Last Week’s report

Economic Reports

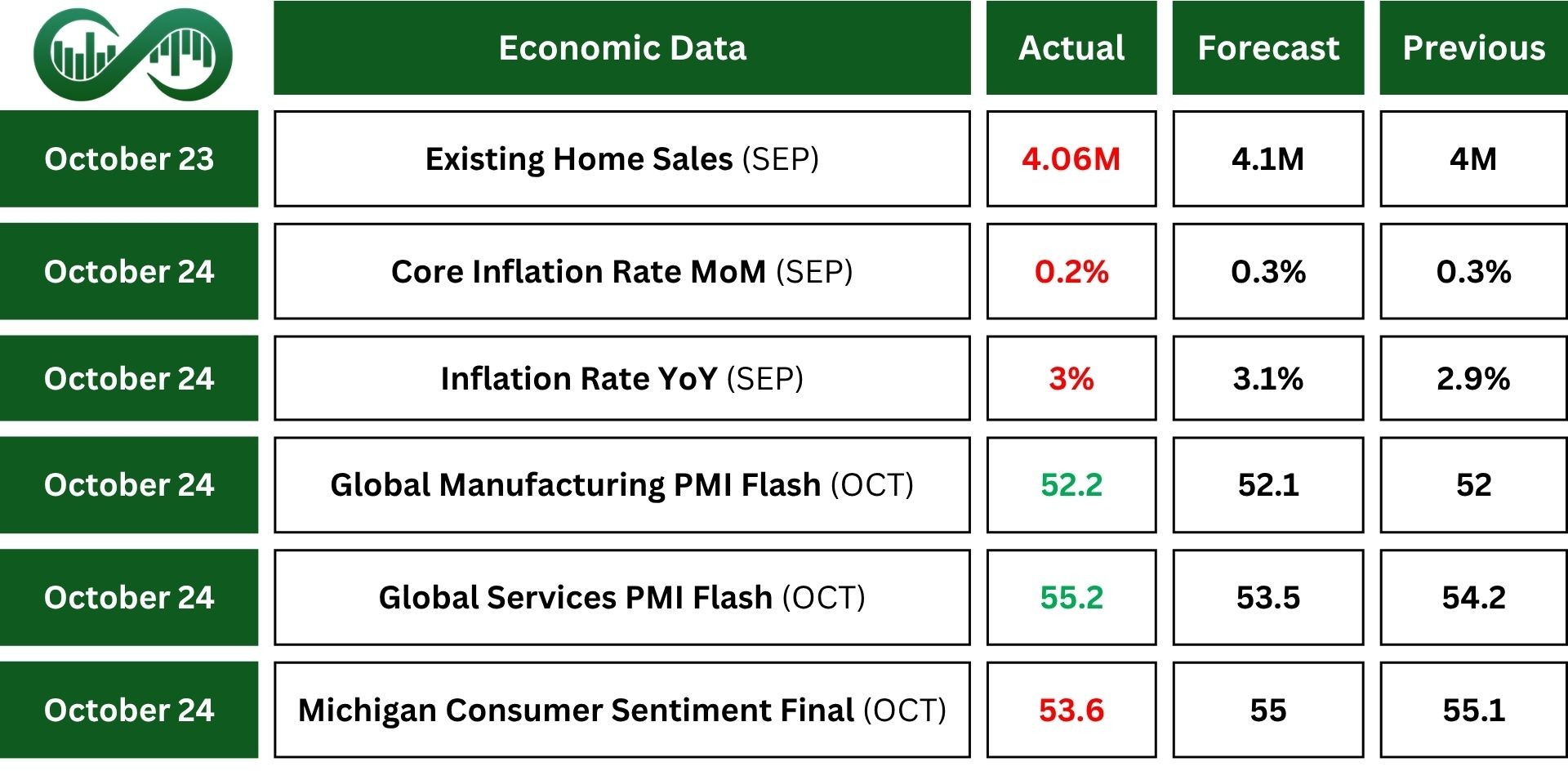

U.S. CPI inflation rose to 3% in September 2025, slightly up from August but below expectations. Energy prices jumped, especially fuel oil. New vehicle prices edged up, but food, used cars, and transportation services saw slower increases.

Core inflation, which excludes food and energy, actually eased to 3%. On a monthly basis, overall prices rose 0.3%, mainly due to a 4.1% rise in gasoline, while core prices increased just 0.2%.

Michigan consumer sentiment fell to 53.6 in October, the lowest in five months. Views on current conditions and future expectations both dropped. Inflation expectations for the next year dipped slightly to 4.6%, while the five-year outlook rose to 3.9%. People feel their personal finances are mostly unchanged, with inflation and high prices still a major concern. Most don’t see a link between the government shutdown and the economy.

U.S. services activity picked up in October, with the Services PMI rising to 55.2, its second-fastest growth this year. Strong domestic demand boosted new orders and hiring, even as firms struggled to find qualified workers. Input costs rose due to higher wages and tariffs, but companies raised prices more slowly. Despite the growth, business confidence about future output declined.

President Trump announced a 10% increase in tariffs on Canada, reacting to an ad from Ontario that aired during the World Series.

He had already ended trade talks with Ottawa on Thursday, calling the ad misleading. Ontario Premier Doug Ford said the ad campaign would pause on Monday after talks with Prime Minister Mark Carney, in hopes of restarting negotiations. U.S. and Canadian officials have not yet commented.

Earnings Reports

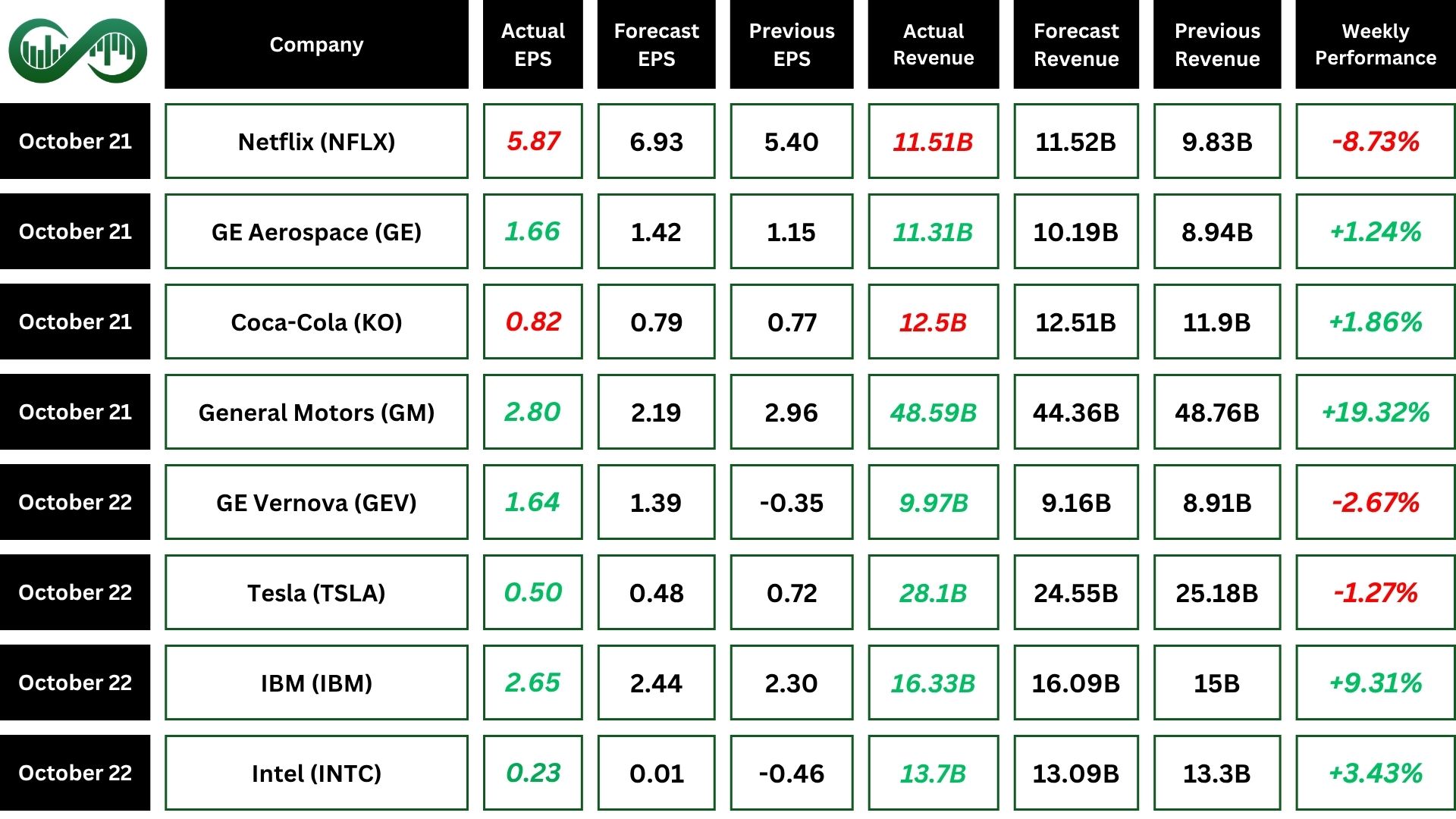

Tesla

Tesla (TSLA) reported Q3 revenue of $28.1 billion, up 12% year-over-year, beating forecasts despite a 37% drop in net income to $1.4 billion, its fourth straight quarter of declining profits.

The company saw a temporary sales boost from customers rushing to claim a $7,500 EV tax credit before its October 1 expiration, which may have pulled forward demand.

Automotive revenue rose 6%, energy storage jumped 44%, and free cash flow surged 46% to $3.99 billion.

Tesla also launched new vehicle models and energy products, while expanding its AI-powered services. Despite strong operational metrics, there are concerns over profitability, rising costs, and uncertain Q4 momentum.

General Motors

General Motors (GM) posted stronger-than-expected Q3 results, with adjusted earnings of $2.80 per share and $48.59 billion in revenue, beating forecasts despite a slight year-over-year dip.

However, EBIT-adjusted fell 18% to $3.38 billion due to $1.59 billion in EV-related charges and $300 million tied to OnStar investigations.

GM Financial performed well, with earnings before taxes up 17%. The company raised its full-year EPS guidance to $9.75–$10.50 and boosted its free cash flow forecast to $10–$11 billion.

GM shares surged over 19% on the upbeat earnings and improved outlook, despite challenges in its EV strategy.

Intel

Intel (INTC) reported stronger-than-expected Q3 results with $13.7 billion in revenue and $0.90 GAAP EPS, driven by solid operational cash flow and strategic momentum.

The company secured $8.9 billion in U.S. government funding, received major investments from NVIDIA and SoftBank, and unveiled new AI-focused products including Panther Lake processors and next-gen Xeon and GPU platforms.

Intel also expanded partnerships with Microsoft and made Fab 52 in Arizona fully operational. Despite forecasting a modest Q4 with a GAAP loss, the stock rose as investors welcomed its AI roadmap, manufacturing scale-up, and long-term growth outlook.

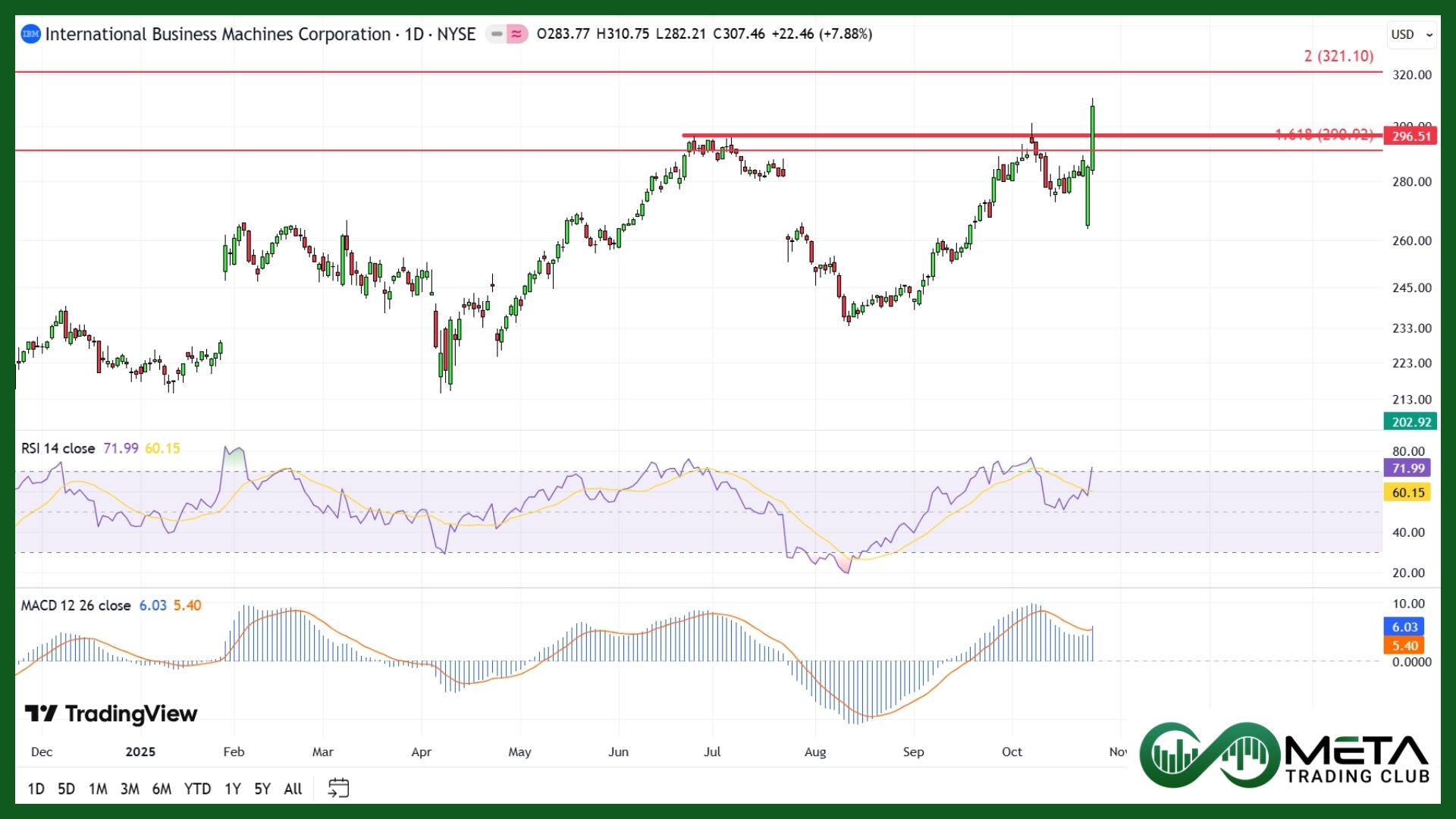

IBM

IBM (IBM) delivered strong Q3 results, with revenue up 9.1% year-over-year to $16.33 billion and non-GAAP EPS of $2.65, both beating expectations.

Growth was driven by robust infrastructure demand, especially a 61% surge in IBM Z, and rising interest in AI.

Software and consulting segments also posted gains, while transaction processing dipped slightly.

IBM raised its full-year outlook for revenue and free cash flow, now projected at $14 billion.

Indices

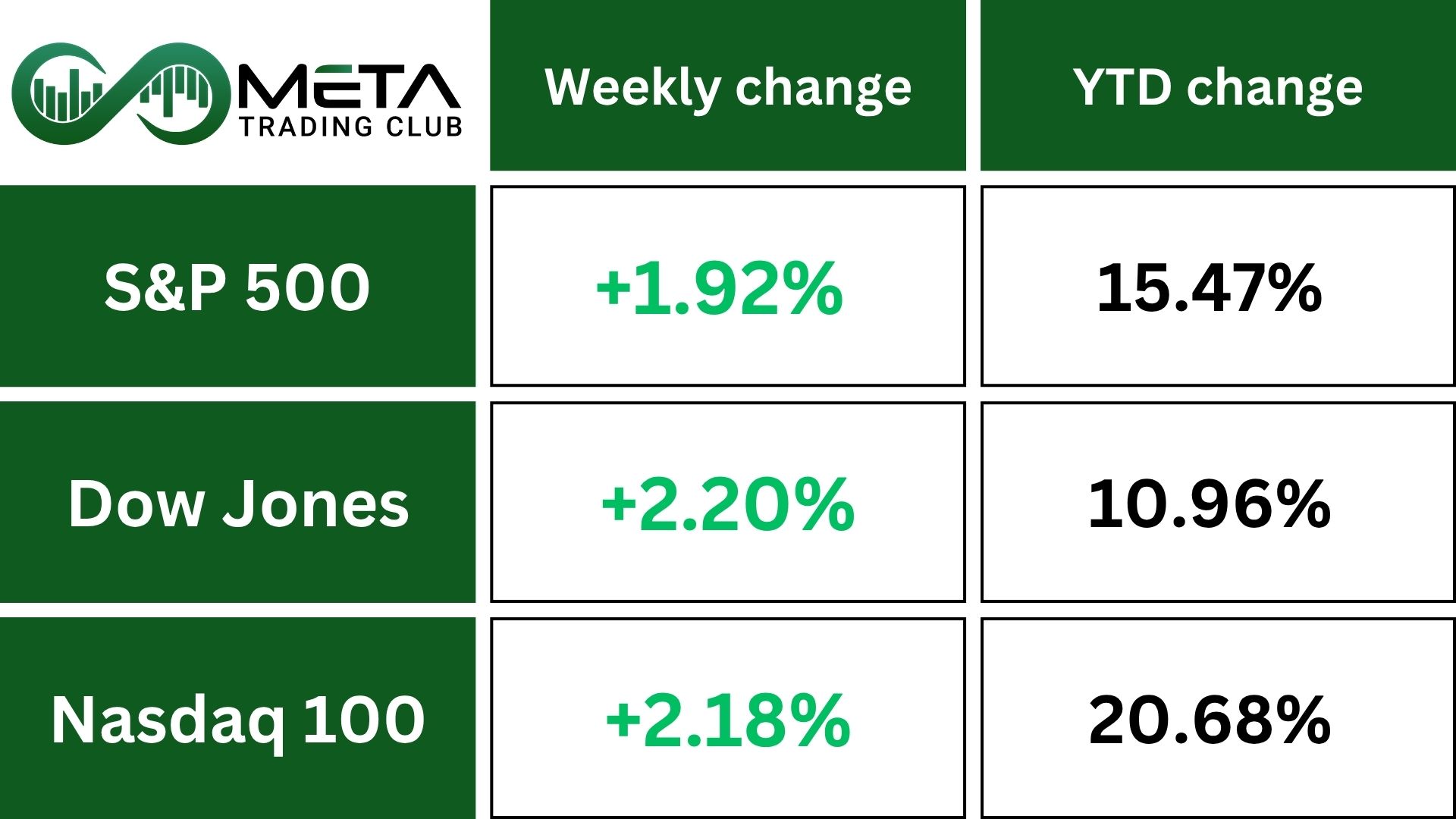

Indices’ Weekly Performance:

Wall Street ended the week on a high note, with the S&P 500, Nasdaq, and Dow all posting record closing highs.

The rally was fueled by a softer-than-expected September inflation report and upbeat tech news.

The Nasdaq led the charge, notching its 33rd record close of the year, while the Dow hit its 13th record in 2025 and closed above the 47,000 mark for the first time.

Stocks

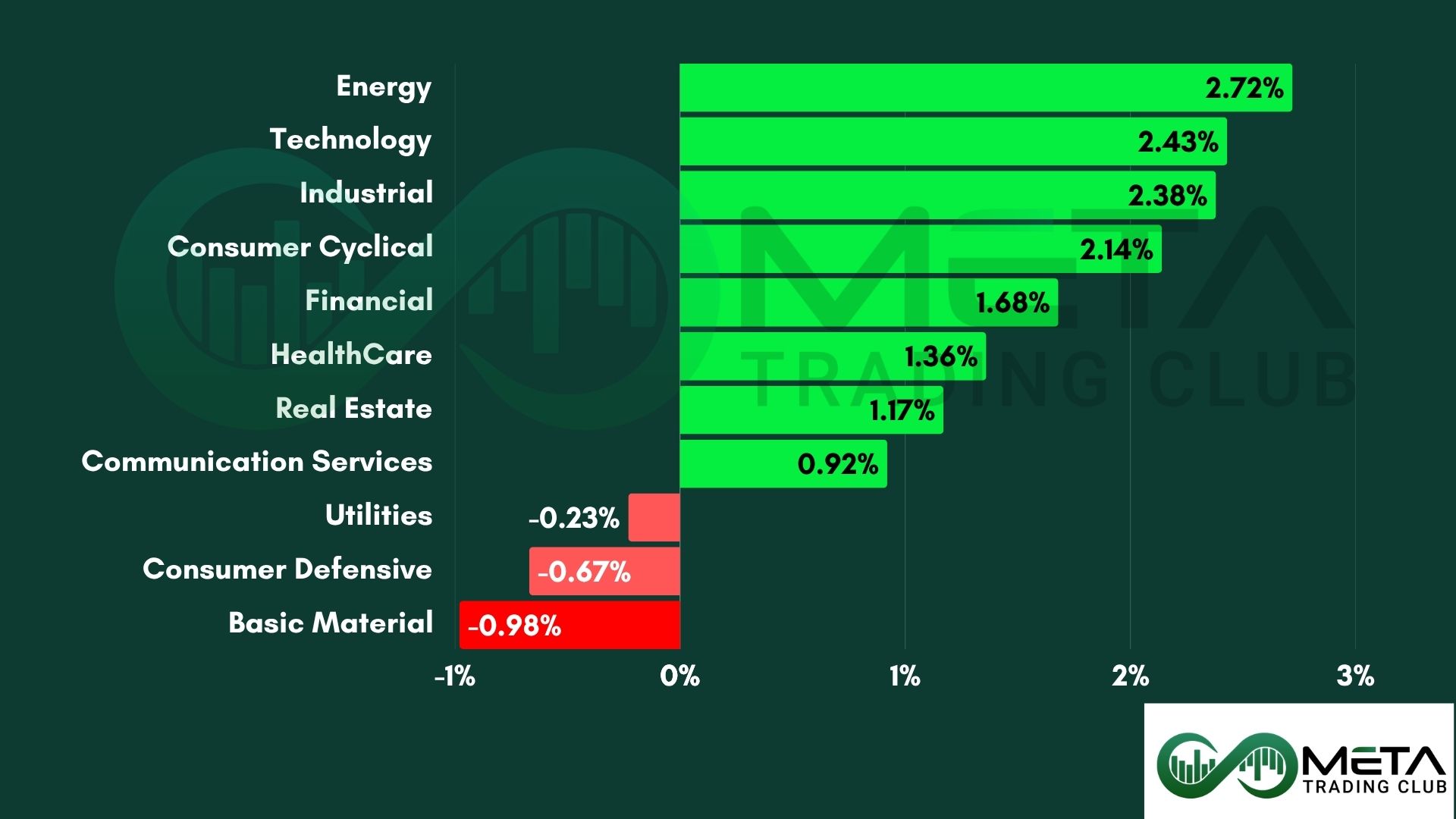

Sector’s Weekly Performance:

Markets posted solid gains across most sectors last week, with investor sentiment buoyed by strong earnings, easing inflation concerns, and resilient economic data.

- Energy (+2.72%) Led the pack as oil prices rebounded and earnings from major players like Exxon Mobil and Chevron impressed. Tariff-related cost pressures also contributed to rising input prices, boosting margins.

- Technology (+2.43%) Fueled by Intel’s earnings beat and anticipation around upcoming reports from Apple, Microsoft, and other tech giants. Semiconductor stocks surged, with the SOX index hitting a record high.

- Financial (+1.1), supported by stable rate expectations and solid earnings.

- Communication Services (+0.92%) Mixed results from Netflix and other media players capped gains. Anticipation builds around Alphabet and Meta earnings

- Consumer Defensive (-0.67%) Despite Procter & Gamble’s strong quarter, broader staples underperformed as investors rotated into growth sectors.

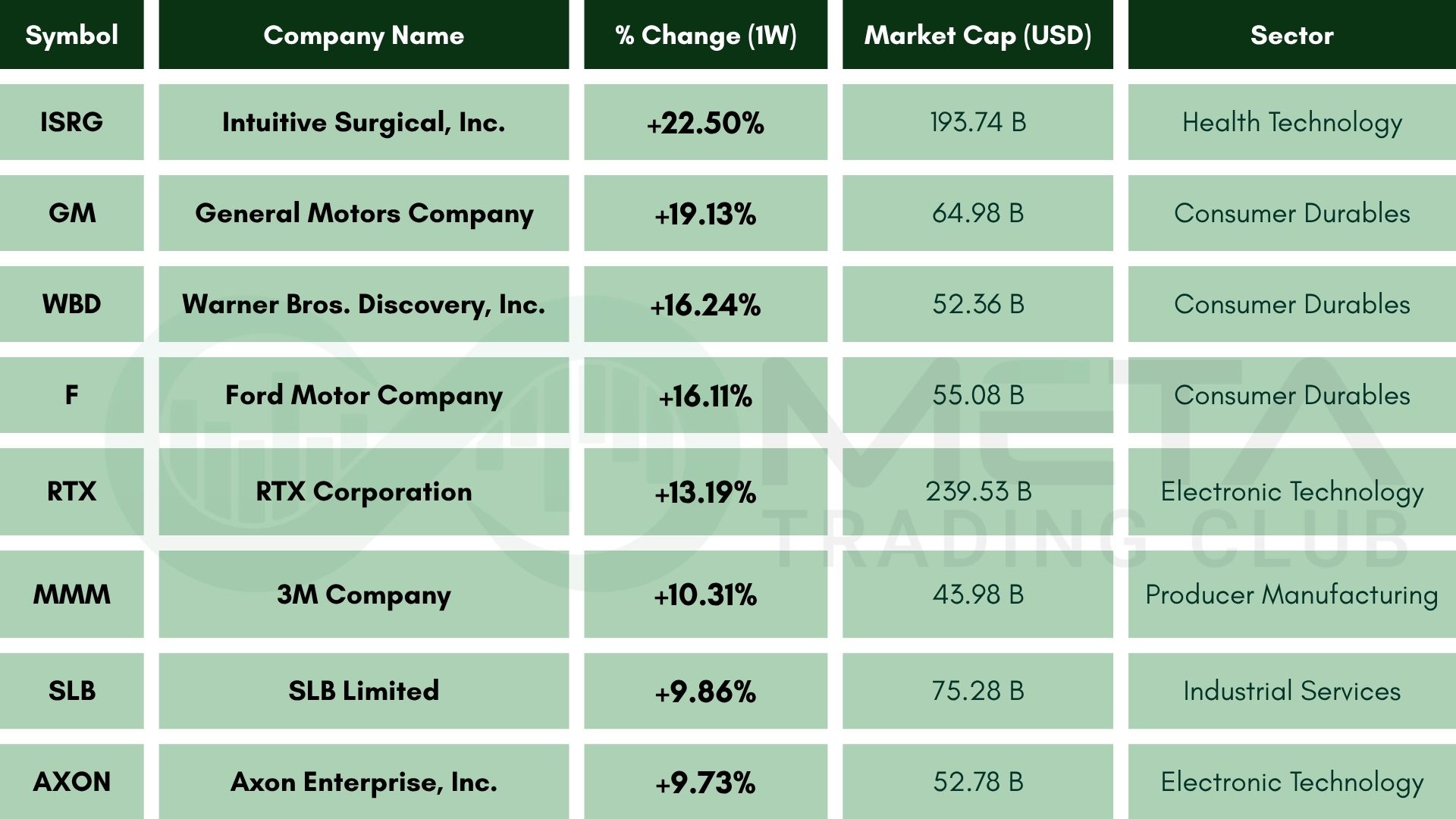

Top Performers

Last week saw a remarkable stock market performance, with several companies standing out as top gainers:

- Intuitive Surgical (ISRG): Surged 22.5% due to beating Q3 earnings estimates with revenue of $2.51B and EPS of $2.40, driven by a 20% increase in global procedures and strong demand for its da Vinci systems.

- General Motors (GM): Jumped 19.3% after posting stronger-than-expected Q3 earnings, with EPS of $2.80 and revenue of $48.6B. The rally was fueled by resilient truck sales and renewed confidence in its EV strategy.

- Warner Bros. Discovery (WBD): Rose 18.6% as investors responded to streaming price hikes and strategic restructuring. Positive signals around subscriber growth and profitability boosted sentiment.

- Ford Motor Company (F): Gained 16.1% following record Q3 revenue of $50.5B and EPS of $0.45. Strong hybrid and truck sales helped offset labor-related disruptions.

- RTX Corporation (RTX): Climbed 13.95% after announcing a strategic overhaul and reporting solid Q3 results. Strength in its aerospace and defense segments supported the rebound.

- 3M Company (MMM): Advanced 13.0% on better-than-expected Q3 earnings, with adjusted EPS of $2.19. Progress in resolving legal liabilities and cost efficiencies lifted investor confidence.

- SLB Limited (SLB): Rose 12.4% as oil prices stabilized and global drilling activity remained strong. The company’s international exposure and tech leadership in energy services drove the rally.

- Axon Enterprise (AXON): Gained 9.6% on rising demand for law enforcement tech and cloud-based solutions. Strong adoption of TASER 10 and new AI partnerships fueled optimism.

- Shopify (SHOP): Increased 9.4% on momentum from strong merchant growth and improved profitability. Anticipation of a robust holiday season and new product rollouts supported the surge.

- IBM (IBM): Up 9.3% after beating Q3 earnings and raising full-year guidance. Growth in hybrid cloud and AI services continues to drive enterprise adoption.

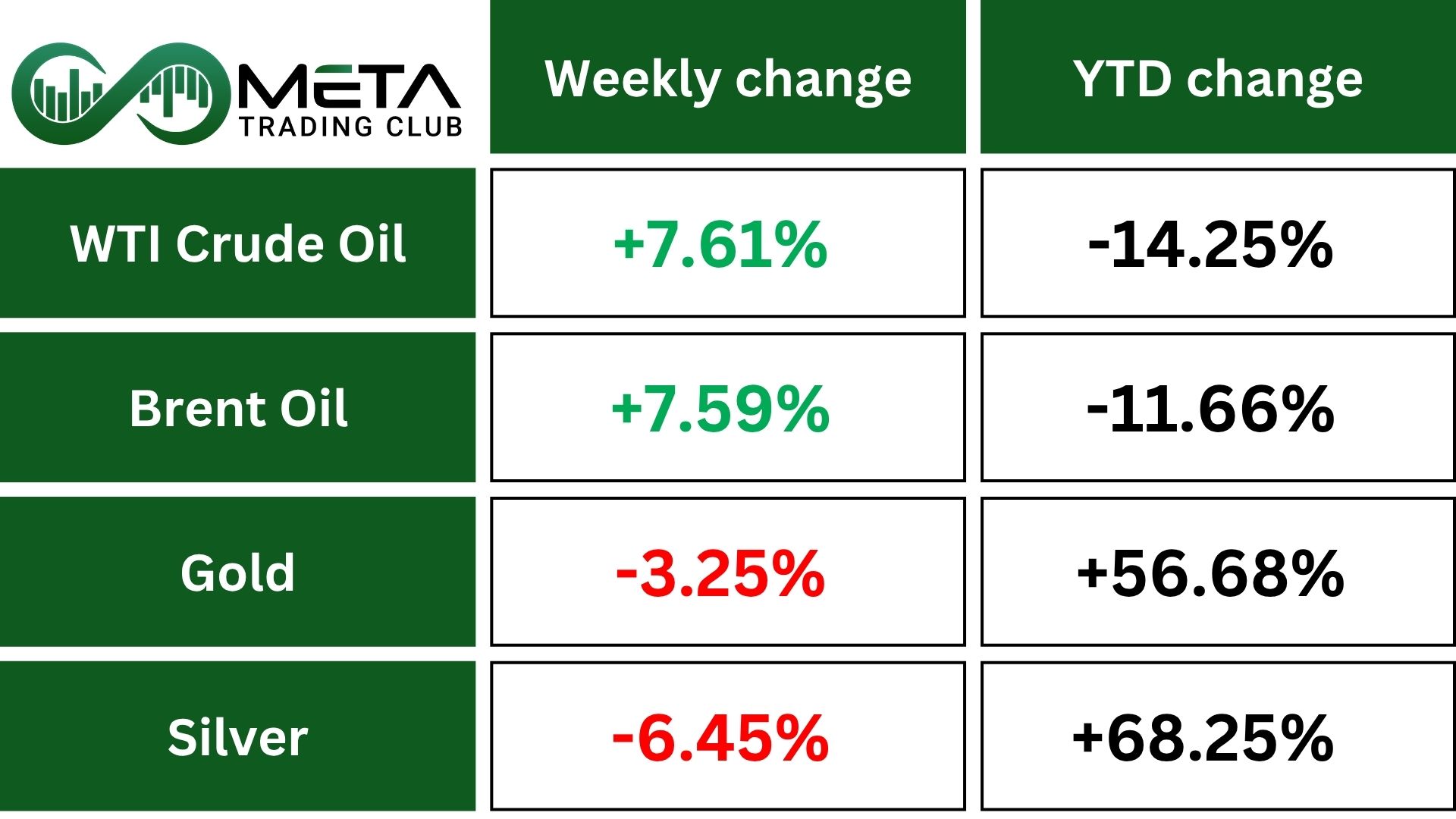

Commodity

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Gold

Gold prices fell, ending a nine-week winning streak after heavy selling and a 5% drop earlier in the week. The decline was linked to large withdrawals from gold ETFs.

Despite the pullback, gold is still up 55% year-to-date, supported by trade tensions, U.S. sanctions on Russia, and expectations of more Fed rate cuts. Investors now await the CPI report, which could impact the Fed’s next move.

Oil

Crude oil prices surged over 7% following new U.S. sanctions on Russian energy giants Rosneft and Lukoil. The sanctions, aimed at pressuring Moscow over its war in Ukraine, raised concerns about tighter global supply and disrupted trade flows, driving crude sharply higher.

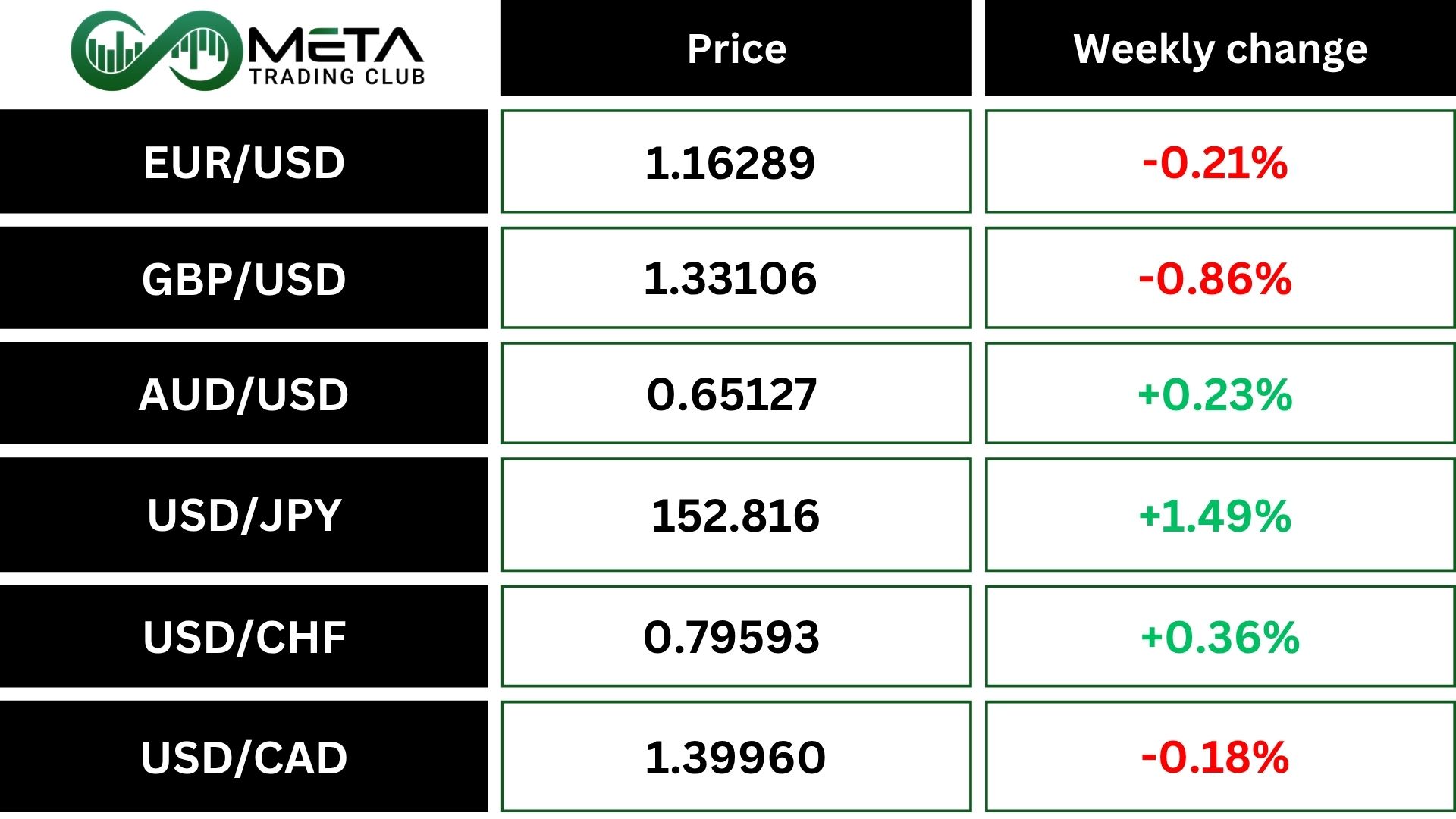

Forex

Weekly Performance of Major Foreign Exchange Pairs:

Dollar Index (DXY): The U.S. dollar index dipped slightly on Friday. Despite the pullback, it remained on track for a modest weekly gain. The decline followed a softer-than-expected CPI report, which reinforced expectations of Federal Reserve rate cuts in both November and December. Notably, the inflation data was released despite a government shutdown, as it’s used to calculate Social Security cost-of-living adjustments.

USD/JPY: The Japanese yen weakened against U.S. dollar, down for the week, as markets reacted to Prime Minister Sanae Takaichi’s dovish stance and plans for a stimulus package exceeding last year’s $92 billion. Despite core inflation staying above 2%, expectations for a near-term rate hike remain uncertain.

GBP/USD: The British pound fell about 1% for the week, as soft inflation data fueled speculation of a Bank of England rate cut, despite strong retail sales driven by gold demand.

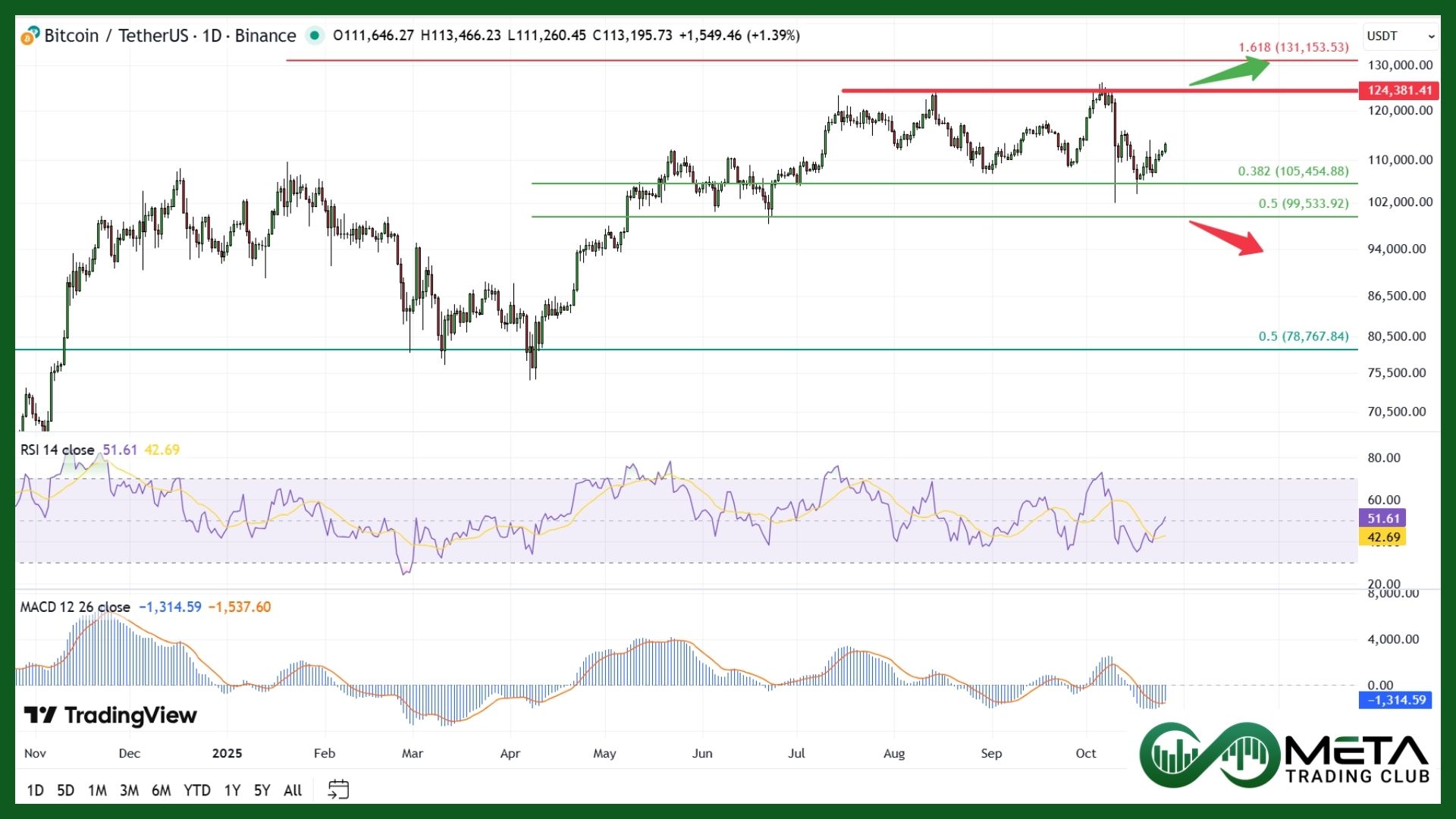

Crypto

Trade tensions between the U.S. and China are easing, which is boosting Bitcoin and Ethereum. Bitcoin hit $113,851 and Ether nearly reached $4,100. Earlier this month, markets dropped sharply after the U.S. announced 100% tariffs, causing a record $19 billion in crypto liquidations.

Now, after high-level talks at the ASEAN summit, the U.S. is delaying those tariffs and China is postponing rare earth metal restrictions. This has sparked hope that a full trade deal may be on the way.

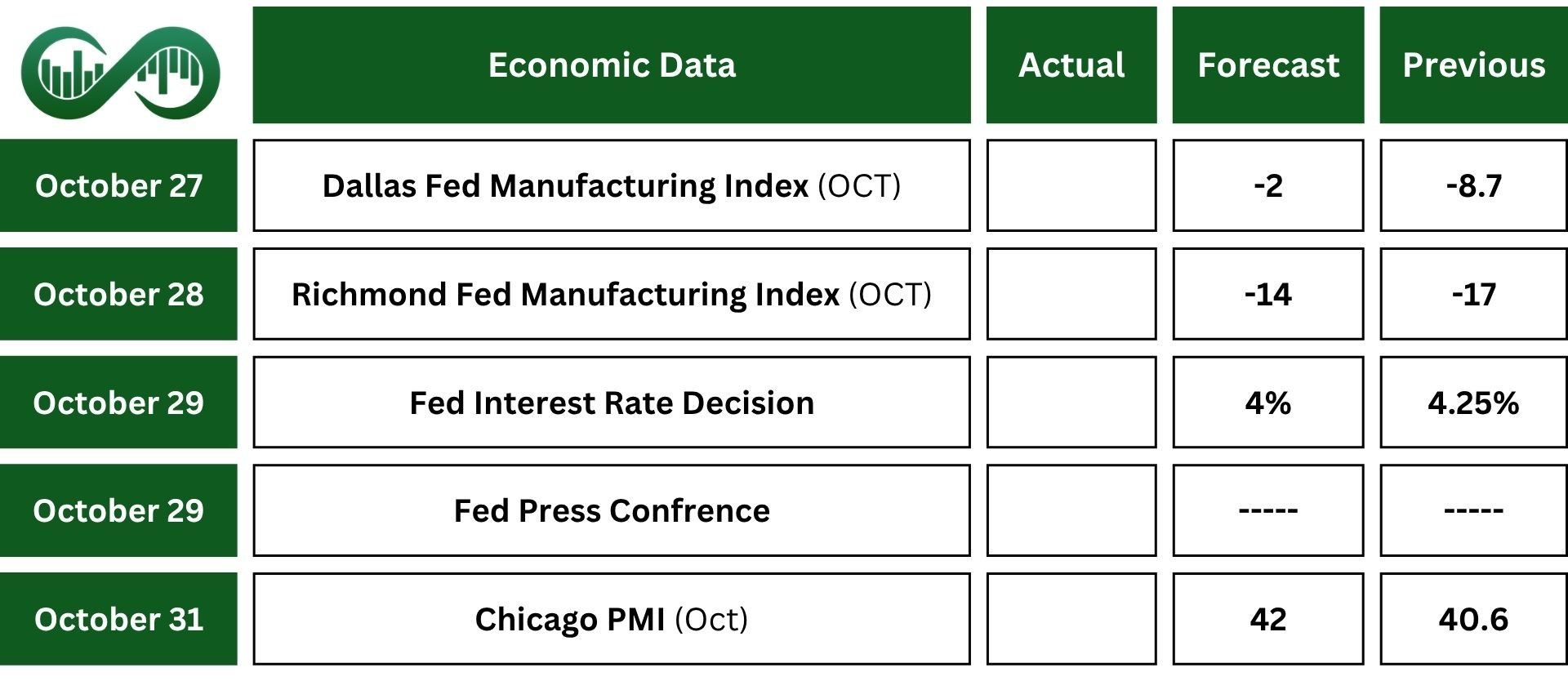

Next Week’s Outlook

Economic Events

This week, all eyes will be on the Federal Reserve, with markets expecting another 25 basis point rate cut, bringing the federal funds rate down to a target range of 3.75% to 4%.

At the same time, the government shutdown, now the second-longest in U.S. history, is likely to drag on into next week with no clear end in sight.

Despite the uncertainty, we will still have some key data to digest, including regional Fed manufacturing and services indexes (Dallas and Richmond), Case-Shiller home prices, pending home sales, and the Chicago PMI.

Earnings Events

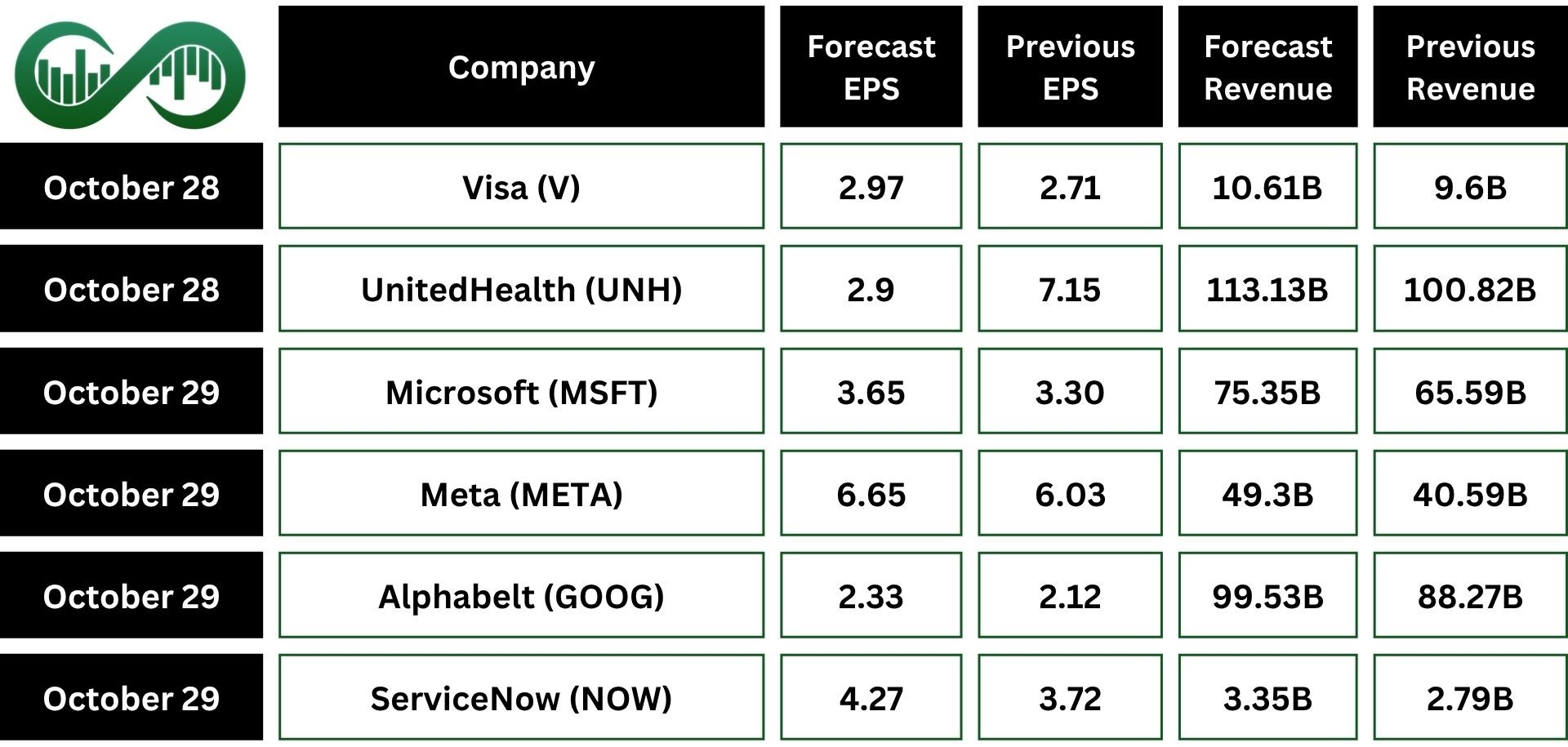

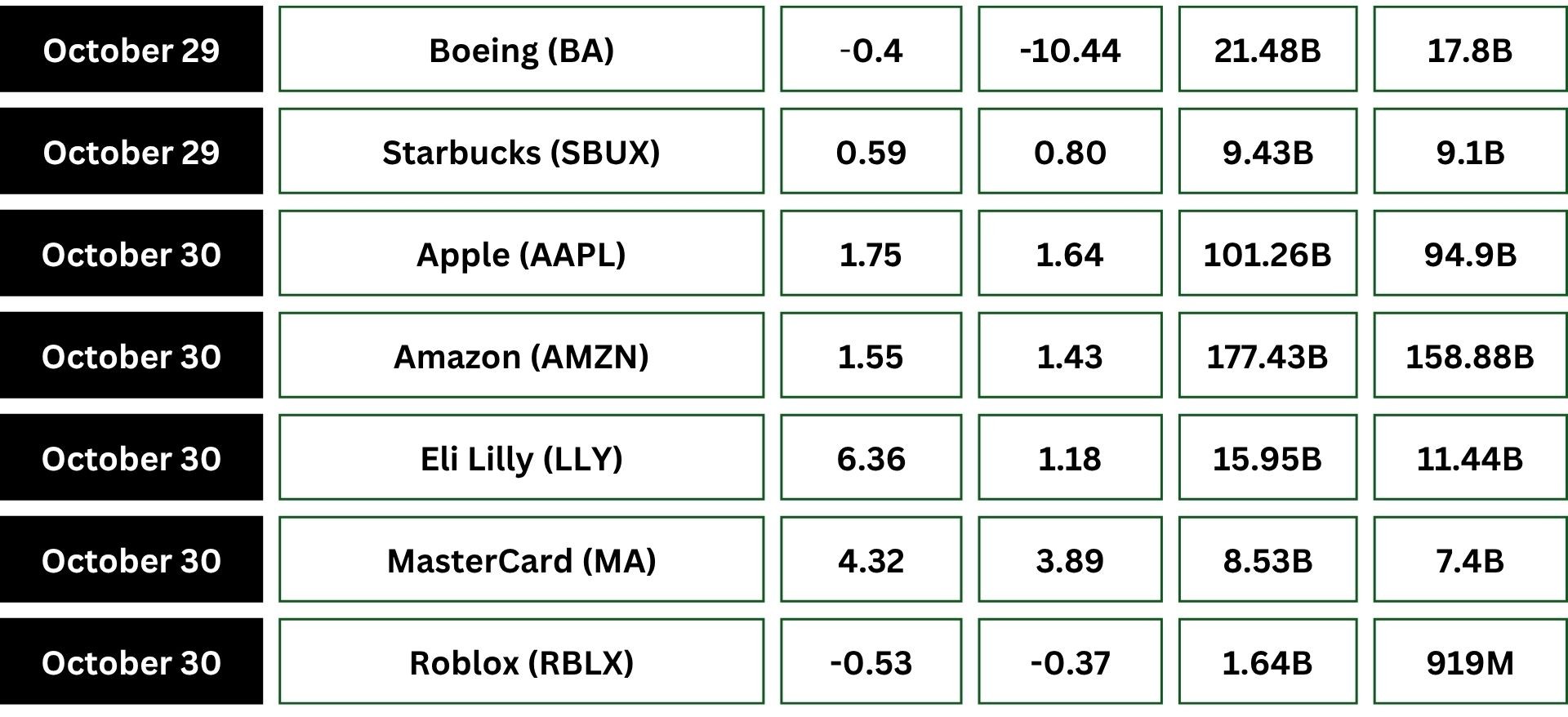

Earnings season hits a critical point this week. More than 170 names are scheduled to report.

Major tech companies, including Microsoft (MSFT), Apple (AAPL), Amazon (AMZN), Meta (META), and Alphabet (GOOG), are in the spotlight.

Other key reports are expected from Visa (V), UnitedHealth Group (UNH), NextEra Energy, Booking, Caterpillar (CAT), Verizon (VZ), Boeing (BA), Eli Lilly (LLY), Mastercard (MA), Merck (MRK), Exxon Mobil, AbbVie, and Chevron.