Last Week’s report

Economic Reports

Federal Reserve commentary dominated markets last week, with several regional presidents striking a hawkish tone. St. Louis Fed President Musalem and Boston Fed President Collins warned against further rate cuts, echoing similar caution from Vice Chair Jefferson, Chicago’s Goolsbee, and Chair Powell. While some officials, like Governor Miran, still favor aggressive easing, the overall message pushed market odds of a December cut down from 63% to 42%, tilting expectations toward holding rates steady.

Heightened caution reflects limited visibility on labor market conditions due to the government shutdown, though private and state-level data suggest the jobs market is cooling gradually rather than collapsing.

The weekly ADP employment report announced a cut of an average of 11,250 jobs per week in late October, signaling that labor market momentum is dropping. With the government shutdown delaying official employment data, these private reports have taken on added importance.

Further highlighting the slowdown, Challenger reported 153,074 job cuts in October, the highest for that month since 2003.

The NFIB Small Business Optimism Index in the U.S. slipped to 98.2 in October, the lowest in six months. Small business owners reported weaker sales and profits, while many still struggled to hire due to labor shortages, with labor quality cited as the biggest challenge. About one-third of owners had job openings they couldn’t fill, and fewer expected better business conditions ahead. Price increases also eased compared to September, reflecting a softer outlook for Main Street.

Earnings Reports

Cisco

Cisco (CSCO) delivered strong Q1 FY2026 results, with revenue rising 8% to $14.9 billion and non-GAAP EPS up 10% to $1.00, both beating estimates.

Product orders surged 13%, driven by robust demand for networking and AI infrastructure, including $1.3 billion in hyperscaler orders.

The company also launched a major campus networking refresh cycle, boosting next-gen tech adoption.

Despite a 12% drop in operating cash flow, margins remained solid and guidance was raised. Cisco’s stock jumped over 9% last week, reflecting investor confidence in its growth trajectory.

Walt Disney

Walt Disney (DIS) reported mixed results for Q4 FY2025, with flat quarterly revenue at $22.5 billion and full-year revenue up 3% to $94.4 billion.

However, streaming and theme parks showed strong growth, with Disney+ and Hulu reaching 196 million subscribers and record income from the Experiences segment.

Weaknesses in cable TV and theatrical content weighed on quarterly performance, leading to a drop in Disney’s stock.

Despite this, the company expects double-digit EPS growth in fiscal 2026, boosted by $24 billion in content investment, expanded buybacks, and a higher dividend.

Applied Materials

Applied Materials (AMAT) posted mixed Q4 FY2025 results, with revenue down 3.5% year over year to $6.8 billion and non-GAAP EPS at $2.17, slightly beating expectations.

Regional sales fell in the U.S., Europe, Japan, and China, but grew in Taiwan, Southeast Asia, and Korea. Segment-wise, Semiconductor Systems and Global Services declined, while Display surged 68%.

Despite record annual revenue of $28.37 billion and strong full-year EPS growth, cautious guidance and regional weakness led to a drop in the stock. Investors remain wary as the company expects demand to pick up only in the second half of 2026.

Indices

Indices’ Weekly Performance:

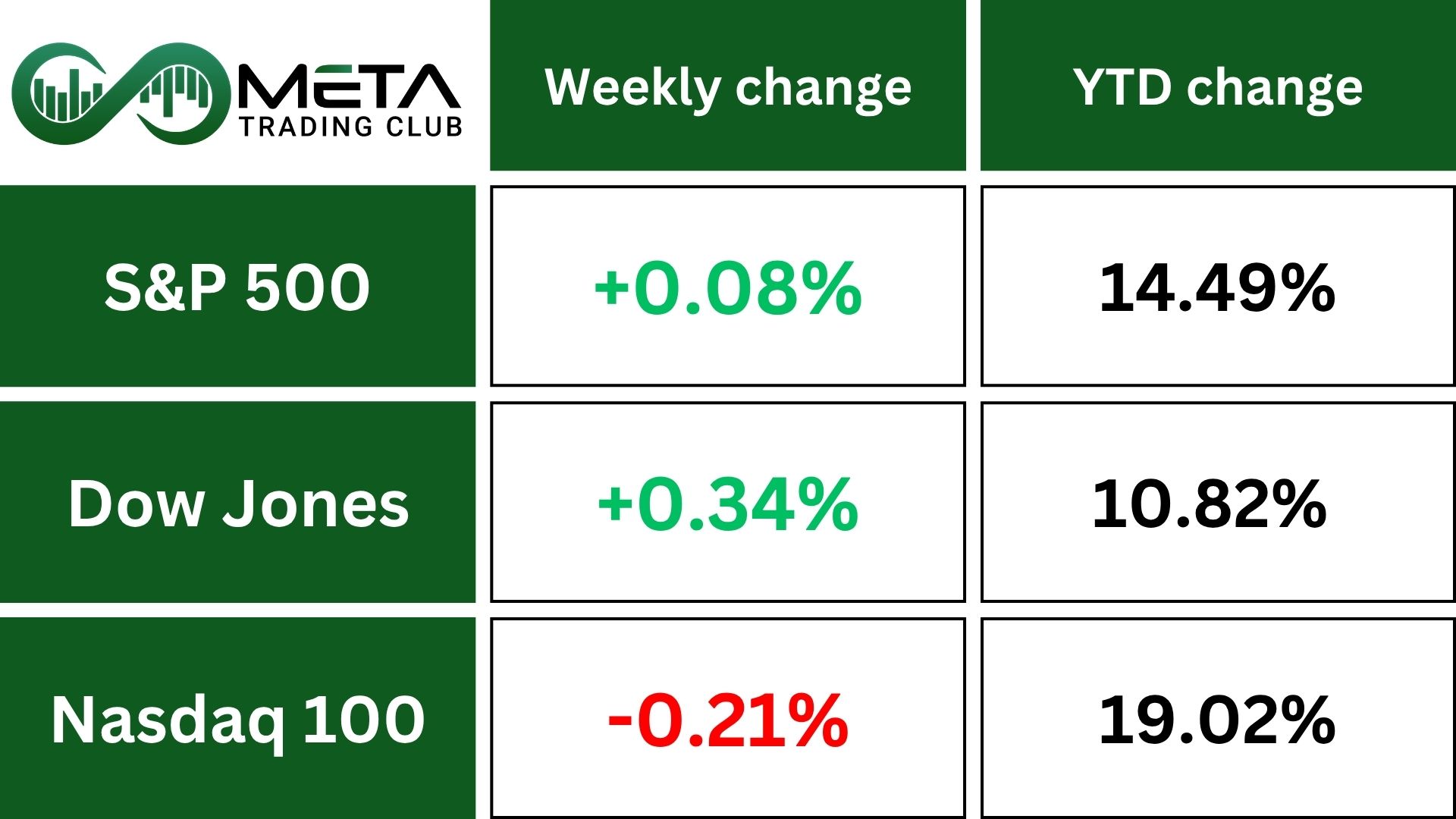

The S&P 500 edged up 0.08% this week, marking its fourth gain in the past five weeks and reflecting steady investor optimism.

Markets closed flat last week as traders weighed fading hopes for a December rate cut and looked ahead to Nvidia’s earnings. Concerns over inflation and stretched valuations persisted, with the odds of a Fed cut dropping below 50% from 67% a week earlier, pressured by global tariffs.

For the week, performance was mixed. The S&P 500 rose 0.1%, the Dow added 0.3%, while the Nasdaq slipped 0.5%. Investor sentiment remained cautious, with worries about labor market health and inflation outlooks.

Even after the record-long U.S. government shutdown ended on Thursday, traders expect lasting gaps in official economic data, leaving markets to rely on incomplete visibility.

Stocks

Sector’s Weekly Performance:

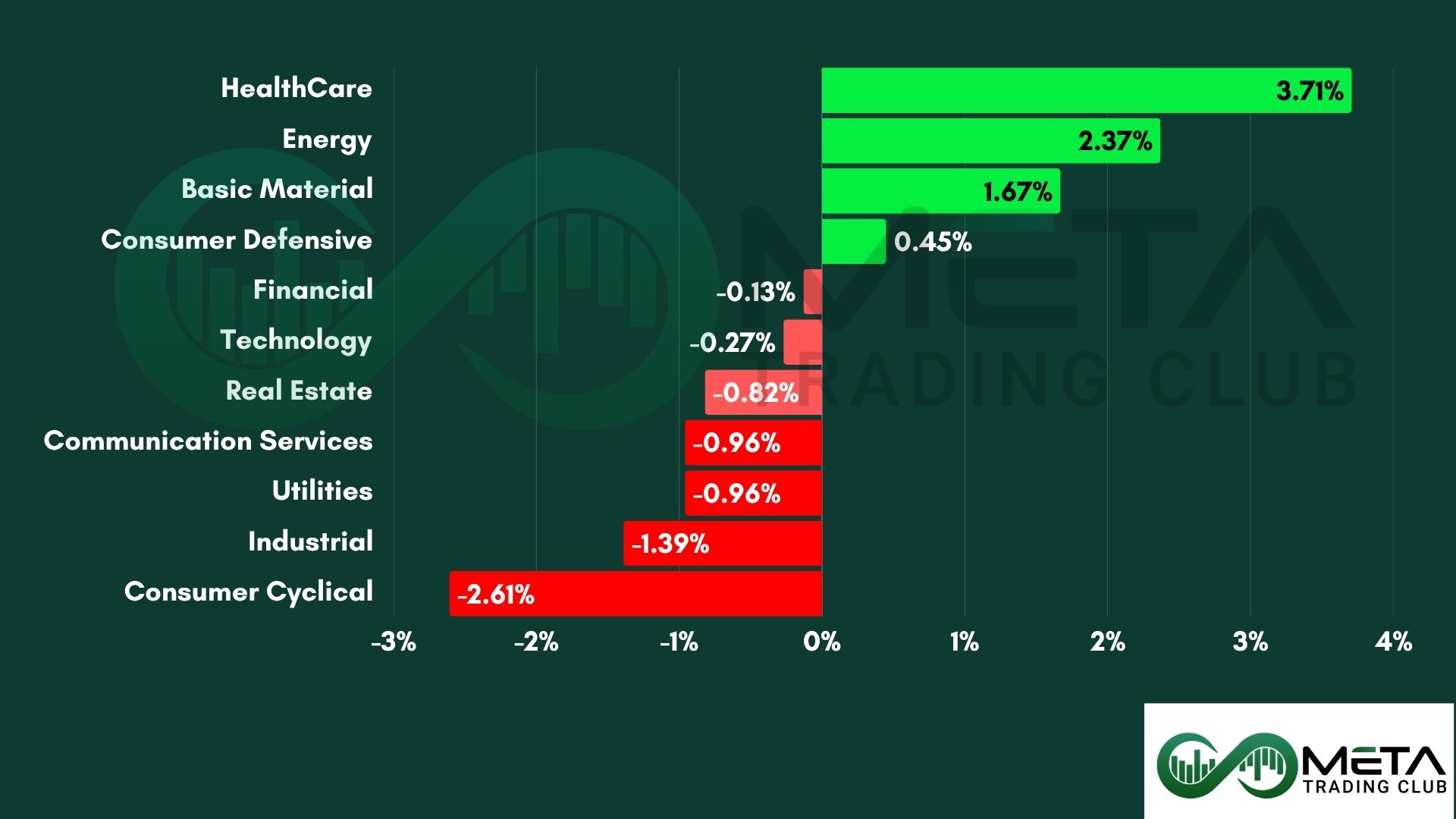

Despite mixed market sentiment and lingering uncertainty from the recent U.S. government shutdown, several sectors posted strong gains last week, led by health care and energy.

- HealthCare (+3.71%): Led the market as investors rotated into defensive names. Strong earnings and M&A activity boosted sentiment.

- Energy (+2.37%): Oil price rebound and geopolitical tensions lifted energy stocks.

- Industrial (−1.39%): Weighed down by post-shutdown data gaps and cautious investment outlook.

- Consumer Cyclical (−2.61%): Hit hardest as discretionary spending concerns grew.

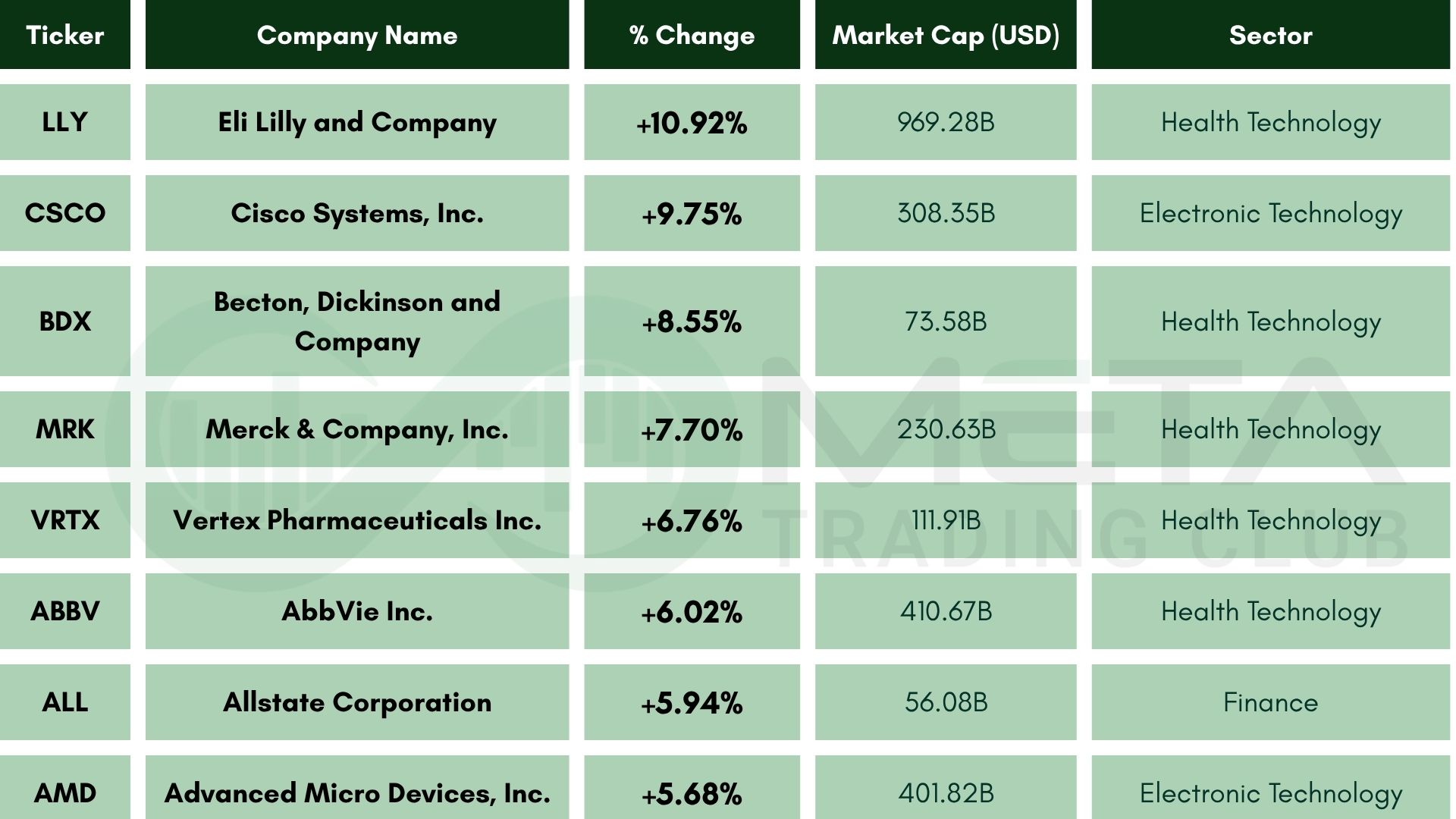

Top Performers

- Eli Lilly and Company (LLY): Surged 11% due to securing a major U.S. government pricing agreement, boosting investor confidence.

- Cisco Systems (CSCO): Soared 10% after beating earnings expectations and maintaining strong guidance.

- Becton, Dickinson and Company (BDX): Increased 8.5% after surprising analysts with an earnings beat and raising its full-year guidance.

- Merck & Company (MRK): Advanced 7.7% following announced positive clinical trial results for KEYTRUDA and WELIREG, expanded European approvals, and a $700M research partnership with Daiichi Sankyo.

- Vertex Pharmaceuticals (VRTX): Climbed 6.7% due to beating Q3 earnings estimates and raising its full-year guidance.

- AbbVie (ABBV): Rose 6% after it received bullish analyst upgrades.

- Allstate (AAL): Gained 6% after delivering a record net income.

- Advanced Micro Devices (AMD): Increased 5.6% following the announcement of a $100B data center revenue target and a foundational partnership with OpenAI. Analysts raised price targets, citing AI-driven growth.

Commodity

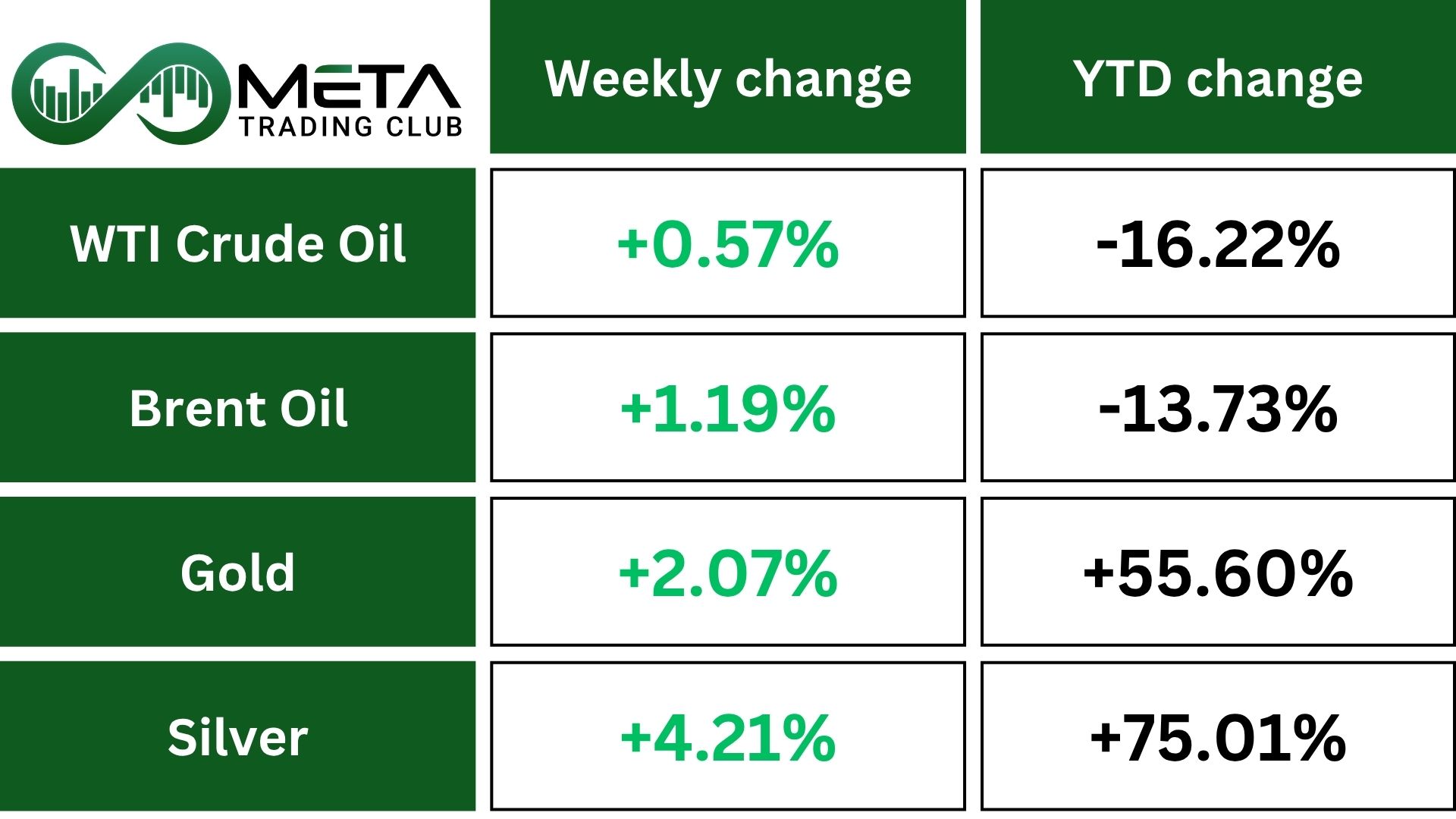

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Gold prices climbed above $4,200 per ounce on Thursday, marking a seventh straight gain and their highest level in over three weeks. This came after investors welcomed the end of the 43‑day U.S. government shutdown and anticipated renewed economic data releases alongside possible rate cuts.

However, by Friday, gold fell 3% in a broad market sell-off after hawkish comments from Federal Reserve officials dampened hopes for a December rate cut, erasing much of the week’s earlier rally.

Crude oil prices ended the week higher after rebounding on Friday from midweek losses.

The rally was driven by Ukraine’s strikes on Russian oil facilities, Iran’s seizure of a tanker, and ongoing sanctions, all of which tightened supply.

However, earlier declines came after OPEC projected a global surplus, but strong demand from China and heightened geopolitical risks helped crude recover and close the week in positive territory.

Forex

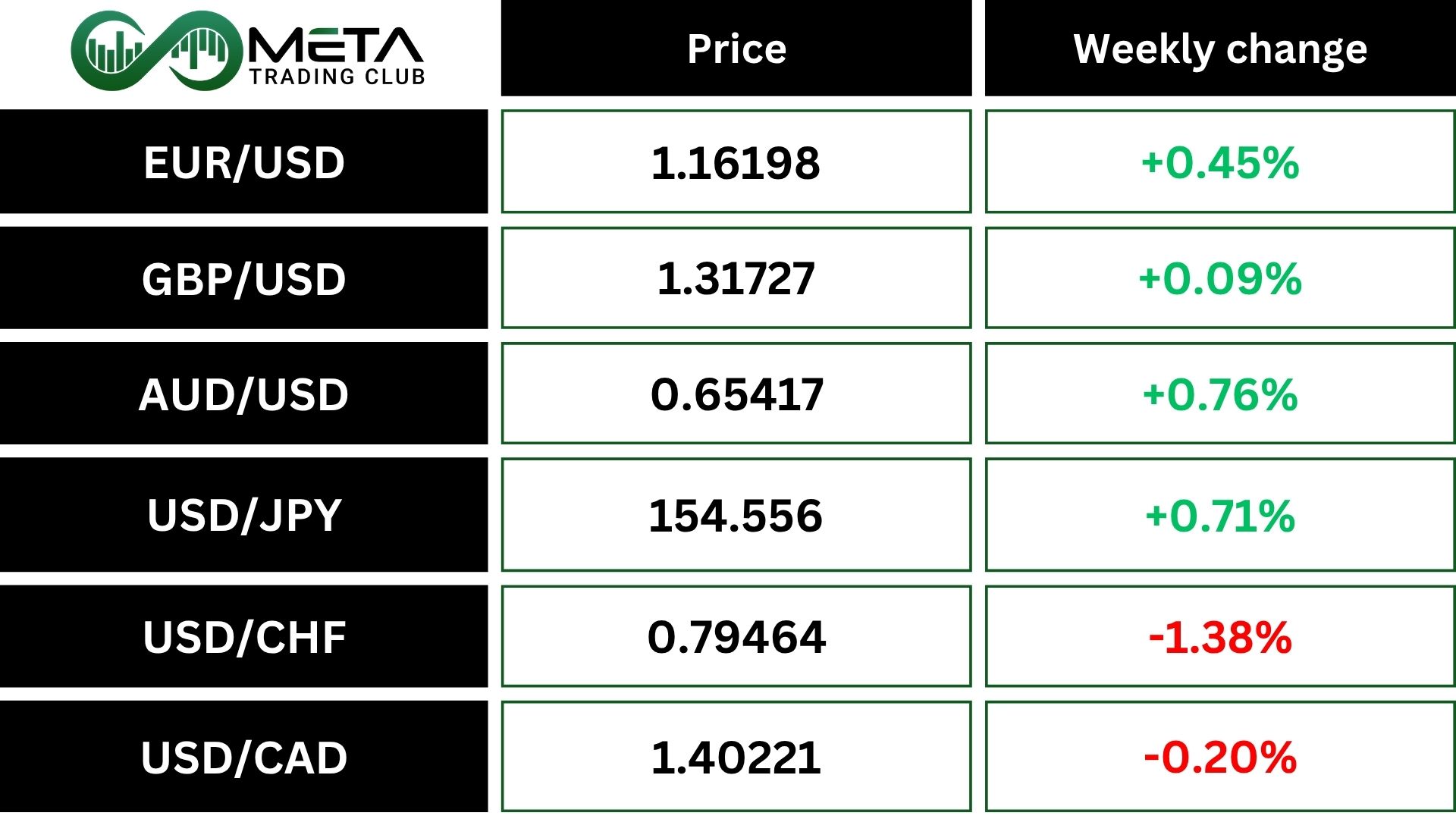

Weekly Performance of Major Foreign Exchange Pairs:

Dollar Index (DXY) showed mixed performance last week, reflecting diverging trends across major pairs. This divergence stems from fading expectations of a December Fed rate cut, now below 50% probability, and persistent inflation pressures, partly linked to President Trump’s global tariff policies.

The Swiss franc surged, with USD/CHF falling 1.38%, signaling a flight to safety amid global uncertainty. The move was amplified by Switzerland’s decision to cut tariffs on U.S. goods from 39% to 15%, easing trade tensions and boosting investor confidence in Swiss assets. The franc’s strength underscores its role as a safe-haven currency during periods of geopolitical and economic stress.

Crypto

Bitcoin has dropped below $96,000 for the first time since May, extending losses to nearly 25% from its record high of $126,000.

Selling pressure has intensified as risk appetite weakens, with over $600 million in crypto positions liquidated in the past 24 hours.

Unlike past dips, buyers are hesitant to step in, signaling caution and shifting sentiment. The selloff has spread across the market, with Ethereum sliding toward $3,100 and Solana falling into the mid-$140s, deepening the multi-day decline in altcoins.

Next Week’s Outlook

Economic Events

The longest government shutdown in U.S. history has ended, and major statistical agencies plan to release new schedules for delayed economic reports. However, some key data may be dropped if agencies can’t finish them due to disrupted data collection.

US data releases resume this week following the government shutdown, starting with the delayed September jobs report. However, normalization will be gradual, as data collection was also impacted during the closure.

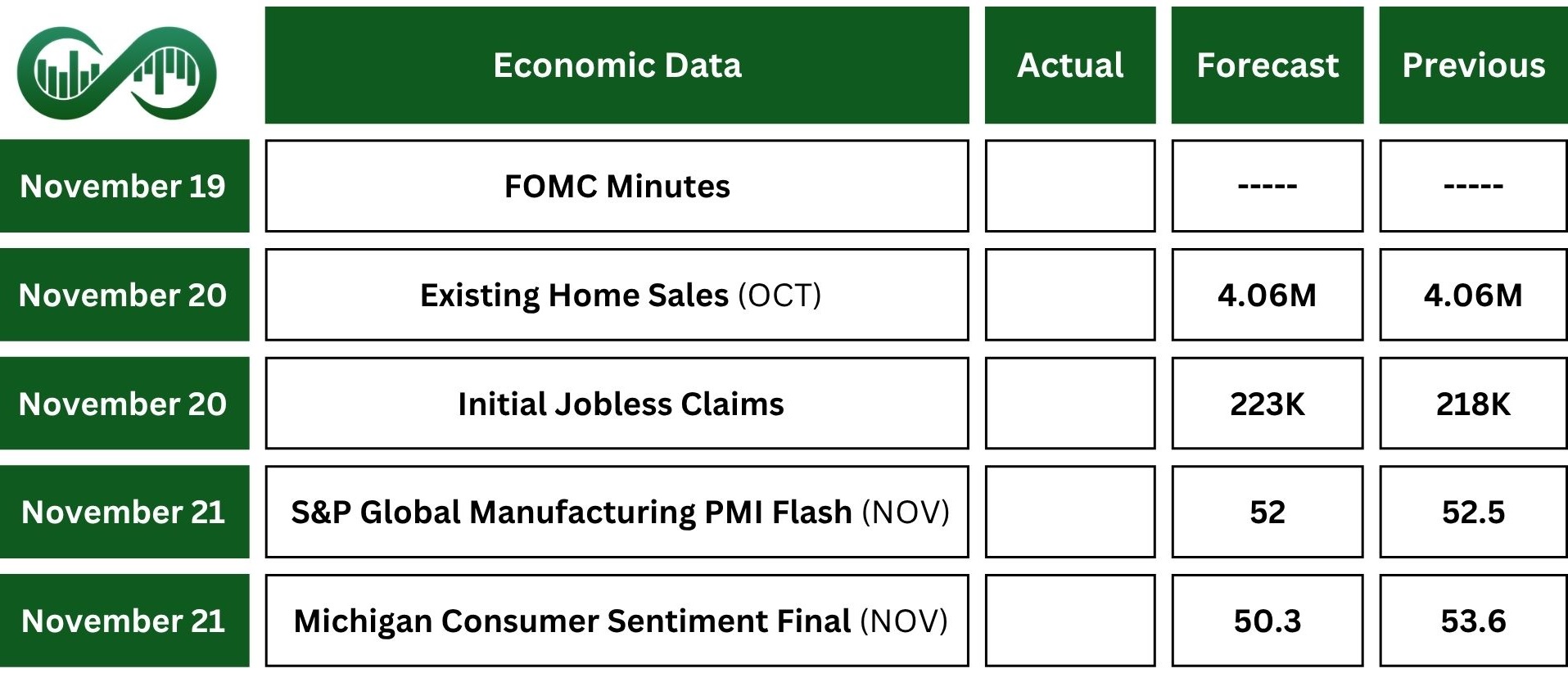

Despite this, private and regional indicators will still give clues about the economy. October’s existing home sales likely stayed flat. The NAHB Housing Market Index is expected to dip slightly, and the New York Empire State Manufacturing Index is expected to weaken.

Other upcoming data includes S&P Global Flash PMIs, ADP employment reports, Michigan Consumer Sentiment, and manufacturing surveys from the Philadelphia and Kansas Federal Reserve.

Investors will also watch the Federal Reserve closely, with speeches and FOMC meeting minutes offering hints about future policy moves.

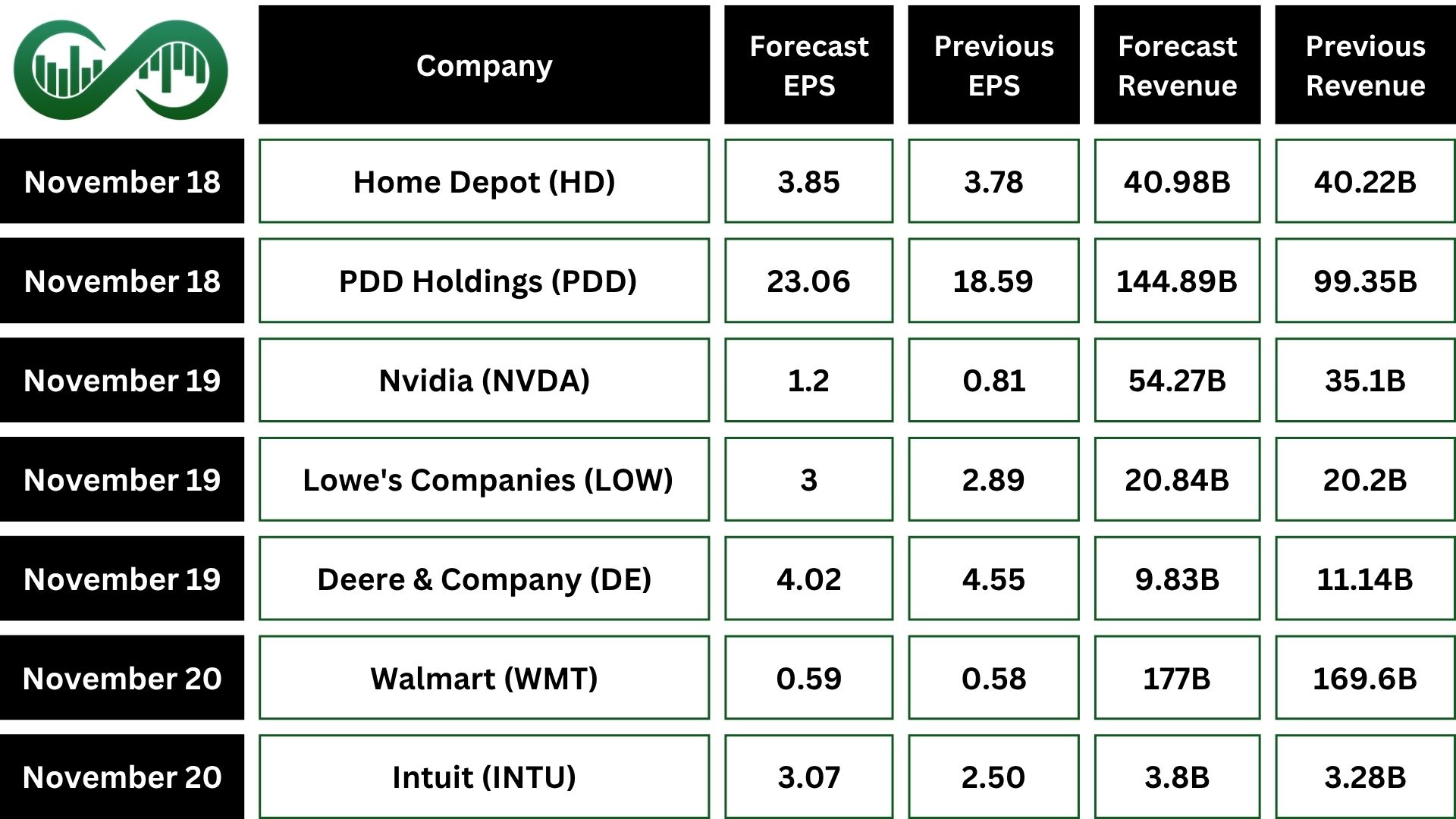

Earnings Events

On the earnings side, major companies reporting next week include Nvidia (NVDA), Walmart (WMT), Target (TGT), Home Depot (HD), TJX Companies (TJX), Lowe’s (LOW), Deere & Company (DE), and Intuit (INTU).

Nvidia’s upcoming earnings report is drawing intense focus, as investors look for signs that momentum in AI technology remains strong. Any disappointment could trigger a sell-off, but expect dip buyers to quickly return and help stabilize the stock.