Last Week’s report

Economic Reports

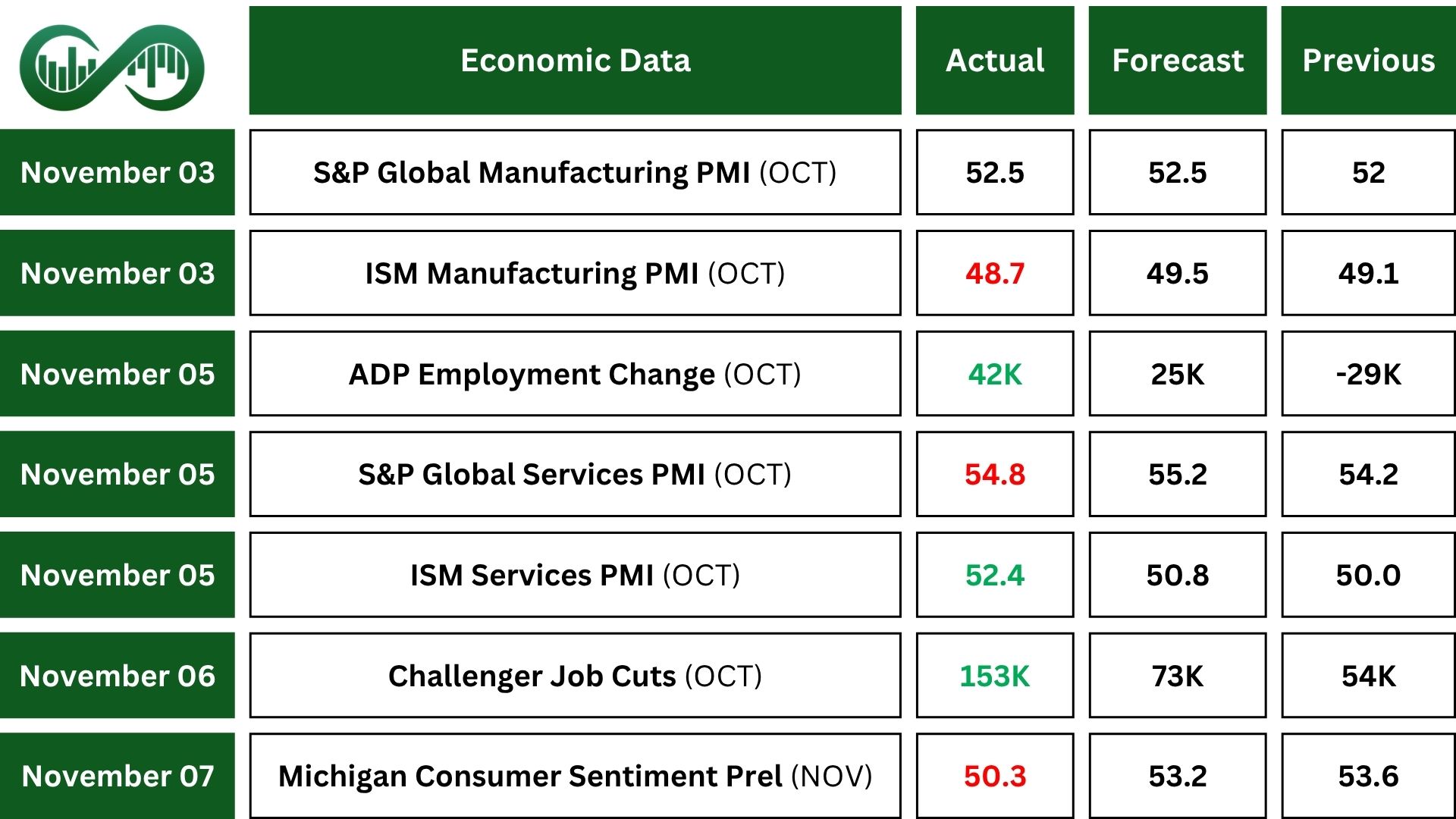

U.S. manufacturing activity continued to shrink in October, with the ISM Manufacturing PMI falling to 48.7, marking the eighth straight month of contraction. Employment remained weak as most companies focused on managing headcount rather than hiring. Price pressures eased slightly, but supplier deliveries slowed for the third month in a row.

ADP Employment Change reported private businesses added 42,000 jobs in October, recovering from job losses in September and beating expectations. It was the first monthly gain since July, though not across all sectors. Goods-producing industries added a few jobs, but manufacturing saw losses. Pay growth stayed flat, with job-stayers earning 4.5% more and job-changers 6.7%, suggesting a balanced labor market.

U.S. services activity picked up in October, with the ISM Services PMI rising to 52.4, the strongest growth since February. Business activity and new orders improved, but hiring continued to shrink, showing uncertainty about the economy’s strength. Price pressures increased slightly, driven by ongoing tariff impacts.

In October, Challenger Job Cuts announced over 153,000 job cuts, the highest for that month since 2003 and nearly triple September’s total. 2025 job cuts have reached over 1 million, up 44% from all of 2024, with the government and tech sectors leading in layoffs.

U.S. consumer sentiment dropped sharply in November, with the University of Michigan’s index falling to 50.3, its second-lowest level ever. The decline reflects growing concerns over the economic impact of the prolonged government shutdown. People felt worse about their personal finances, and expectations for future business conditions also fell. Confidence weakened across most groups, except for wealthier households with strong stock holdings, which saw a boost. Inflation expectations were mixed, with short-term forecasts rising slightly and long-term ones easing.

Earnings Reports

Palantir

Palantir Technologies (PLTR) reported strong Q3 2025 results, with total revenue up 63%. Also, U.S. commercial revenue surged 121% year over year.

The company raised its full-year guidance, now expecting up to $4.4 billion in revenue and over $1.4 billion from U.S. commercial operations. It closed record-breaking deals and achieved 45% year-over-year customer growth.

Despite the strong performance, Palantir’s stock fell due to AI bubble concerns over high valuation.

Advanced Micro Devices

Advanced Micro Devices (AMD) posted record Q3 2025 revenue of $9.2 billion, up 36% year-over-year, with strong profits and free cash flow.

This growth was driven by high demand for EPYC processors, Ryzen chips, and Instinct AI accelerators. Data center, client, and gaming segments saw major gains, while embedded revenue declined.

AMD announced major AI partnerships with OpenAI and Oracle, and expects Q4 revenue to reach up to $9.6 billion.

Despite strong results and guidance, AMD’s stock fell due to valuation concerns and cautious market sentiment around tech and AI stocks.

Shopify

Shopify (SHOP) reported strong Q3 2025 results, with revenue up 32% and an 18% free cash flow margin. This is its ninth straight quarter of double-digit free cash flow.

The company expects continued growth in Q4, with projected revenue rising 25–30% year over year.

Despite solid performance, the stock fell over concerns about valuation and market sentiment.

Qualcomm

Qualcomm (QCOM) reported strong Q4 and full-year 2025 results, with $44.3 billion in revenue and earnings beating estimates.

Its QCT division hit record highs, with non-Apple revenue up 18% and Automotive/IoT up 27%.

The company expects up to $12.6 billion in Q1 revenue and solid earnings per share.

Despite strong performance, Qualcomm’s stock dipped after warning it may lose business from Samsung, which tempered investor enthusiasm.

Indices

Indices’ Weekly Performance:

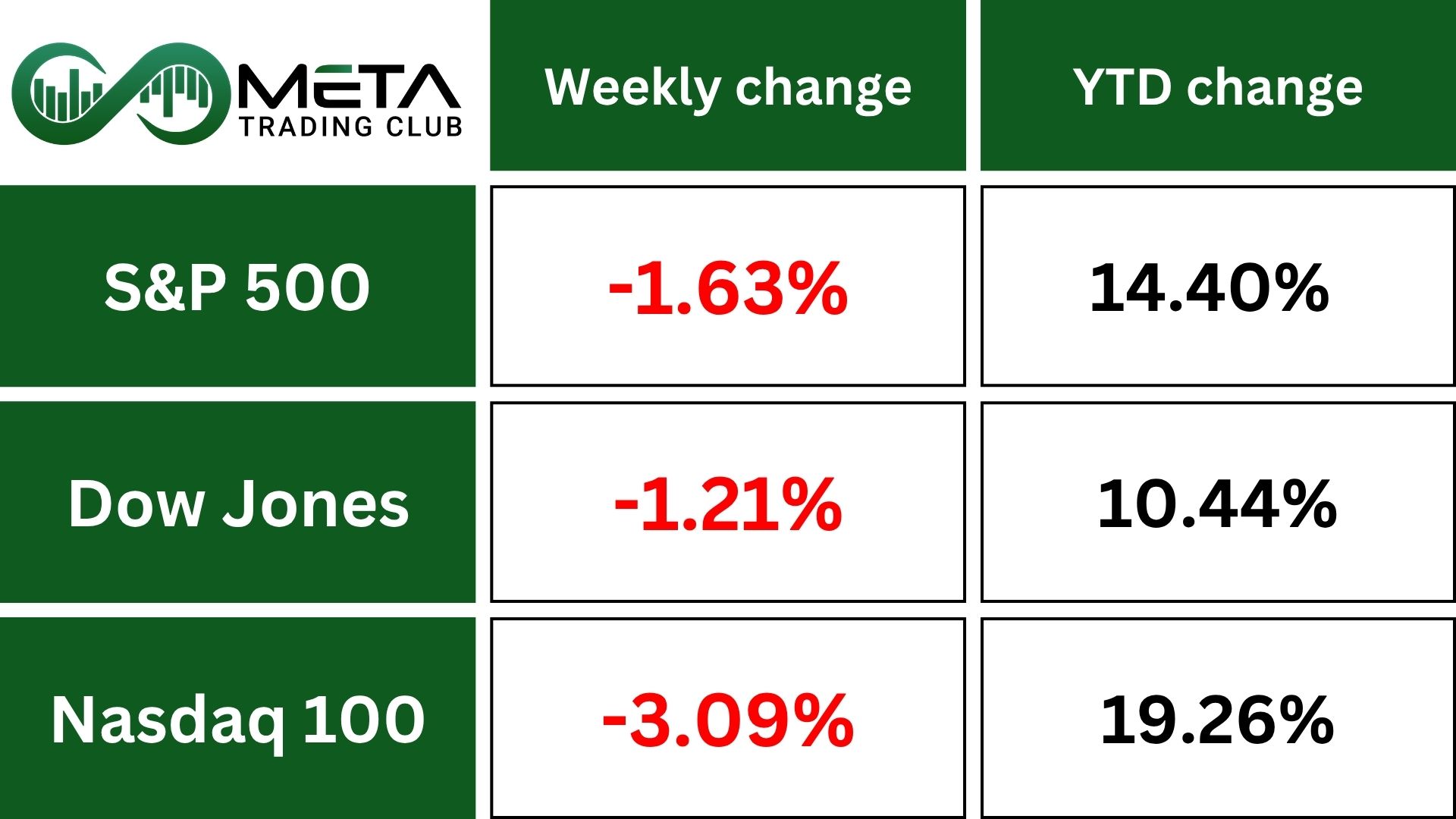

The Nasdaq posted its biggest weekly drop since April, falling about 3% as investors grew cautious about the recent AI-driven rally.

Tech and chip stocks led the decline, partly due to concerns raised by Nvidia’s CEO about China overtaking the U.S. in AI. Some of the weakness was also seen as profit-taking after strong gains since April.

While all major U.S. indexes were down last week.

After recently surging to all-time highs, the S&P 500 (SPX) has entered a mild corrective phase. It has now filled both of the late October gaps and closed below its initial support level at 6,750. However, this move doesn’t signal a major breakdown.

The next key support lies between 6,500 and 6,550, a zone that has held firm in previous tests. A break below this range could shift the outlook to significantly more bearish.

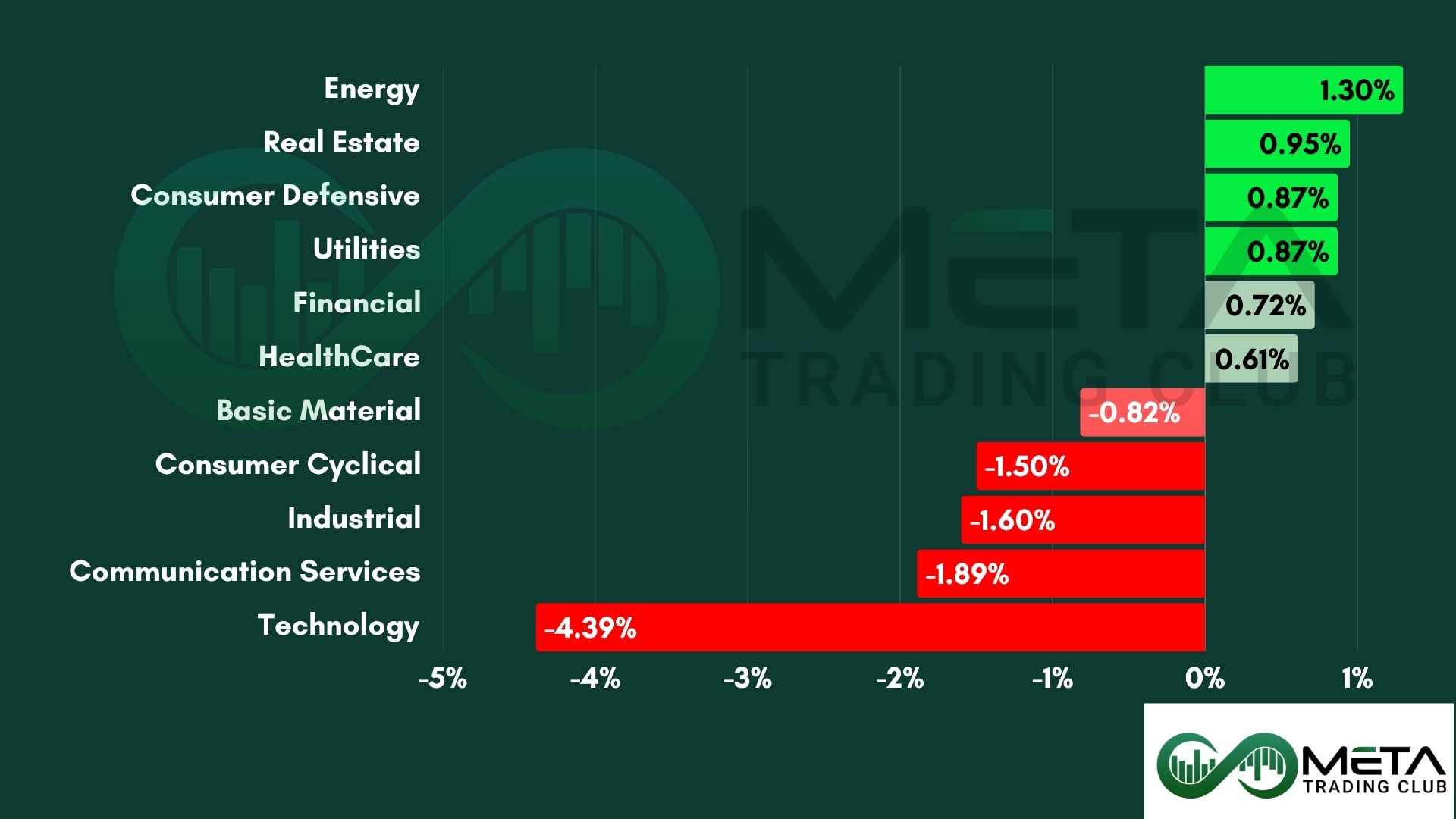

Stocks

Sector’s Weekly Performance:

U.S. stocks broke a three-week winning streak as worries over high valuations and limited economic data from the government shutdown led to profit-taking.

Earnings season has been strong so far, with 82.5% of S&P 500 companies beating expectations, well above the recent average of 77%. The overall earnings surprise rate is 10.3%, the highest since mid-2021 and far above the long-term average. Revenue growth has also been solid, currently at 8.1% year-over-year.

Tech-heavy markets faced their biggest weekly drop in seven months as investors questioned the strength of the AI stock rally. The technology sector dropped over 4% last week.

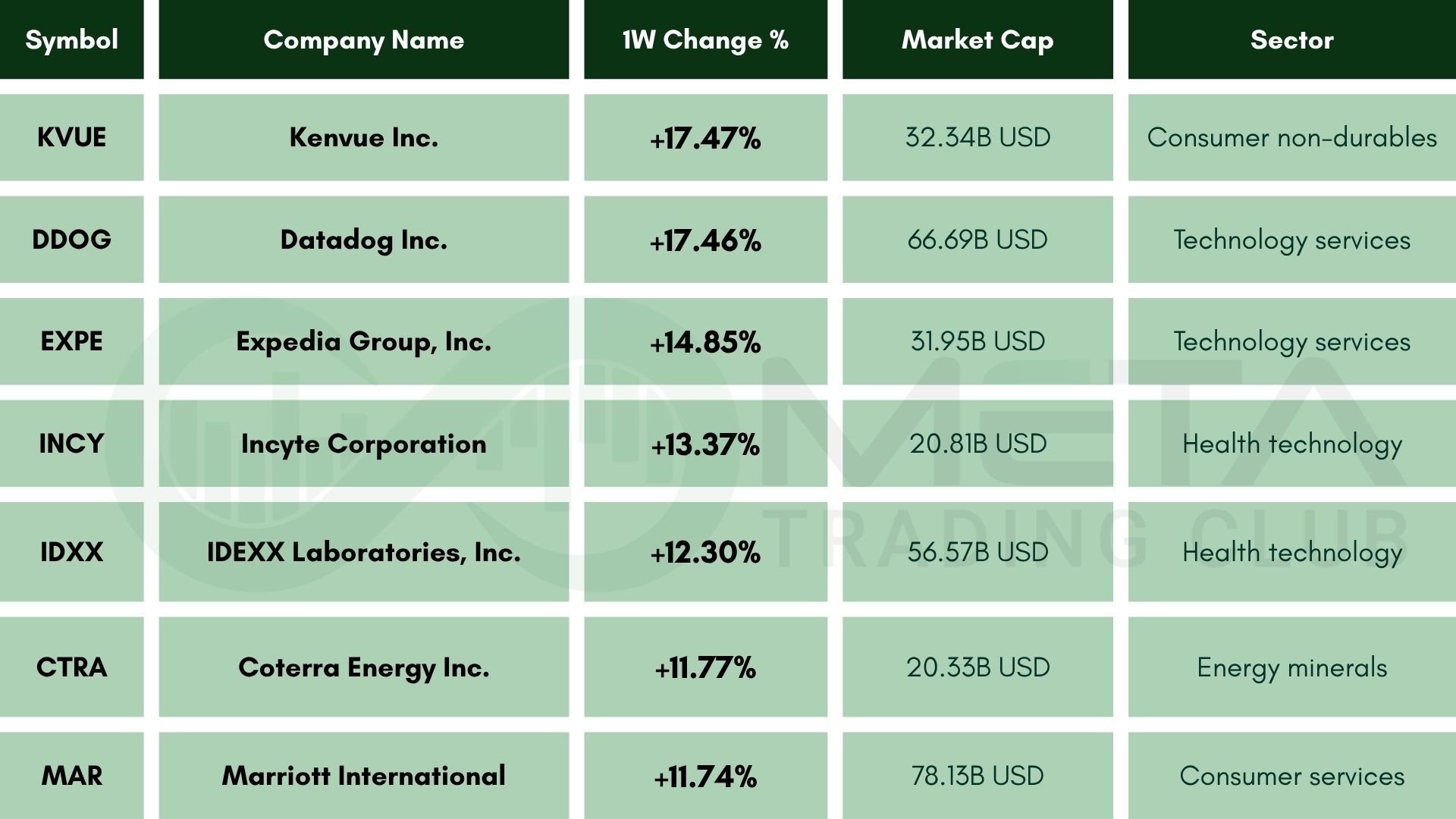

Top Performers

Last week saw a remarkable stock market performance, with several companies standing out as top gainers:

- Kenvue (KVUE): Surged 17.47% due to strong Q3 earnings and raised guidance.

- Datadog (DDOG): Advanced 17.46% after beating Q3 earnings expectations and raising full-year guidance, driven by strong cloud monitoring services.

- Expedia (EXPE): Soared 14.85% on robust travel demand and better-than-expected Q3 results.

- Incyte (INCY): Gained 13.37% following positive clinical trial updates and investor confidence in its oncology pipeline

- IDEXX Laboratories (IDXX): Rose 12.30% due to strong Q4 earnings, EPS growth of 13%.

- Coterra Energy (CTRA): Up 11.77% as investors rotated into undervalued energy stocks with strong free cash flow and dividend yield.

- Marriott (MAR): Gained 11.74% on record occupancy rates and strong international travel recovery, especially in Asia-Pacific and Europe.

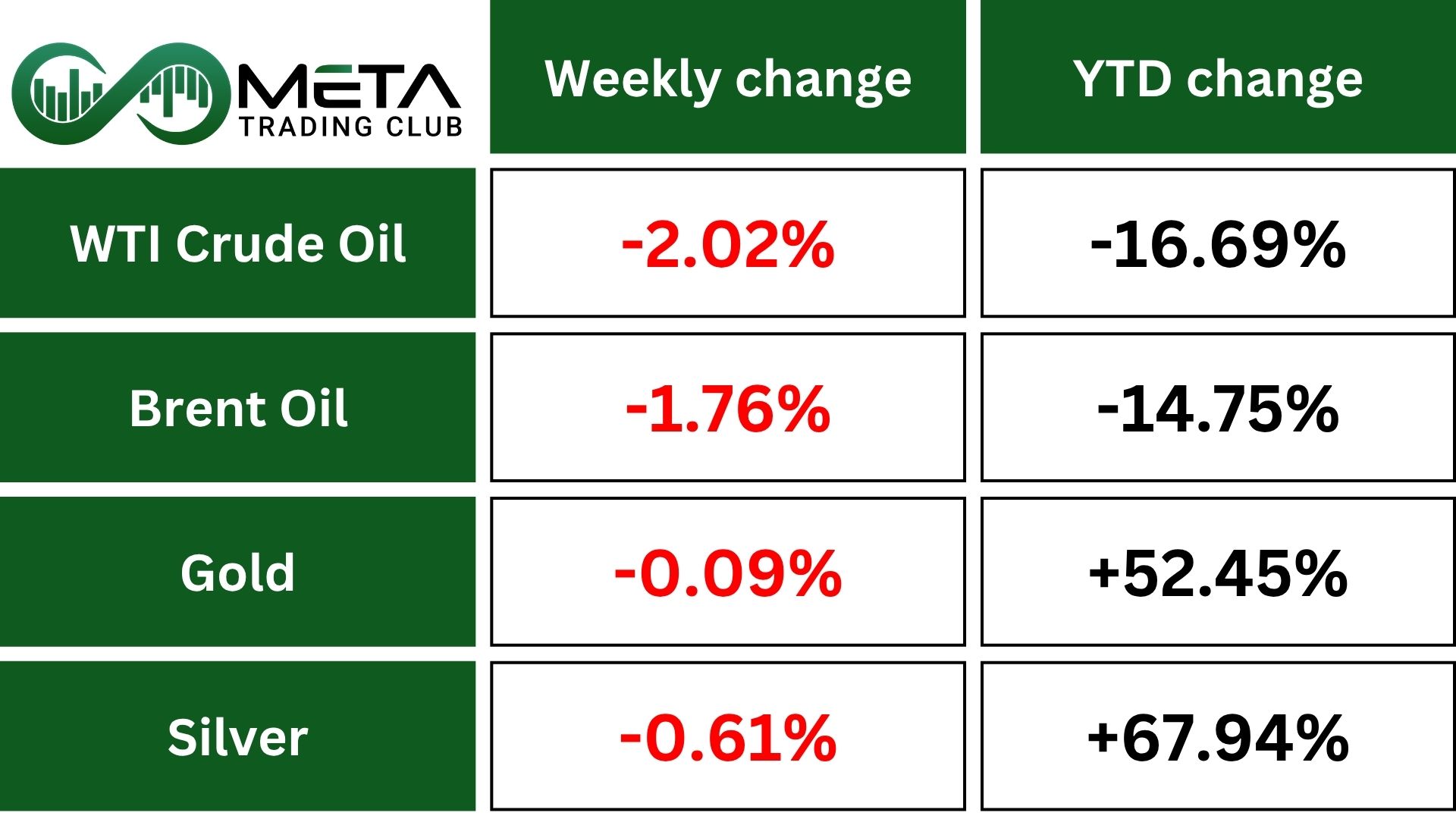

Commodity

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Gold prices are rising again after a two-week pause. Front-month gold ended the week up 0.4%, helped by a 0.5% gain on Friday.

Gold and silver prices may be stabilizing, with gold remaining a popular safe-haven during uncertain times and low interest rates.

Due to the government shutdown, traders relied on private data showing October job losses to assess the chance of a Fed rate cut, now seen as 66% likely in December. Meanwhile, China is revising its rare earth export rules, but full trade restrictions are expected to stay.

Crude oil ended the week lower as OPEC+ announced it will pause easing production cuts early next year.

Ukrainian attacks on Russian oil sites lifted diesel prices, giving crude some support. Still, worries about oversupply remain.

Forex

Weekly Performance of Major Foreign Exchange Pairs:

Dollar Index (DXY) ended the week mostly flat as investors weighed the Fed’s cautious stance against ongoing economic concerns. The U.S. labor data which weakened the greenback after a strong run the previous week. Uncertainty around the December Fed meeting also added pressure.

The euro’s weekly gain against the dollar came from expectations that the European Central Bank will keep rates steady, while markets anticipate further rate cuts in the U.S. and U.K. in 2026. This policy divergence gave the euro some support.

The dollar’s weekly drop against the yen reflected renewed demand for safe-haven assets, with the yen regaining its role as the market’s preferred defensive currency.

With limited data available, markets are reacting strongly to any labor signals, and a December rate cut remains unlikely unless conditions worsen.

Crypto

Bitcoin stays just above $100K after being pushed back from $116K. Price swings have slowed, but the trend looks shaky.

Buyers haven’t stepped in strongly yet, and with open interest dropping, the market is staying cautious. If BTC breaks $100K, then there is a chance for further drops.

Next Week’s Outlook

Economic Events

The government shutdown, now the longest in the nation’s history, is expected to persist, once again restricting the release of economic data and delaying key indicators such as the Consumer Price Index (CPI).

With limited data available, investors are likely to focus on the upcoming ADP employment report for insights into a labor market that has been showing signs of a marked slowdown.

The NFIB Small Business Optimism Index is also scheduled for release and is anticipated to reflect weaker sentiment.

Meanwhile, remarks from Federal Reserve officials will be closely monitored for additional guidance on potential policy actions in December.

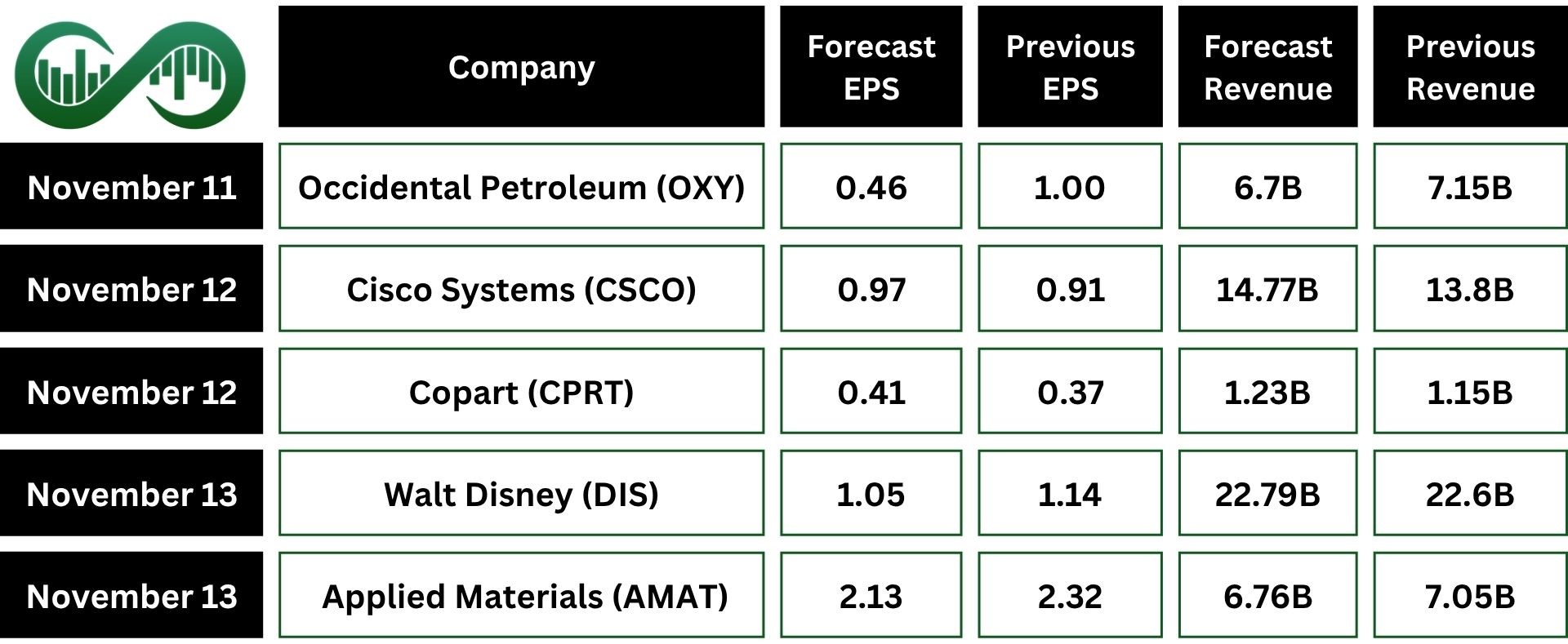

Earnings Events

As the earnings season draws to a close, several notable companies, including Cisco Systems (CSCO), Walt Disney (DIS), and Applied Materials (AMAT), are still scheduled to report their quarterly results next week.