Last Week’s report

Economic Reports

Federal Reserve Chair Jerome Powell noted that recent data shows the U.S. job market is slowing, with fewer hires and layoffs. Economic conditions remain similar to September, but risks in the labor market have significantly increased, justifying the Fed’s September rate cut.

Powell emphasized that monetary policy effects now appear with longer delays, and it’s too early to fully assess the impact of recent decisions. He also warned that trade tariffs could lead to persistent inflation and cautioned against acting too quickly, which could leave inflation control incomplete.

Powell expressed concern over the ongoing federal government shutdown, which has halted key macroeconomic data releases. This lack of visibility makes it harder for the Fed to evaluate the economy and labor market.

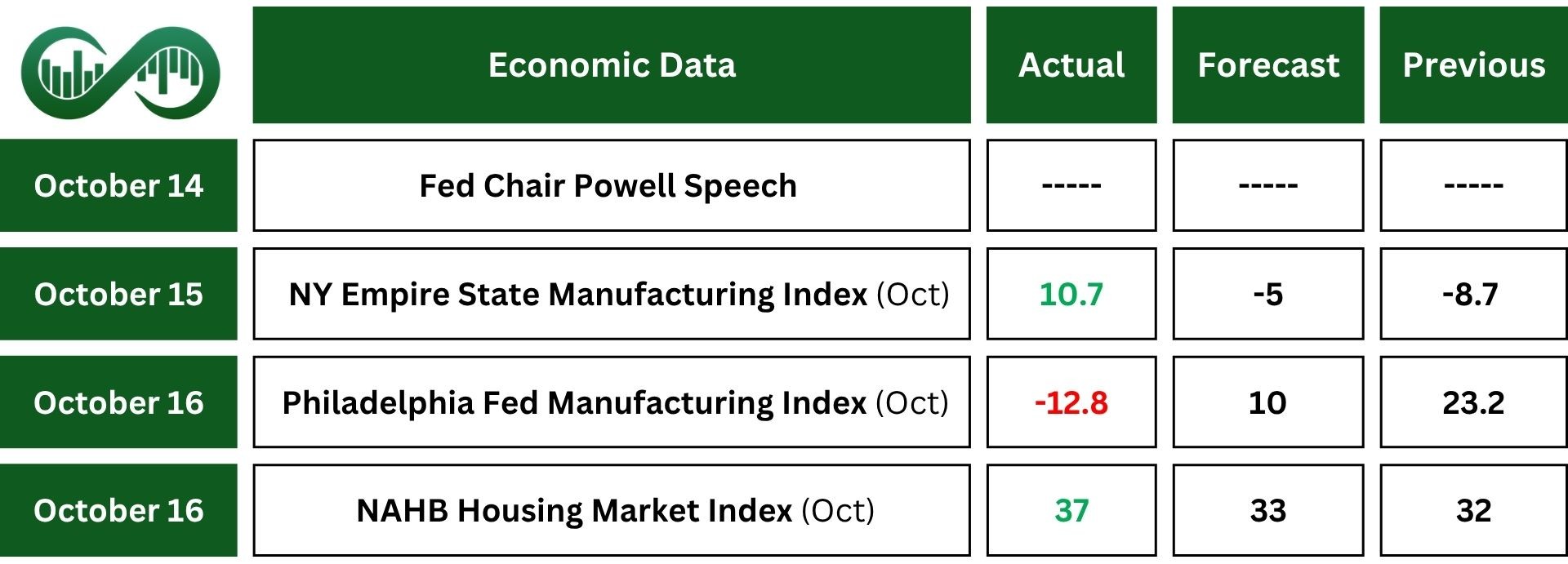

The Empire State Manufacturing Index rose to 10.7 in October, beating expectations and signaling modest business growth. New orders and shipments improved, while inventories stayed flat. Employment increased, though the average workweek shortened. Input costs and selling prices rose faster, and nearly half of surveyed firms expect better conditions ahead.

In contrast, the Philadelphia Fed Manufacturing Index dropped sharply to -12.8, its lowest since April, indicating contraction. Shipments declined but remained positive, and new orders rose modestly. Employment held steady, but price pressures intensified. Despite current weakness, firms anticipate growth over the next six months, especially in capital spending on equipment and software.

Earnings Reports

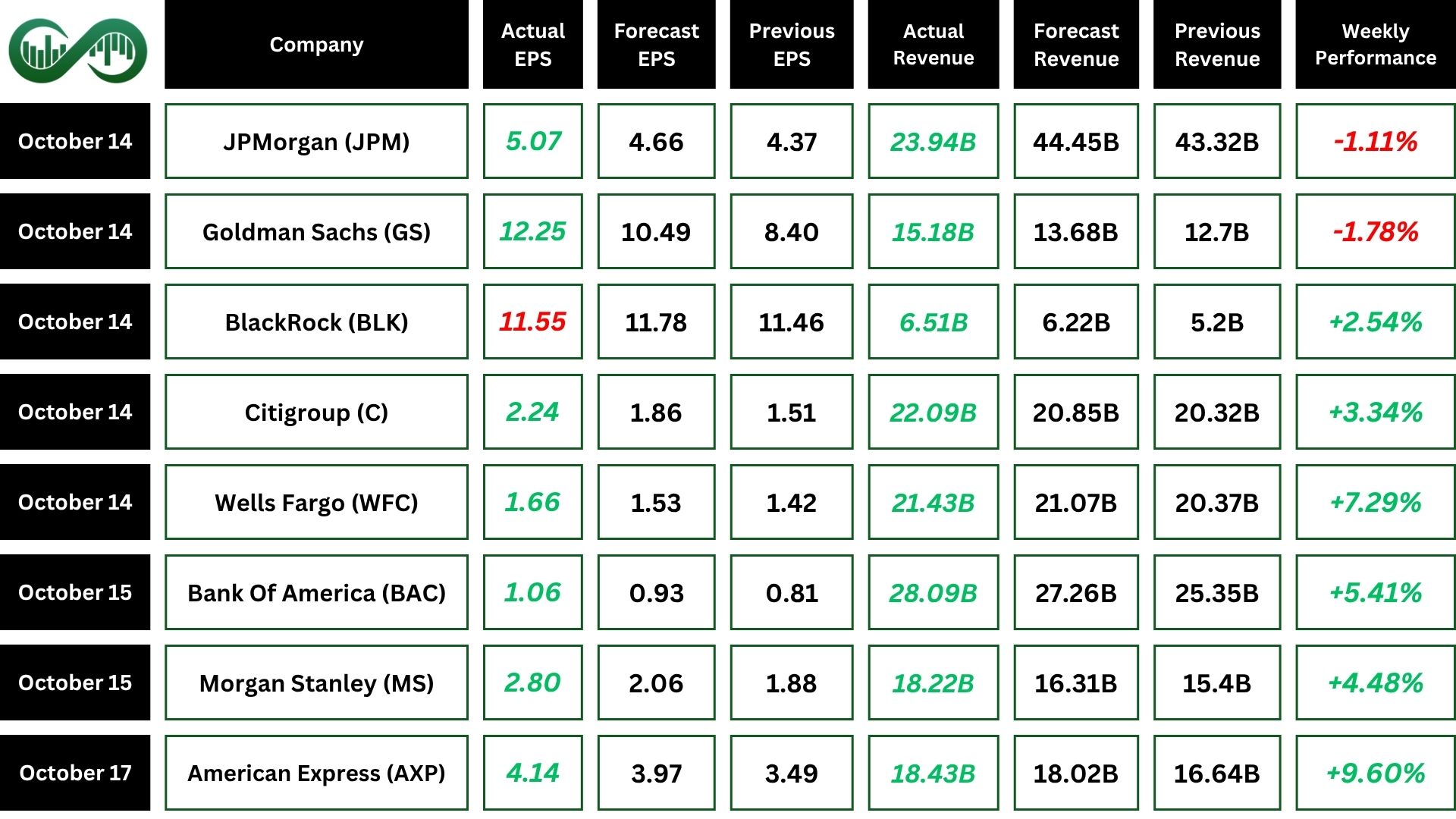

Wells Fargo

Wells Fargo (WFC) reported strong Q3 2025 results, with net income rising to $5.6 billion and earnings per share reaching $1.66, beating forecasts.

Revenue grew 5% year-over-year to $21.4 billion, driven by higher net interest and fee-based income. The bank saw growth in average loans and assets, while credit loss provisions declined due to improved credit performance. Consumer and corporate banking segments posted loan and deposit growth, though commercial banking revenue fell slightly.

Wells Fargo returned $6.1 billion to shareholders through buybacks and raised its dividend by 12.5%. Following the report, WFC shares surged over 7%, reflecting strong investor confidence.

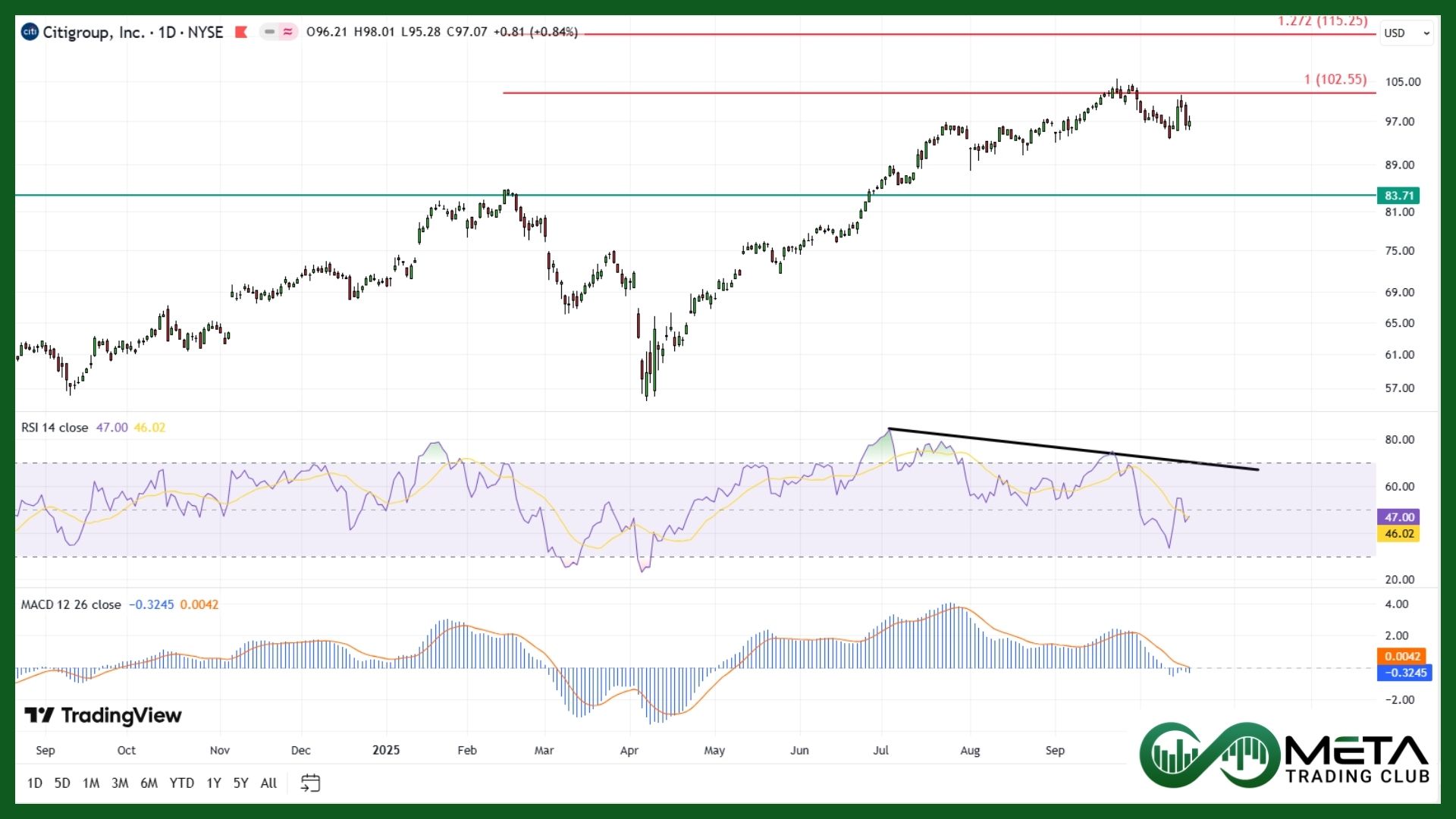

Citigroup

Citigroup (C) reported strong Q3 2025 results, with revenue rising 9% year-over-year to $22.1 billion and net income climbing to $3.8 billion, or $1.86 per share, both beating expectations.

Growth was driven by solid performance across all five core business segments and legacy franchises, along with a 12% increase in net interest income and lower credit costs.

Despite higher operating expenses and a one-time goodwill impairment, the bank showed operational momentum in Banking, Wealth, and Services. Following the report, Citi’s stock rose 3%, reflecting investor confidence in its strategic progress and earnings resilience.

BlackRock

BlackRock (BLK) reported strong Q3 2025 results, with assets under management reaching a record $13.46 trillion, up 17% year-over-year, and revenue rising 25% to $6.51 billion.

The firm posted $205 billion in net inflows, driven by high demand for iShares ETFs, private markets, and cash strategies. Adjusted operating income grew 23% to $2.62 billion, while adjusted net income rose 11% to $1.91 billion.

Despite a drop in GAAP earnings due to acquisition-related expenses, the completion of the HPS Investment Partners deal and $375 million in share buybacks boosted investor confidence. BlackRock shares rose over 2% following the report.

Bank of America

Bank of America (BAC) reported strong third-quarter 2025 results, with net income rising to $8.5 billion and earnings per share up 31% to $1.06, both beating expectations.

Revenue grew 11% year-over-year to $28.1 billion, driven by solid loan and deposit growth, a 9% increase in net interest income, and a 43% surge in investment banking fees.

All major business segments, including Consumer Banking, Global Wealth and Investment Management, and Global Markets, posted gains. The bank also returned $7.4 billion to shareholders through dividends and buybacks. Following the report, BAC stock rose 5%, reflecting strong investor confidence.

Morgan Stanley

Morgan Stanley (MS) delivered strong third-quarter results, with net revenues rising to a record $18.2 billion from $15.4 billion a year earlier and earnings per share climbing to $2.80 from $1.88.

Both figures beat expectations, and the firm posted a return on tangible common equity of 23.5%. Growth was driven by a 44% rebound in investment banking, a 35% surge in equity trading, and 13% gains in both wealth and investment management.

The firm also maintained solid operating efficiency with a 69% expense ratio and repurchased $1.1 billion in stock. Following the report, Morgan Stanley shares rose 4.5%, reflecting strong investor confidence.

American Express

American Express (AXP) reported strong fiscal Q3 2025 results, with revenue up 11% year-over-year to a record $18.4 billion and earnings per share rising 19% to $4.14, both beating expectations.

Growth was driven by a 9% increase in Card Member spending, strong demand for the refreshed U.S. Platinum Card, and higher net interest income. The company lowered its credit loss provisions and maintained a stable write-off rate, while expenses rose due to higher customer engagement costs.

Following the report, AXP shares rose 9.6% after report released and the company raised its full-year forecast for revenue and EPS.

Indices

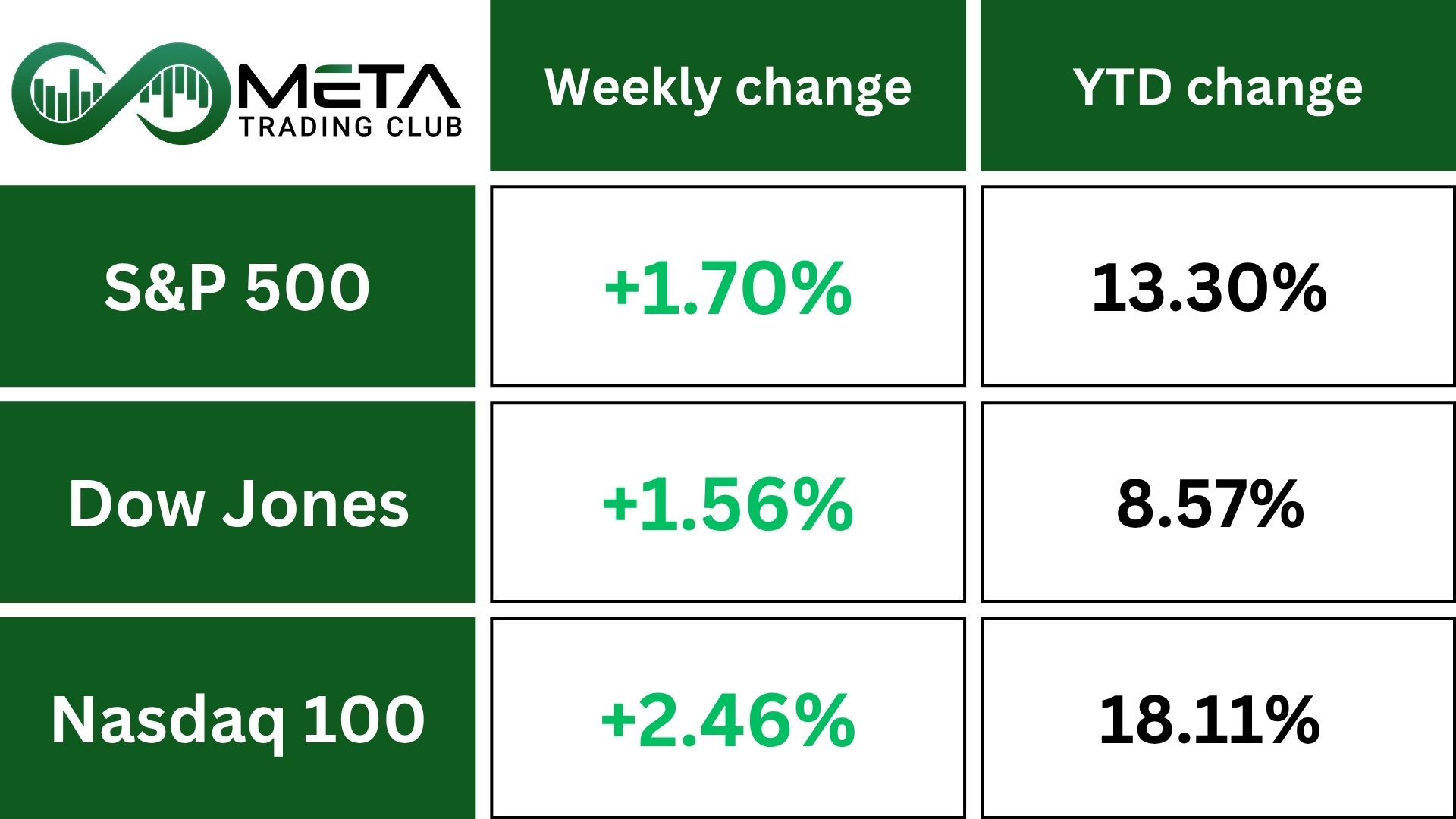

Indices’ Weekly Performance:

Main indexes moved higher during a volatile week as investors weighed President Trump’s latest comments on China and found temporary relief in corporate earnings.

Trump announced plans to meet Chinese President Xi Jinping in South Korea in two weeks and acknowledged that a 100% tariff on Chinese goods would not be sustainable.

The frequent shifts in messaging around trade and tariffs make it difficult for investors to gain clarity or confidence.

Stocks

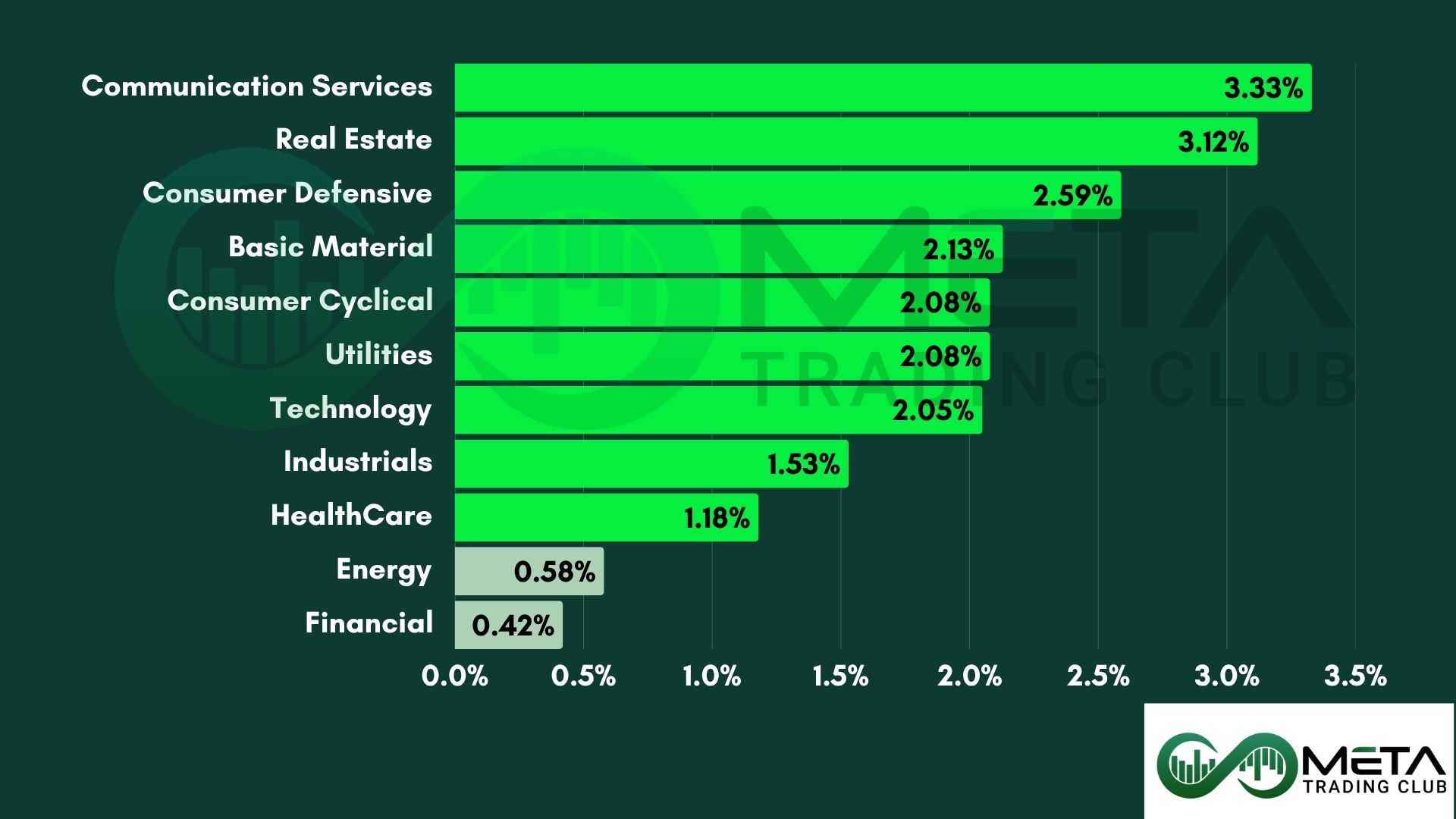

Sector’s Weekly Performance:

Sector performance surged last week, led by Communication Services, Real Estate, and Technology.

- Communication Services soared 3.33% as Google surged following a $15 billion investment in AI, fueling market optimism.

- Real Estate climbed 3.12% as Prologis jumped on better-than-expected Q3 earnings and raised full-year guidance.

- Basic Materials advanced 2.13% as Newmont Corporation rallied on gold’s record-breaking price surge.

- Consumer Cyclical gained 2.08% as Starbucks rose sharply, driven by seasonal product demand and renewed optimism about China expansion.

- Technology rose 2.05% as Broadcom surged after announcing a multi-billion dollar custom chip deal with OpenAI, reinforcing its leadership in AI infrastructure. AMD also jumped after securing a major GPU supply agreement with OpenAI.

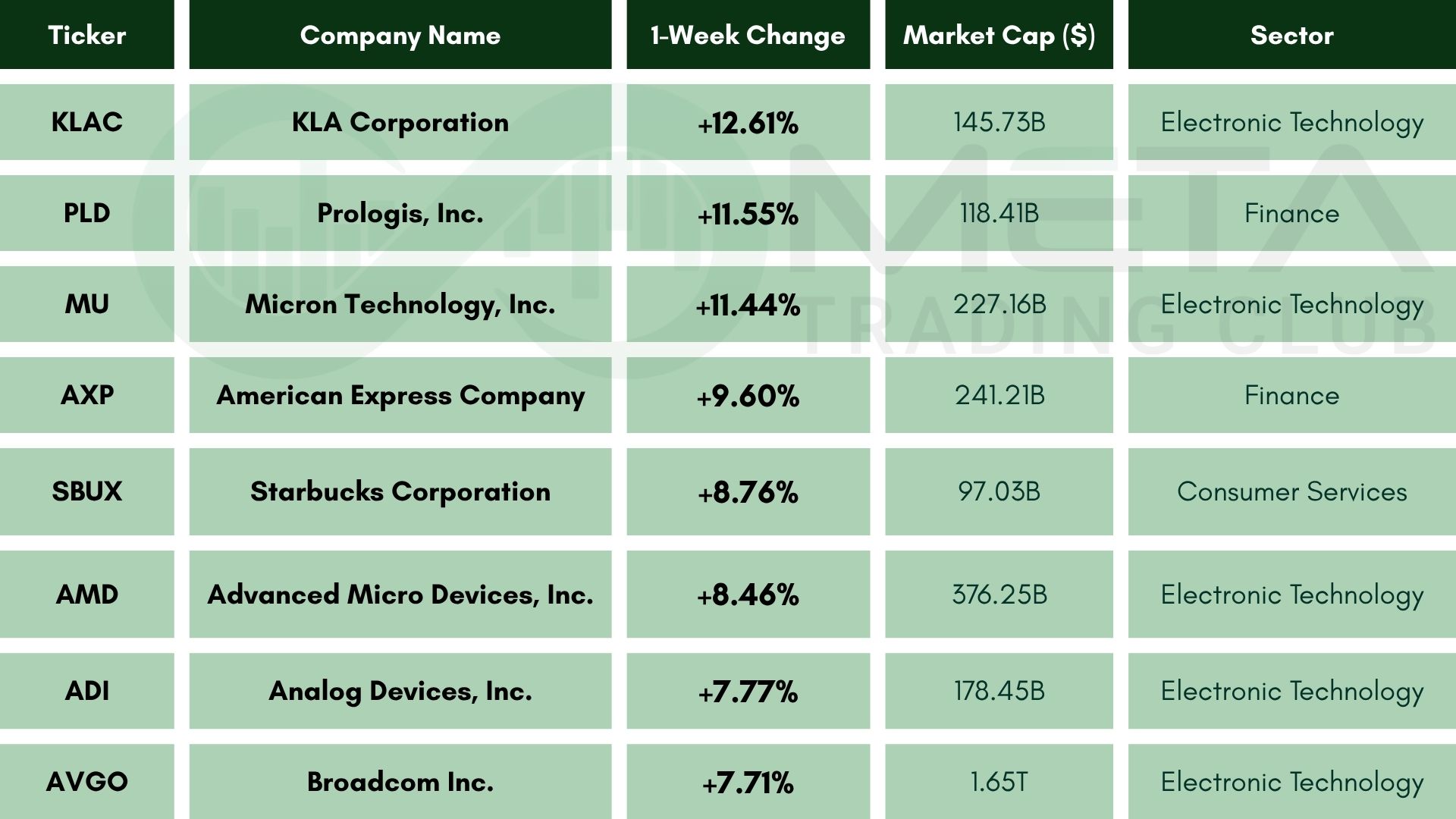

Top Performers

Last week saw a remarkable stock market performance, with several companies standing out as top gainers:

- KLA Corporation (KLAC): Advanced 12.6% from upgrades by banks, citing resilience in chip equipment and AI tailwinds. Price targets were raised significantly.

- Prologis (PLD): Surged 11.5% on strong Q3 earnings and raised full-year guidance. Its role in powering data centers for AI infrastructure boosted investor confidence.

- Micron Technology (MU): Soared 11.4% on strong Q4 results, rising profitability, and bullish forecasts for memory chips driven by AI demand. Citigroup raised its price target.

- American Express (AXP): Rose 9.6% due to reported record quarterly revenue and EPS, driven by affluent consumer spending and premium card growth. Also, the outlook was revised upward.

- Starbucks (SBUX): Gained 8.7% on seasonal product momentum (e.g., Pumpkin Spice Latte), strategic China partnerships, and analyst upgrades. Investor interest in Starbucks China also rose.

- Advanced Micro Devices (AMD): Jumped 8.5% after securing a major GPU supply deal with OpenAI, supporting 6 gigawatts of AI compute.

- Analog Devices (ADI): Climbed 7.7% due to delivering double-digit growth across segments in Q3, beating expectations.

- Broadcom (AVGO): Soared 7.7% after announcing a multi-billion dollar deal with OpenAI to supply custom ASICs for large language models.

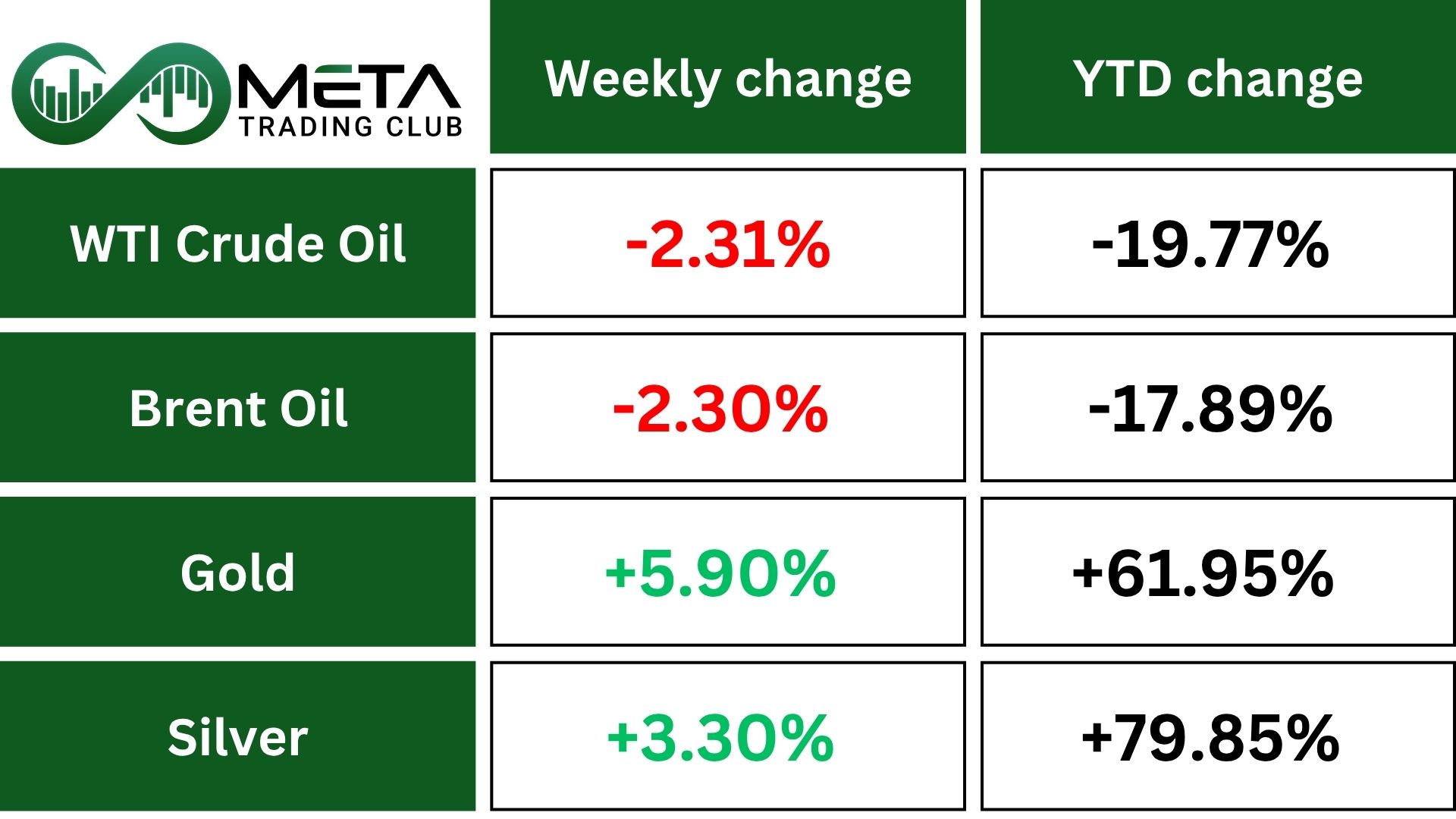

Commodity

Weekly Performance of Gold, Silver, WTI, and Brent Oil:

Gold ended the week with a gain of over 5%, hitting a record high above $4,300 per ounce before pulling back slightly. Gold made its best week in 5 years.

The major drivers are concerns over U.S. regional banks, global trade frictions, and expectations of further rate cuts

Gold prices are rising fast, bringing big gains to emerging markets and boosting investor confidence in gold-producing countries.

In South Africa, where the world’s deepest gold mines are located, mining stocks are having their best year in 20 years, with companies like Sibanye Stillwater, AngloGold Ashanti, and Gold Fields seeing their shares triple. Ghana, Africa’s top gold producer, just got a credit rating upgrade from Moody’s. Many emerging economies are also buying more gold, helping strengthen their national reserves.

Crude oil hovered near a five-month low of $57 per barrel on Friday, marking a third straight weekly decline, the longest losing streak since March.

The drop was driven by concerns over rising global supply, as President Trump’s upcoming meeting with Russian President Putin raised hopes for easing restrictions on Russian oil output.

Additionally, a 3.5-million-barrel increase in U.S. crude inventories and ongoing U.S.–China trade tensions fueled worries about weakening demand.

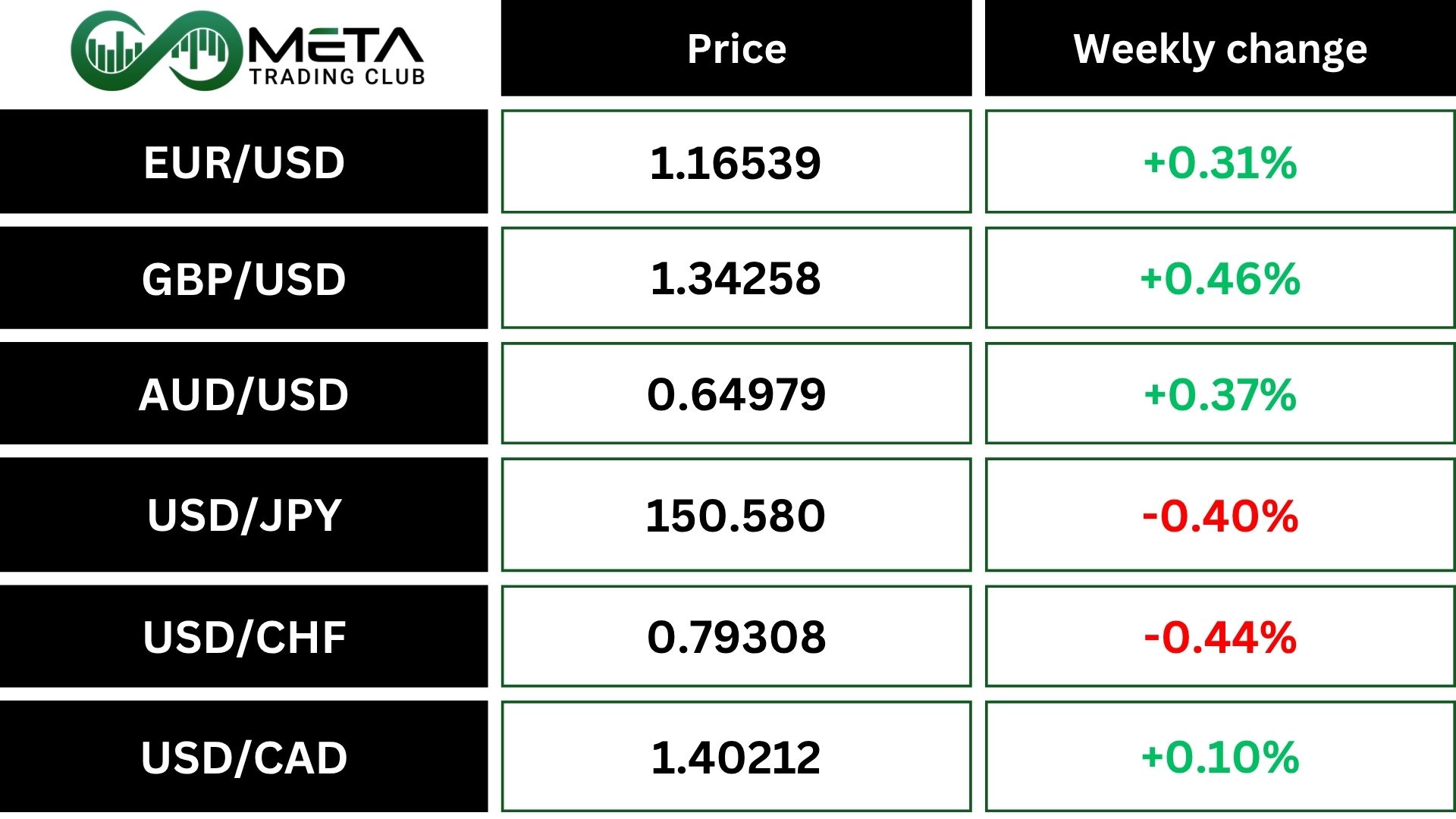

Forex

Weekly Performance of Major Foreign Exchange Pairs:

The U.S. dollar posted a weekly loss against the Swiss franc and Japanese yen, pressured by rising trade tensions and growing concerns over regional American banks.

The ongoing U.S. government shutdown, now in its third week, also weighed on sentiment by halting key economic data releases, leaving investors with limited visibility into the economy’s health.

President Trump acknowledged that his proposed 100% tariff on Chinese goods was unsustainable, but blamed Beijing for the latest breakdown in trade talks. He confirmed plans to meet Chinese President Xi Jinping in South Korea in two weeks, aiming to ease tensions.

The dollar index (DXY) slid 0.43% for the week. Meanwhile, the euro gained 0.17% to be on track for its strongest weekly performance against the dollar in nine weeks. Also, Sterling set for a weekly gain.

In Japan, speculation over a potential rate hike by the Bank of Japan added pressure to the dollar, while political uncertainty around the delayed prime minister vote kept the yen in focus.

Fed Governor Christopher Waller signaled support for another rate cut later this month, citing mixed signals from the labor market.

Crypto

Bitcoin climbed from low as investors feel more confident, hoping the U.S. and China will ease tensions.

Last week, President Trump said he plans to meet Chinese President Xi Jinping in South Korea in two weeks, after recently warning about new tariffs.

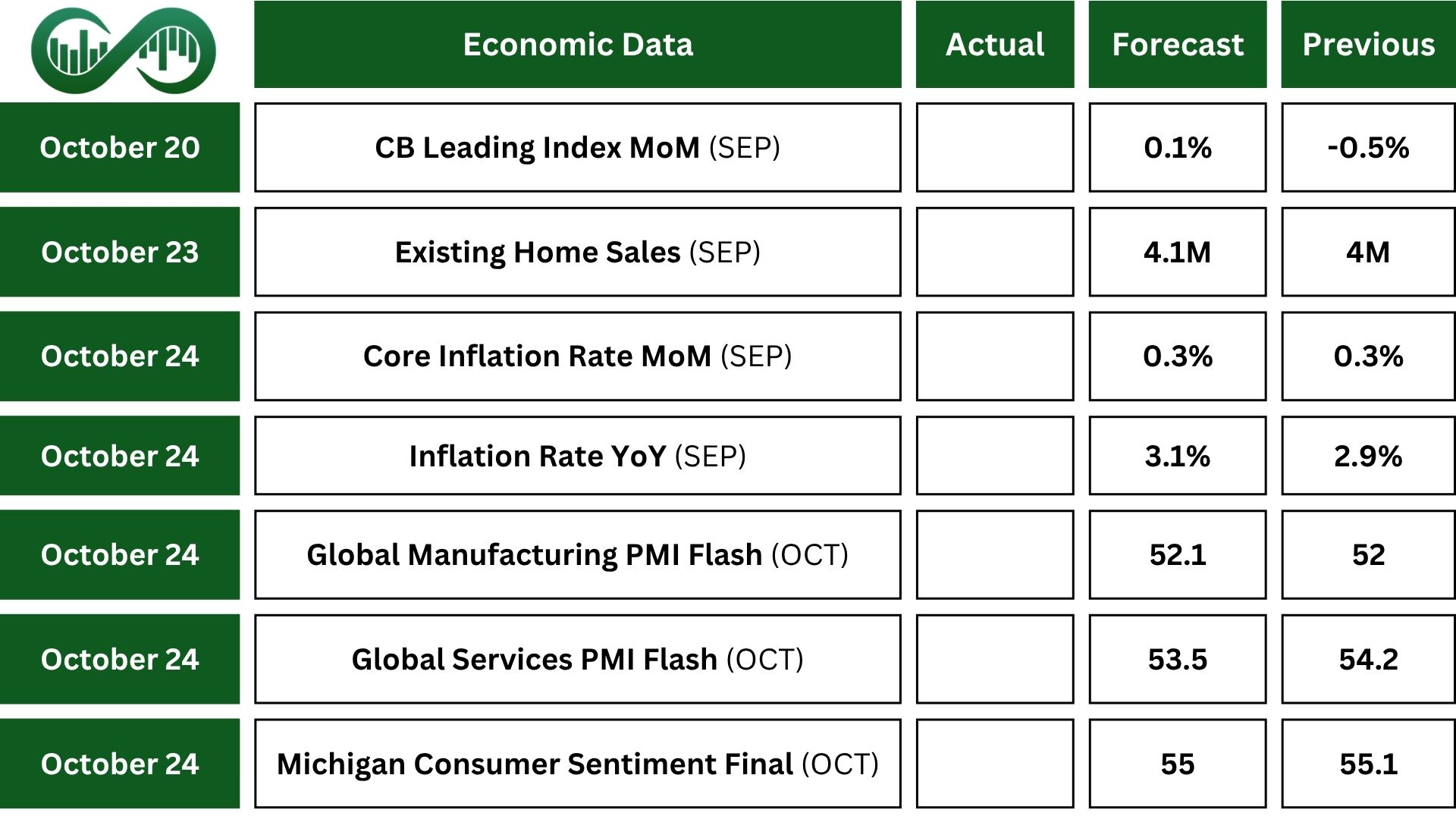

Next Week’s Outlook

Economic Events

Despite the ongoing U.S. government shutdown entering its fourth week, we will still get one key report this Friday, the Consumer Price Index (CPI). It’s the only major release from federal agencies since October 1st.

Inflation for September is expected to rise to 3.1%, the highest since May. Core inflation is likely to stay at 3.1%, with monthly figures holding steady at 0.4% for headline CPI and 0.3% for core.

This suggests tariff-related inflation remains under control. Investors will also watch other U.S. data like flash PMIs, home sales, and the Chicago Fed activity index.

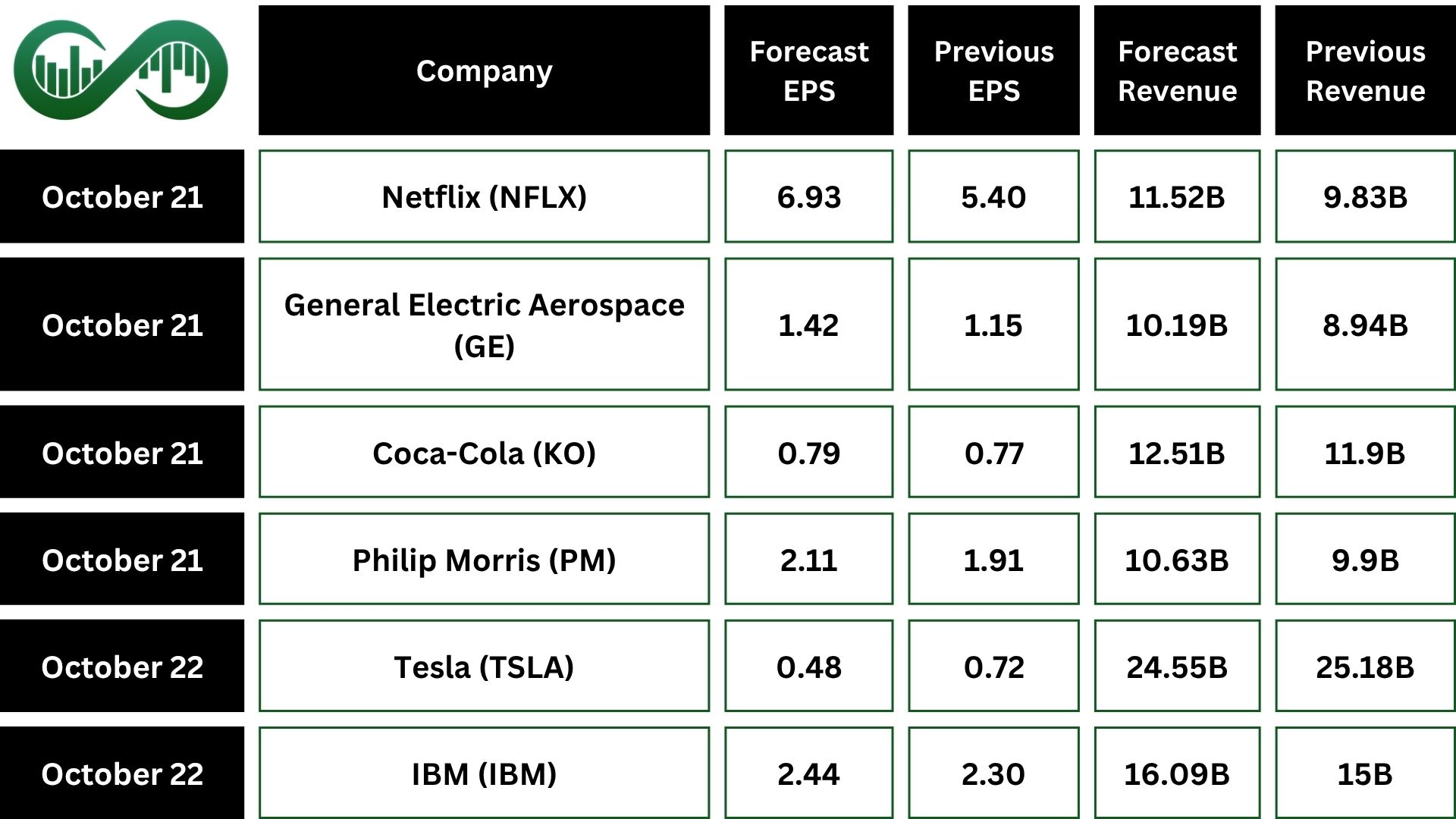

Earnings Events

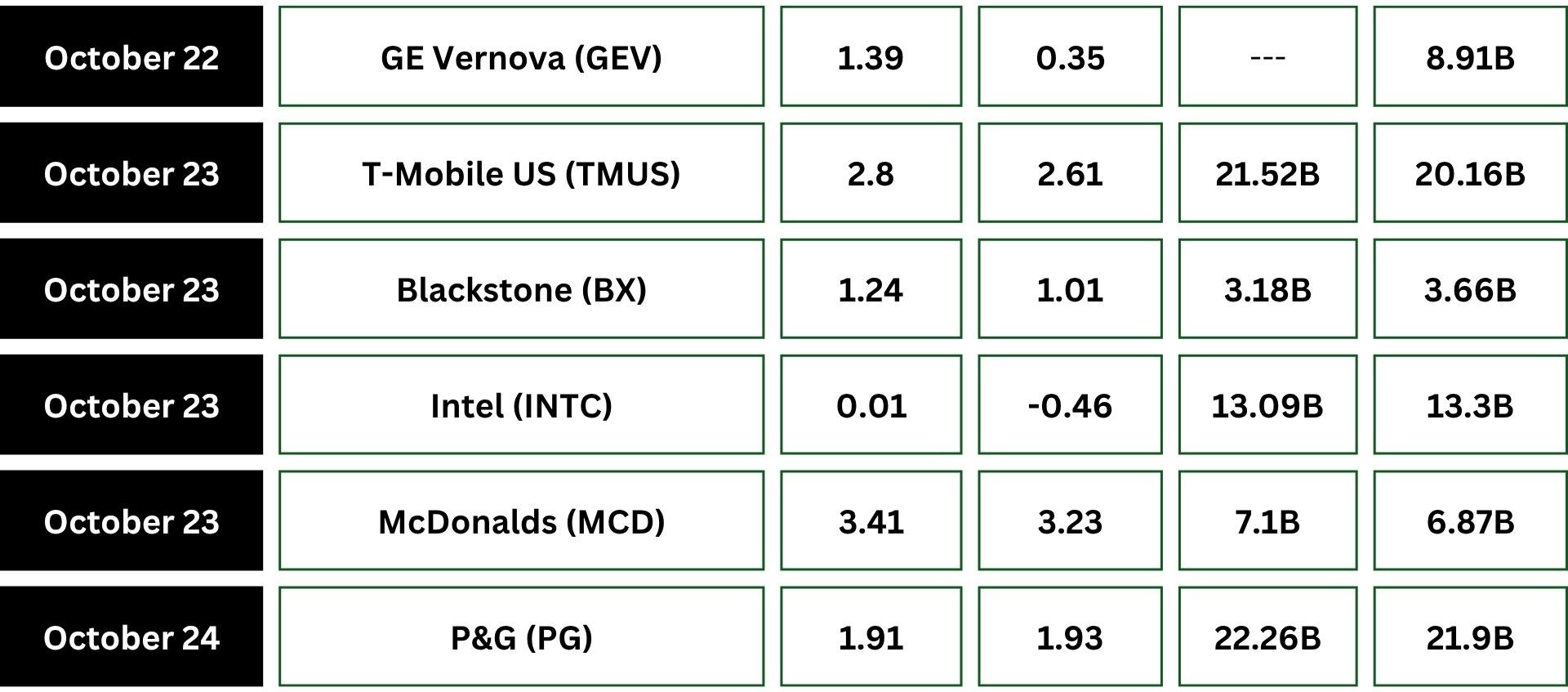

The Q3 earnings season is still going strong, with big names like Tesla (TSLA), Procter & Gamble (PG), GE (GE), Coca-Cola (KO), Netflix (NFLX), Intel (INTC), and Ford (F) set to release their results.

Other key reports are expected from IBM, AT&T, Blackstone, Thermo Fisher, Philip Morris, GE Aerospace, CME Group, and Intuitive Surgical.