenue plunged 30%.

Nike’s stock fell nearly 12% after the company warned of a revenue decline this quarter. Investors remain concerned about soft demand in China, excess inventory, and market‑share losses in running.

FedEx

FedEx (FDX) reported solid quarterly results, but its shares. The company expects 5–6% sales growth and adjusted EPS of $17.80 to $19 for fiscal 2026. Its FedEx Express unit performed well, helped by higher‑priced priority shipments and stronger domestic volume, even as rising wages added pressure.

Analysts remain upbeat, raising price targets for FedEx stock to a range of $210–$330, signaling a broadly positive outlook.

Indices

Indices’ Weekly Performance:

U.S. stocks rose on Thursday and Friday last week, allowing the S&P 500 and Nasdaq to finish the week with small gains after several days of choppy trading driven by renewed worries about AI‑related stocks.

Friday’s “triple witching”, when stock options, index options, and futures all expire at once, added support to the market. The bounce in oversold stocks and the clearing of options positions helped stabilize trading, though he warned that markets could become more volatile after Christmas.

The historic $7.1 trillion Triple Witching event took place on Friday, December 19, 2025, marking the largest derivatives expiration in market history. On this day, an estimated $7.1 trillion in stock options, index options, and futures contracts expired simultaneously, a quarterly event known for triggering heavy trading flows and increased volatility.

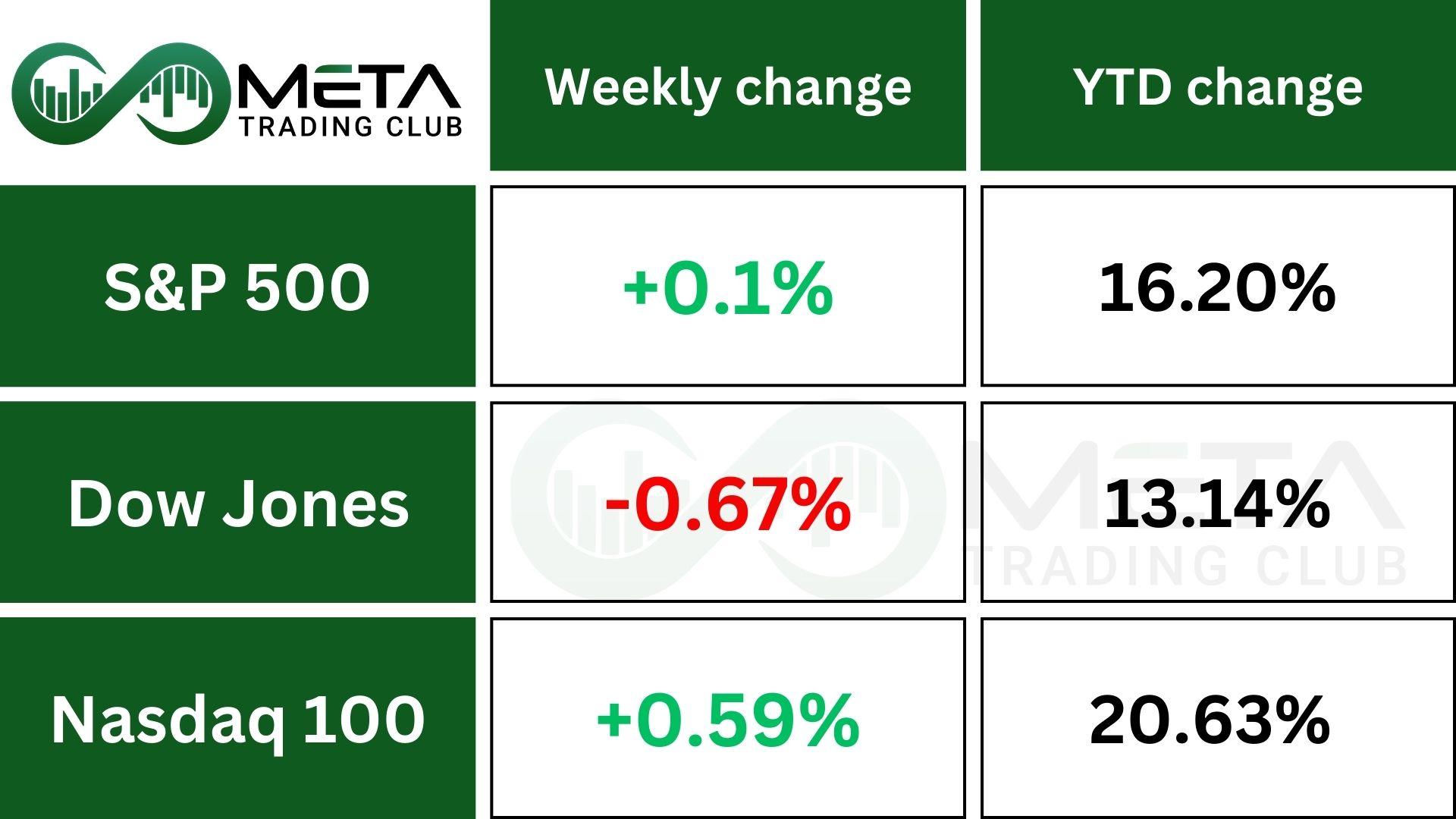

For the week, the S&P 500 inched up 0.1%, the Nasdaq gained 0.48%, and the Dow slipped 0.67%.

Stocks

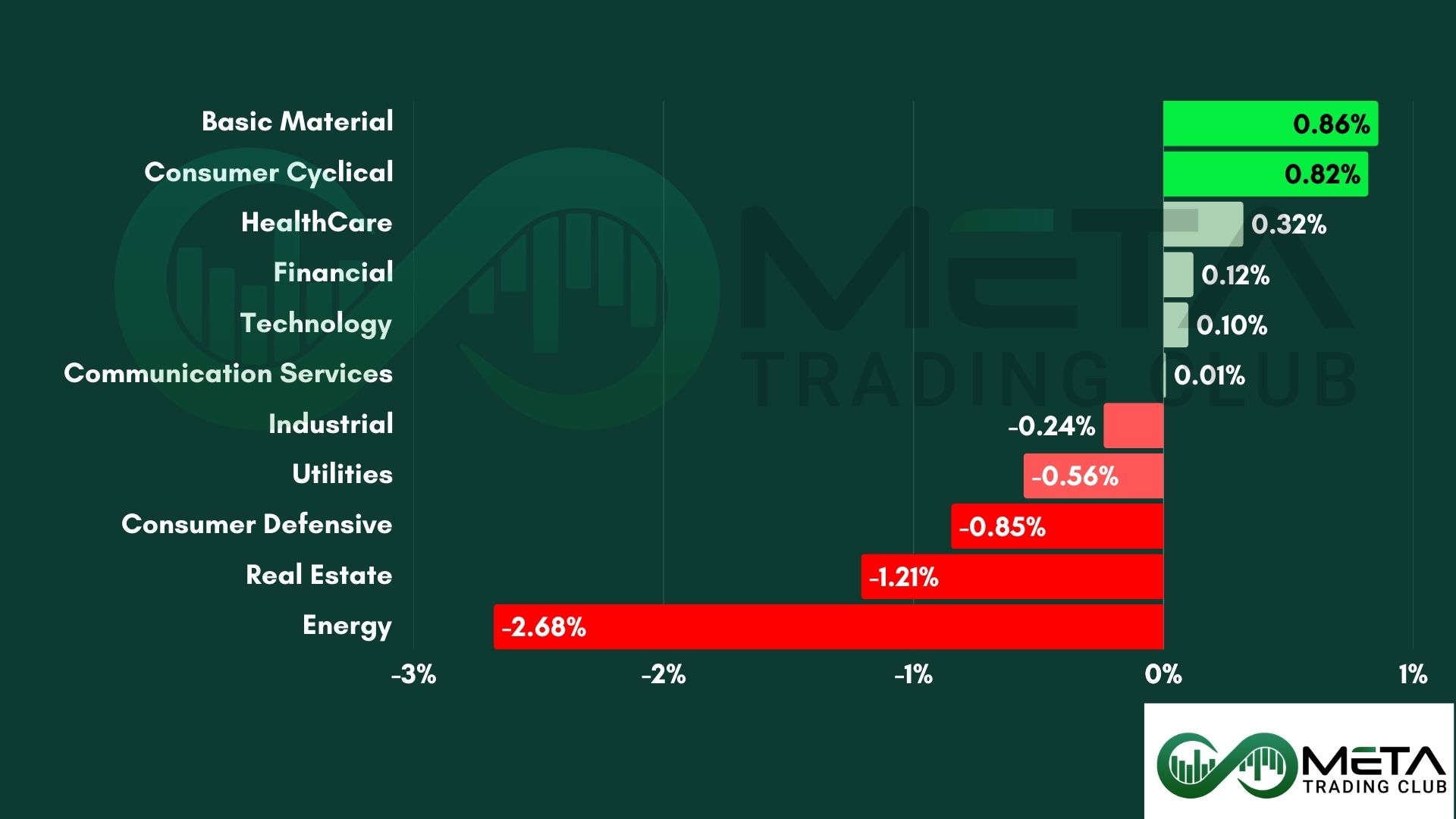

Sector’s Weekly Performance:

- Basic Materials rose 0.86% due to strong demand for industrial and precious metals, driven by inflation hedging and supply constraints.

- Consumer Cyclical gained 0.82% as holiday retail momentum and discretionary spending optimism lifted key names in e-commerce and autos.

- Technology set small 0.10% gain as Micron’s bullish outlook and Nvidia’s China chip optimism helped stabilize sentiment after midweek AI volatility.

- Communication Services ticked up 0.01% with TikTok-related optimism on Oracle, offsetting broader concerns around ad spending and platform engagement.

- Utilities fell 0.56% as rate sensitivity and weak seasonal demand weighed on power producers.

- Consumer Defensive declined 0.85% due to margin pressure and soft grocery and packaged food performance.

- Real Estate dropped 1.21% amid rising long-term yields, very high mortgages rates and weak flows into REITs.

- Energy sank 2.68% as oil prices fell over 2% for the week, pressured by supply glut fears and subdued demand.

Top Performers

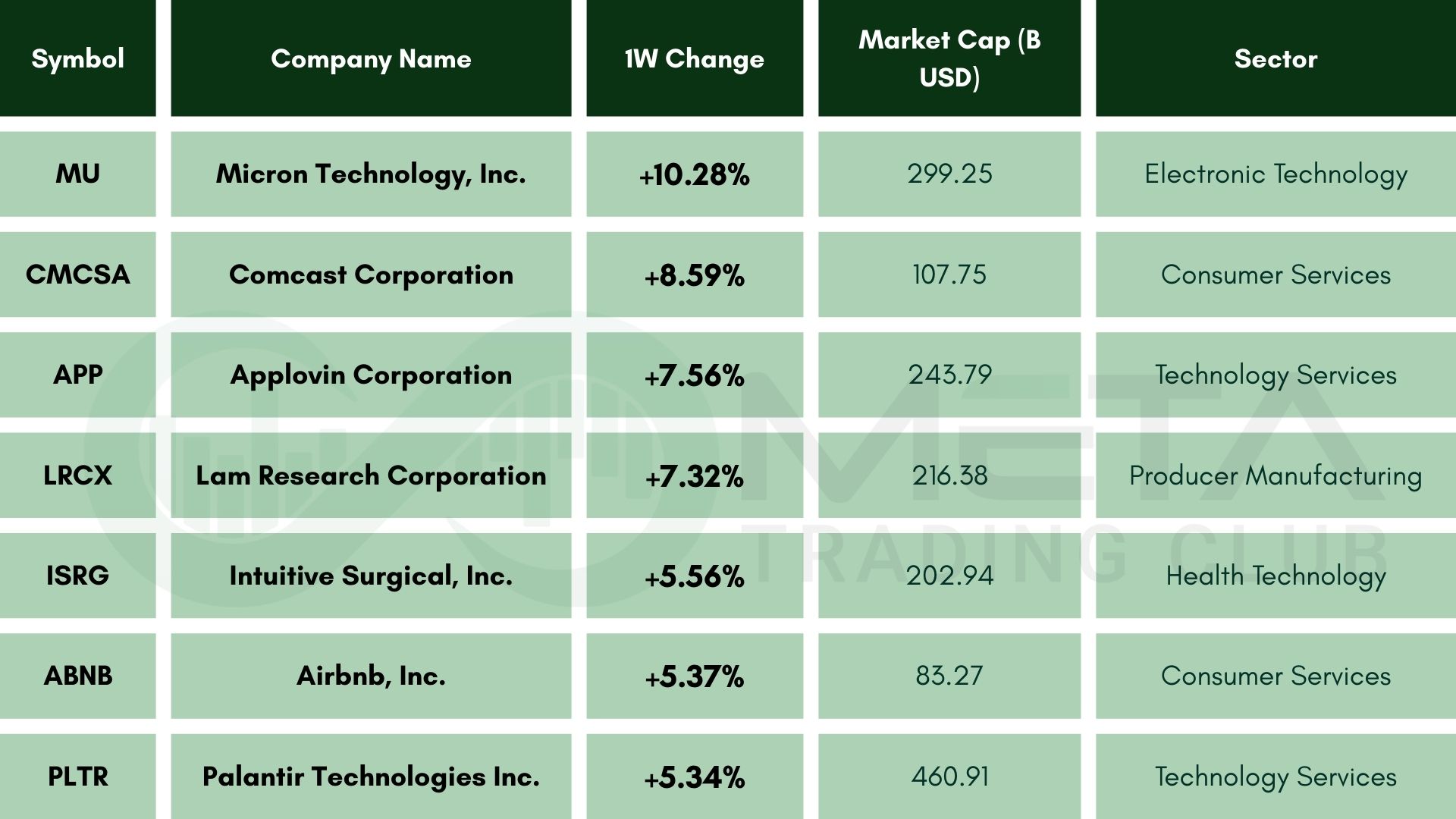

Last week saw a remarkable stock market performance, with several companies standing out as top gainers:

- Micron Technology (MU): Surged 10.28% after delivering a strong earnings outlook, easing concerns about chip sector valuations and AI infrastructure spending.

- Comcast (CMCSA): Jumped 8.59% on stronger broadband subscriber growth and holiday streaming demand.

- Applovin (APP): Rose 7.56% as ad‑tech momentum and investor rotation into high‑growth software boosted sentiment.

- Lam Research (LRCX): Climbed 7.32% alongside semiconductor equipment peers, supported by bullish chip sector guidance.

- Intuitive Surgical (ISRG): Gained 5.56% on robust procedural volumes and growing adoption of robotic surgery platforms.

- Airbnb (ABNB): Advanced 5.37% thanks to strong holiday travel bookings and upbeat forward guidance.

- Palantir (PLTR): Added 5.34% as investors rotated back into AI software leaders following midweek volatility.

Commodity

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Metals

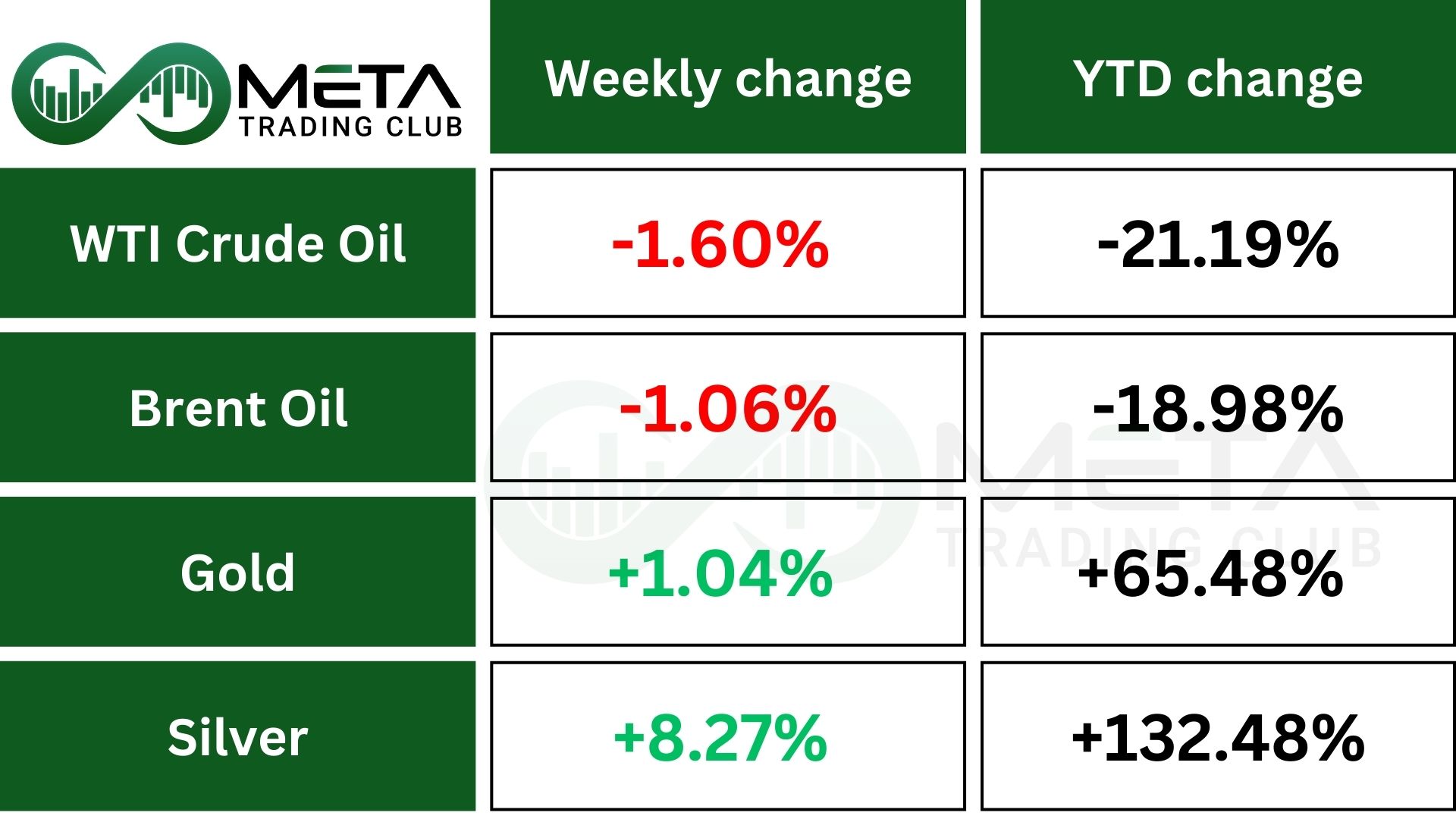

Gold and silver hit new record highs again on Friday, something they’ve been doing throughout 2025.

Gold futures closed at a record for the 51st time this year, with prices now up 66% in 2025. Silver has climbed even faster: its most‑active contract is up 131% this year and has set 14 new records.

Both metals are on track for their strongest yearly gains since 1979, which was also the last time they saw this many record highs.

Energy

Oil prices are on track for a weekly drop of about 2%, as worries about a growing supply glut outweigh geopolitical tensions. Crude is now 20% lower this year due to expectations of excess supply and weak demand.

Prices did get a brief lift after tensions rose between the U.S. and Venezuela, following a U.S. blockade on sanctioned tankers. But with trading volumes thinning ahead of the holidays, liquidity is falling, increasing the risk of sharper price swings.

Forex

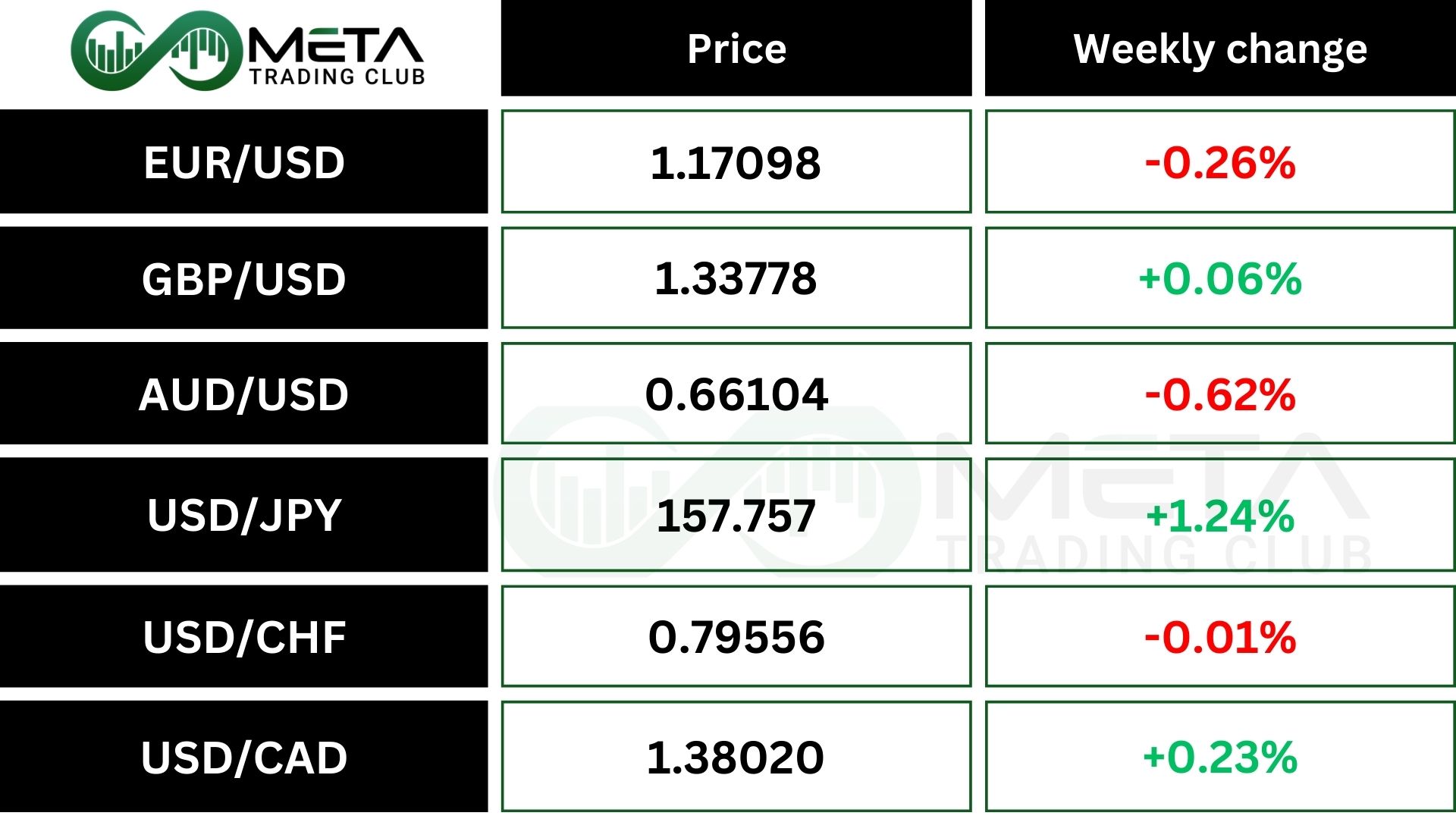

Weekly Performance of Major Foreign Exchange Pairs:

The Bank of Japan raised rates by 25 basis points to 0.75%, the highest level since 1995, but the move was fully expected and already priced in.

Instead of strengthening, the yen weakened as traders reacted to the lack of a hawkish shift. Markets were hoping for a clearer roadmap for future tightening, but the BOJ stuck to a cautious tone, signaling continuity rather than escalation.

Crypto

Bitcoin looks set to finish the year with losses, marking one of its weakest fourth quarters in recent years. Maybe 2026 could bring some relief, but the current price structure suggests Bitcoin may still face a deeper pullback first.

Bitcoin is stuck around its Point of Control (POC), a key price level where the most trading has occurred. Because BTC hasn’t reclaimed its recent highs, the price could slip below this level and fall toward the $70,000–$73,000 zone.

A weakening RSI also supports the idea of a drop into that range. Traders should watch for potential reversal signals near $72,000. However, if Bitcoin fails to hold the $70,000–$73,000 support, the market could face a deeper correction and a longer bearish phase.

As of now, Bitcoin trades around $88,330, with little movement in the past day. If BTC could break up $90K then crypto coins may rise further.

Next Week’s Outlook

Economic Events

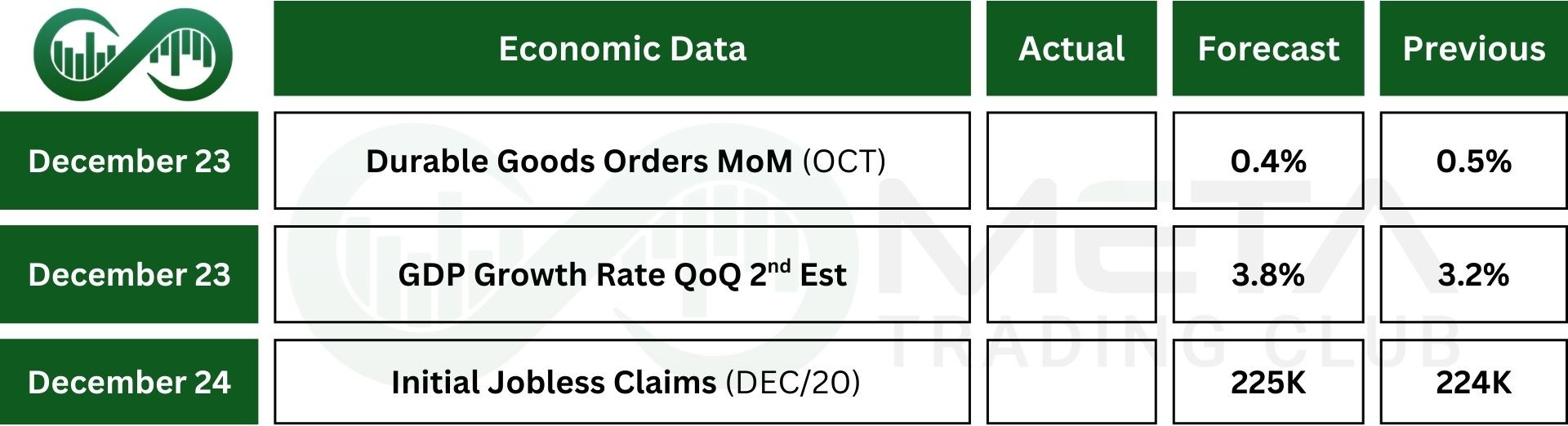

Christmas week is usually quiet in the US, with markets closing early on December 24 and fully closed on December 25.

Still, investors will have several delayed economic reports to review. The second estimate of Q3 GDP is expected to confirm 3.2% annualized growth, and new data on corporate profits will also be released.

October durable goods orders are forecast to rise 0.4%, and the Federal Reserve will publish industrial production numbers for October and November.

Other key updates include consumer confidence from the Conference Board, the Richmond Fed’s manufacturing index, and the Chicago Fed’s national activity index.

Earnings Events

This week brings no notable earnings releases.